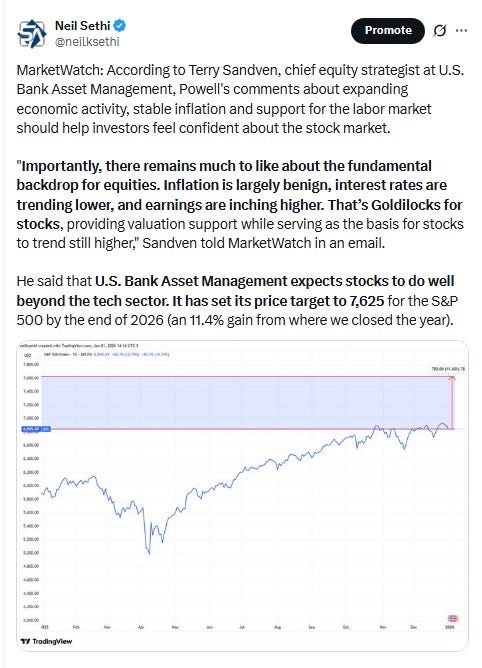

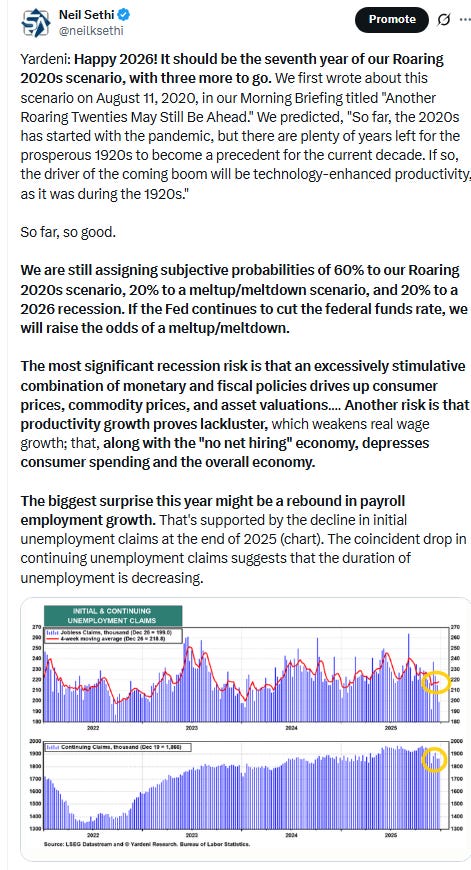

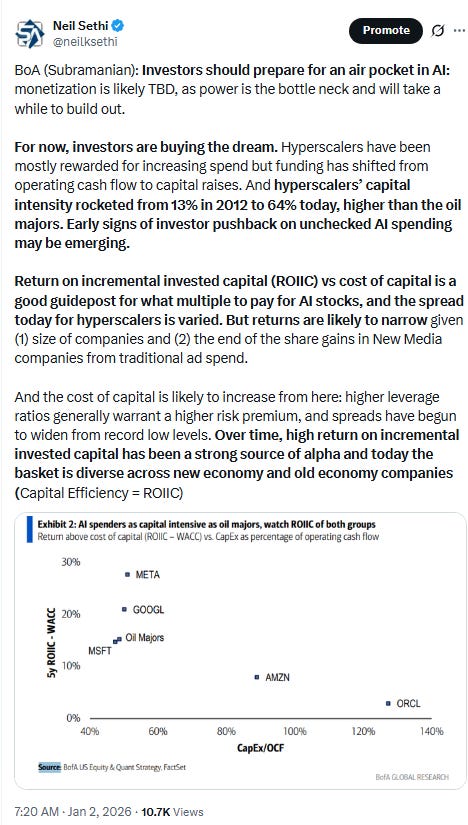

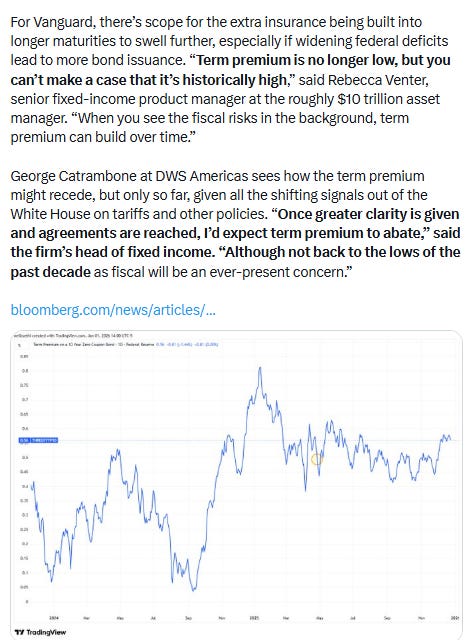

Markets Update - 1/2/26

Update on US equity and bond markets, US economic data, the Fed, and select commodities with charts!

To subscribe to these summaries, click below (it’s free!).

To invite others to check it out (sharing is caring!),

Link to posts - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog. Also please note that I do often add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

Finally, if you see an error (a chart or text wasn’t updated, etc.), PLEASE put a note in the comments section so I can fix it.

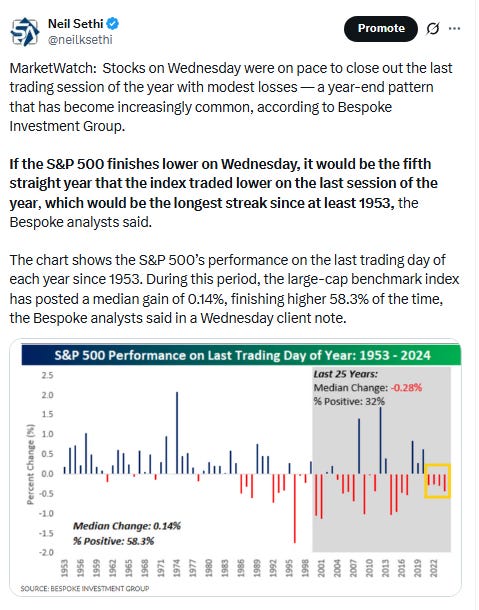

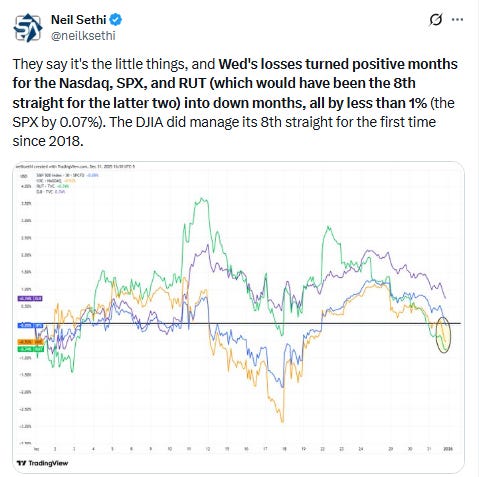

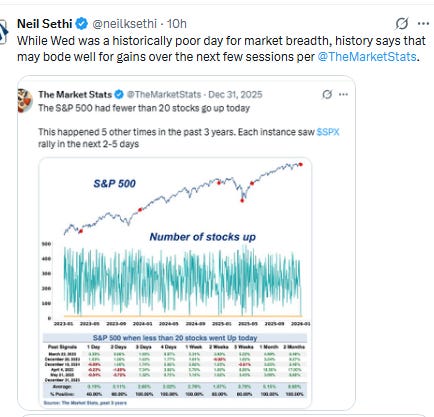

US equity indices opened 2026 solidly higher looking to break the four-day losing streak that left a sour taste to the end of a third consecutive double-digit gain for the SPX in 2025. It was far from a certainty as since 1953, the S&P 500’s median change to kick off a new year has been a -0.3% drop, with gains less than half the time, according to a note by Bespoke Investment Group. But renewed optimism around the AI trade saw those stocks lead gains with Nvidia shares up more than 1% in the premarket, Palantir Technologies more than 2%, and fellow tech stocks Apple, Alphabet and Microsoft also trading higher. Nvidia would hold those gains, but software stocks like Palantir would turn sharply lower leading the megacap growth sectors into the red (despite solid performances from semiconductors (the SOXX semiconductor index was +4.0%)).

