Markets Update - 2/19/26

Detailed update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with lots of charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!),

Link to posts - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog. Also please note that I do often add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

Finally, if you see an error (a chart or text wasn’t updated, etc.), PLEASE put a note in the comments section so I can fix it.

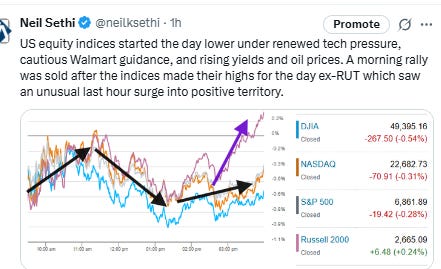

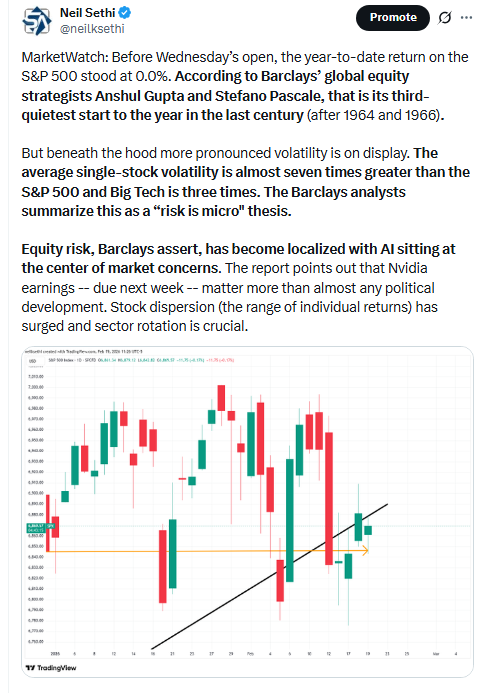

US equity indices opened today modestly lower under pressure from tech not extending on Wed’s rally, megacap Walmart slipping following tepid guidance (seeing those shares end the day down over -1%), and increasing bond yields (which would reverse) and oil prices (which would stick) along with general geopolitical unease as Pres Trump continued to escalate rhetoric towards Iran while a huge array of US forces gathers in the Middle East, including two aircraft carriers, fighter jets and refueling tankers leading some news outlets like Reuters to say it is "a matter of time" before what could be an extended US attack.

A morning rally was sold and marked the highs for the big cap indices who all finished lower, which the small cap Russell 2000 was on track to do as well before an unusual last hour surge vaulted it into positive territory.

Elsewhere, bond yields were little changed, but the dollar pushed to a 2-week high. Crude moved to the highest close since Aug, and bitcoin saw a small gain, while gold copper, and natgas all were modestly lower (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was -0.3%, the equal weighted S&P 500 index (SPXEW) -0.3%, Nasdaq Composite -0.3% (and the top 100 Nasdaq stocks (NDX) -0.4%), the SOXX semiconductor index -0.5%, and the Russell 2000 (RUT) +0.2%.

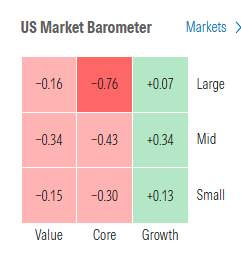

Morningstar style box interestingly just had growth (mildly) in the green.

Market commentary:

“What’s really interesting is that there seems to be no long-short strategy at play,” said Alexandre Baradez, chief market analyst at IG in Paris. “This will continue at least until the next earnings season when we’ll get more insight. In the meantime, all eyes will be on Nvidia’s results next week.”

“A rebound in mega‑cap stocks, along with a pause in the rotation and broadening theme that has defined market performance this year, would not be surprising in the weeks ahead,” said Edward Jones senior global investment strategist Angelo Kourkafas. “Selling has been broad and indiscriminate, and in some cases, valuations may already reflect a substantial degree of disruption risk relative to current fundamentals,” he added. To be sure, Kourkafas said that even as pessimism in the tech sector has likely become overstated, the prospect of the group “regaining sustainable leadership remains doubtful” as the macroeconomic environment continues to favor cyclical stocks.

