Markets Update - 11/15/24

Update on US equity and bond markets, US economic reports, the Fed, and select commodities with charts!

To subscribe to these summaries, click below (it’s free!).

To invite others to check it out (sharing is caring!),

Link to posts - Neil Sethi (@neilksethi) / X (twitter.com)

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog.

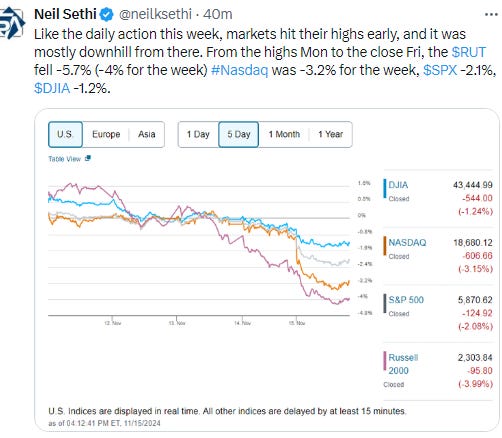

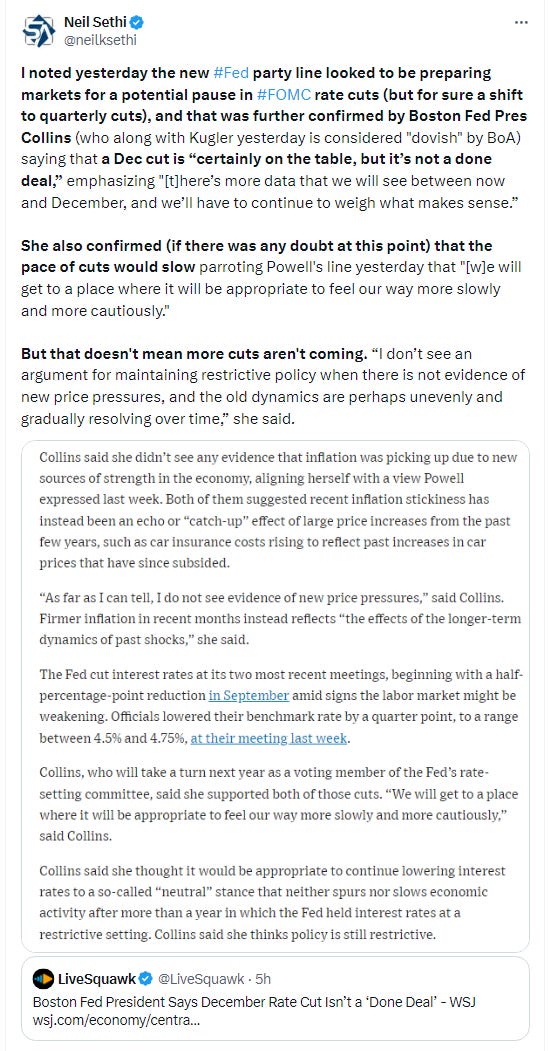

US equity indices peaked in the first hour Friday (as they had every day previously last week) again falling throughout the morning, this time on the back of stronger than expected (with revisions) retail sales paired with hotter than expected import prices and comments from Boston Fed President Collins that a December rate cut was “not a done deal.” Tech and healthcare stocks led the declines. However with no Powell speech to quash a rally, like every day other than Thursday, stocks found their footing after noon and pared some of the losses, still though finishing broadly lower to cap a solidly down week (a relative rarity this year), the worst in 2 months according to BBG.

