1/30/23 Quick Summary

1/30/23 Quick Summary

If you're a new reader or maybe one who doesn’t make it to the end feel free to take a second to subscribe now. Sources are Argus and Bloomberg unless otherwise noted.

Subscribe for free to receive new posts and support my work.

Or invite others to check it out,

__________________________________________________________

Quick update on today’s action.

As noted in the weekend update (which is much more in depth than the quick summaries, I encourage you to check it out if you haven’t), as with last week there’s reasons to be bullish this week (technicals, breadth, systematic flows(?)), but also reasons to be bearish (remain mildly overbought conditions, technical resistance), and some wildcards (data, global events, Fedspeak, and earnings).

So, a very busy week. Catch your breath on Monday because starting Tuesday between earnings and data it’s a firehose. So while I could point to positive technicals, breadth, seasonality, and/or institutional flows as conducive to the rally continuing, I think this week will be more about the fundamentals (earnings, economic data, and the Powell’s press conference). If those items continue to broadly cooperate (earnings come in “better than feared”, economic data supports a continued slowing in inflation and the economy without it (the economy) falling into more than a potential mild recession, and the Fed continues to stick to their current messaging (going a little over 5% and holding for 2023)) we could see this rally continue much further than people expect. If you remember, I noted at the beginning of the year, “the consensus for 2023 is a poor first half with a better second half. Makes me think it’s unlikely that’s what we get.” In that regard I think most were not expecting a 10% up January (Doug Kass, Ed Yardeni, and Charlie McElligott are three who did call for it), so it’s likely many are already offsides (the flows out of US equities this month support that). That makes further gains even more “painful” for those out of position which could create a late “scramble in” to the rally. But, again, that requires the fundamentals to cooperate.

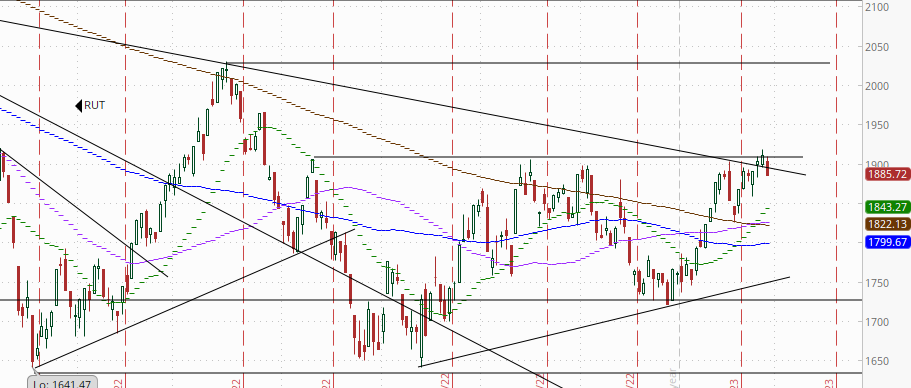

And ahead of all of that, and after the big runup the past few weeks, I guess it’s not a big surprise that traders took risk off the table Monday. An unexpected jump in inflation in Spain and a weaker than expected GDP reading from Germany (i.e., stagflationary data) didn’t help, nor did both yields and the dollar gaining Monday. The damage wasn’t severe by any measure, just taking the SPX back down to Thursday’s lows and keeping it above support, but it does evidence a bit of a risk off mindset ahead of the data this week, and it sets up 4100 on the SPX as more significant resistance. It also did take the Nasdaq back under its 200-DMA and the RUT below 19100 (below). Daily technicals on all of those indices though remain in ok shape for now.

Dollar

10-year yield

SPX

Argus:

This busy week for the stock market got started on a downbeat note as investors took some money off the table following a strong showing this month. Entering today, the Nasdaq and S&P 500 were up 11.0% and 6.0%, respectively, so far in January. The main indices spent most of the session on a steady decline, ultimately settling near their worst levels of the day.