February is known to be a tougher month for stocks, and this year doesn’t look too different, according to Ryan Detrick, chief market strategist at Carson Group. “After a 9-month win streak on the Dow, it makes sense that February is a choppy, aggravating month,” Detrick said early Thursday, noting that tech shares were lower in the large-cap sector, but that mid-cap and small-cap tech was holding up. Detrick said investors also were in a wait-and-see mode about what actions the U.S. might take against Iran, potentially as soon as the weekend. “The stock market’s been fairly calm all things considered.”

“The big news of the week will likely be the Personal Consumptions Expenditures (PCE) release tomorrow, because it is the Fed’s preferred inflation measure and the big argument within the Fed is whether or not to proactively lower rates to support the job market, or to keep rates higher for longer in order to fight inflation,” said Chris Zaccarelli, chief investment officer for Northlight Asset Management in Charlotte, N.C. “Tomorrow’s report should provide another look at inflation and add to the debate.”

“Oil and Iran are dominating the backdrop for today’s mixed markets, in which USD remains bid, oil has jumped another 1%, bond yields are rising and stock markets are mixed, with APAC bid, EMEA offered and U.S. futures flat, Bob Savage, head of markets macro strategy at BNY, said in a Thursday client note.

“Whether oil breaks through $68/barrel (WTI) and sparks more fear about inflation going up may be a factor to watch for fixed income markets, but for the dollar the linkage appears to be changing.”

“Crude oil prices are rising on the anticipation of possible military action in Iran,” said Louis Navellier at Navellier & Associates. “The US and Iran are expected to meet again, and those negotiations are expected to be closely watched.”

With Iran’s military proxies greatly weakened and the economy in crisis, the country doesn’t find itself in a very strong negotiating position, so the markets likely expect a diplomatic resolution, according to Dennis Follmer at Montis Financial. “Right now, stocks have not priced-in the tensions between the US and Iran and that seems appropriate,” he said. One of the biggest threats to stocks from the Iran situation would be if they were to shut down the Strait of Hormuz - a key global shipping lane. Follmer bets this is a “low probability risk,” given the amount of US military assets gathering in the region and Iran’s economic need to get oil out through the strait. “Given the likelihood of a diplomatic solution and that the resulting volatility from an actual armed conflict would be fairly contained, we think any portfolio changes are unwarranted,” Follmer noted.

“Lots of discussion around potential geopolitical conditions that could come to a head this weekend. I wouldn’t be surprised that unless we get a clear narrative that nothing is going to happen, the market could have a very risk-off move on Friday as we head into the weekend,” Victoria Fernandez, chief market strategist at Crossmark Global Investments told MarketWatch. "Tech pulling back and some broadening occurring in the market serve as tailwinds to the bull market, and give investors a chance to rotate out of some existing overweights to tech and move into sectors that have lagged but are showing signs of positive trends, including energy, staples and industrials," Fernandez said. "However, these sectors do appear to be overbought, and we would wait for a pullback to enter."

“Oil markets rarely wait for tankers to stop moving before reacting,” said Stephen Innes, managing partner at SPI Asset Management, of concerns around a potential U.S.-Iran conflict and the risks of oil disruptions through the critical Strait of Hormuz. “In oil, perception often moves the market before reality does correctly or incorrectly, but we should find out soon.”