And stocks in other sectors also did well (the equal-weighted SPX finished +0.7%), but it was hard to escape the pull from those large growth sectors. As a result the indices gave up their initial gains in the first hour. They traded mixed from there until 2pm with the small cap Russell 2000 index (RUT) and the DJIA drifting higher, while the SPX & Nasdaq were led lower by those megacaps. All though managed to rally in the 2-3pm hour with indices finishing at those 3pm levels led by the RUT’s +1.1%. The DJIA was +0.7%, the SPX +0.2%, and the Nasdaq lagged finishing flat. Still, it was the first gain for the SPX on the first trading day of a year since 2022.

Elsewhere, bond yields edged higher, as did the dollar. Commodities were mixed with bitcoin seeing a solid gain, natgas seeing a loss, but gold, crude, and copper were all little changed.

The market-cap weighted S&P 500 (SPX) was +0.2%, the equal weighted S&P 500 index (SPXEW) +0.7%, Nasdaq Composite unch (and the top 100 Nasdaq stocks (NDX) -0.2%), the SOXX semiconductor index +4.0%, and the Russell 2000 (RUT) +1.1%.

From Wed:

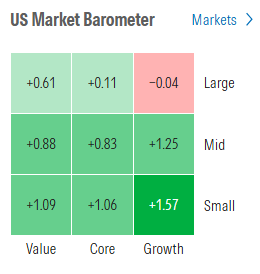

Morningstar style box again showed broad gains for the first time this week outside of large cap growth which saw a small loss. A clear preference for smaller market caps Friday.

Market commentary:

From Friday:

“We think that you will have this ongoing rotation back and forth between tech and non-tech, but that overall we’ll drift higher,” said Jay Hatfield, Infrastructure Capital Advisors CEO. Hatfield, who has an 8,000 year-end target for the S&P 500, said the rally will be “better balanced” as regional banks outperform and tech stocks with expensive valuations such as Tesla start to lag. “There are themes besides tech that are very likely to work this year,” he continued.

“What we are seeing today is a continuation of the run higher in equities, with AI and tech again at the forefront,” said Tim Waterer, chief market analyst at KCM Trade. “Traders are still in a buying mood, with many of the bullish themes from 2025 carrying forward into 2026.”

“The bumpy ride occurring on the first day of 2026’s trading is poised to be emblematic of what the rest of the new year has in store for Wall Street,” said José Torres, senior economist at Interactive Brokers, in emailed comments on Friday. “Stocks opened sharply higher before retreating to modest losses and are now advancing again as investors contemplate whether the tech sector has the fuel to deliver another year of terrific returns or if the enthusiasm surrounding AI is overdone,” he said.

Barclays Plc strategists warned equity markets could get choppy as they enter 2026 at record highs that are “over-reliant on AI success.” The team still expects further gains this year, thanks to resilient corporate earnings and a favorable trade-off between growth and monetary policy.

Bank of America Corp. strategists see the S&P 500 hitting 7,100 this year, a roughly 4% gain from its current price. The “growing capital-intensity of big tech spenders that make up an outsized share of the index, elevated multiples, plus cracks in the labor market (with further downside linked to AI upside) argues for a more cautious stance,” they wrote.

“The first trading day has been an incredibly poor guide in recent times to how the rest of the year plays out,” wrote Deutsche Bank AG strategists including Henry Allen. In fact, “2022 saw an all-time high on the first day, before the index fell into a bear market and its worst year since 2008. Whatever happens today, we really shouldn’t overegg the day one moves.” The strategists noted that several key themes apart from AI will shape markets in 2026, including new developments in US trade policies and specifically a Supreme Court case that will rule on the legality of levies. The Fed will be another major focus, with President Donald Trump expected to name a successor to Jerome Powell early in the year.

“The scope for further gains driven purely by valuation expansion in 2026 may be limited,” wrote Linh Tran, an analyst at XS.com. “Shocks related to interest rates, earnings, or policy could therefore trigger faster and more pronounced corrections than in earlier phases of the cycle.”

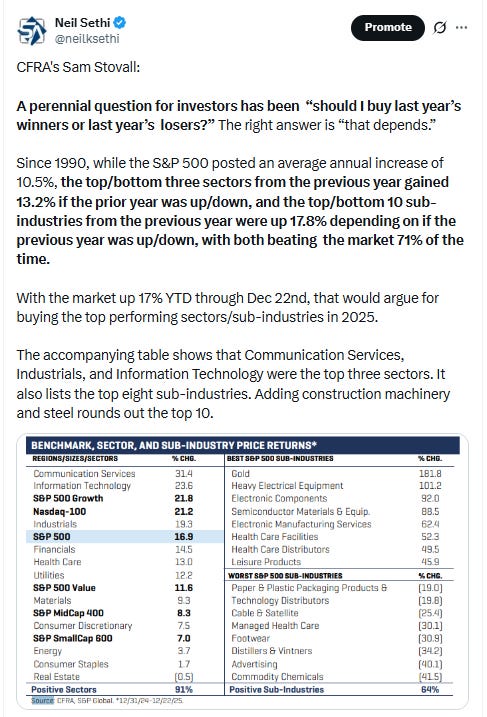

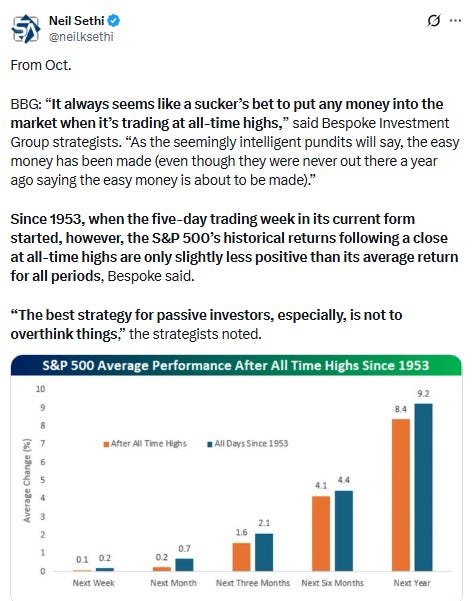

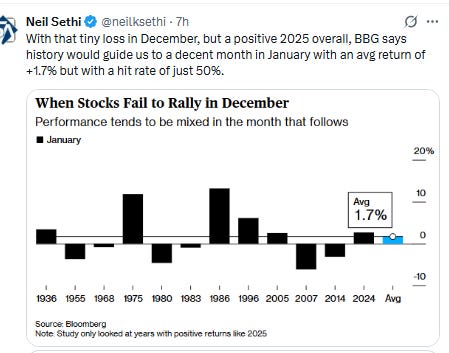

“In years when the S&P 500 rose in January yet failed to rally in December, returns were pretty mixed. Ultimately, seasonality offers little guidance. Earnings might help, but the fourth-quarter season doesn’t kick off until mid-January. That leaves stocks trading with little direction, guided mainly by business surveys and shutdown-impacted economic data.” — Tatiana Darie, Macro Strategist, Markets Live.

From Wed/Thurs:

Market participants “aren’t necessarily cautious,” said Steve Sosnick, chief strategist at Interactive Brokers. However, “they may be fully invested going into the new year.”

“Wall Street rounded out the year in a subdued fashion, capping a good year for stocks, albeit one that included a nervous moment or two,” said Kyle Rodda, senior financial market analyst at Capital.com However, Rodda warned that markets are pricing in a close to perfect set of circumstances going into next year. “Above trend economic growth, a stable labor market, continued disinflation, more rate cuts, and an AI boom underpinning it all. That will have to be delivered if stocks are going to justify current lofty valuations. The risk is that too much good news is priced-in and investors aren’t positioned for nasty surprises,” he said.

“Next week brings several readings on employment, including November job openings, but the main event is likely to be December nonfarm payrolls due next Friday,” followed by the fourth-quarter earnings season starting the week after, Mazzola said in emailed commentary on Wednesday.

“As we look towards next year, we’re expecting a little bit more volatility,” Meghan Shue, head of investment strategy and portfolio construction at Wilmington Trust, said Tuesday on CNBC’s “Closing Bell.”