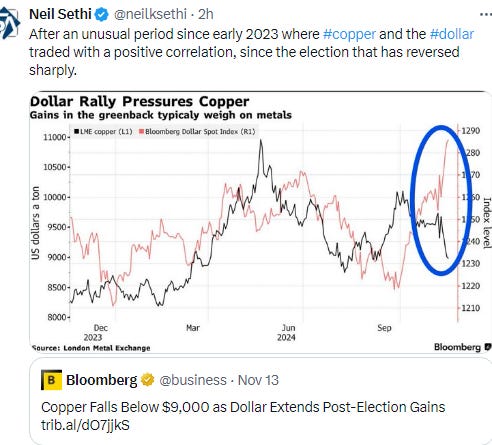

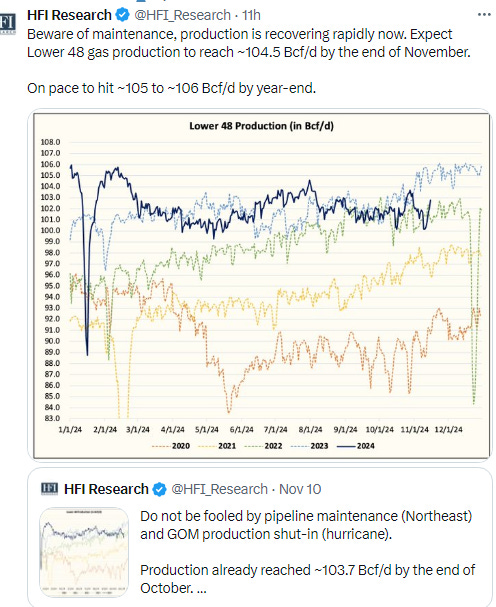

The dollar edged lower but remains not far from 2 yr highs. Gold and copper still fell again, as did crude to a key support level. Nat gas though got a bounce and bitcoin jumped over $90k to another all-time closing high.

The market-cap weighted S&P 500 was -0.6%, the equal weighted S&P 500 index (SPXEW) -0.8%, Nasdaq Composite -0.6% (and the top 100 Nasdaq stocks (NDX) -0.7%), the SOX semiconductor index -0.1%, and the Russell 2000 -1.4%.

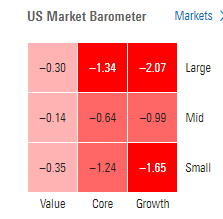

Morningstar style box very similar to Thursday’s with broad weakness but value outperforming.

Market commentary:

“Investors are catching their breath and evaluating whether the advance has merit,” said Sam Stovall, chief investment strategist at CFRA Research. “We really don’t see anything on the horizon right now to upend stocks, but investors are always sort of looking around to see what could cause the trend to end.”

As the initial euphoria about Trump’s pro-business agenda begins to fade, investors are coming to terms with the costs of his fiscal plans and their potential to reignite inflation. “It will come at the expense of potentially larger budget deficits, potentially larger debt and there is also the inflation dimension,” said Charles-Henry Monchau, chief investment officer at Banque Syz & Co. “There’s been a realization that there is a price to pay for this.”

“The market is expensive and I think Powell’s speech last night basically saying that Fed officials don’t need to rush to lower rates, that’s probably the main reason why we’re selling off specifically today,” John Davi, CEO and CIO at Astoria Advisors, said by phone. “The higher rates go, the more equity risk premiums tilt more in the favor of bonds.”

“While we think the macro backdrop still bodes well for risk assets, in the near term we should expect some micro volatility, particularly around potential policy shifts under a new administration,” said Kristy Akullian, head of iShares investment strategy, Americas, at BlackRock. “We expect the U.S. equity market to continue to move higher, but don’t expect that rise to happen in a straight line.”

“Some controversial cabinet announcements obviously do not help the market,” Mathieu Racheter, head of equity strategy at Julius Baer Group Ltd., said.