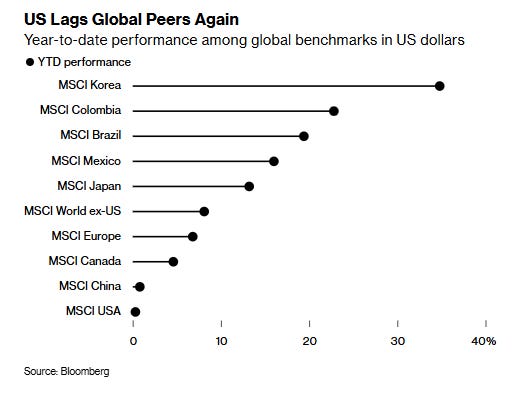

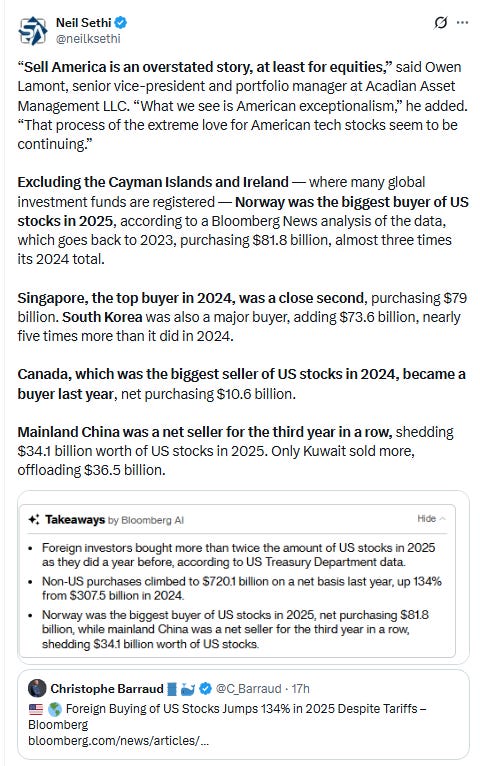

“Despite the healthy foreign inflows into US markets, US stocks are still dead last in a global ranking of benchmarks again this year. No matter how you look at it, US assets are underperforming as the US economy has so far been paying the biggest price for the trade war, and a broadening of earnings growth globally will make this trend difficult to reverse.” —Tatiana Darie, Macro Strategist, Markets Live

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

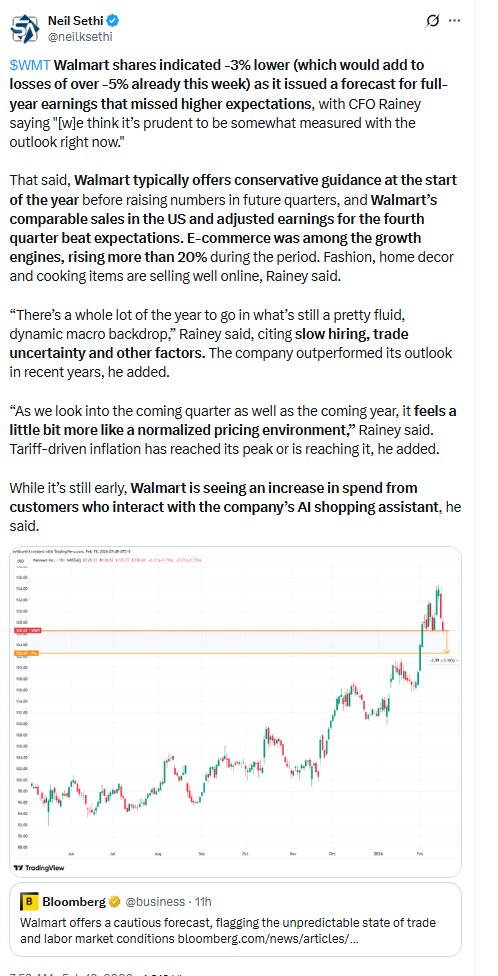

Adding to the downbeat sentiment Thursday, Walmart shares were down more than 1% after the company’s full-year earnings outlook fell short of expectations. This overshadowed better-than-expected results for the fourth quarter.

Investors moved out of private credit stocks after private market and alternative assets manager Blue Owl Capital announced it’s going to tighten investor liquidity following its sale of $1.4 billion in loan assets, spurring worries among investors about losses in the murky private loans area. That stock declined about 6%, while others such as Blackstone and Apollo Global Management were each down more than 5%.