“I think this is a healthy sort of churn as we reset for the next leg of the bull market, which we expect to continue, outside of what we still have as a decently high recession risk,” Shue added.

“Describing 2025 as ‘resilient’ might be an understatement,” said Adam Turnquist, chief technical strategist for LPL Financial. “The economy showed remarkable strength by overcoming higher inflation, a slowing labor market, fewer rate cuts than originally expected, and a sharp rise in the effective tariff rate. Despite these challenges, growth remained steady without slipping into recession.”

“After an excellent year in equity markets, and with positioning close to highs in late November, portfolio and fund managers may have been closing their bets and realigning them to benchmark,” said Roberto Scholtes, head of strategy at Singular Bank. “Our base case is for the bull run to continue, albeit with more volatility and resulting in mid-single digit returns.”

“There were lessons learned on the part of the administration that smarter, more narrow tariffs with a gradual implementation is what the market can absorb,” said Keith Buchanan, senior portfolio manager at Globalt Investments. “The market is now, because of 2025, able to look past any tariff shifts in 2026, banking on the administration remembering those lessons from 2025 and also corporate America being able to adjust on the fly in a way that continues to preserve margins.”

“We’ve seen internals change in a way that indicates us that 2026 could ... look very different than 2025, even more so than 2023 and 2024,” Buchanan said. ”[The market] is going to be driven more by fundamentals that are less dependent on monetary policy and AI infrastructure buildout.”

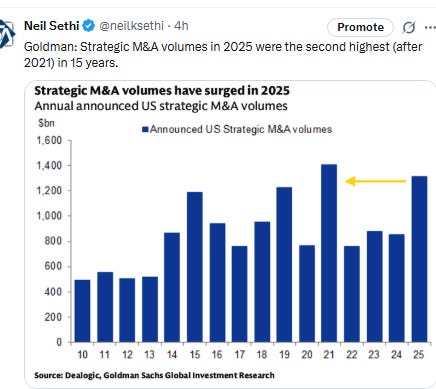

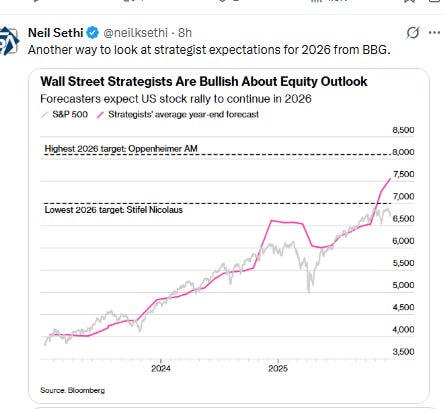

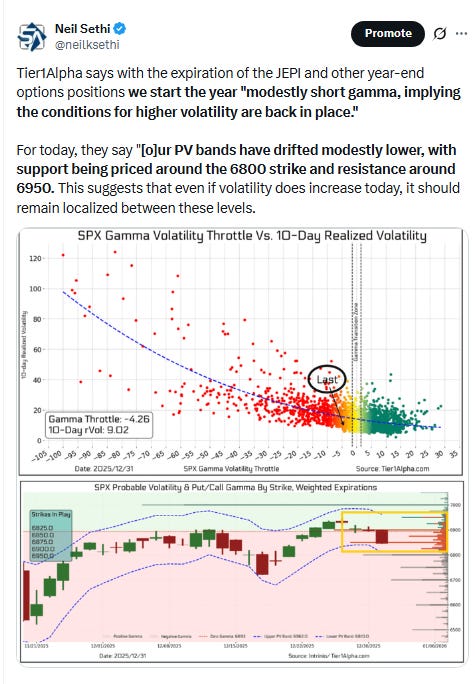

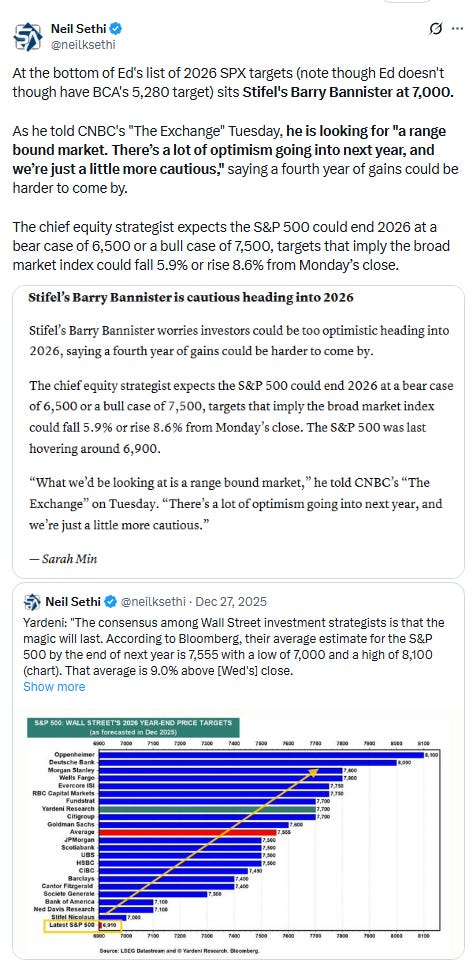

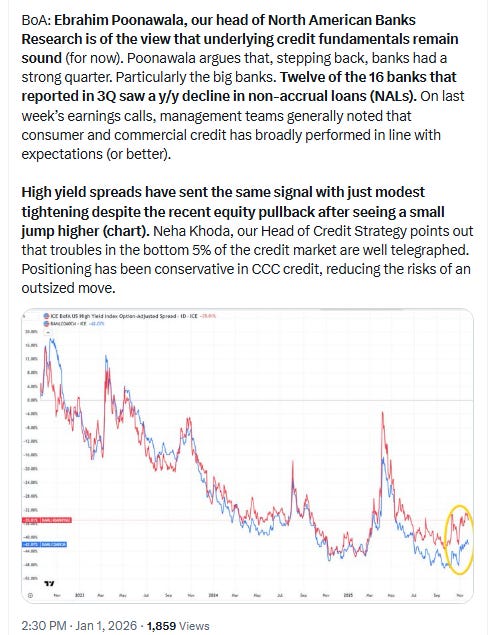

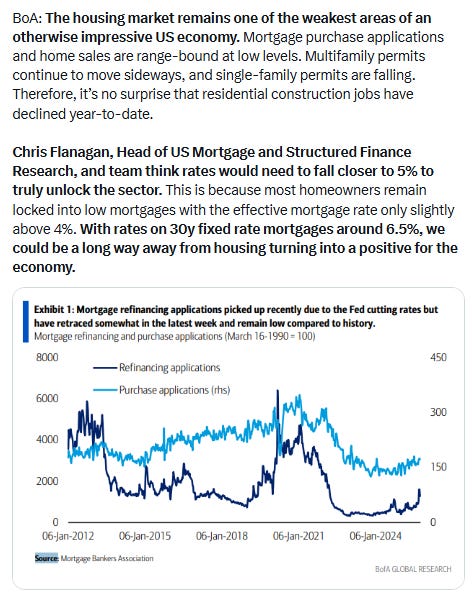

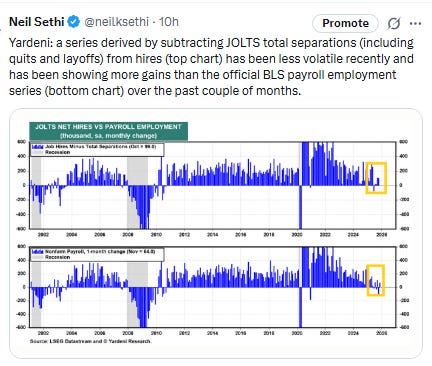

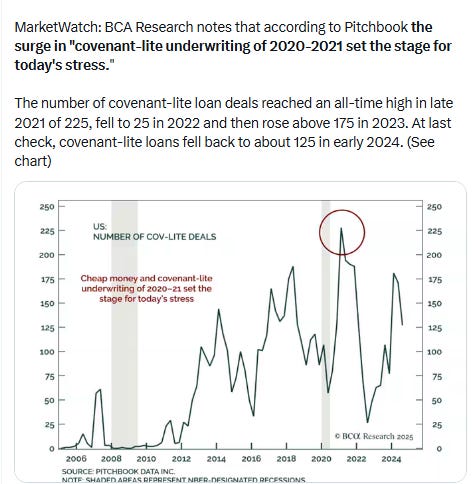

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts (all free).