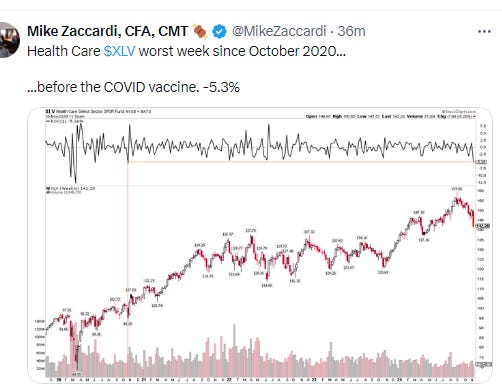

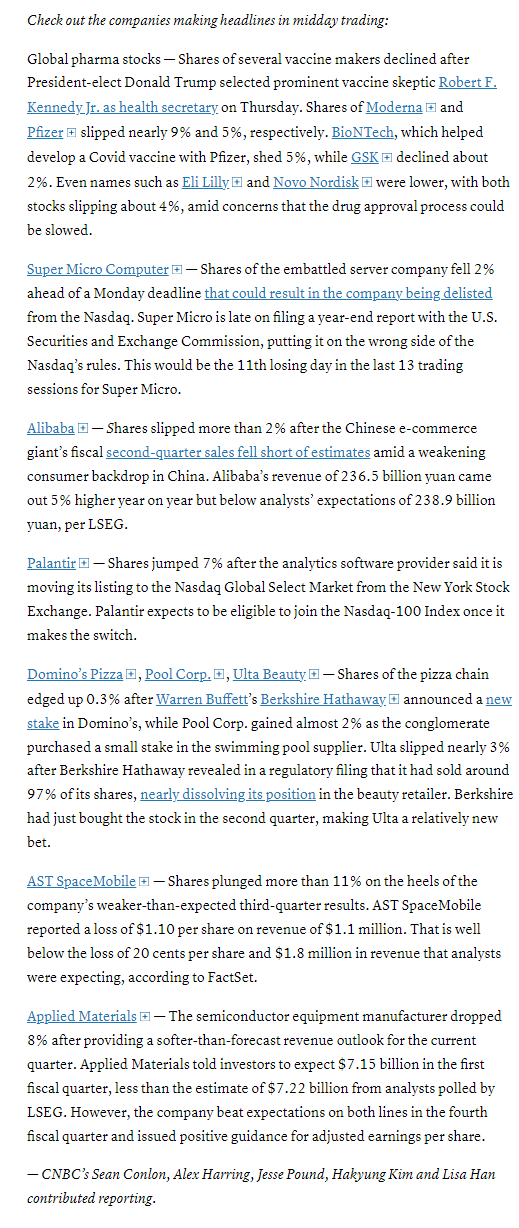

In individual stock action, the information technology sector of the S&P 500 was the worst performing corner of the market, down more than 2% as Nvidia, Meta Platforms, Alphabet and Microsoft tumbled. Tesla was a rare exception among its Magnificent Seven peers, as shares of the electric vehicle giant and so-called “Trump Trade” were higher by 3%. Applied Materials Inc., the largest US maker of chip-manufacturing equipment, suffered its worst stock decline in a month -9.2% after giving a disappointing revenue forecast.

Declines in pharmaceutical stocks also weighed on the 30-stock Dow and the S&P 500, with Amgen down about 4.2% and Moderna off by 7.3%. President-elect Donald Trump said on Thursday that he planned to nominate vaccine skeptic Robert F. Kennedy Jr. to lead the U.S. Department of Health and Human Services. The SPDR S&P Biotech ETF (XBI) tumbled more than 5% and posted its worst week since 2020.

Some tickers making moves at mid-day from CNBC.

In US economic data:

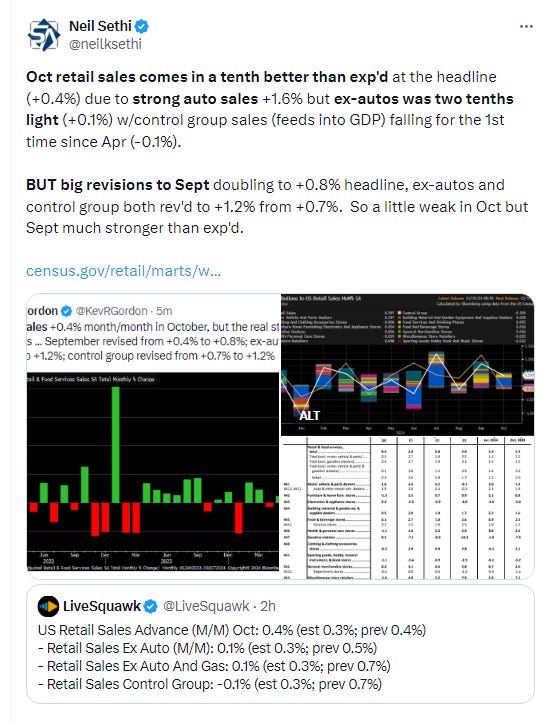

Oct retail sales were a tenth better than expected at the headline level (+0.4%) due to strong auto sales (+1.6%) but ex-autos was two tenths light (+0.1%) w/control group sales (which feed into GDP), falling for the 1st time since April (-0.1%). BUT big revisions to Sept which doubled the headline gain to +0.8% and ex-autos and control group were both revised to +1.2% from +0.7%. So a little weak in Oct, but Sept much stronger than previously thought.

