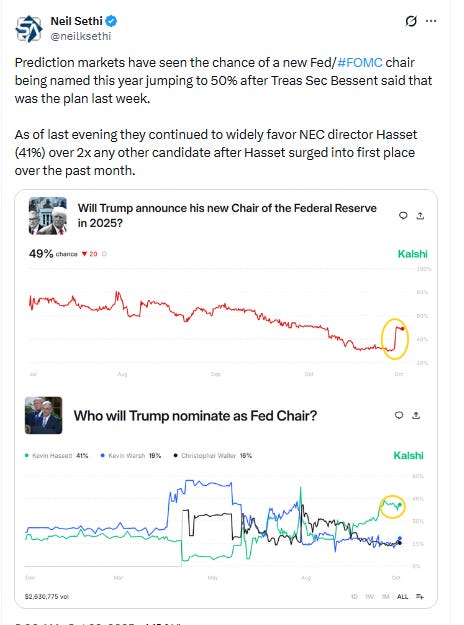

Markets Update - 10/29/25

Update on US equity and bond markets, US economic reports, the Fed, and select commodities with charts!

To subscribe to these summaries, click below (it’s free!).

To invite others to check it out (sharing is caring!),

Link to posts - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog. Also please note that I do often add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

Finally, if you see an error (a chart or text wasn’t updated, etc.), PLEASE put a note in the comments section so I can fix it.

Major US equity indices started the session trading mildly higher boosted by continued gains in the largest stocks and as they awaited the Fed decision and Powell press conference as well as Alphabet, Meta and Microsoft earnings after the close (more on those below). Nvidia shares were up more than 3% in the premarket, and the chipmaker hit a market capitalization of $5 trillion during the session. Investors were also encouraged by the continued warming of ties between the US and trade partners, notably China, who reportedly made their first purchase of soybeans this year after President Trump indicated the removal of the fentanyl tariffs on China may be removed tomorrow. The US also signed trade deals with South Korea and Japan this week.

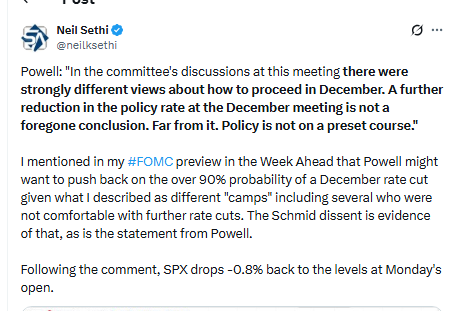

The indices were trading modestly higher with very little volatility even through the mostly as expected Fed decision/statement release, but dropped sharply when Powell in the press conference went out of his way to emphasize that a December rate cut was “far from” certain (“A further reduction in the policy rate at the December meeting is not a foregone conclusion. Far from it,” he said (and he reiterated it in another answer later)). Following that equities dropped sharply, recovered some of that drop, then fell again post-press conference, bounced again, but all but the Nasdaq ended lower than where they started, with just the Nasdaq in the green supported by those megacap stocks which did the heavy lifting for a fourth session.

Elsewhere, Treasury yields jumped on the hawkish cut, as did the dollar. Gold continued its recent correction, and bitcoin also was lower. Copper was higher as was natgas after a roll to the December contract (more on that below). Crude was little changed.

The market-cap weighted S&P 500 (SPX) was unch, the equal weighted S&P 500 index (SPXEW) -1.1%, Nasdaq Composite +0.6% (and the top 100 Nasdaq stocks (NDX) +0.4%), the SOXX semiconductor index +1.9%, and the Russell 2000 (RUT) -0.9%.

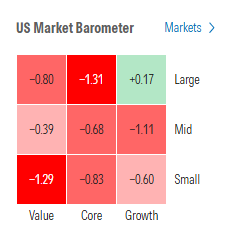

Morningstar style box for a third day showed losses across all styles except large cap growth which held up the indices.

Market commentary:

“Powell is reflecting the tension on the Fed between those who favor more aggressive easing and those who are concerned that inflation remains too high, even as the labor market weakens,” said Michael Rosen, chief investment officer at Angeles Investments. “Our view has been that the market has been too aggressive in pricing in the pace and magnitude of future cuts. Inflation is elevated above the Fed’s target, and we see monetary policy as moderately loose, with nominal rates below nominal GDP growth.”

“Given these dissents on both sides, it might be difficult to put a down payment on December,” said Neil Dutta at Renaissance Macro Research.

“Powell gave investors a peak behind the curtain showing markets that there is no forgone agreeable path when it comes to the committee voters,” said Jay Woods at Freedom Capital Markets. “Their goal to satisfy their dual mandate remains tricky and could prove quite delicate going forward.”

The knee-jerk reaction is a great example of the market being forward-looking because the immediate news – a rate cut and the end of quantitative tightening – are both positives for stocks and bonds, according to Chris Zaccarelli at Northlight Asset Management. “However, markets already expected this and were negatively surprised that future cuts might be taken off the table,” he said.

Zaccarelli thinks this will prove to be a buying opportunity because the Fed is likely to continue to support both stock and bond markets by cutting rates significantly over the next 12 months. That’s even if officials do keep rates unchanged in December.

“At a time when it’s flying with only one eye open, the Fed decided that the softening in the labor market is a bigger concern than the stickiness of inflation,” said Jack McIntyre at Brandywine Global. “What makes less sense is the odd range of dissents. This divergence means less complacency in financial markets, more volatility, and more two-way flows.

To Bret Kenwell at eToro, the biggest question now is: which side of the dual mandate will the Fed focus on — the weakening labor market or persistent inflation? Inflation could very well keep the Fed from moving as quickly or aggressively as they’d like to head off further weakness in the labor market, but that task becomes even more difficult without key economic updates, he said. “If a December rate cut is ‘far from’ a foregone conclusion as Chair Powell stated, will that have investors hitting the brakes on the market’s recent run? Earnings will play a large role over the next several days, but we could see some profit taking after a powerful run,” Kenwell noted. As long as earnings growth remains strong and the consumer remains resilient, pullbacks could lead to a compelling buying opportunity, he says. “That’s as the shallow, short-lived dips over the last few months have left plenty of cash-heavy investors on the sideline waiting for a more enticing buying opportunity to emerge,” he concluded.

“The story of AI is still intact,” said Anthi Tsouvali, a multi-asset strategist at UBS Global Wealth Management. “The fact that the Fed is cutting rates — and we do expect that the Fed will cut another 25 points — is very good for the economy. It’s easing financial conditions, boosting growth.”

