Markets Update - 2/23/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with lots of charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!),

Link to posts - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog. Also please note that I do often add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

Finally, if you see an error (a chart or text wasn’t updated, etc.), PLEASE put a note in the comments section so I can fix it.

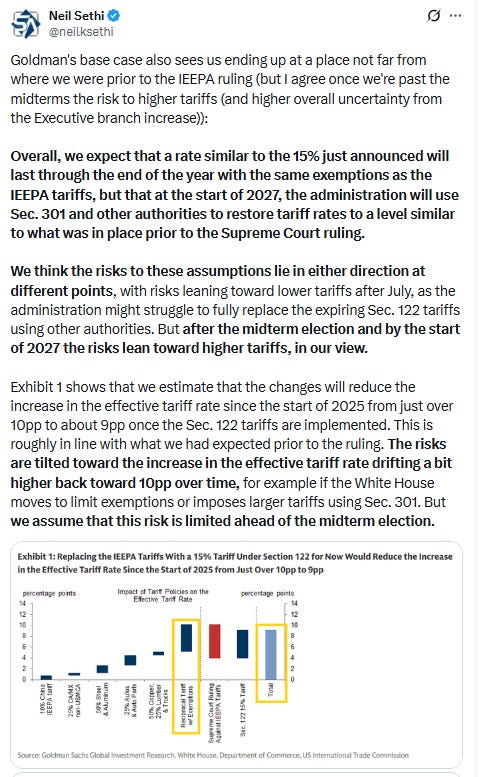

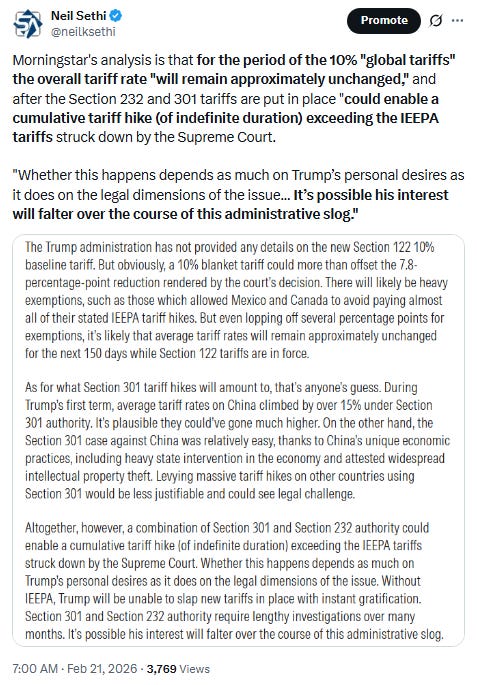

US equity indices opened the week lower as they continued to digest the ramifications from the Supreme Court removing Pres Trump’s IEEPA tariff powers Friday, following which the administration implemented a 15% “global tariff” over the weekend, with follow on posts from Pres Trump warning countries that he now had more power than before and cautioning them from backing away from recently negotiated trade deals with the US, saying that he would hit them with much higher duties under different trade laws that would be coming in the next few months.