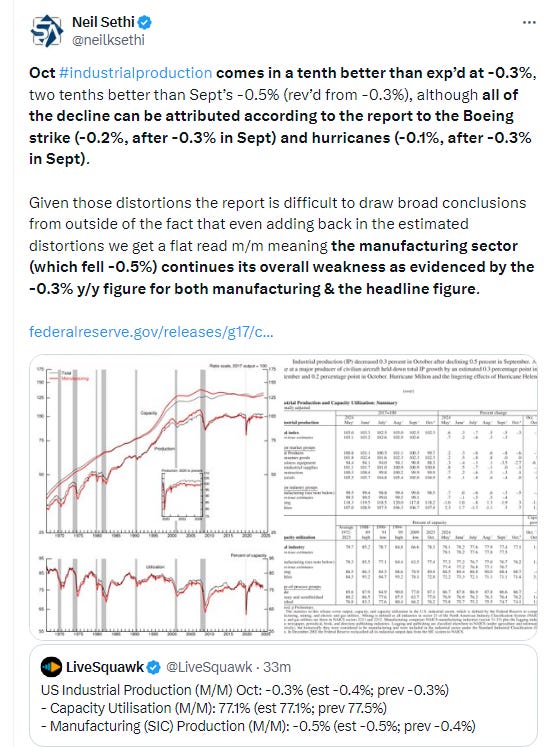

Oct industrial production came in a tenth better than exp’d at -0.3%, two tenths better than Sept’s -0.5% (rev’d from -0.3%), although all of the decline can be attributed according to the report to the Boeing strike (-0.2%, after -0.3% in Sept) and hurricanes (-0.1%, after -0.3% in Sept). Given those distortions the report is difficult to draw broad conclusions from outside of the fact that even adding back in the estimated distortions we get a flat read m/m meaning the manufacturing sector (which fell -0.5%) continues its overall weakness as evidenced by the -0.3% y/y figure for both manufacturing & the headline figure.

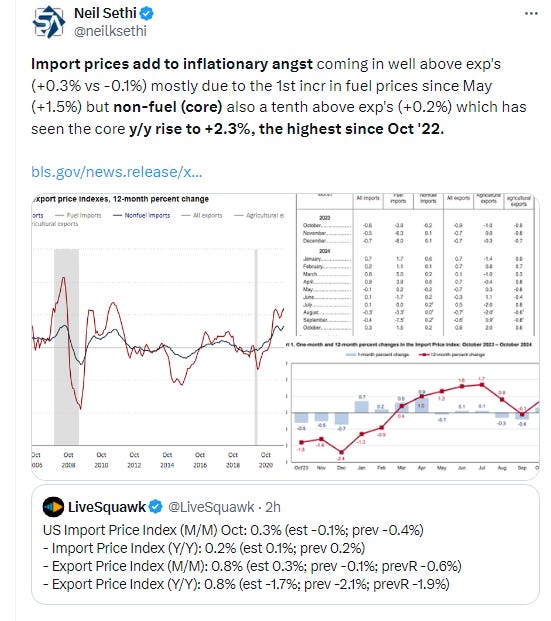

Import prices came in well above exp's (+0.3% vs -0.1%) mostly due to the 1st incr in fuel prices since May (+1.5%) but non-fuel (core) also a tenth above exp's (+0.2%) which has seen the core y/y rise to +2.3%, the highest since Oct '22.

Link to posts - Neil Sethi (@neilksethi) / X (twitter.com) for more details.

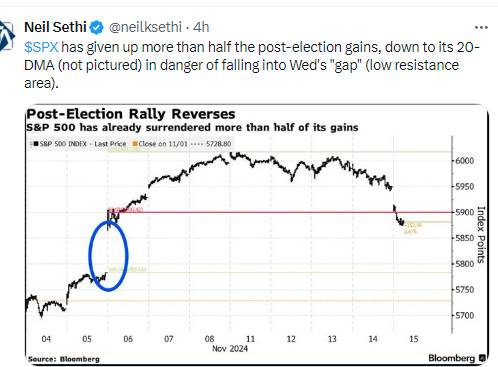

The SPX sits right around its breakout level having given up all of its gains since Wednesday’s open and edging into the gap, with its MACD & RSI rolling over and very close to turning negative.