Investors took a more cautious approach today in front of policy decisions from the Fed, the ECB, and the Bank of England later this week. The skittishness around the FOMC decision largely relates to Fed Chair Powell's press conference and the possibility that Mr. Powell will make a concerted effort on Wednesday to rein in the market's enthusiasm by tamping down its optimism over any potential rate cuts this year. On a related note, Nick Timiraos of The Wall Street Journal wrote over the weekend that Fed officials are concerned that inflation could reaccelerate due to tight labor markets. Mr. Timiraos added in a Monday article that the Fed's interest rate strategy could depend on how much members believe the economy will slow.

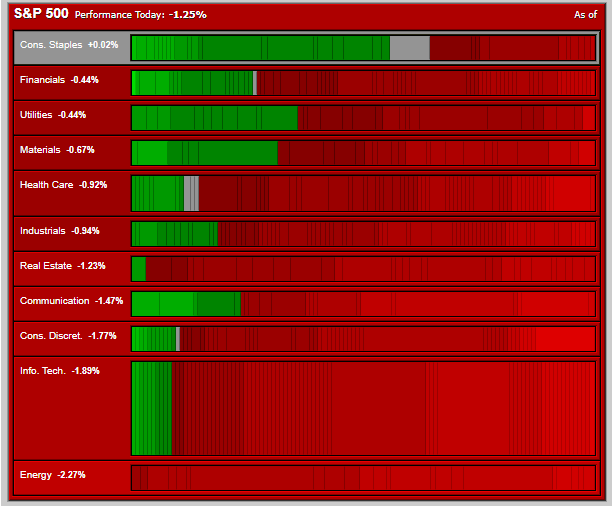

Also upcoming are several market-moving data releases, including the Q4 Employment Cost Index, the January ISM releases, and the January Employment Situation Report. In addition, more than 100 S&P 500 companies will be reporting earnings this week, headlined by Meta Platforms (META 147.06, -4.68, -3.1%), Apple (AAPL 143.00, -2.93, -2.0%), Alphabet (GOOG 97.95, -2.76, -2.7%), and Amazon.com (AMZN 100.55, -1.69, -1.7%). Mega cap stocks had been leading the January charge, but trailed the broader market today as they succumbed to profit-taking interest. The Vanguard Mega Cap Growth ETF (MGK) closed down 1.9% versus a 1.1% loss in the Invesco S&P 500 Equal Weight ETF (RSP) and a 1.3% loss in the S&P 500. Downside leadership from the mega cap space was evident in S&P 500 sector performance. The information technology (-1.9%), communication services (-1.8%), and consumer discretionary (-1.7%) sectors were among the worst performers today. Energy (-2.3%) was the top laggard for the 11 sectors as oil prices faded ahead of the OPEC+ meeting later this week. WTI crude oil futures fell 1.9% to $77.94/bbl. Only one sector -- consumer staples (+0.1%) -- was able to maintain a slim gain by the close.

Caterpilllar (CAT), Exxon Mobil (XOM), General Motors (GM), Marathon Petroleum (MPC), McDonald's (MCD), Pfizer (PFE), Phillips 66 (PSX), PulteGroup (PHM), Spotify (SPOT), Sysco (SYY), and UPS (UPS) are among the notable companies reporting earnings ahead of tomorrow's open.

Looking ahead to Tuesday, market participants will receive the following economic data:

8:30 a.m. ET:

- January Chicago PMI (Briefing.com consensus 45.4; prior 44.9)

- Q4 Employment Cost Index (Briefing.com consensus 1.1%; prior 1.2%)

9:00 a.m. ET:

- November FHFA Housing Price Index (prior 0.0%), November S&P Case-Shiller Home Price Index (Briefing.com consensus 6.8%; prior 8.6%)

10:00 a.m. ET:

- December Consumer Confidence (Briefing.com consensus 108.1; prior 108.3)

Bloomberg:

US stocks declined on Monday as investors turned cautious going into an eventful week that includes the Federal Reserve’s rate decision and a slew of big-tech earnings. The Nasdaq 100 suffered its worst day since Dec. 22 while the S&P 500 fell the most since Jan. 18. Declines in Apple Inc. and Microsoft Corp. weighed on both the indexes as investors await earnings from companies including Alphabet Inc. and Meta Platforms Inc. this week. Treasuries pared earlier declines, with the benchmark 10-year rate ending around 3.54%. A dollar index rose. Oil fell to its lowest in almost three weeks.