“From an investment standpoint, while the narrative for US equities remains ‘bullish with conviction,’ sustaining this uptrend will require patience and disciplined risk management,” wrote Linh Tran, market analyst at XS.com. “Monetary policy decisions, trade developments, and corporate earnings are set to become the key catalysts driving the next phase of the market.”

The warming relationship was a key driver in the market on Tuesday, according to Thierry Wizman, global FX & rates strategist at Macquarie Group.

“The market is seeing President Trump re-engaging with the rest of the world again (i.e., China and Japan), and this is a good thing, insofar as it may temper his desire for more tariffs,” Wizman said. “The prospect of seeing very high tariffs, especially on China, have diminished. To some extent, this also plays to the prospect that the Fed will be dovish too, given there is a connection between lower tariffs and lower inflation.”

“This week’s big tech earnings may be the most important in recent memory since many investors are skeptical about the stock market’s rally,” said David Laut at Kerux Financial. “Big tech earnings will provide clarity and data that investors can use to determine if the past few week’s of gains are justified.”

“I anticipate that we’re going to continue to see enthusiasm as we go through this week,” Lauren Goodwin, chief market strategist at New York Life Investments, told CNBC’s “Closing Bell” on Tuesday. She added, “I think through the end of the year we’re free and clear.”

“Technical tailwinds continue, including breadth, momentum, and seasonality, while fundamental indicators, such as consumer spending, economic growth and earnings expectations, are an increasing driver for markets,” said Mark Hackett, chief market strategist at Nationwide. “This combination, along with the support from fiscal and monetary stimulus, provides a healthy backdrop for equities.”

A slew of recent tech headlines suggests AI demand is in a strong spot and should continue supporting U.S. stocks for the near-term and beyond, according to UBS. Moreover, markets’ widely held expectation of an imminent rate cut, as well as upcoming earnings, should be a boon for risk assets, the firm said. “A definite timing on the end of quantitative tightening should support risk sentiment,” Ulrike Hoffmann-Burchardi, Americas chief investment officer Americas and global head of equities at UBS, wrote in a Wednesday note to clients. “Rising adoption and integration of AI tools should continue to boost demand for computational resources, underpinning strong AI capex. Third- quarter results from big tech companies in the next two days should offer further insights into the spending and monetization trend. We maintain our conviction that AI-related stocks should drive further equity performance in the months and years ahead.”

“There are two important tailwinds behind the equity market here,” said Paul Eitelman, global chief investment strategist at Seattle-based Russell Investments, which had about $369 billion in assets under management as of Sept. 30. “We continue to see a solid or strong earnings season,” he said via phone on Wednesday. Blended earnings growth for the S&P 500, which reflects both consensus estimates and actual numbers that have been reported, are just above 10% versus a year ago, Eitelman added. Meanwhile, expectations are that U.S. President Donald Trump and China President Xi Jinping, who are scheduled to meet on Thursday, are “moving toward a potential deal,’‘ he said. Along with this, an anticipated trade pact between the U.S. and South Korea was helping to reduce uncertainty over the U.S. economic outlook.

“The market isn’t cheap,” said Robert Pavlik, senior portfolio manager at Dakota Wealth Management. “The valuation concerns are still there.” But positive tones ahead of Trump’s meeting with Beijing’s top leader Xi Jinping later this week have been easing some trade jitters about the latest U.S. threats of potentially more tariffs against its crucial trade partner, he said. Furthermore, another rate cut on Wednesday could help push borrowing costs lower, Pavlik told MarketWatch. “Does the economy need a rate cut? I don’t think it does now,” he said. “But it might later on to keep things moving forward.”

While the upward momentum in large-cap technology and growth continues, the diverging breadth and underperformance in small- and mid-cap stocks raise some concerns, according to Craig Johnson at Piper Sandler.

“Investors must remain vigilant within the current uptrend, especially as volatility will likely increase with earnings results and Fed commentary,” he said.

“When we look at this setup against overbought chart conditions which extend across multiple time frames, it continues to imply the potential for elevated volatility into year-end 2025,” said Dan Wantrobski at Janney Montgomery Scott. While Wantrobski is still looking for the S&P 500 to hit the 7,000 mark this year - with an intermediate-term target toward 7,400 - he notes that markets are still vulnerable to “air pockets, some of which could prove pretty nasty.” “We think November may be a target, despite its reputation as one of the best months for stocks,” he said.

Link to posts - Neil Sethi (@neilksethi) / X for more details/access to charts.

In individual stock action:

Megacap technology name Nvidia clung to gains Wednesday, advancing 3.1%. The artificial intelligence chip darling’s market capitalization had rocketed up above $5 trillion in the session, the first time a U.S. company reached such a valuation. The stock notched a five-day winning streak as well. The move comes just a day after the company announced an array of new deals, especially one that involves the chip giant taking a $1 billion stake in Finnish networking company Nokia.

Stocks that stand to lose from higher rates led the rollover in the market. Consumer stocks like Costco and McDonald’s declined. Visa and Mastercard also fell.