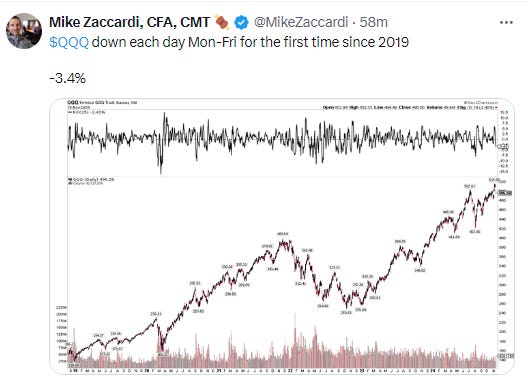

The Nasdaq Composite, similar to the SPX, sits right around its breakout level having given up all of its gains since Wednesday’s open and edging into the gap, with its MACD & RSI rolling over and very close to turning negative.

RUT (Russell 2000) after getting to a tenth of a percent of an ATH Monday has seen a “waterfall” type decline. I said Thurs it seemed headed for a test of the 2300 breakout level, and it got there in one day. MACD remains supportive but it is rolling over, and the RSI already has heading quickly lower indicating a sharp loss of momentum.

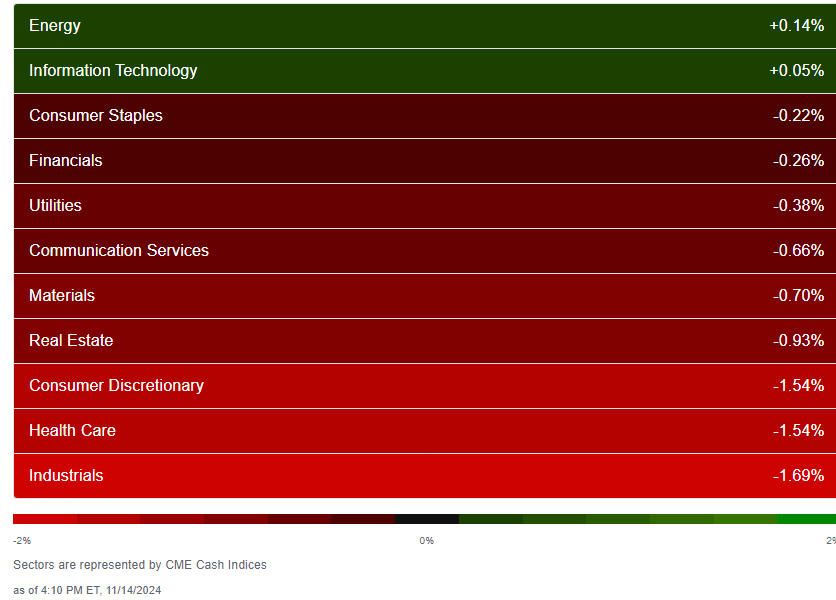

Equity sector breadth from CME Indices improved slightly but remained weak with just 3 green sectors Fri (up from 2 Thurs) with two up more than the best on Thurs ((+0.14%) in financials & utilities (the latter the only sector up over 1%). Four sectors down more than 1% though (one more than Thurs) led by tech (-2.5%).

Stock-by-stock SPX chart from Finviz consistent w/quite a bit of red.

Positive volume was again not bad (but not great) on the NYSE but good on the Nasdaq Fri at 40 & 41% respectively. The 30% is “ok” with both the SPX & RUT seeing solid losses (and actually better than Thurs’s 39% so a positive divergence there) while the 41% is pretty good considering the Nasdaq was down over 400 points on the day. Issues continued to be weaker though at 35 & 28%.

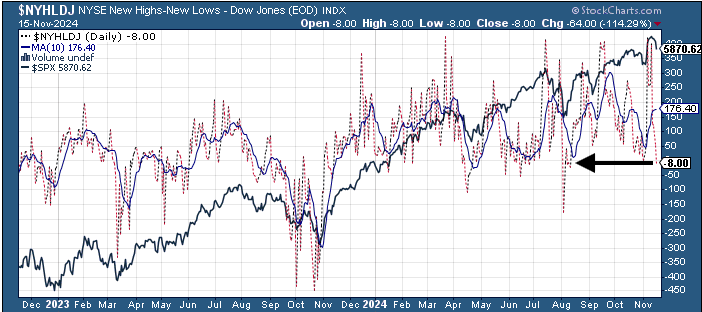

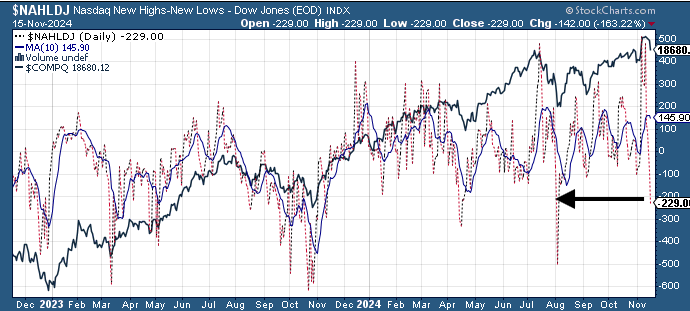

New highs-new lows though continued to drop to -8 and -229 (remember they were 404 & 483 respectively on Monday, which were not far from the best since early 2021). That’s the weakest since August. They’re now well below the 10-DMAs (less bullish), and now the DMA’s continue to start rolling over.