The Fed is widely expected to raise rates by a quarter percentage point on Wednesday, slowing its pace for a second straight session. But traders will be watching for the tone officials set for future meetings. Fed Chair Jerome Powell has continued to push back against traders anticipating rate cuts later this year, emphasizing that he won’t budge until inflation has eased meaningfully. Stocks have still rallied in January, with investors seemingly brushing off Powell’s “higher-for-longer” warning. “Investors seem to have forgotten the cardinal rule of ‘Don’t Fight the Fed.’ Perhaps this week will serve as a reminder,” a team of Morgan Stanley strategists led by Michael Wilson wrote in a note. Investors adding to the rally in stocks this month will be disappointed if they’re in direct defiance of the Fed, the strategists said. Citi Global Wealth’s Kristen Bitterly echoed this, saying that January’s rally was technical as it was largely driven by 2022’s “laggards and losers.”

Traders are also awaiting the US jobs report later this week. A less tight labor market is a key goal for the Fed. Investors have also been parsing a slew of earnings reports, with more to come throughout the week. Signs of earnings pressure have been raising concerns about the health of the economy and the outlook for equities. After the closing bell, NXP Semiconductors NV offered a revenue forecast for the first quarter that missed the average analyst estimate. Whirlpool Corp., meanwhile, said it expects a decline in sales this year.

“The week ahead will not only be a Fed story, as Friday’s employment situation report will provide clarity on the strength of the labor market to start the new year,” wrote Ben Jeffery and Ian Lyngen of BMO Capital Markets.

The European Central Bank and the Bank of England are also each projected to hike by half a percentage point when they deliver decisions a day after the Fed.

A very weak SPX sector flag with ten of eleven sectors down at least four tenths with seven down at least nine tenths. Growth, which had outperformed for most of January, were the weakest outside of energy which had also had a very strong January to date. Every energy stock in the SPX fell today. That fell to support, but any further declines likely signal a longer consolidation for that sector.

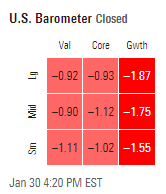

The Morningstar style box also weaker with every style down at least nine tenths. Growth the big underperformer here as well.

Breadth was also weak. 26% of volume was positive on the NYSE, while the Nasdaq had 29%. Issues were 31 and 31%. Breadth has by and large been very good all of January outside of one or two days here and there, so we’ll see if this is just one of those temporary breathers.

Overseas, major equity indices in the Asia-Pacific region began the week on a mixed note. Japan's Nikkei: +0.2%, Hong Kong's Hang Seng: -2.7%, China's Shanghai Composite: +0.1%, India's Sensex: +0.3%, South Korea's Kospi: -1.4%, Australia's ASX All Ordinaries: -0.1%.

I had noted in the weekend update that a cooling off of the Chinese share rally was not unlikely, and after jumping higher at the open, China's Shanghai Composite followed its week-long closure with a daylong pullback from opening highs to end little changed. Hong Kong, which had rallied the end of last week, fell -2.7%. Indian shares underperformed as the rout in Adani Group stocks swelled to $71 billion amid a fight with short seller Hindenburg Research.

China's Ministry of Culture and Tourism reported that domestic trips were up 23% yr/yr during the past week, but down 11.4 % from the 2019 level.

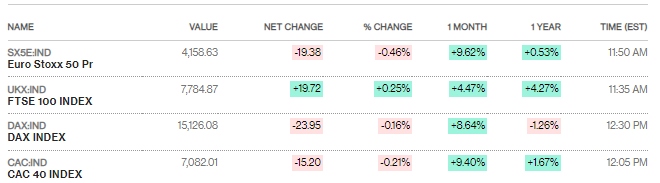

Major European indices mostly fell modestly with the UK’s FTSE 100 bucking the trend.