In individual stock action:

Key chip stocks such as Nvidia and Micron Technology climbed in the session. The former rose more than 1%, and the latter popped more than 10%. Both artificial intelligence-related names were big winners in 2025 — Nvidia jumped about 39%, while Micron surged more than 240%.

But other areas in tech outside of chips suffered some losses. Notably, software stocks came under pressure, as Salesforce dropped more than 4% and CrowdStrike declined more than 3%. Palantir Technologies and Microsoft pulled back as well. Additionally, Tesla shares were more than 2% lower after the company’s fourth-quarter deliveries missed analyst estimates.

Friday’s session had some bright spots elsewhere in the broader market. Shares of Wayfair jumped around 6%, while RH increased roughly 8% after President Donald Trump on New Year’s Eve postponed tariff increases on upholstered furniture, kitchen cabinets and vanities for a year. The order specifically delays a 30% duty on upholstered furniture and 50% levy on kitchen cabinets and vanities, keeping in place a 25% tariff on those goods that was imposed back in September.

Corporate Highlights from BBG:

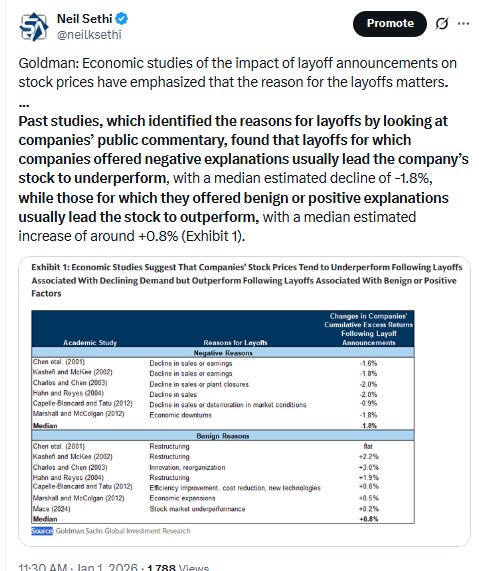

Mega-cap tech companies led a disproportionate share of the US stock market’s gains in 2025. Their executives also accounted for an outsized share of insider selling as billionaire founders, CEOs and directors took more than $16 billion off the table.

BYD Co. met its full-year sales target and likely surpassed Tesla Inc. to become the world’s largest electric-vehicle maker in 2025 — a milestone overshadowed by a challenging outlook for the Chinese auto market in the year ahead.

Orsted A/S filed a legal complaint after the Trump administration suspended the lease of a wind project that’s near completion off Rhode Island.

Mid-day movers from CNBC:

In US economic data:

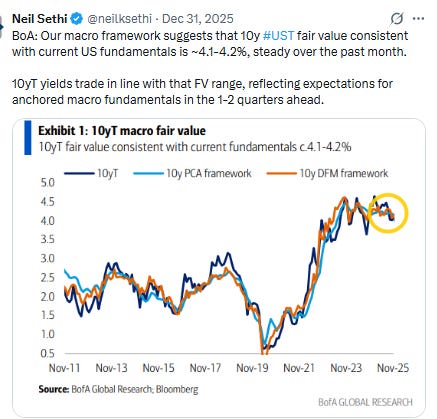

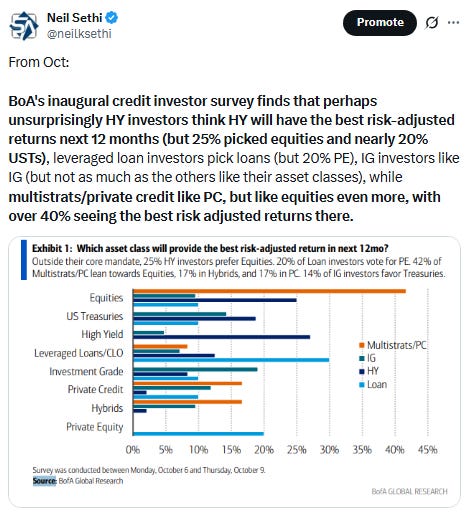

Link to posts for more details/access to charts (all free) - Neil Sethi (@neilksethi) / X

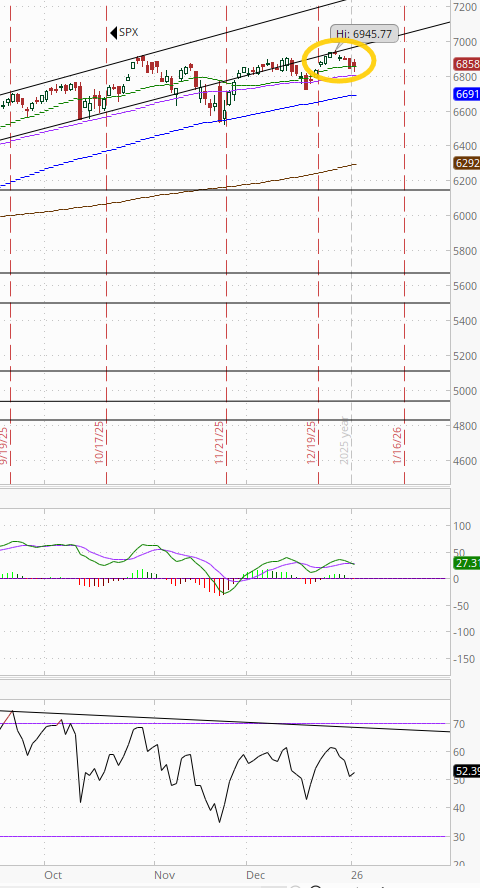

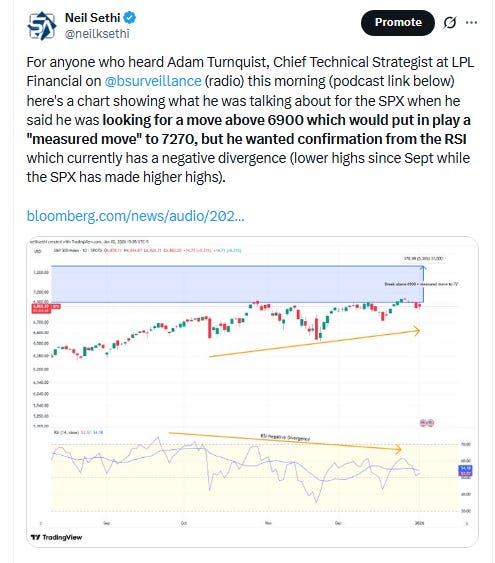

The SPX fell to a one-week low before recovering to finish just above the 20-DMA. The daily MACD has flipped back to a mild “sell longs” positioning, while the RSI is over 50 but both with negative divergences (lower highs, see post from Turnquist).

The Nasdaq Composite a similar story, although its RSI is just under 50.

RUT (Russell 2000) fell Wed to its 50-DMA where it was able to bounce Friday. It has a more pronounced “sell longs” MACD signal through, but the RSI remains around 50.

Monthly charts continue to look constructive, all with MACD’s that are in “go long” positioning.