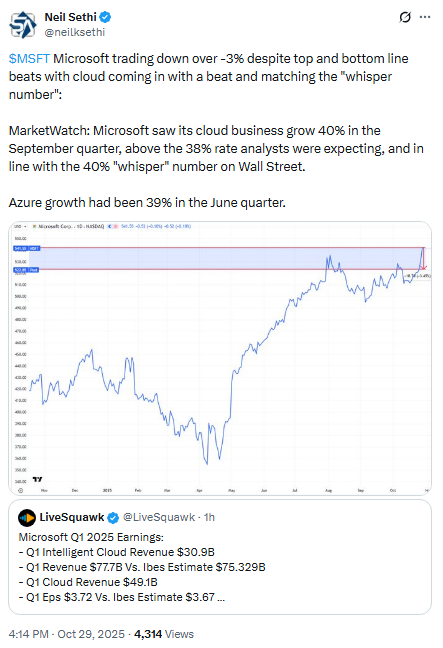

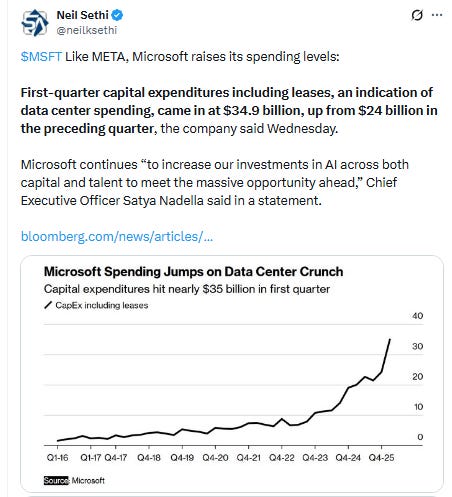

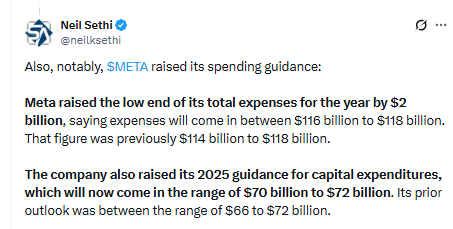

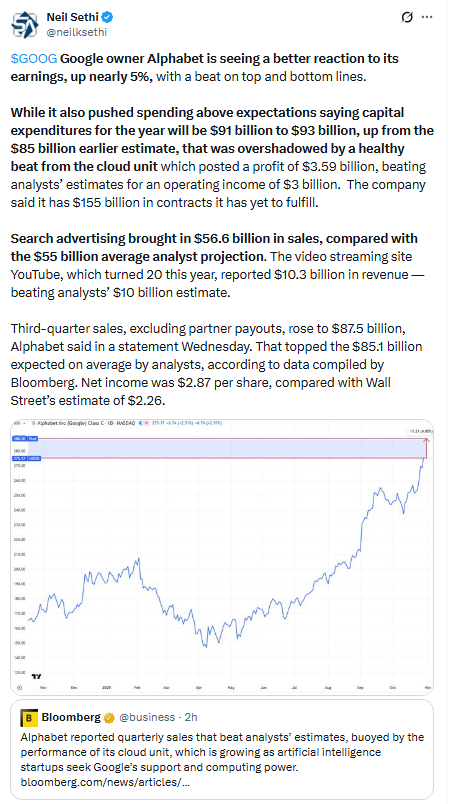

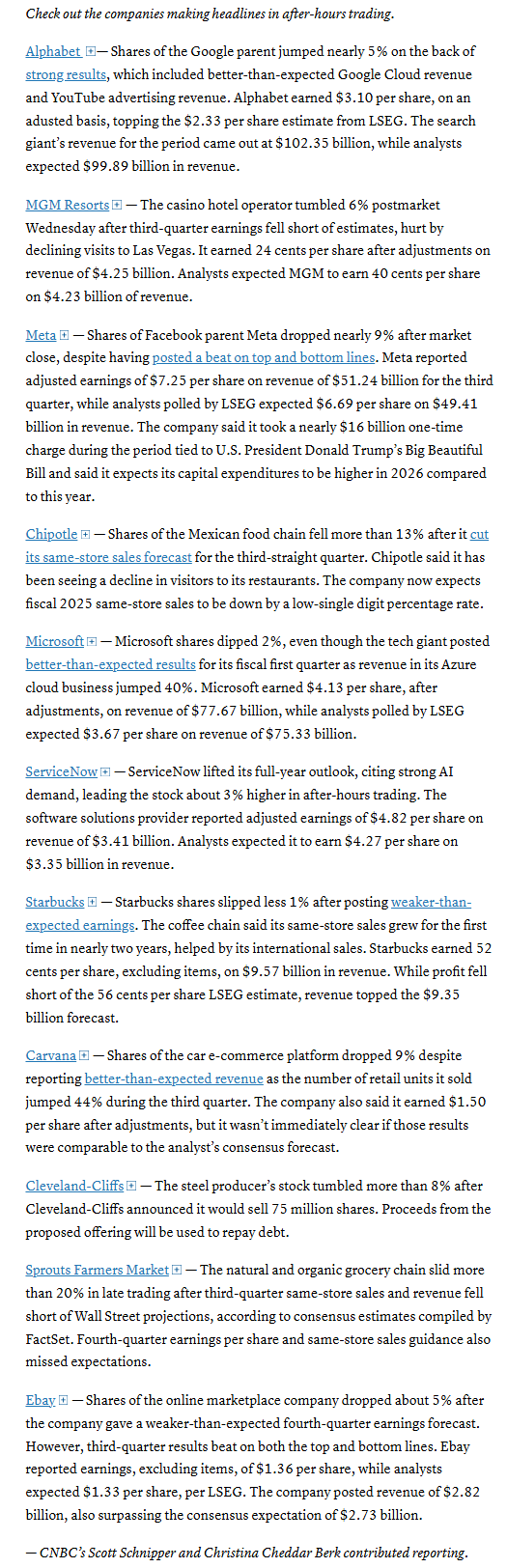

After the bell, Alphabet Inc. reported solid sales. Meta Platforms Inc. sees total expenses to significantly rise in 2026. Microsoft Corp.’s expansion in its Azure unit failed to inspire traders.

Corporate Highlights from BBG:

EBay Inc. gave a profit forecast for the fourth quarter that missed the average analyst estimate, stoking investor concerns about narrowing margins heading into the holiday shopping season.

Starbucks Corp. posted positive same-store sales growth for the first time in over a year, an early sign the coffee chain’s turnaround efforts are gaining traction.

Chipotle Mexican Grill Inc. cut its full-year projection for a third time this year, as diners pulled back from eating out amid heightened economic pressure.