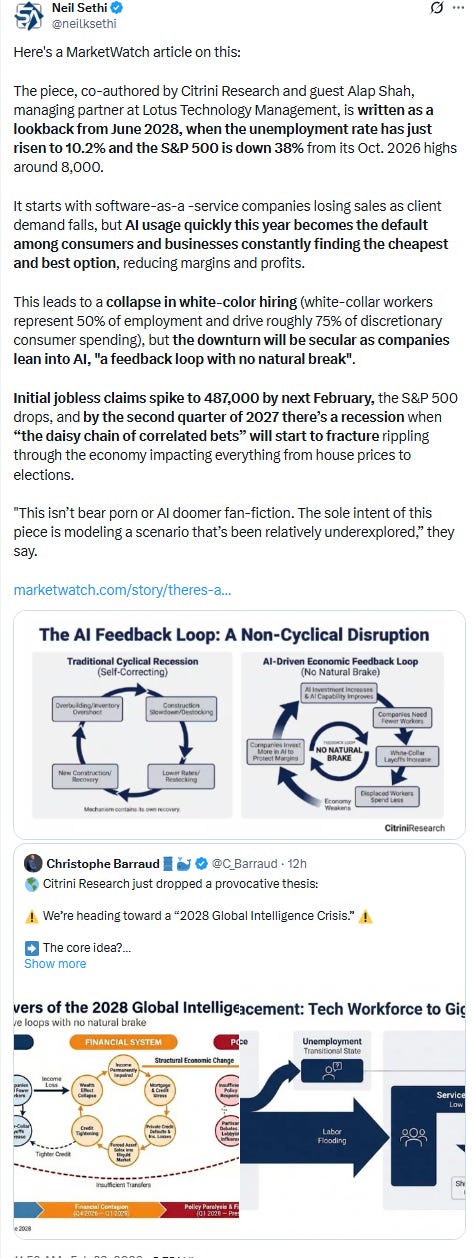

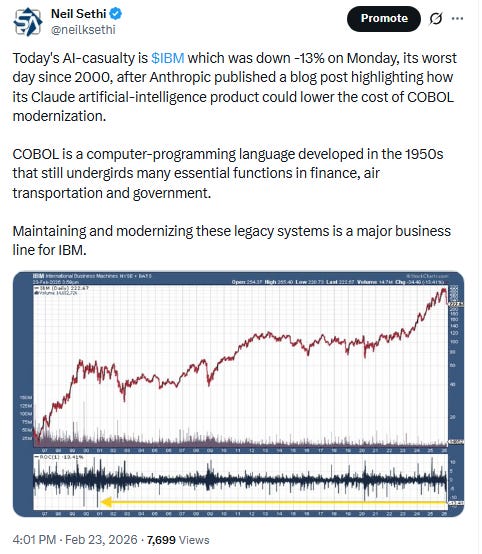

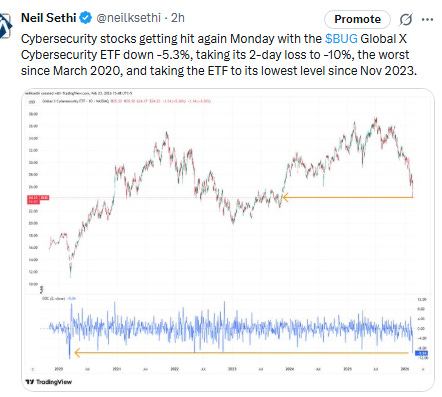

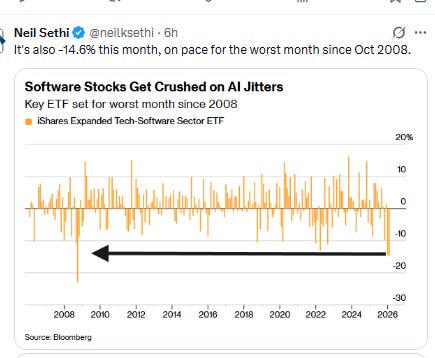

Meanwhile AI concerns also continued to reverberate with software and cybersecurity companies and asset managers getting hit again along with IBM (its worst day since 2000) on yet another tool released from Anthropic. Recession concerns also were raised by a a viral Substack post predicting spiking unemployment, a recession, and a bear market in stocks in the next two years as AI displaces white collar workers (see post below).

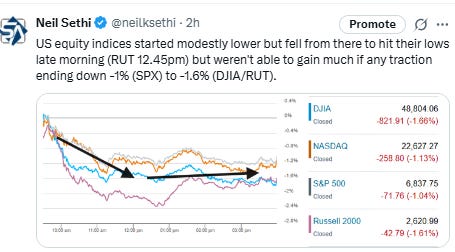

Equity indices fell from the open to hit their lows late morning (Russell 2000 (RUT) early afternoon) but weren't able to gain much if any traction from there ending down -1% (SPX) to -1.6% (DJIA/RUT).

Elsewhere, bond yields fell, while the dollar was little changed after its best week since November. Crude was also little changed after moving to the highest close since Aug last week, but gold pushed to its second highest close on record. Copper, natgas, and bitcoin all fell though (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was -1.0%, the equal weighted S&P 500 index (SPXEW) -1.1%, Nasdaq Composite -1.1% (and the top 100 Nasdaq stocks (NDX) -1.2%), the SOXX semiconductor index -0.6%, and the Russell 2000 (RUT) -1.6%.