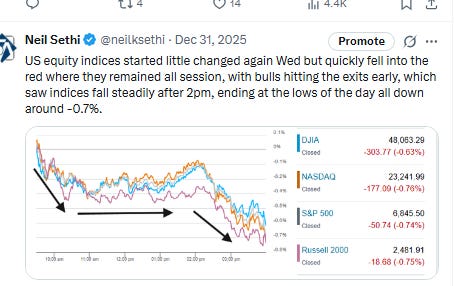

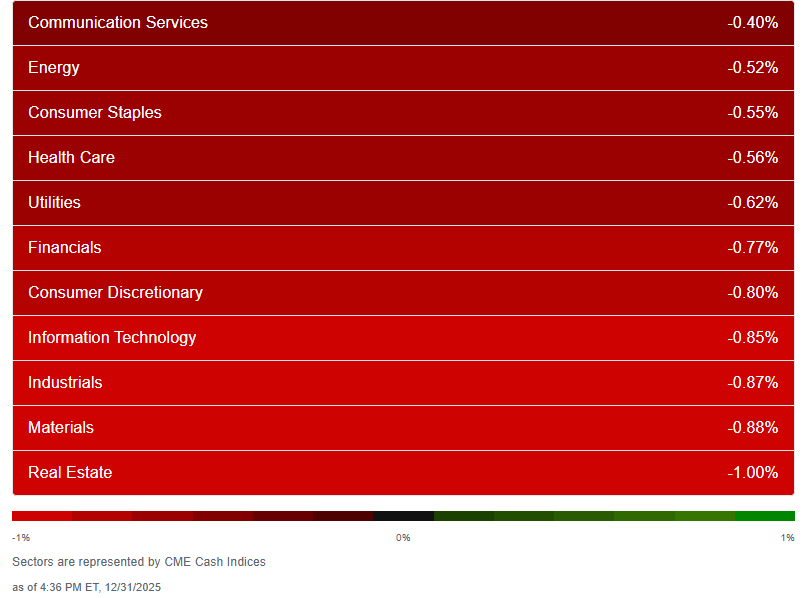

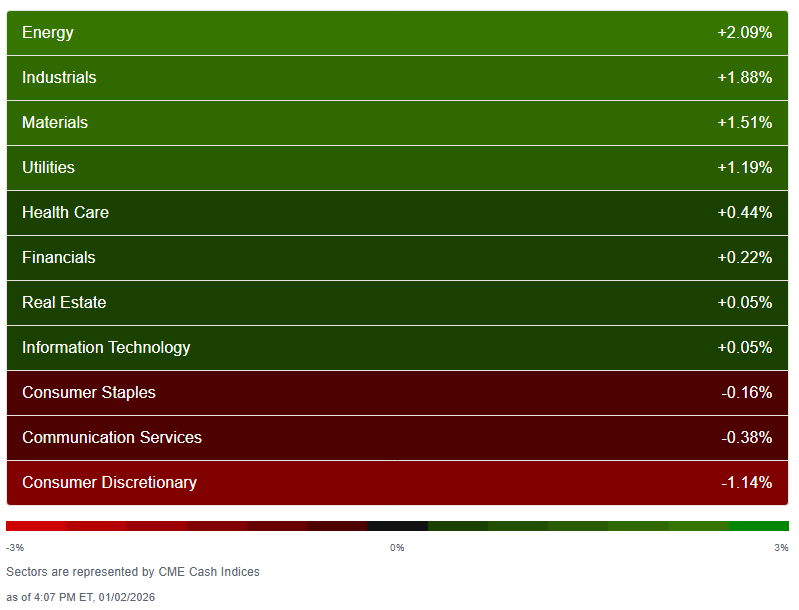

While the SPX was just modestly higher Friday, the results were weighed down by the megacap growth indices which all finished in the red (the only three red sectors) led by Cons Discr -1.1% (w/TSLA -2.5%, AMZN -1.9%) according to CME Cash Indices (uses futures prices).

Outside of those sectors, every sector was higher (8 of 11) a huge improvement from none Wed (w/every sector down at least -0.4%). Friday five sectors were up at least +0.4% and four over 1%.

Wed:

Fri:

SPX stock-by-stock flag from @finviz_com also a very different look from Wed (when just 17 stocks total were green and just three up over a half percent) with plenty of green particularly in Energy, Industrials, Utilities, and Materials. Other sectors were more mixed. Tech an interesting one with a clean bifurcation between semiconductors (very green) and software (very red).

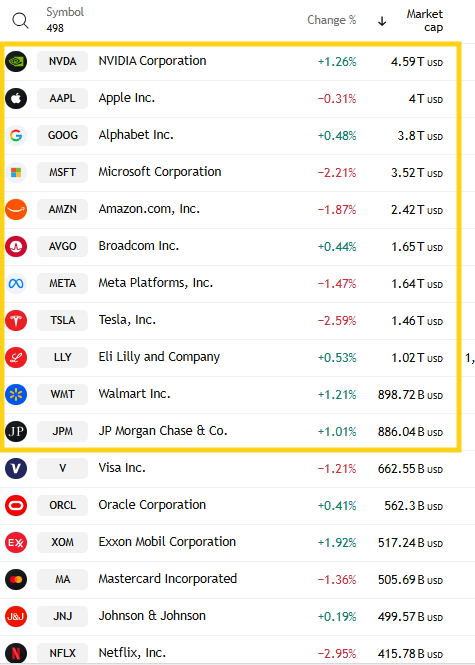

5 of the top 11 were lower (after all 11 Wed (and 24 of the top 25 with just JNJ (+0.02%) higher)). TSLA led to the downside -2.6%, now down over -12% since its intraday high Dec 22nd. Leading gainer was NVDA +1.26% edging out WMT +1.21%. Mag-7 was -1% and -3.9% for the week (worst since April).

68 SPX components were up 3% or more after a total of just four total the week coming into Friday led by 2026 winner SanDisk SNDK +16% followed by the other top stocks from 2026 MU +10.5% and WDC +8.9%. Sixteen >$100bn in market cap up 3% or more (after only one in the previous four sessions total) in MU, LRCX, INTC, BA, KLAC, IBKR, CAT, AMD, GE, GS, GEV, CEG, APH, COP, BX (in descending order of percentage gains).

20 SPX components down -3% or more (up from 4 Wed, 2 Tues three Mon, one last week) led by Applovin APP -8.2% (which also led to the downside Tues). Nine >$100bn in market cap down -3% or more (after seeing just one the prior six sessions) in APP, PGR, PLTR, INTU, ADBE, CRM, NOW, CRWD, ACN (in order of percentage losses). NFLX just missed -2.95% despite the success of Stranger Things.