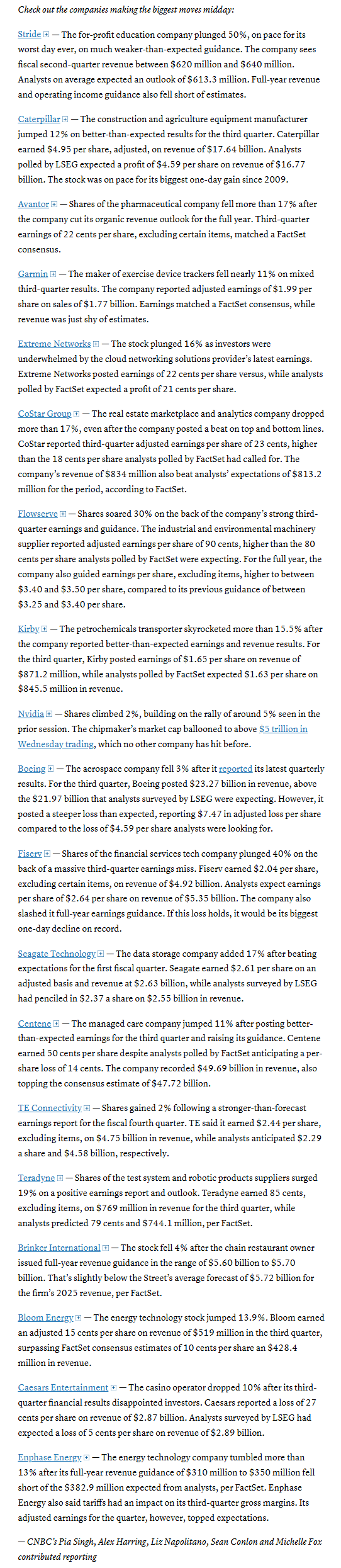

Caterpillar Inc. posted stronger-than-expected earnings and revenue on the back of surging demand from AI data centers for its power-generation equipment.

Boeing Co. announced a $4.9 billion accounting charge and delayed debut for its 777X jetliner, a reminder of the long recovery ahead for the US planemaker even as rising aircraft deliveries bolster its cash.

Boeing is laying plans to push production of its 787 Dreamliner to new heights, testing its ability to clear an inventory of parked planes and the strength of its strapped supply chain.

Kraft Heinz Co. lowered its sales outlook as its chief executive officer said that the feeling of US shoppers has fallen to historic a low.

Verizon Communications Inc. reported a loss in wireless phone subscribers in the third quarter as a new chief executive officer laid out an aggressive growth strategy to reclaim market share.

CVS Health Corp. raised its 2025 profit guidance for a third time in less than six months, a sign that it’s set a new foundation a year into Chief Executive Officer David Joyner’s tenure following challenges in its insurance business.

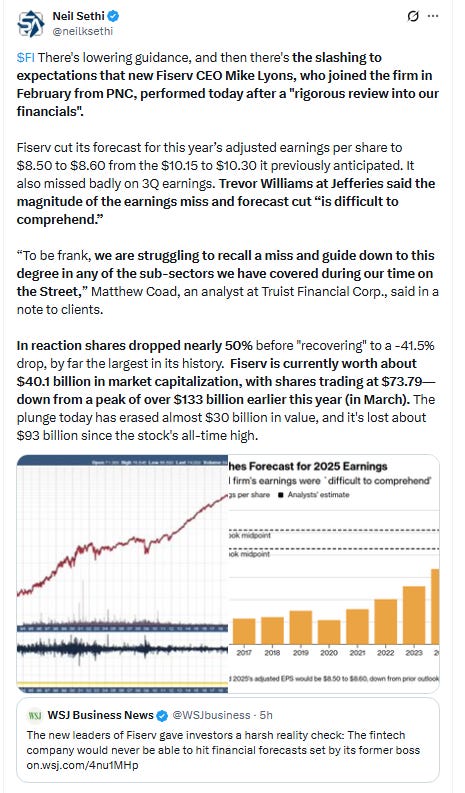

Fiserv Inc. plunged after the fintech slashed its outlook for full-year earnings and unveiled third-quarter results that confounded Wall Street analysts.

Paramount Skydance Corp. began a planned round of job cuts involving 1,000 workers on Wednesday as part of an effort to slash $2 billion in costs following its August merger with Skydance Media. More cuts are expected at a later date.

Centene Corp.’s third-quarter profit surpassed Wall Street expectations and the health insurer raised its outlook, a potential sign of relief for investors after the company’s profit view collapsed earlier this year.

Caesars Entertainment Inc., a major operator of resort casinos, reported third-quarter results that fell short of Wall Street estimates.

Edison International’s executives said the company’s equipment will likely be found to be associated with triggering the deadly Eaton Fire in Los Angeles.

Uber Technologies Inc. is preparing to offer driverless rides on vehicles developed by Lucid Group Inc. and Nuro Inc. in the San Francisco Bay Area for the first time next year, thrusting the company into direct competition with Waymo’s robotaxi service.

Thermo Fisher Scientific Inc. agreed to acquire Clario Holdings Inc., a privately held maker of drug trial software, for about $8.9 billion in cash.

Online marketplace Etsy Inc. will elevate Chief Growth Officer Kruti Patel Goyal to the CEO job, entrusting the company veteran with navigating the artificial intelligence era and lifting the marketplace out of a post-pandemic slowdown.

Airbus SE is keeping its ambitious jet delivery target, setting the company up for a furious production pace to close out the year, after reporting strong quarterly earnings on the back of the defense and space unit.

UBS Group AG results failed to dispel investor anxiety about risks from previously canceled Credit Suisse bonds, the potential impact of Swiss capital reforms and the lender’s involvement in the First Brands bankruptcy, overshadowing a set of earnings that broadly beat expectations.

Deutsche Bank AG exceeded analyst estimates for fixed-income trading, giving tailwind to Chief Executive Officer Christian Sewing just a couple of weeks before he presents a new strategy.

Banco Santander SA posted third-quarter results that beat analysts’ estimates as profit jumped in the US and provisions for souring loans remained contained.

GSK Plc raised its profit and sales forecasts for the year, aided by its HIV and immunology medicines, in Emma Walmsley’s last report as chief executive officer.

Mercedes-Benz Group AG confirmed its annual outlook and plans to proceed with a €2 billion ($2.3 billion) share buyback after the company’s automaking margin climbed in the third quarter.

SK Hynix Inc. reported a 62% jump in profit and revealed it’s sold its entire memory chip lineup for next year, illustrating how a global AI infrastructure buildout is ratcheting up sector-wide demand.

Indonesia’s GoTo Group raised its earnings forecast for the year, a sign that new initiatives and cost cuts to cope with fierce competition in the ride-hailing and delivery market are paying off.