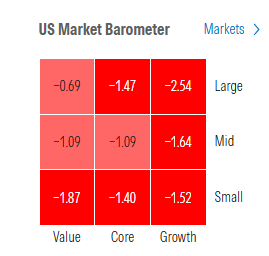

Morningstar style box all red with large value the only not down at least -1%.

Market commentary:

“Markets quickly realized that the ruling might not change much in the near term and will rather increase uncertainties,” said Stephan Kemper, chief investment strategist at BNP Paribas Wealth Management. “Donald Trump is not known to avoid a fight or give up easily.”

“The push and pull with tariffs is likely to be a distracting theme for markets for the remainder of the year, albeit with less volatility than the initial shock last April,” said Michael Landsberg at Landsberg Bennett Private Wealth Management.

“The question is about the benefit of the rebates versus the extra uncertainty that the trade issues are causing, and for me the latter wins,” JPMorgan Asset Management Global Market Strategist Hugh Gimber told Bloomberg TV. “That for me risks putting business activity on hold, because companies simply don’t know what’s to come further down the line.”

“Given the various economic risks and uncertainties that can be linked to the tariff drama, we expect the Fed’s wait-and-see approach to be reinforced,” said Ian Lyngen at BMO Capital Markets.

“Inflation looks to be challenging,” said Sam Stovall, chief investment strategist at CFRA. “And with Trump re-enacting across-the-board tariffs, that’s not going to help the inflation picture.”

President Donald Trump increasing global tariffs to 15% from 10% shouldn’t pose much of a threat to the economy, according to Angelo Kourkafas of Edward Jones. “In our view, the newly announced 15% tariff rate is unlikely to have a meaningful impact on economic activity, and we expect tariff rates to remain elevated compared to history, even after the Section 122 tariffs expire as the administration pursues other avenues to implement tariffs,” the senior global investment strategist said. “We advise investors not to overreact to headlines, and we reiterate our constructive outlook for global equity markets, supported by strong corporate profit growth and healthy economic activity,” he continued.

“The big question for the economy is what happens after this window, and if the tariff policy stays down this path, we may very well be back at the Supreme Court later this year,” said Michael Landsberg, chief investment officer at Landsberg Bennett Private Wealth Management. “The push and pull with tariffs is likely to be a distracting theme for markets for the remainder of the year, albeit with less volatility than the initial shock last April.”

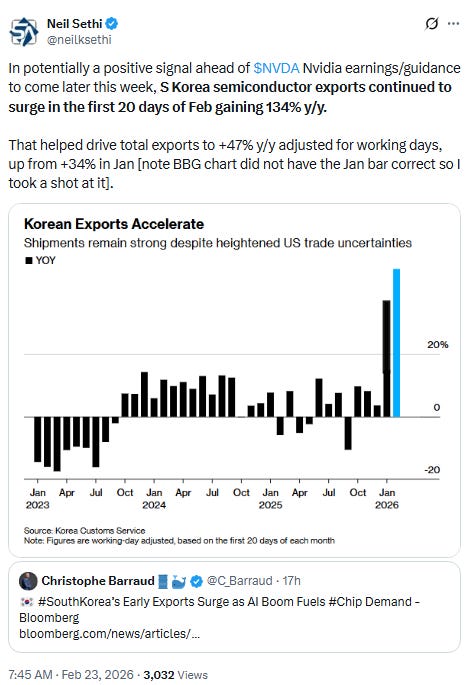

Sentiment around artificial intelligence is a “much bigger influence” on the stock market right now than tariffs, despite the Supreme Court’s Friday rejection of most of President Donald Trump’s tariffs imposed under the International Emergency Economic Powers Act, according to Sevens Report Research founder and president Tom Essaye. “That means this week is a potentially important one for the rally because of AI earnings,” Essaye said in a Monday note. Key software companies releasing quarterly results this week include Workday on Tuesday and Salesforce on Wednesday, with “solid reports” needed to stabilize the iShares Expanded Tech-Software Sector ETF, he wrote. Also, AI-chip maker Nvidia will report its fourth-quarter results on Wednesday, with the giant tech company “still the most important single stock in the entire market,” according to Essaye. “Investors need to see a strong report that pushes back on AI anxiety,” he said.