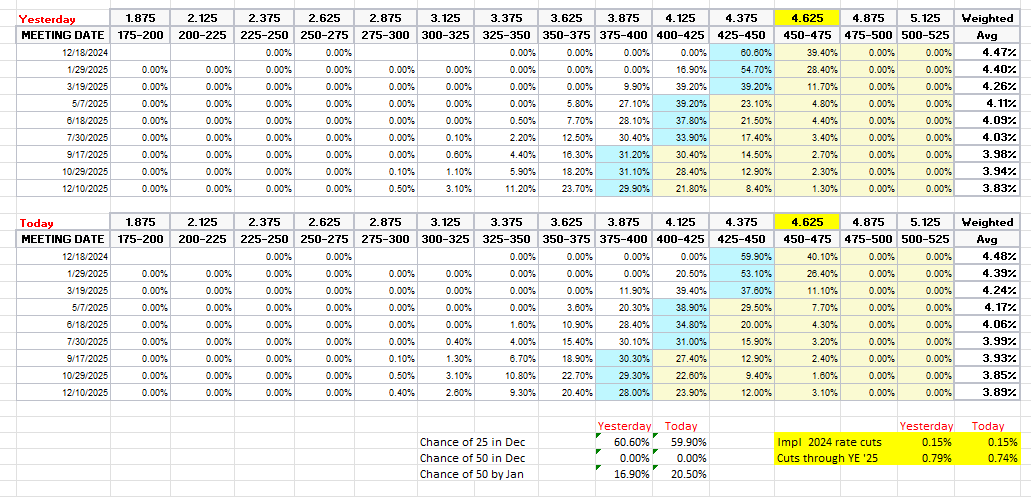

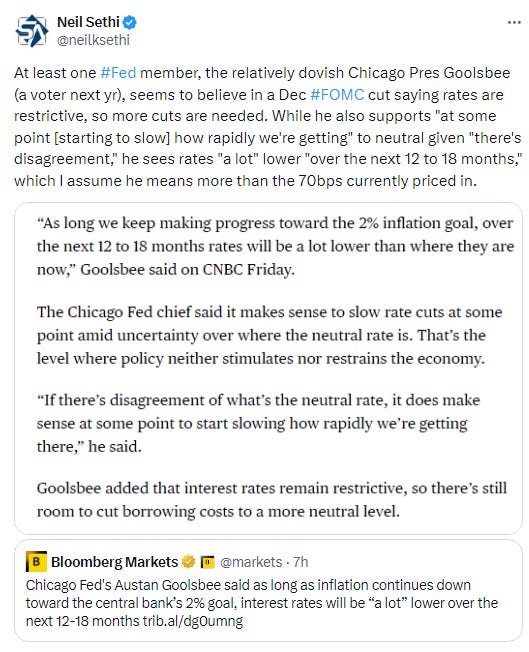

FOMC rate cut probabilities from CME’s Fedwatch tool were also volatile Friday with the chance of a December cut falling to ~50% following the relatively strong retail sales report, hotter than expected import prices, and Boston Fed Pres Collins saying December was “not a done deal.” But by the end of the day they were back to where they were Thursday with the chance of 25bps in December at 60% (still down from 82% Wed), while cuts priced through YE ‘25 were 74bps from 77 Thurs (but still down from around 100 pre-election).

Treasury yields were volatile again Friday, like Thursday moving higher following the morning data then falling back during the day with the 10yr yield, more sensitive to longer term growth/inflation expectations, ending +1 basis point at 4.43% after at one point again nearing 4.5% (identified by many as a “line in the sand”), still +72bps since the start of October. The 2yr yield, more sensitive to Fed policy, was also +1bps to 4.30%, also off the highs but still the highest close since July. It’s up +64bps since the start of October.