The Stoxx Europe 600 index dropped, taking some of the luster off what was shaping to be the biggest January gain on record, after data showed a surprise contraction of the German economy in the fourth quarter and a surprise jump in Spanish inflation. Technology stocks led the decline as Prosus NV slumped more than 5% after a rout in Hong Kong’s tech sector. European bonds fell, with yields on benchmark German securities up six basis points, after Spanish inflation unexpectedly quickened, prompting traders to boost bets on how high the the European Central Bank will raise interest rates. The euro gained.

Germany’s economy shrank 0.2% in the final quarter of last year — a worse outcome than previously flagged and one that makes a recession on the back of rising energy bills more likely after all. The figures Monday from the statistics office contrast with an estimate this month for output to have stagnated in the fourth quarter. They also mean a contraction in the period through March would still produce a technical recession in the euro area’s largest economy. Demand is weighed down as surging prices continue to filter through to consumers. “We expect more of the same for early 2023, namely a modest decline in real GDP reflecting mostly lower consumption,” said Salomon Fiedler, an economist at Berenberg. “Following the mild winter recession, the economy is likely to stabilize in spring and start to expand significantly again in mid-2023.” There was some good news elsewhere. Belgium managed to eke out growth of 0.1% and Latvia grew 0.3%, while euro-area economic confidence rose for a third month in January, climbing to the highest level since June. But Germany’s outsized manufacturing sector, while underpinned by a large backlog and an easing of supply bottlenecks, is seeing orders fall.

Spanish inflation unexpectedly quickened in January after a five-month run of slowing price growth, prompting traders to boost their bets on how high the European Central Bank will raise interest rates. Consumer prices advanced by 5.8% from a year ago, up from the previous month’s 5.5% increase, the statistics institute in Madrid said Monday. That’s well above the 4.8% median estimate in a Bloomberg survey of economists, though the predictions ranged from 3.8% to 6.5%. The task of forecasters was complicated this month by a re-weighting of the euro-zone inflation basket. Money markets amped up ECB rate-hike wagers by as much as 9 basis points on Monday, pricing the deposit rate to peak above 3.50% by the middle of the year, up from 2% now. Euro-area bonds sold off, lifting Spanish bond yields about 8 basis points across the curve. Yields on German 10-year debt, the benchmark for the region, were up as much as 8 basis points to 2.32%, the highest since Jan. 6. “The higher core inflation is a concern,” said Antoine Bouvet, a rates strategist at ING Bank NV. “That selloff shows that markets are biased toward lower inflation and that release is catching them offside.” Spain’s acceleration was driven by a rebound in fuel costs and smaller discounts in start-of-year apparel sales. A gauge of underlying prices that excludes volatile items surged to a record 7.5%, suggesting price pressures are still widespread. “ The surprise jump in Spain’s headline EU Harmonized inflation at the start of the year suggests the fall in price growth won’t be as fast as we expected. The economy posted a mild GDP gain in the last quarter of 2022, and we expect it to grow again in the first quarter, helped by lower inflation. The risk is that cost pressure proves stickier than we forecast.” —Ana Andrade, Bloomberg economist.

UK-listed companies issued 305 profit warnings last year, 50% more than in the previous year, as an increasing number of businesses struggled with higher costs, according to a report by consultancy firm EY-Parthenon. Almost 18% of the UK’s 1,193 listed businesses issued a profit warning. That’s a similar proportion as during the global financial crisis in 2008, according to the report. Retailers and travel and leisure were the FTSE industries that posted more warnings. While the pain was most acute in consumer-facing sectors, in the last quarter stress deepened and spread into other areas of the economy, such as industrial sectors, according to Jo Robinson, head of EY-Parthenon’s Turnaround and Restructuring Strategy in the UK and Ireland.

The gloom shrouding the UK economy is beginning to lift, despite more signs that activity declined at the start of 2023, surveys Monday showed. Growing hopes of a brighter economic outlook and cooling price pressures boosted business confidence to a six-month high in January, according Lloyds Banking Group Plc’s monthly business barometer. Lloyds said confidence rose by five points to 22%, with firms’ expectations for their own prices moderating from the record high hit in December. Confidence indicators have been sending conflicting messages over the state of the economy, though, as forecasters warn that the UK is likely heading into recession in the first half of 2023. That picture was reinforced by a separate survey by the Confederation of British Industry, which showed private-sector activity fell over the winter due to a cocktail of headwinds, including strikes, staff shortages and the cost-of-living crisis.