Alongside asset managers, software was another area under pressure. Salesforce shares were lower by more than 1%, while Intuit shares fell roughly 2%. Shares of Cadence Design Systems declined nearly 3%.

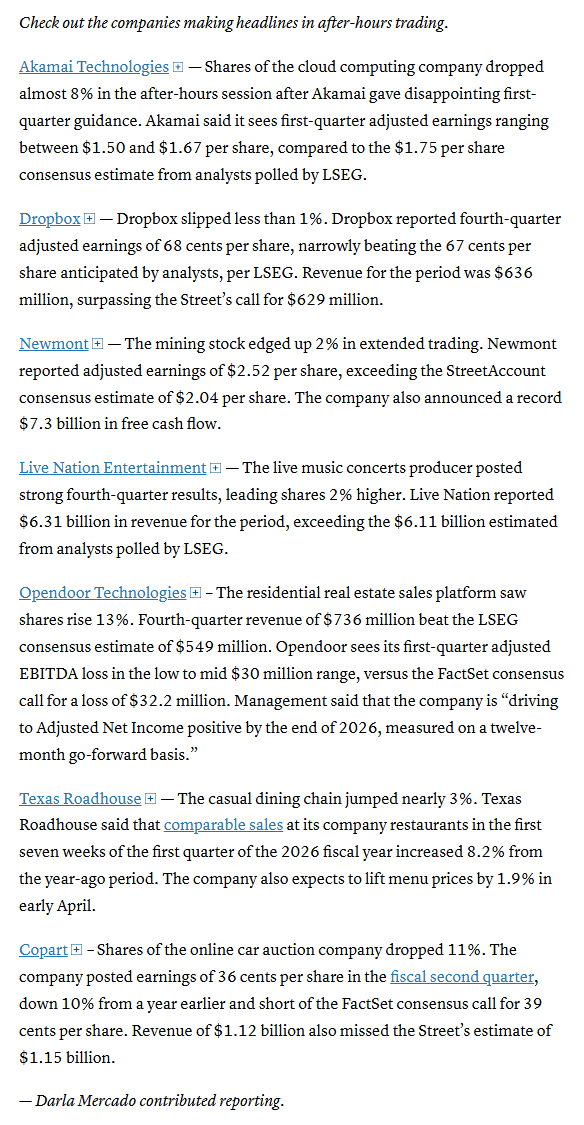

Companies making the biggest moves after-hours from CNBC.

Corporate Highlights from BBG:

Amazon.com Inc. has officially dethroned Walmart Inc. as the biggest global company by revenue, a milestone attesting to the massive scale the e-commerce and cloud-computing giant has achieved since its humble beginnings in 1994 as an online bookseller in Jeff Bezos’ Seattle-area garage.

West Virginia sued Apple Inc. Thursday, alleging it has knowingly allowed users to store and distribute child sexual abuse material on its iCloud platform.

New York Governor Kathy Hochul has pulled a proposal that would have allowed for commercial robotaxi services outside New York City, a blow to Alphabet Inc.’s Waymo as it seeks to aggressively expand its driverless fleet this year.

OpenAI is close to finalizing the first phase of a new funding round that is likely to bring in more than $100 billion, according to people familiar with the matter, a record-breaking financing deal that would give the startup additional capital to build out its artificial intelligence tools.

AppLovin Corp. is preparing to build a social networking platform after the mobile advertising company’s failed bid to buy TikTok’s assets outside of China last year.

JPMorgan Chase & Co. said President Donald Trump improperly named the bank’s chief executive officer, Jamie Dimon, as a defendant in his lawsuit over closure of his accounts in order to file the case in Florida state court.

Bank of America Corp. is committing $25 billion to private-credit deals, joining its Wall Street rivals in putting its own balance sheet behind lending in the fast-growing market, according to people with knowledge of the matter.