Dollar ($DXY) took another run at the 107 level but fell back to again finish below, only its 2nd down day since the election. The 2023 high was $107.35. Daily MACD & RSI remain supportive.

The VIX & VVIX (VIX of the VIX) both moved to the highest levels since the election before falling back. The former still though to 16 (consistent w/1% daily moves over the next 30 days) and the latter to 99 (just under the 100 level which is consistent with more “elevated” daily moves in the VIX over the next 30 days).

1-Day VIX jumped to highest since the day after the election likely due both to elevated volatility this week in equities and Treasuries but also as Friday was monthly option expiration which releases the “gamma pin” from monthly options that has often seen volatility move higher the following week. Now at 13.4, it’s looking for a move of ~0.84% Thursday, near what BoA said was implied from options markets coming into the week.

WTI fell back to just under $67, a level it had previously closed under only once (Sept 10th) in nearly 3 yrs (since Dec ‘21). There’s mild support down to the Sept 10th intraday low of $65.27 but this area really needs to hold or we’re looking back 3 years for support levels, not a great situation. Daily MACD & RSI are no help, remaining tilted negative.

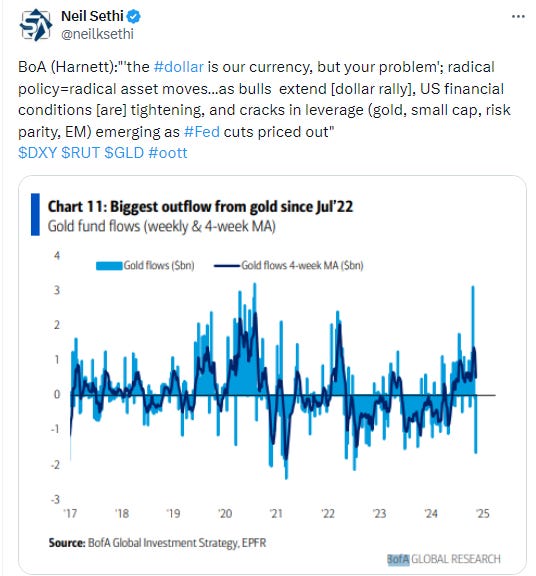

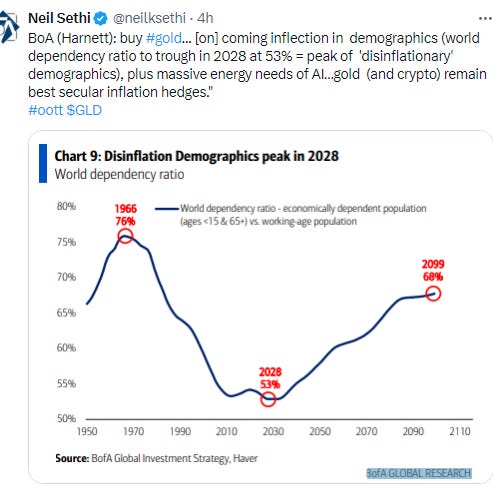

Gold fell for the 7th day in 8 to a 2-mth low, although continuing to hang on to its 100-DMA by its fingernails. As I said Wednesday, “we’ll see if that holds given as noted Monday the daily MACD is firmly in ‘sell longs’ positioning, and the RSI is now the weakest since Oct ‘23.” If it doesn't hold no great support until way down at $2400 area.

Copper (/HG) like gold fell for 7th day in 8, in its case to the lowest close in 3 mths, with an odd back-to-back candle pattern of a hammer followed by a shooting star, both reversal candles. Daily MACD & RSI as noted Monday are in a negative positioning, so we’ll see if we don’t test $4 again.

Nat gas (/NG) continued to fall to start the Friday session but got a bounce at its 20-DMA to finish up a couple percent, still below the highs of the week near $3. The MACD & RSI remain positive for now, but the growing production HFIR sees is definitely going to be a headwind.

Bitcoin futures got that push I mentioned Thursday to stay over $90k, an all-time closing high. I noted last Friday it had gotten very extended, but that it had gotten more extended in February, so we’ll see if it has enough to get to $100k. As a reminder Katie Stockton’s target was $97.5k.

The Day Ahead

Enjoy the weekend. More on Sunday.

Link to X posts - Neil Sethi (@neilksethi) / X (twitter.com)

To subscribe to these summaries, click below (it’s free!).

To invite others to check it out,