“This is starting to look like the same kind of rotation we saw in the year 2000,” Joseph Shaposhnik, founder and portfolio manager of the Rainwater Equity ETF, said during an interview with MarketWatch.

“The software selloff is a reminder of what can happen when momentum-driven sectors shift into reverse,” said Steve Sosnick at Interactive Brokers. “The broader, more important question is: How many sectors can go into reverse before they drag the broader market along with them?”

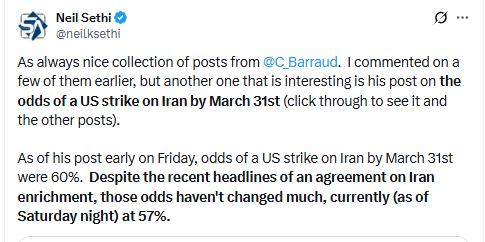

For JPMorgan Chase & Co. strategists, an equity-market pullback driven by global tariff policies or an escalation in Iran could create dip-buying opportunities as long as the macro backdrop remains positive. “Adverse geopolitical headlines” could lead to de-risking given the recent rally and stretched technicals, wrote the team led by Mislav Matejka. “But we believe that these will not be long-lasting, and should be seen as buying opportunities.”

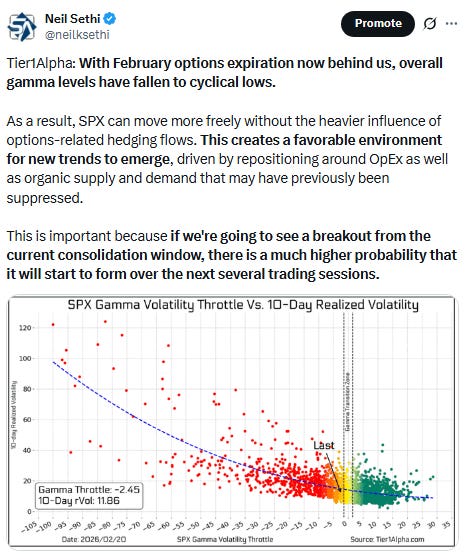

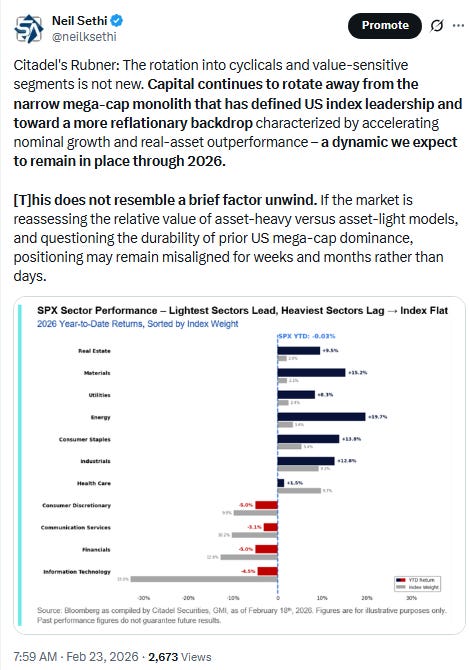

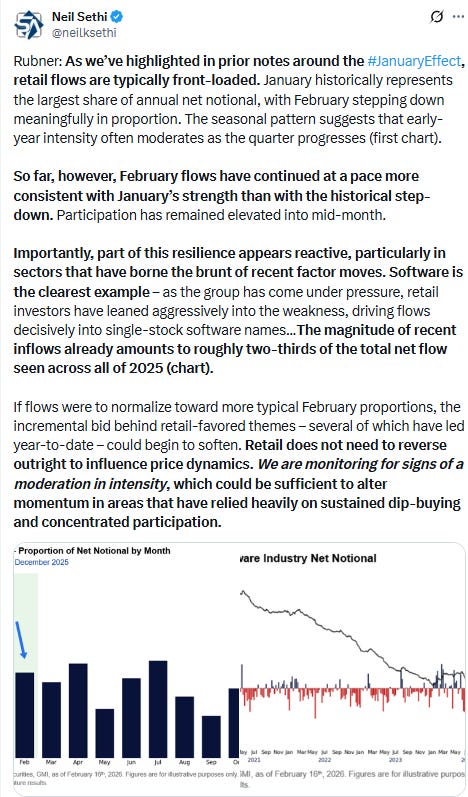

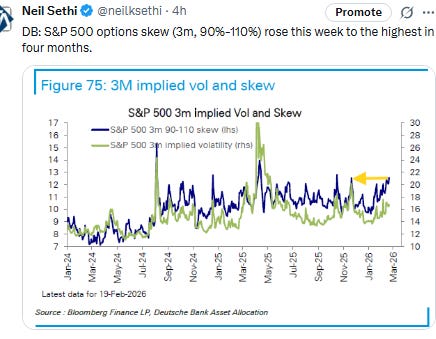

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

The 30-stock Dow was dragged down by IBM shares, which declined 13% on the heels of Anthropic outlining new programming capabilities for its Claude Code product.

Software stocks such as Microsoft and CrowdStrike were under pressure yet again as AI disruption worries hovered over the market. Microsoft dropped 3%, while CrowdStrike retreated nearly 10%. Software hasn’t been the only sector to be hit due to AI fears recently: Stocks linked to trucking and logistics, commercial real estate and financial services have similarly suffered losses this month.

Concerns around what AI could mean for the economy were fueled this past weekend after Citrini Research put out a piece of research on how the AI boom could hurt the broader economy, as it would lead to 10% unemployment.

The research paper was cited by Wall Street trading floors for the weakness seen in software stocks, as well as financials. American Express lost 7%, weighing down the Dow. Mastercard shares dropped nearly 6%.