CNBC stocks making the biggest moves after hours:

Mid-day movers from CNBC:

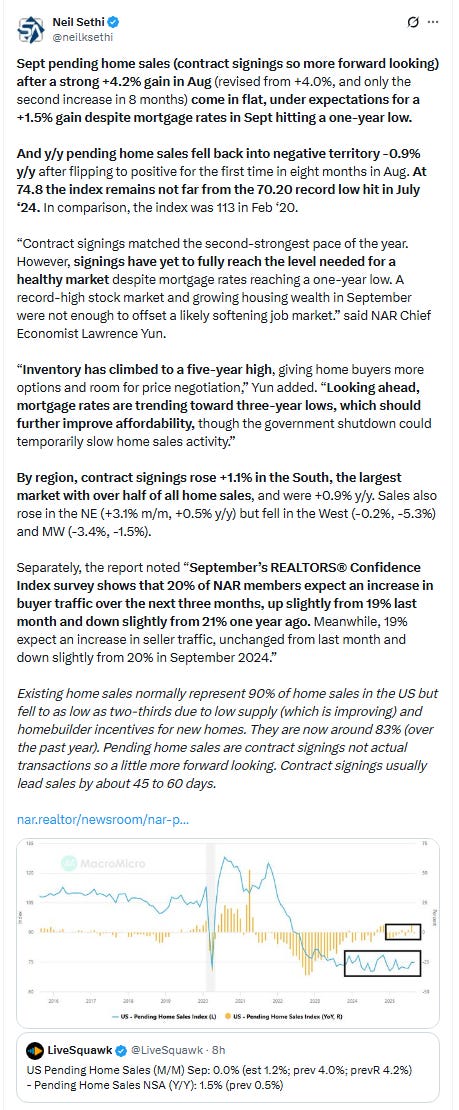

In US economic data:

Link to posts for more details/access to charts (all free) - Neil Sethi (@neilksethi) / X

The SPX recovered from its minor dip remaining at all-time highs. As noted Fri the daily MACD moved to “go long” positioning, and the RSI is over 50 and has almost eliminated its negative divergence.

The Nasdaq Composite a similar story but did make a fresh high.

RUT (Russell 2000) fell back to the trendline from the April lows again. As I mentioned Monday “not seeing the same escape velocity as the big cap indices.” Daily MACD now tilts negative, and the RSI a bigger negative divergence.

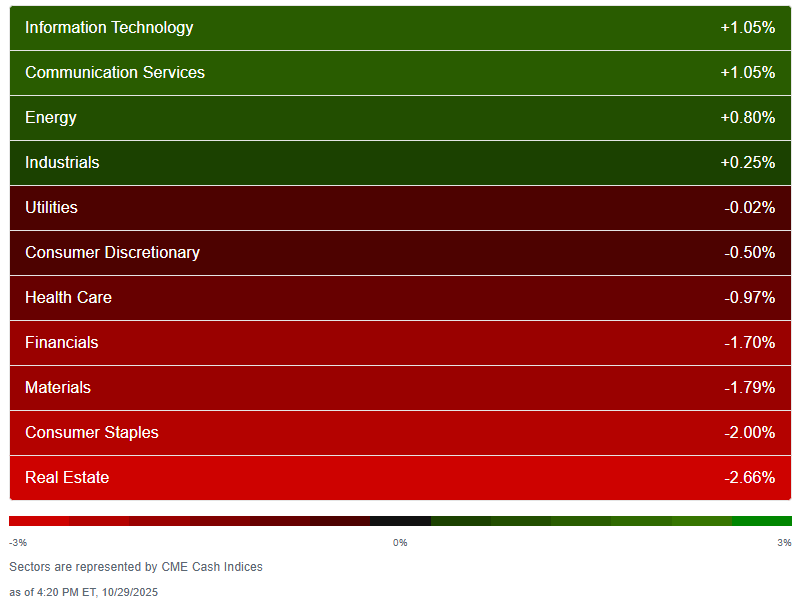

Sector breadth from CME Cash Indices did improve a touch to 4 of 11 sectors higher, up from 3 Tues but down from 9 Mon, again dominated by the megacap growth sectors which took the top two spots for a fourth session (with Tech in there each time). Both were up over 1% (making four days in a row for Tech).

Of the red sectors, six were down at least -0.5% down one from Tues but still pretty weak with four down -1% or more (actually all down at least -1.7%) led again by RE, down -2.7% after -2.2% Tues, followed by Staples also down -2% (after -1% Tues).

SPX stock-by-stock flag from @FINVIZ_com looks quite a bit like Tuesday’s with really just a few changes here and there, but more bright red today in many of the smaller names.

But the top 8 (trillion-dollar club) saw seven of eight higher (at least that many up for a fifth straight session) led by AVGO +3.5%. MSFT the only decliner and it was down just -0.1%. Mag-7 was up +1%, now up +4.9% for the week.

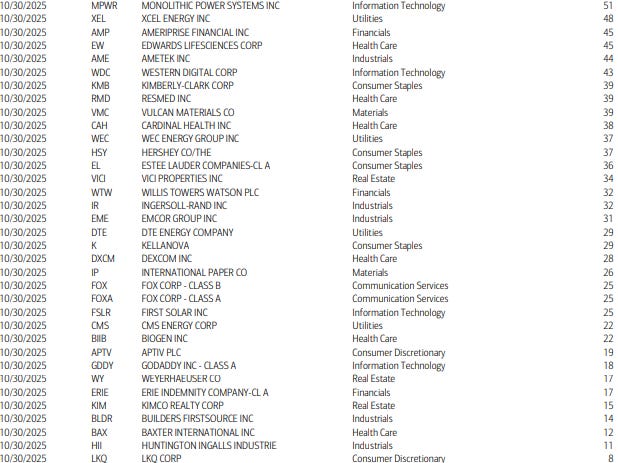

25 SPX components up 3% or more up from 14 Tues, 22 Mon/Fri but down from 51 Thurs. Teradyne TER +20.5% led all components following earnings. STX. WDC, CNC, CAT all also up +10% or more. CAT, PLTR, CEG, AMAT, AVGO (again), ANET, LRCX, ETN were the >$100bn in market cap over 3% (in descending order of percentage gains). NVDA just missed +2.99%.

But 85 SPX components down -3% or more (up from 37 Tues, 5 Mon, 11 Fri). Fiserv FI led decliners will a huge -44% drop after slashing its guidance. SW, GRMN, VRSK were also down over -10%. But of that 85, just six were >$100bn in market cap in APD, ADBE, SPGI, TXN, UNH, and INTU (in order of percentage losses).

NYSE positive volume (percent of total volume that was in advancing stocks) fell to 33.4%, consistent with the -0.75% loss.

[The charts are again not updating. If this continues I’ll try to find another source for net volume].

Nasdaq positive volume similarly fell to 41.4%, again very weak for the +0.55% gain.