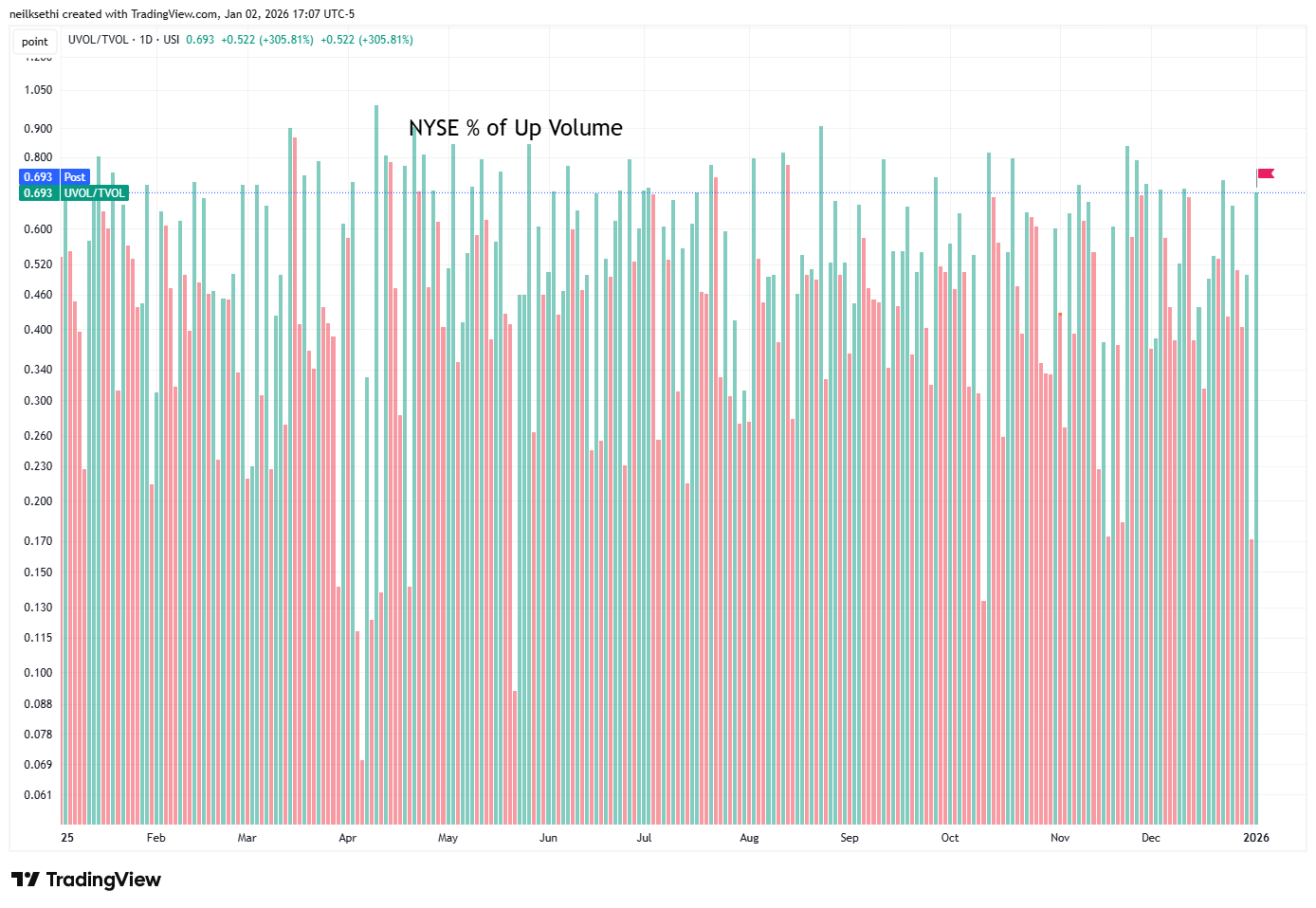

Unlike the SPX, the NYSE composite index was up +1.04%, which saw NYSE positive volume (percent of total volume that was in advancing stocks (these also use futures)) improve to 69.3%, the best since Dec 22nd (although the index was only up +0.85% that day).

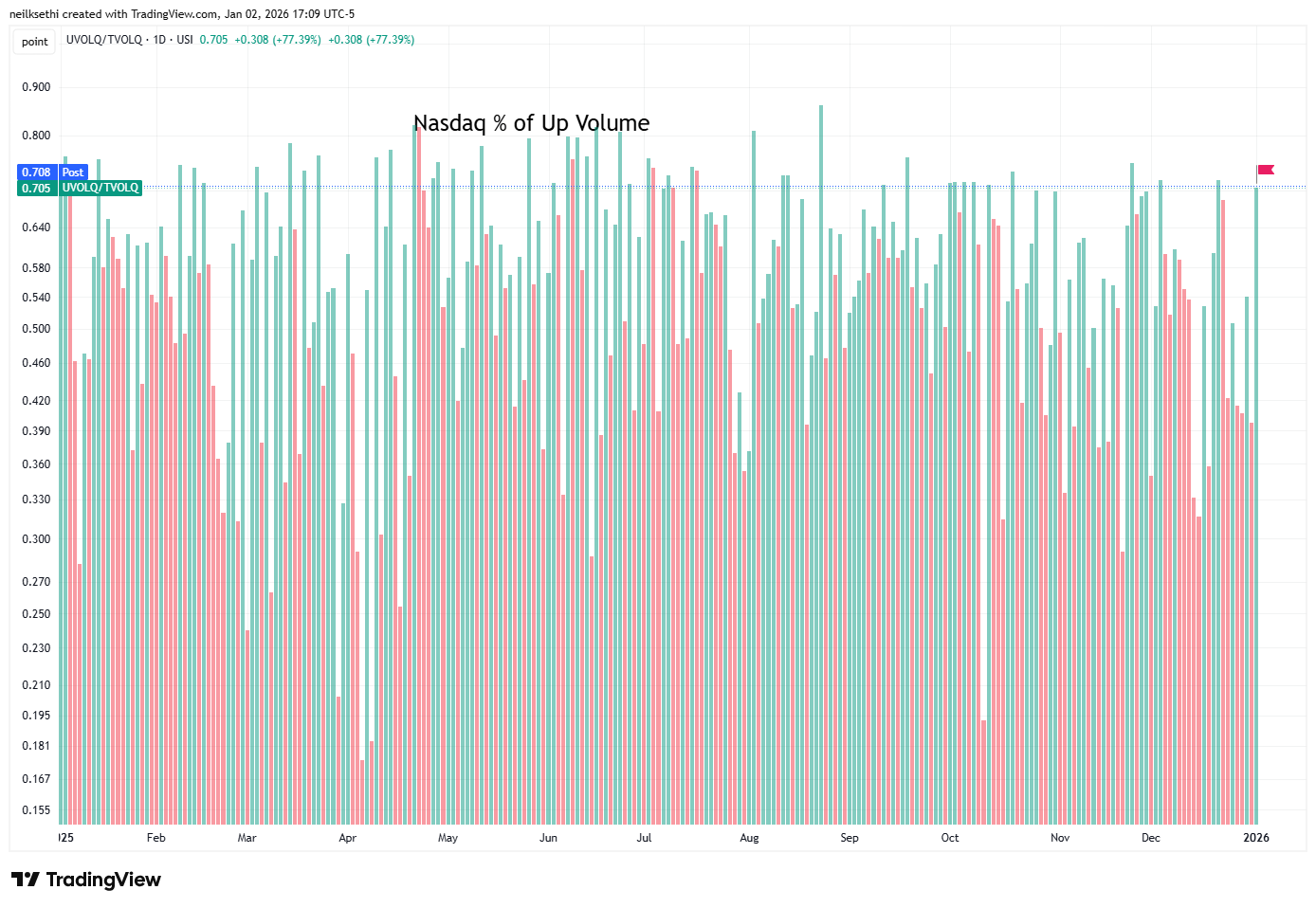

But Nasdaq positive volume (% of total volume that was in advancing stocks) was similarly strong at 70.8%, the best since Dec 19th, even as it lost -0.03% Friday vs gaining +1.31% that day.

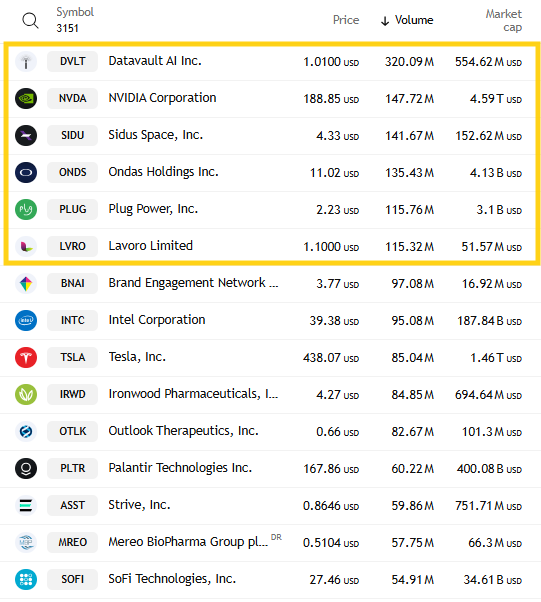

Which of course made me think we probably had higher speculative volumes on the Nasdaq, but those fell back from Tuesday’s elevated levels. The top three stocks by volume on the Nasdaq collectively traded a little over ~600mn shares, down from 1.3bn Tuesday and ~700mn a week ago, making the Nasdaq positive volume number that much more impressive. 6 companies had volumes over 100mn shares the same as Tues but down from 8 Mon.

Positive issues (percent of stocks trading higher for the day) which are not as inflated by penny/meme stocks still lagged though on the Nasdaq at 60.4% while the NYSE was closer at 66%.