Its business volumes indicator slumped from -1 to -13 in the three months to January amid further weakness in services.

In other markets:

The dollar was up slightly for a third day, starting to look like it wants to bottom. As I noted last week, the daily technicals are showing signs of turning more supportive. It’s coming up on a key trendline if it can continue moving sideways. A lot of resistance above though.

The VIX did jump higher back above 20, but remains under the downtrend line dating back to October. A break of that and the 50-DMA (at 21.25 would say to me we’re going to see mid-20’s soon.

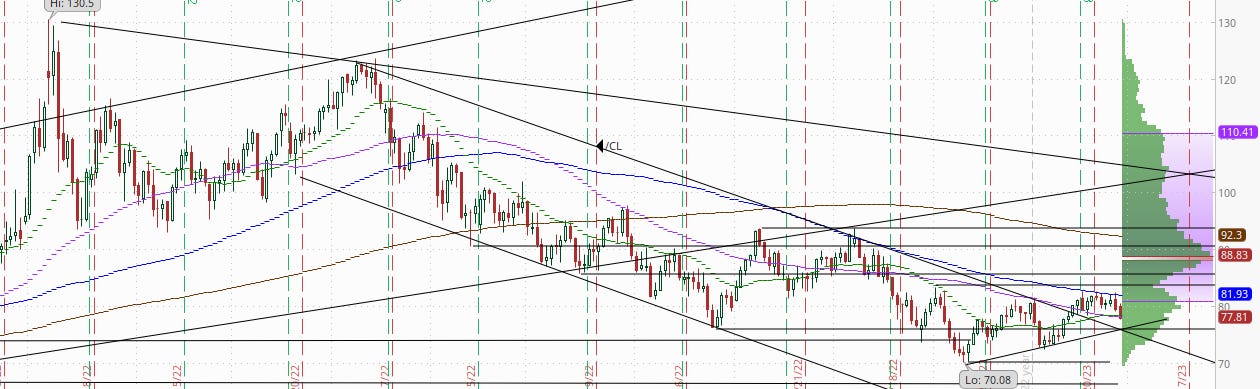

WTI - After spending the past week pushing against its 100-DMA, WTI gave up today and fell back towards the uptrend line which I thought was likely before the rally a week ago. I had been bullish on WTI moving through the 100-DMA after that rally given the technicals, but after it struggled with that resistance I noted the end of last week “I’m starting to wonder if it will get through as I had been more confident about earlier in the week. The 100-DMA is proving very difficult to crack.” Now it appears that the more likely path is a test of support. Also the technicals are weakening so we’ll see if that support holds. Not helping things today were rumors that Saudi Aramco will lower crude prices to Asia for a fourth straight month.