Speculative activity fell back further Wed with the top two stocks by volume on the Nasdaq down to 0.8bn shares traded from 1.2bn Tues and 2.15bn Monday (and down from 4.5bn last Wednesday), representing 8% of total volume (down from 12% Tues, 20% Mon, 30% last Wed).

Adding in the next four stocks by volume only brought the total to 1.6bn, down from 2.45bn Tues, 3.2bn Mon and 6.24bn last Wed, as a percentage it was 16% down from 23% Tues, 29% Mon and 43% last Wed.

Positive issues (percent of stocks trading higher for the day) which are not as inflated by penny/meme stocks despite the lower speculative activity continued to be notably lower on the Nasdaq at 30% (despite the index closing up +0.55%) while the NYSE was 29%.

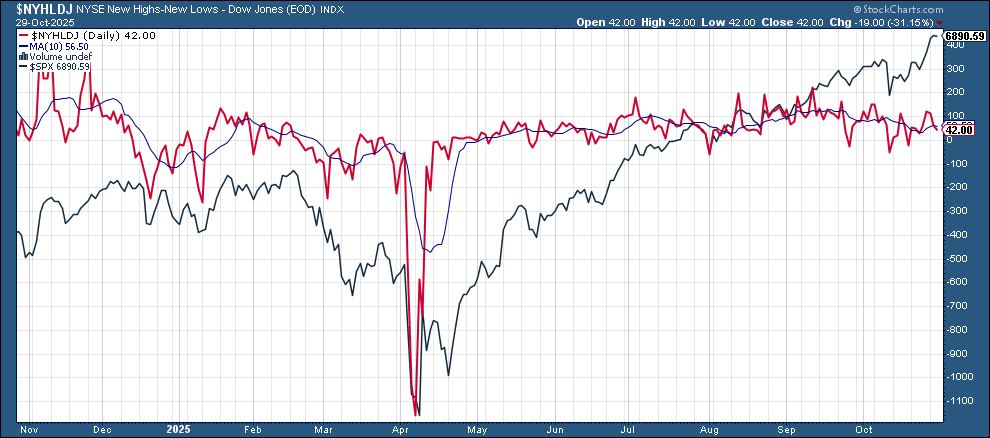

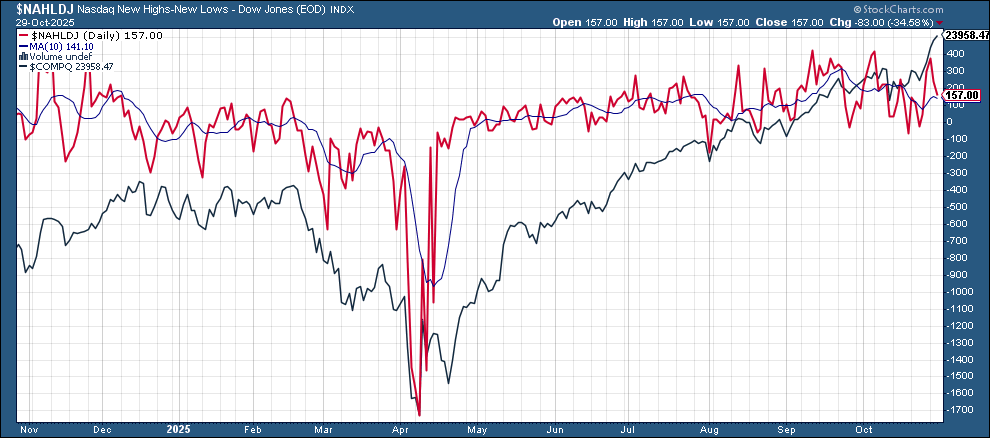

New 52-wk highs minus new 52-wk lows (red lines) fell back to 42 on the NYSE and 157 on the Nasdaq.

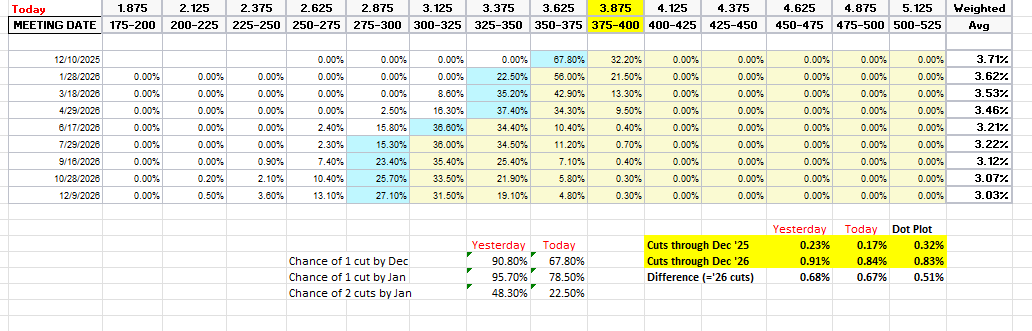

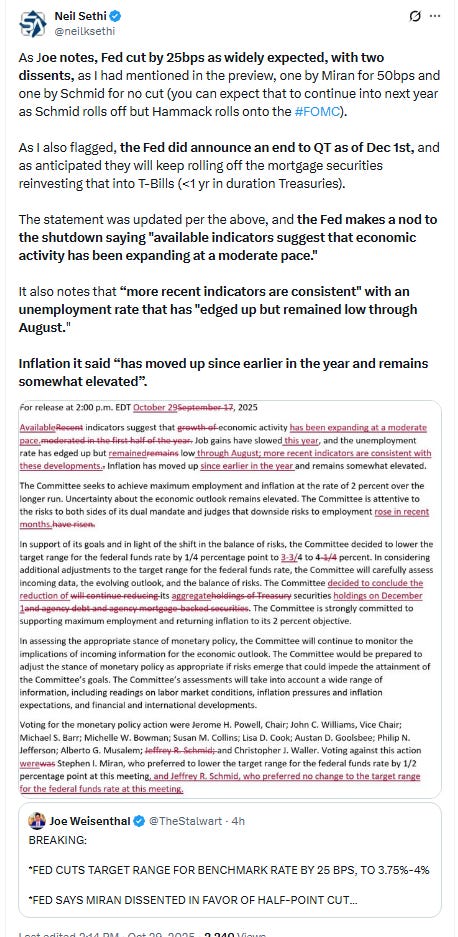

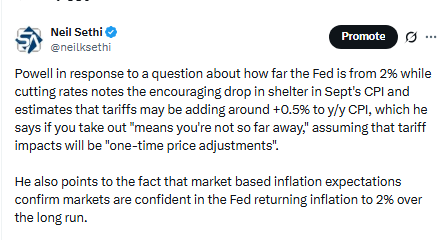

FOMC rate cut pricing for a December cut dropped sharply following Powell’s comments (as a reminder I had said yesterday “Powell might want to talk that down”) according to CME’s Fedwatch tool, although ended the day off the lows of the session at 68%, down from 91% Tues, but up from 55% at the lows (and from over 100% Oct 16th). A cut by January isn’t even a sure thing at 79% (down from 96%).

