Markets Update - 2/2/24

Update on US equity and bond markets and select commodities with charts!

To subscribe to these summaries, click below (it’s free!).

To invite others to check it out,

Link to today’s tweets - Neil Sethi (@neilksethi) / X (twitter.com)

US large cap equities continued their bounce fueled by big tech earnings which overcame a jump in yields and the dollar following a blowout headline on the Non-Farm Payrolls report which saw a full cut priced out of 2024 Fed rate cut expectations. Unfortunately small caps don’t have giant tech stocks to help them out and suffered for it although the losses were less than what we saw on Wednesday. The Vanguard Mega Cap Growth ETF (MGK) was +2.2% (and the SOX semiconductor index +1.3%), the Nasdaq Composite +1.7% (and the top 100 Nasdaq stocks (NDX) +1.7%), while the market-cap weighted S&P 500 was +1.1%, but the equal weighted S&P 500 index (RSP) was -0.1%, and the Russell 2000 -0.6%.

The Morningstar style box showed the weakness outside of the growth stocks.

Corporate news was mostly dominated by carryover from last night’s large tech earnings. Meta Platforms (META 474.99, +80.21, +20.3%) and Amazon.com (AMZN 171.81, +12.53, +7.9%) saw big gains following positive earnings news drove index level upside moves, along with strength in other mega caps like NVIDIA (NVDA 661.57, +31.30, +5.0%). Even Apple (AAPL 185.85, -1.01, -0.5%) briefly turned positive when the market was at session highs after being down as much as 4% earlier today following relatively disappointing outlook for fiscal Q2 iPhone sales. Exxon Mobil Corp. and Chevron Corp. surpassed earnings forecasts as bigger-than-expected oil output from shale fields (and for Exxon strong trading profits) helped cushion the blow from weakening crude prices, although only Chevron was up today.

Link to today’s tweets - Neil Sethi (@neilksethi) / X (twitter.com)

Economic data was dominated by the monthly Non-Farm Payrolls report which didn’t disappoint coming in almost double expectations on the headline with average hourly earnings a full 2x expectations. There were some caveats under the hood (particularly a continued fall in the workweek), but the headline is what drove the action today as we’ll go through. We also got the final read on the University of Michigan consumer sentiment survey which confirmed the preliminary read of a +27% 2-month jump in sentiment (one of the largest on record) with improvement on personal finances and inflation and 1-yr ahead inflation expectations remaining the least since 2020. Finally, we got December factory orders which saw core business spending come in as expected improving to an all-time high.

Link to today’s tweets - Neil Sethi (@neilksethi) / X (twitter.com)

The SPX (+1.1%) pushed back to new ATHs today consistent with yesterday’s note that “market continues to have a lot of momentum and support.” That caps the 13th up week in 14. Also, the gains the last two days have turned the daily technicals back to positive even if momentum is lower keeping that negative divergence in place.

On a weekly chart, the SPX is the most overbought since July 2021.

The Nasdaq Composite (+1.3%) also eked out a new 2yr high. It has a similar technical situation.

RUT (-0.6%) though not able to follow up with another green day, and its technical situation is much less constructive. Starting to get “fan lines” which are a technical pattern I’ll get into more if we get a third one.

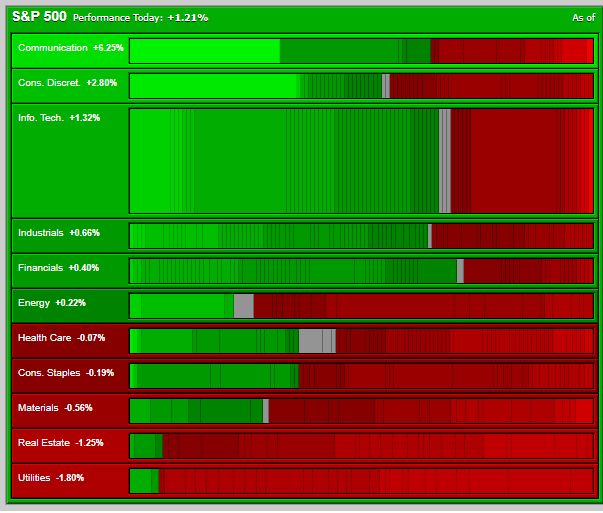

SPX sector breadth decelerated to just 6 of 11 sectors up with no non-growth sector up over +0.65%. The growth sectors all up at least 1.3%. Defensives lagged.

Here’s the stock-by-stock SPX chart from Finviz.

Positive volume really disappointing. NYSE just 31% and Nasdaq 43%. Issues were just 31 and 37%. New highs-new lows remained better on the NYSE with 123, still though down from 151 Wednesday (when the SPX was down 80 points) while Nasdaq was just 11 (it was 153 on Monday).

Yields jumped on the NFP report and pricing out of Fed cuts. The 10-yr yield ended up 17 basis points (so basically back to where it was on Wednesday) at 4.03% still down -13 basis points for the week though, the 2-yr note yield was up 19 basis points (so did get back all of the week’s decline) to 4.37%, and the 30-yr bond yield ended up 12 basis points at 4.22%, still down -14 basis points for the week.

Fed rate cut expectations as noted fell sharply pricing out almost a full cut for 2024. March fell to just 21%, a cut by May still is 72%, but that’s down from 96% yesterday, a June second cut is 66% from 97%, and a 3rd cut in July cut is 58% from 96%. The December 2024 implied rate is now 4.13% w/2024 rate cuts at 124 bps down from 147 yesterday.

The dollar after breaking lower yesterday had a huge reversal today closing the highest since December 11th. The daily technicals remain supportive.

VIX remains subdued.

WTI followed its first monthly gain since September with its worst week since November falling through key support. Daily technicals have also now turned negative, so not a great day.

Gold though was able to hold above support breaking its 6-day win streak. Daily technicals continue to be supportive.

Copper though also down, in its case for a third day, also to support. Daily technicals remain positive for now but are turning.

Nat gas continues to hold above the $2 level but that’s about the best I can say, and the daily technicals remain very negative.

More on Sunday.

Link to today’s tweets - Neil Sethi (@neilksethi) / X (twitter.com)

To subscribe to these summaries, click below (it’s free!).

To invite others to check it out,