In contrast, defensive areas of the market such as consumer staples outperformed. Shares of Walmart and Procter & Gamble led the way there, rising more than 2% each.

Companies making the biggest moves after-hours from CNBC.

None today.

Corporate Highlights from BBG:

Anthropic PBC Chief Executive Officer Dario Amodei will meet with US Defense Secretary Pete Hegseth on Tuesday, according to a senior Pentagon official, as contract talks with the artificial intelligence startup remain deadlocked over the company’s insistence on guardrails for use of its technology.

Anthropic said three leading artificial intelligence developers in China worked to “illicitly extract” results from its AI models to bolster the capabilities of rival products.

PayPal Holdings Inc. is attracting takeover interest from potential buyers after a stock slide wiped out almost half of its value, according to people familiar with the matter.

Abbott Laboratories sold $20 billion of bonds to help fund its acquisition of cancer-screening company Exact Sciences Corp.

Gilead Sciences Inc. agreed to buy US cancer-focused biotech Arcellx Inc. for as much as $7.8 billion as it seeks to boost its drug pipeline.

Merck & Co. is splitting its main pharmaceutical unit in two in an effort to better highlight the parts of the business that are growing, as it stares down a patent cliff for its best-selling cancer drug Keytruda.

Novo Nordisk A/S’s next-generation weight-loss drug CagriSema isn’t even on the market yet, but the company’s chief executive officer is already batting back suggestions that the drug is obsolete following the release of disappointing trial results.

Domino’s Pizza Inc. reported a larger-than-expected rise in comparable sales, as consumers were drawn to the pizza chain’s budget-friendly pies.

Chevron Corp. emerged as the front-runner to take control of Iraq’s second-largest oil complex from Russian producer Lukoil PJSC after signing a deal to engage in exclusive talks over the giant field.