Pricing for 2026 though just edged -1bps to 67bps (-9bps from the highs Oct 22nd), with total cuts through Dec ‘26 at 84bps (down from 103bps which was the highs of the year (for cuts from Dec on)). As a reminder the average dot on the dot plot has ~60bps of total rate cuts through Dec ‘26 from this point.

I said after the big pricing out of cuts in January (and again in February) that the market had pivoted too aggressively away from cuts, and that I continued to think cuts were more likely than no cuts, and as I said when they hit 60 bps “I think we’re getting back to fairly priced (and at 80 “maybe actually going a little too far” which is definitely where we were Apr 20th (a little too far) at 102bps). I said the day before July NFP “now it seems like we’re perhaps getting back to too few cuts”. I think at 76bps heading into the Sept FOMC we were perhaps a bit overdoing it, but if so not by much (really it will depend on what the trio of Miran, Bowman, and Waller want to do). Now that we see that Waller and Bowman aren’t going to follow Miran to push for large rate cuts, I think my previous stance that there will be at least 50bps this year (we’ve now gotten) but probably not a lot more than that looks pretty solid (which has been my call since last December). I said I thought we got back to overdoing it when over 50bps of rate cuts were priced for the rest of the year Oct 16th. I had said “while 50bps is my base case it’s less than 100% I think,” and that now is certainly the case. I think the market has probably got it right at this point with odds a little better than even that we get that December cut.

Also remember that these are the construct of probabilities. While some are bets on exactly two, three, or four cuts some of it is bets on a lot of cuts (5+) or very few.

After the hawkish cut, the 10yr #UST jumped back over the 4% level +8bps ato 4.06%.

The 2yr yield, more sensitive to FOMC rate cut pricing, jumped +11 basis points to 3.60%. With the drop in the Fed Funds midpoint with the rate cut it is now just 28bps below the Fed Funds midpoint, so calling for rate cuts much less loudly now.

The red line (the Effective Fed Funds Rate) wasn’t updated but didn’t change throughout the day at 4.12%, up 4bps since Sept 18th evidencing continued pressure on funding markets that led to the Fed ending QT. I drew in where I expect it to be tomorrow after the rate cut is incorporated.

I had said when the 2yr yield it was around 4.35% (in Jan & again early Feb) that I found the 2-yr trading rich as it was reflecting as much or more chance of rate hikes as cuts while I thought it was too early to take rate cuts off the table (and too early to put hikes in the next two years on), but then the 2yr fell to 3.65% past where I thought we’d see it, so I took some exposure off there. We got back there but I never added back what I sold, so I stuck tight. Ian Lygan of BMO said on his weekly podcast he now sees it at 3.3% by year’s end (but sees risk to the downside), but I still took some off Sept 5th at 3.5%. I’ll add back at ~3.90% if we get there (seems though that ship might have also sailed).

The DXY dollar index (which as a reminder is very euro heavy (57%) and not trade weighted) followed yields higher after treading water for five sessions towards the high end of its range since May. The daily MACD and RSI are starting to push more positive again.

VIX edged higher to 16.9. That level is consistent w/~1.08% average daily moves in the SPX over the next 30 days.

The VVIX (VIX of the VIX) also continued its rebound from the uptrend line from the March lows. It ended at 103.6, just over Nomura’s Charlie McElligott’s breakeven “stress level” of 100 (and now consistent with “moderate” daily moves in the VIX over the next 30 days (normal is 80-100)). As I said Friday, “If that trendline breaks, it will be notable.” Seems safe for now.

With the Fed falling off but Mag-7 earnings rolling on, the 1-Day VIX moved up to 15.2. It implies an ~0.95% move Thurs.

WTI futures able to stabilize but not much more Wed despite a very strong storage report. The MACD remains with a “cover shorts” signal but the RSI is under 50, so it’s using up its time with favorable technicals.

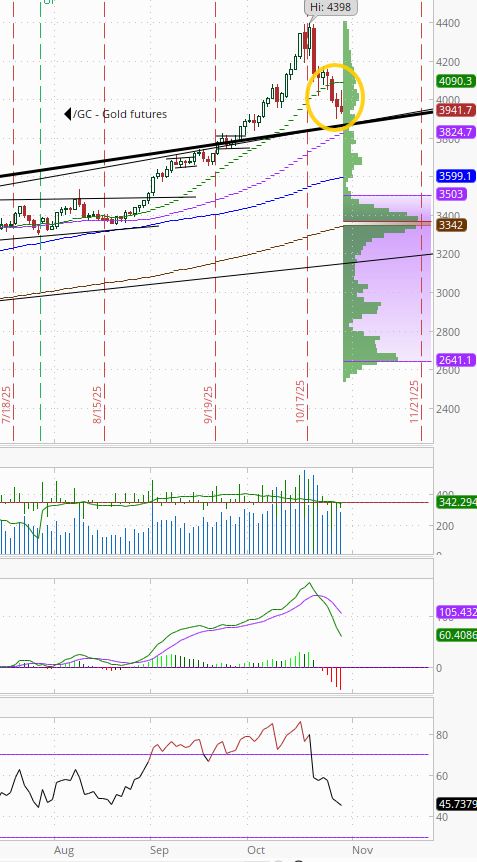

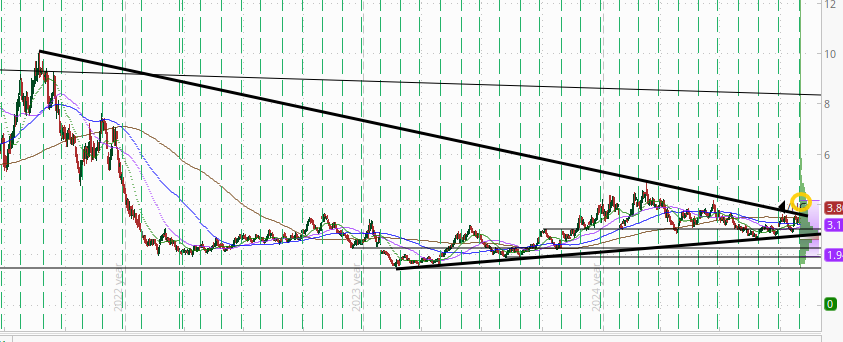

Gold futures (/GC) continued their correction now down -11% from the peak although the decline has slowed considerably as it sits above the top of an uptrend line stretching back to Oct ‘23. As noted Wed, daily MACD has now crossed over to “sell longs” and as noted Tues the RSI fell from a very elevated level to under 60 (now under 50), which has typically led to some consolidation in the past. Seems that’s what we’re seeing.

