CPI - June 2026

June CPI much cooler than expected w/biggest drops in headline and core since April 2020 on broad based softening in price pressures. Real average weekly earnings rise most since then as well.

US CPI (M/M) Jun: -0.4% (est -0.1%; prev +0.5%)

- CPI (Y/Y): +3.5% (est +3.8%; prev +4.2%)

- Core CPI (M/M): 0.0% (est +0.2%; prev +0.2%)

- Core CPI (Y/Y): +2.6% (est +2.8%; prev +2.9%)

US CPI Supercore (M/M) Jun: -0.20% (prev +0.27%)

- CPI Supercore (Y/Y): +3.17% (prev +3.67%)

Executive Summary

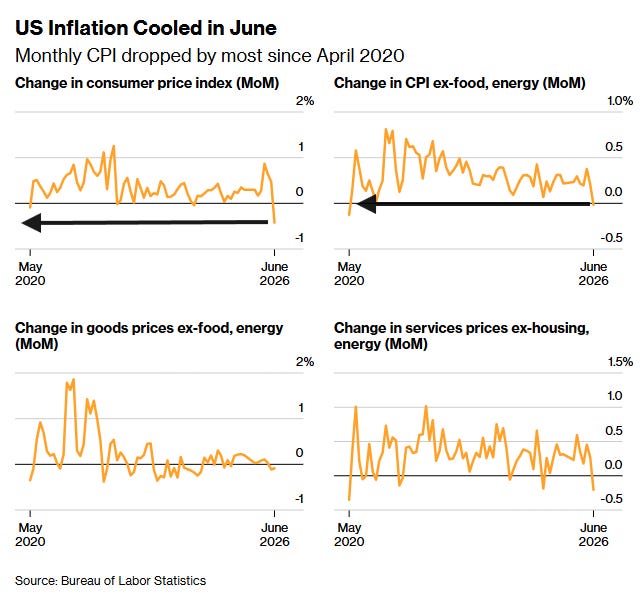

US June headline CPI -0.4% (-0.42%), its largest monthly decline since April 2020 on the back of falling energy prices and broad core disinflation dragging the y/y rate down to +3.5% (+3.53%) from +4.2% — the first sub-4% reading since March and well below the -0.1% expected.

Energy tumbled -5.7% (its largest drop since April 2020) and was the single biggest contributor to the decline, with gasoline -9.7%.

Core CPI though also declined -0.02% — the first monthly decrease in core since May 2020 — well below the +0.2% expected with core y/y easing to +2.6% (+2.59%) from +2.9%, on broad-based declines across motor vehicle insurance, communication, apparel, medical care, and used cars.

Core Goods deflated for a second month (-0.09%), and core Services rose just +0.03%, the least since September 2021, helped by shelter slowing to +0.12% — its smallest monthly gain since January 2021.

Supercore (core services ex-housing) fell -0.20%, its biggest monthly decline since May 2020, with the y/y rate down to +3.17% from +3.67%.

The read-through to households was very positive: real average weekly earnings jumped +0.77% m/m — outside the April 2020 COVID spike, the strongest since January 2016 — and turned positive y/y at +0.36% (from -0.42%).

Rate-hike odds slumped: pricing for a July hike fell from roughly 40% to 15% after the print.