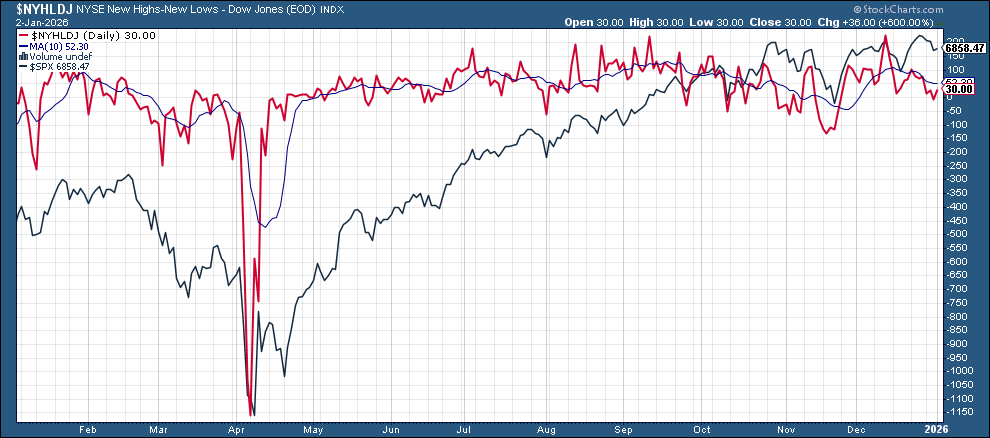

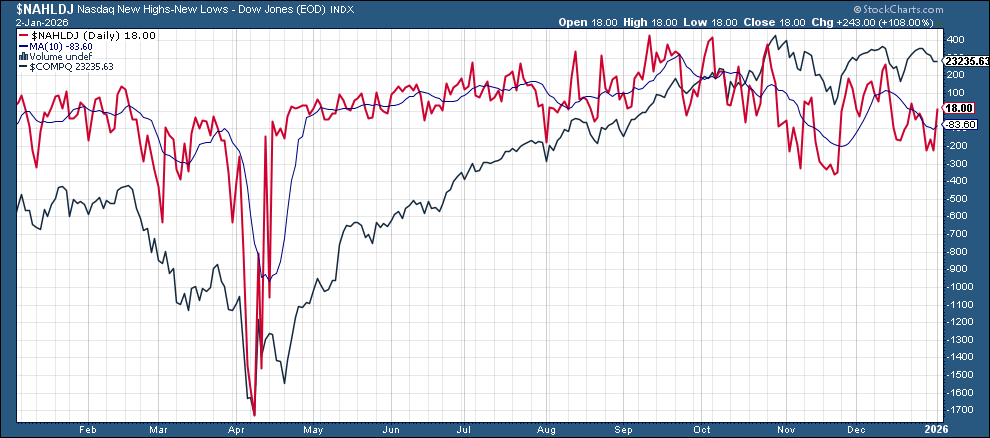

New 52-wk highs minus new 52-wk lows (red lines) improved from the least since November to 30 from -6 on the NYSE and to to 15 from -227 on the Nasdaq.

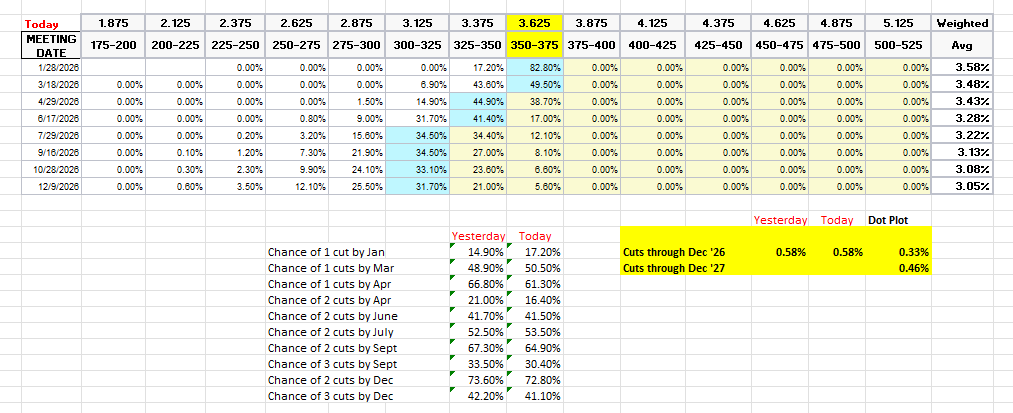

#FOMC rate cut pricing edged higher (more cuts) according to the CME’s Fedwatch tool. Probability of a cut in Jan remains low at 17% (up slightly from the recent low of 13% last week, the least since pre-Dec FOMC), with the first cut in March at 51% (from 47%). A second cut is in July at 54%.

Pricing for 2026 overall remained at 58bps, with pricing for two cuts 73% and three cuts 41%, down from 68bps Dec 3rd (and 80bps mid-Nov which was highest we’d been for 2026 cuts)).

The dot plot as a reminder has just 33bps for the average dot for 2026.

Remember that these are the construct of probabilities. While some are bets on exactly one, two, etc., cuts some of it is bets on a lot of cuts (3+) or none (and may include a hike at some point).

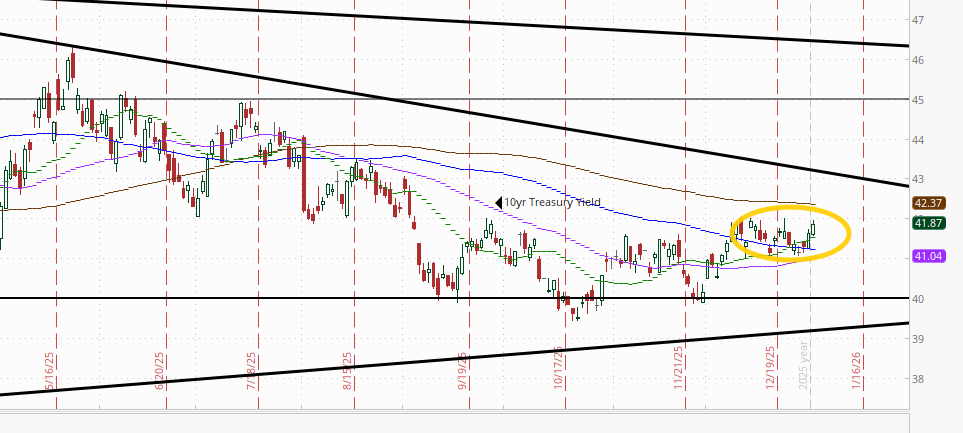

The 10yr #UST yield now up to 4.19% from to 4.13% Tues, now at the top of its range since the start of December.

Monthly chart has the same wedge as the weekly chart.

The 2yr yield, more sensitive to FOMC rate cut pricing, ended the week at 3.48%, just above the 2-month low and 6bps above the least since 2022. It remains in the channel it’s been in since the start of 2024, -15bps below the Fed Funds midpoint. Outside of recessions it is normally above by around +50bps on average, so still calling for at least a couple more rate cuts.

The Effective Fed Funds Rate (red line) remained at 3.64%.

This seems like a fairly rich yield at these levels unless we really aren’t going to get any more rate cuts (then it’s a bit expensive (i.e., yield should be higher)). That said I just don’t know that I want to buy 2-years at what is basically the 1-month yield.

Monthly chart has the same channel as the weekly chart.

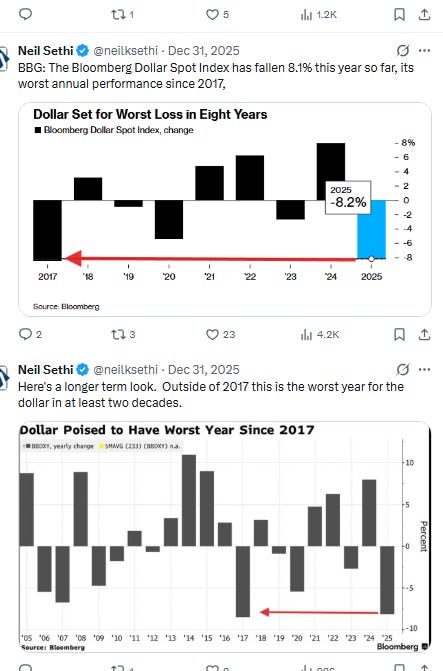

The $DXY dollar index (which as a reminder is very euro heavy (57%) and not trade weighted) up for a third session to a 1-week high and now over its short-term downtrend line from the Nov peak. The daily MACD has now crossed to “cover shorts” positioning and the RSI is the best since Nov (although still under 50).

Monthly chart like the weekly has competing channels, but the MACD tilts negative.