Morgan Stanley chopped pricing in half for clients trading private companies’ shares on its newly acquired EquityZen platform, undercutting competitors as it looks to expand in a growing market.

CME Group Inc. is moving closer to crypto’s always-on trading model, saying it will allow futures and options on digital assets to trade 24 hours a day later this year.

Johnson & Johnson is preparing a potential sale of the orthopedics unit that it has been planning to separate, with big buyout firms already circling, according to people familiar with the matter.

Ted Sarandos, co-chief executive officer of Netflix Inc., said his company’s acquisition of Warner Bros. Discovery Inc. will lead to more films in theaters, addressing a key complaint from Hollywood in the high-stakes battle for one of the industry’s iconic studios.

Deere & Co., the world’s largest farm-machinery maker, boosted its annual profit outlook, anticipating a long-awaited upturn in the agriculture economy.

DoorDash Inc. gave an outlook for orders in the current quarter that surpassed Wall Street’s expectations, a testament to its efforts to expand business beyond restaurant takeout.

Carvana Co.’s higher-than-expected costs dented its fourth-quarter profit in a sign of growing pains as the company pursues rapid growth.

Figma Inc., a creative software maker, gave an annual revenue outlook that topped estimates, easing Wall Street anxiety that the business is threatened by the emergence of rival artificial intelligence products.

Six Flags Entertainment Corp. reported 2025 earnings and revenue that were slightly ahead of analyst estimates as the amusement park operator works to rebound from lackluster attendance.

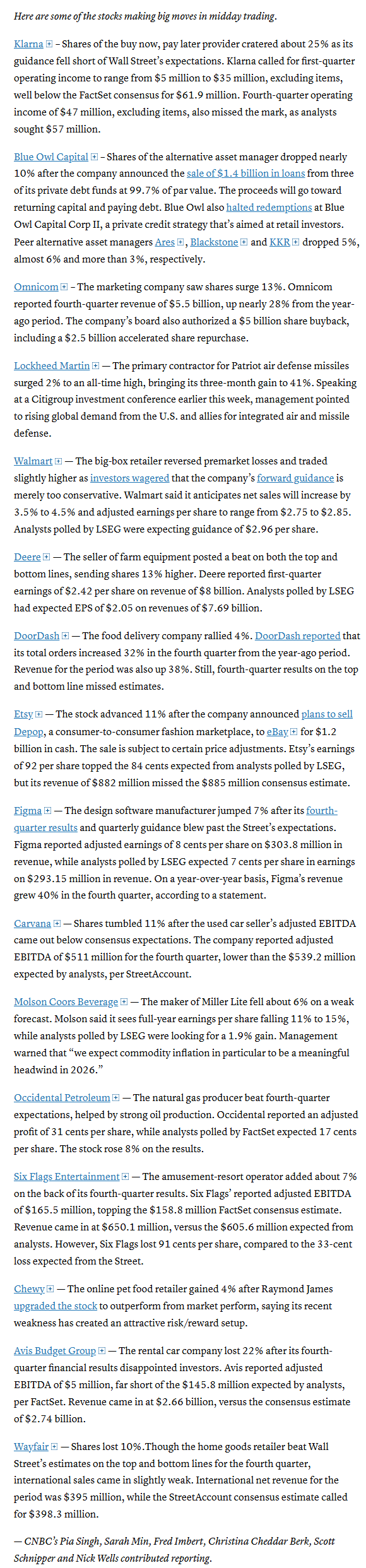

Mid-day movers from CNBC:

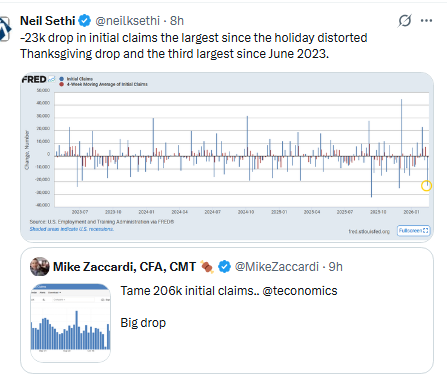

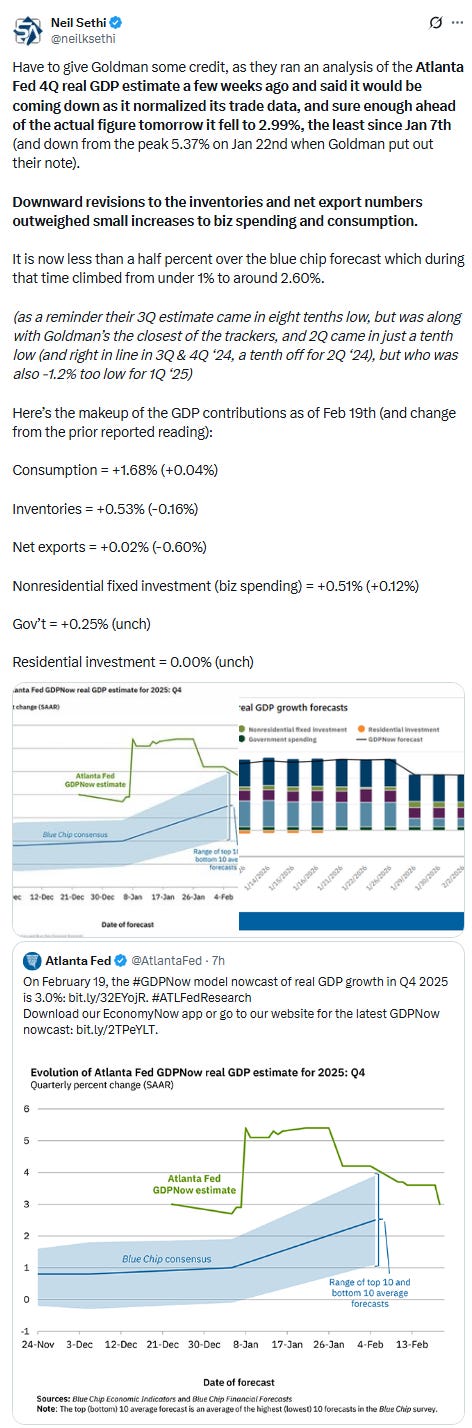

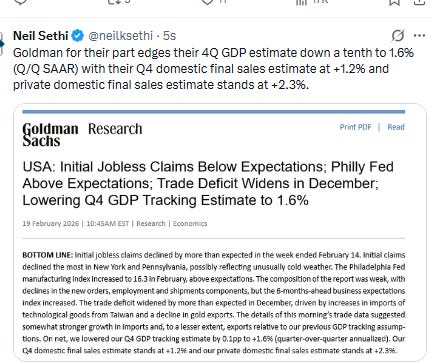

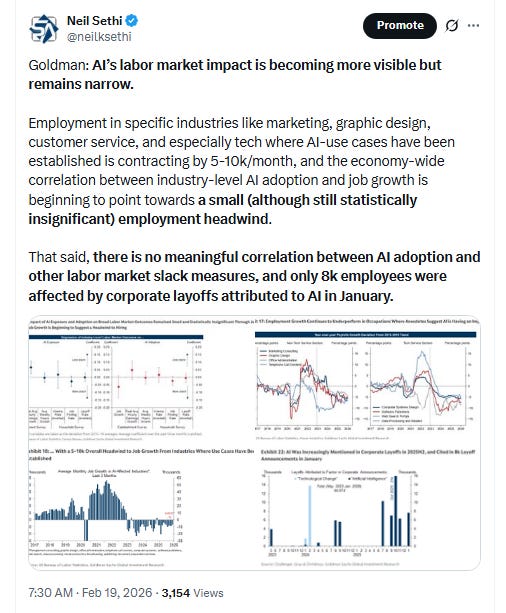

In US economic data:

Substack articles:

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X