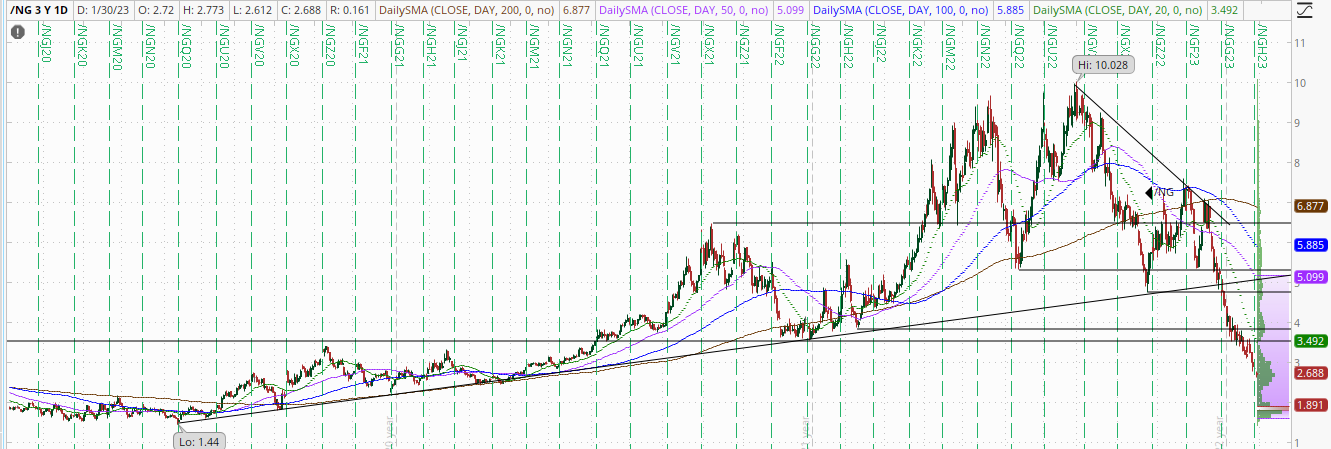

On nat gas, as a reminder after breaking my “must hold” level two weeks ago I said “it will bounce somewhere, but where is the question.” Since then I have thought if it can just stabilize a few days we could see it move higher, but so far it hasn’t been ale to do that. As I said last week the fact that it couldn’t bounce despite a letter Thursday by the Federal Energy Regulatory Commission authorizing Freeport LNG to resume some activities before a full reopening and a larger than expected storage draw spoke volumes, as did the fact that the key March/April spread - essentially a bet on how tight supplies will be at winter’s end — had reversed to a discount. Fell another -5.7% today to new 20-month lows. That said, there do appear to be some indications of downside exhaustion so I think a bounce is coming. Below is a 3-year chart.

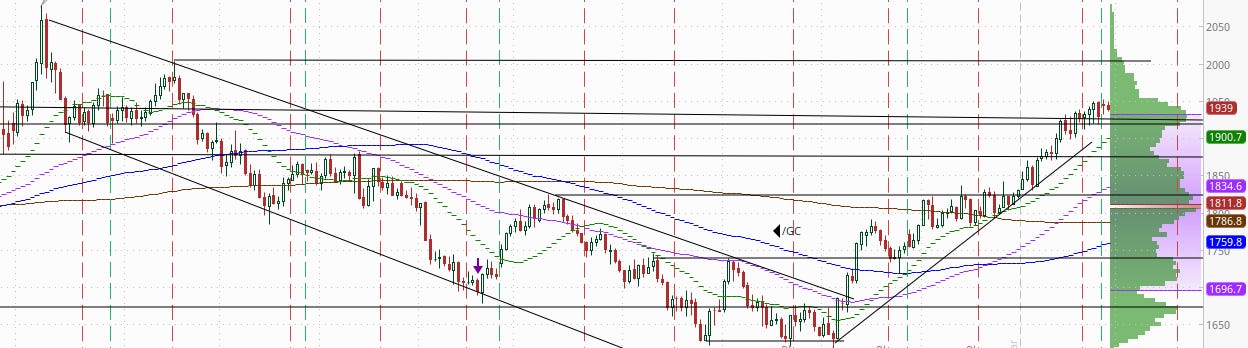

And on gold as a reminder I have been calling for a consolidation for a couple of weeks, but since we turned the calendar into 2023, it has not taken more than a couple of days off in between gains. I noted Friday it had been two days so normally we would see a jump Monday, but we didn’t. This might indicate a longer consolidation at this $1950 level. Technicals here are also indicating a consolidation is likely.

So traders didn’t feel like pushing things further, and I can’t say that I blame them. Regardless, starting tomorrow it will be all about the data, with tomorrow’s key report the Employment Cost Index pre-market. That is the Fed’s favorite measure of wage inflation. A very hot number will likely see this pullback continue. A cool number and we could rally, but I’m not necessarily expecting it with the Fed up the very next day.

Reports today:

Note: I’ve try to do a quick-take on Twitter on the bigger economic reports when they’re released if you don’t follow me there currently (link is at the bottom of this summary).

To subscribe to these summaries, click below.

To invite others to check it out,

To see more content, including summaries of most major U.S. economic reports and my morning and nightly updates go to Neil’s Newsletter Substack for newer posts or https://sethiassociates.blogspot.com for the full history. You can also follow me on Twitter at @NeilKSethi