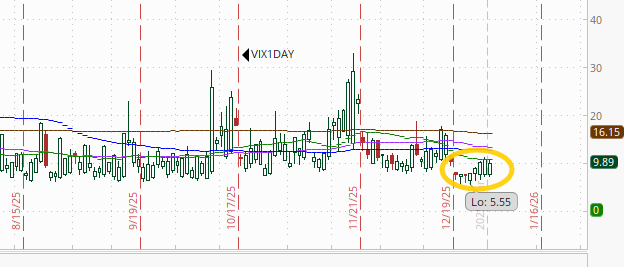

VIX edged up to 14.5, but still remains around the lows of 2025. The current level is consistent w/~0.91% average daily moves in the SPX over the next 30 days.

The VVIX (VIX of the VIX) edged lower but only after climbing the past week to 90.1 from 81.7, which was the least since July ‘24 (before the carry trade blow-up). The current level remains consistent with “moderate” daily moves in the VIX over the next 30 days (historically normal is 80-100, but we’ve been above 90 almost the entire time since July ‘24)).

Despite the weekend, the the 1-Day VIX remained at 9.9. The current reading implies a ~0.63% move in the SPX next session.

#WTI futures again not able to clear the resistance they have struggled with since the start of Oct (50-DMA and downtrend line from the July highs). As I said a week ago, “like several previous times the daily MACD crossing to ‘cover shorts’ and the RSI moving over 50 weren’t enough [so far at least] to push it through.”

Monthly chart like the weekly chart not favorable.

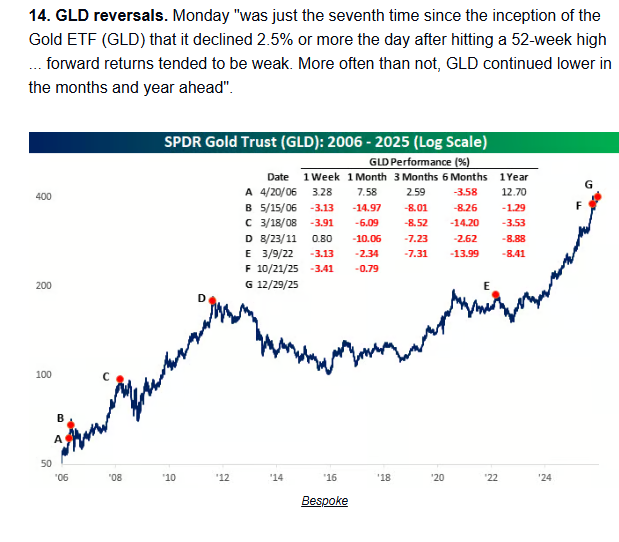

Gold futures (/GC) again not able to bounce (but also not pulling back further) after their largest pullback since October on Monday.

As noted then, “like [the October pullback], the RSI fell from well over to well under 70, and the daily MACD has crossed over to ‘sell longs’ positioning. After that plunge, gold futures drifted lower over the following week or so before resuming the uptrend. We’ll see if we get something similar here.” So far not so much.

Monthly chart looks just as strong as the weekly chart. Another monthly all-time closing high.

US copper futures (/HG) not able to follow through on their bounceback Tuesday from Monday’s losses, still remaining not far from record closing highs. Similar to gold the RSI went from well over to under 70, but the daily MACD has not crossed over from “go long” positioning.

Longer term, copper futures remain in the grinding uptrend since August (and longer than that in the uptrend started in March 2020).

Monthly chart as noted continues to look favorable with December easily setting an all-time monthly closing high.

Natgas futures (/NG) dropped again, all the way to the 200-DMA where they found their footing, but now down -35% from the intraday high Dec 5th to the lowest close since Oct 28th. The daily MACD remains in ‘sell longs’ positioning, and RSI is the weakest since Aug.

Monthly chart continues to favor an uptrend.

Bitcoin futures finally able to close over $90k for the first time since Dec 12th. The daily MACD remains in “cover shorts” positioning, and the RSI is now at 50 and the strongest since Oct.

Monthly chart not yet favoring a sustained uptrend.

The Week Ahead

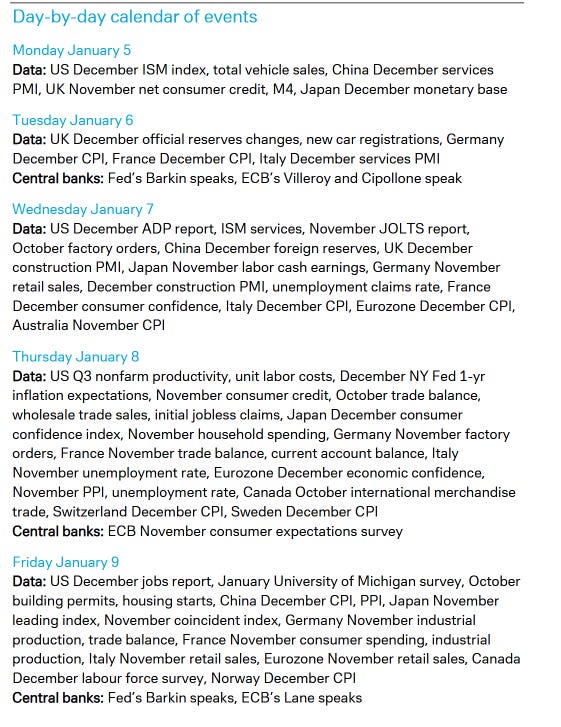

We’ll jump into 2026 with both feet next week as we get our normal first week of the month reports with a focus on the labor market and a return to “jobs Friday”. But as usual, before we get there, we’ll get Dec ADP, Nov JOLTS, and weekly jobless claims. And, as usual, we’ll get the Dec ISM PMIs (and S&P final services), auto sales, and as we often get the first week, reports on the trade deficit and factory orders, but for Oct (so a month late).

But we’ll also get some reports we don’t normally get the first week as the shutdown delayed 3Q productivity report comes in (an important report given the Fed’s new focus on this subject as a reason rate cuts may be appropriate despite strong growth), and due the upcoming Friday being the second Friday of the month, we’ll also unusually get Nov consumer credit and the preliminary UMich consumer sentiment survey on jobs week, along with the normal weekly mortgage applications and EIA petroleum and natgas inventories reports. So lots of data to kick off 2026.

Fed speakers on the official calendar are light with just Fed Gov Bowman (who is now officially out of the running for Fed chair, so we’ll see if her tone changes), Philadelphia Fed Pres Paulson (on Sat) and Richmond Fed Pres Barkin (twice), but I’m sure there will be a lot more.

No non-Bill Treasury auctions (>1yr in duration) until they pick back up the following week.

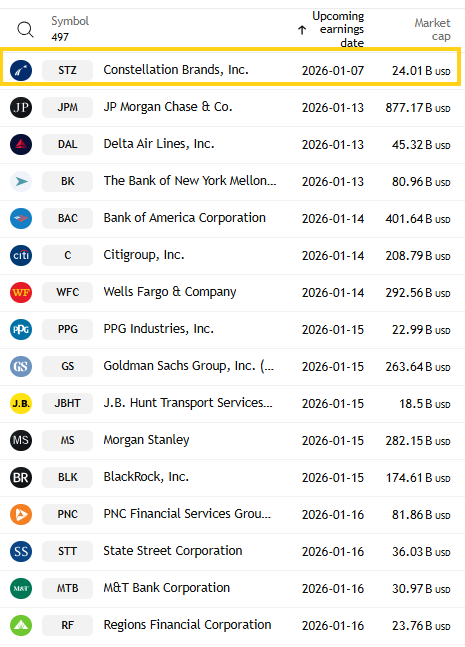

Similarly, just one SPX earnings report next week in Constellation Brands (STZ), but the following week we’ll kick off 4Q earnings season with JPM on the 13th.

Also, next week we have the CES (consumer electronics show) in Las Vegas. This has morphed into a tech confab which in addition to all the new products is led by a kick-off speech from Nvidia’s CEO Jensen Huang that has proven to be market moving in the past. He speaks Monday.

Ex-US we’ll also get the normal first week of the month data filled with inflation, employment, consumer, and other reports from around the globe. DB’s one-pager is below.

Link to X posts - Neil Sethi (@nelksethi) / X

To subscribe to these summaries, click below (it’s free!).

To invite others to check it out,