US copper futures (/HG) edged up to the highest close since July at the top of their October range. As noted Monday Daily MACD has now crossed to “go long” positioning and the RSI now over 60.

Nat gas futures (/NG) had a down session, but a very favorable roll to the December contract which is trading 16% higher than where November closed saw it jump above a downtrend line running all the way back to Aug ‘22. Daily MACD remains in “go long” positioning for now, while the RSI is over 50 so we’ll see if it can make a run or falls back to fill the “roll gap”.

Bitcoin futures fell back for a second session from the highest close in two weeks remaining in the middle of the new trading range they’ve created going back to early July. The daily MACD remains in “go short” positioning but is improving and the RSI is around 50.

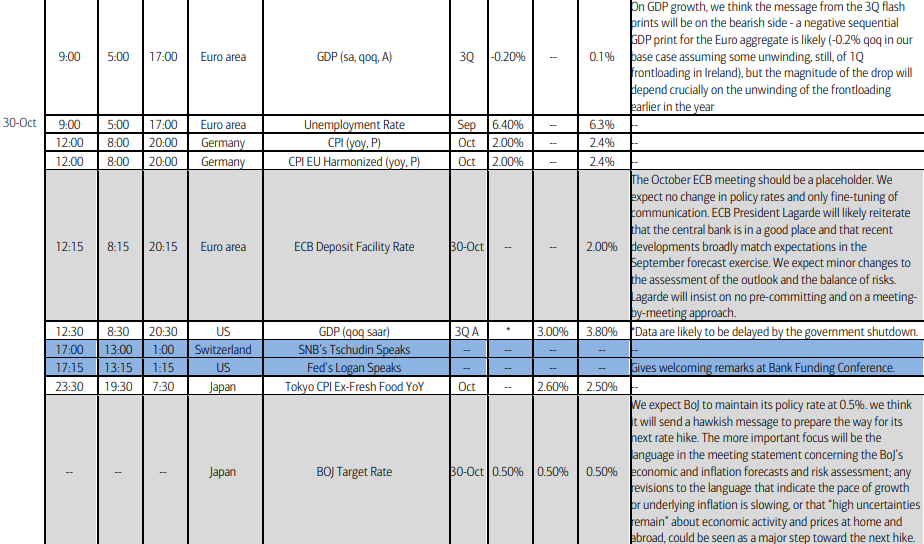

The Day Ahead

US economic data Thursday empty of major releases with the shutdown.

As noted in the Week Ahead, we will unusually hear from Fed speakers the day after the decision (they normally wait until at least Friday) but as they’re both welcoming remarks, I’m guessing they won’t be commenting on monetary policy. The speakers are Gov Bowman giving opening remarks for the Economic Growth and Regulatory Paperwork Reduction Act (EGRPRA) Outreach Meeting and Dallas Fed Pres Logan (2026 voter) at the Dallas Fed’s research conference “The Evolving Landscape of Bank Funding.”

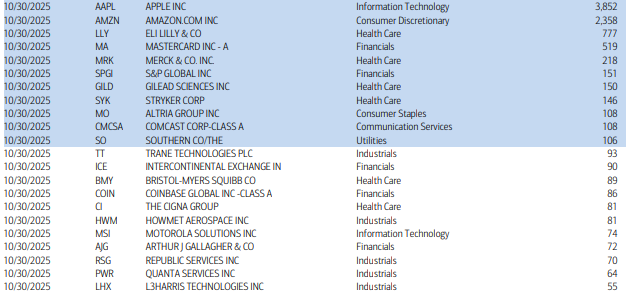

Earnings remain in top gear Thursday with 56 SPX reporters, again eleven of which are >$100bn in market cap led by two more Mag-7 components in AAPL & AMZN. The others are LLY, MA, MRK, SPGI, GILD, SYK, MO, CMCSA, SO (in descending order by market cap).

Ex-US DM highlights are policy decisions from the ECB and BoJ. On the former, like the Fed meeting today, there is little drama expected with anything but a hold a major shocker and Lagarde almost certainly to remain noncommittal as to any future moves. On the latter BoJ though there is some drama. Most analysts expect a hold, but some (like JPM) expect a cut despite the new prime minister not being a fan of rate hikes. There will also be much attention paid to the vote split (there will almost surely be dissents no matter which way it goes, the question is how many), and of course the Ueda press conference will be important. In terms of data, we’ll also get EU GDP and unemployment, German CPI,

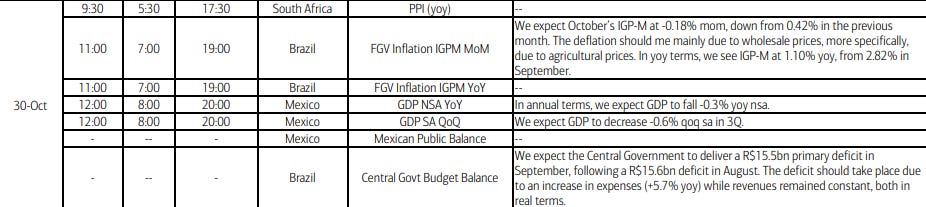

In EM, highlights are Brazil inflation and Mexico GDP data.

Burying the lead perhaps we’ll get the much anticipated meeting between Presidents Trump and Xi where all indications are they will dial things back to where they were prior to the most recent dust-up and perhaps go a little further as floated in the Week Ahead with potentially a dialing back of the fentanyl tariffs, agreements on soybean purchases and perhaps Tiktok.

Link to X posts - Neil Sethi (@nelksethi) / X

To subscribe to these summaries, click below (it’s free!).

To invite others to check it out,