Mid-day movers from CNBC:

In US economic data:

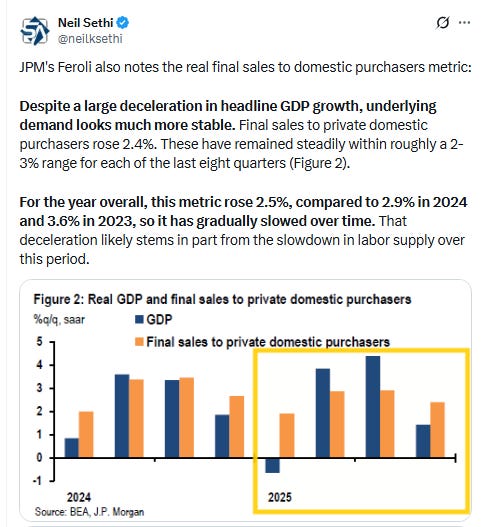

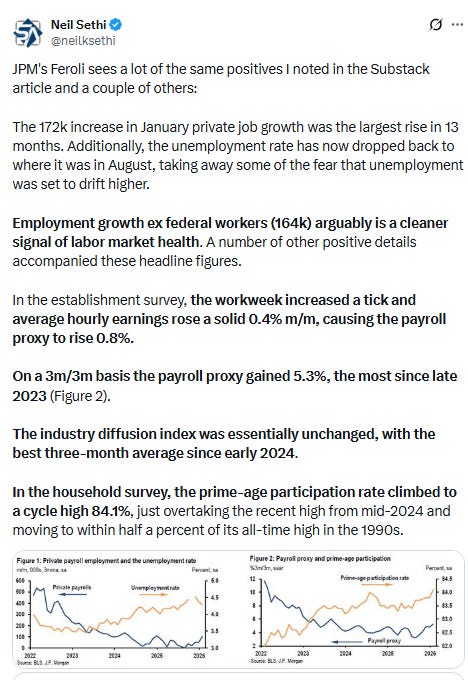

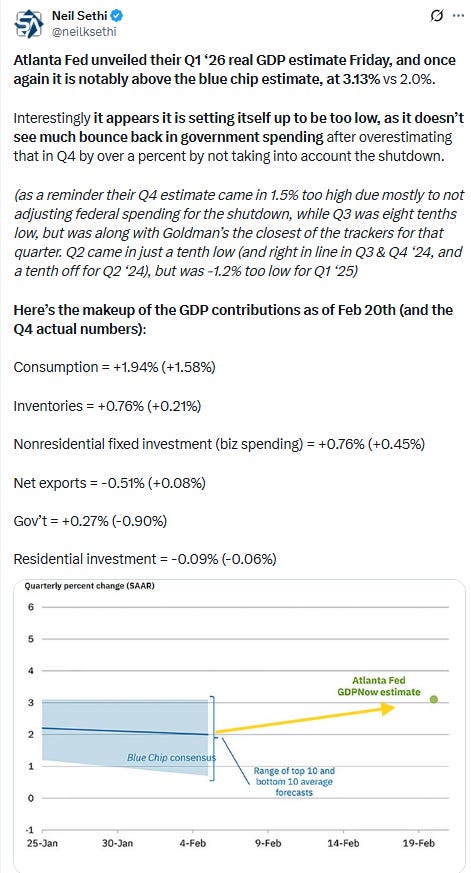

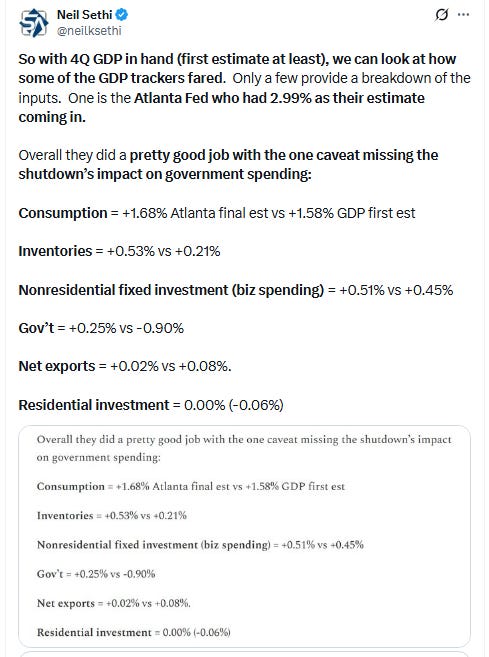

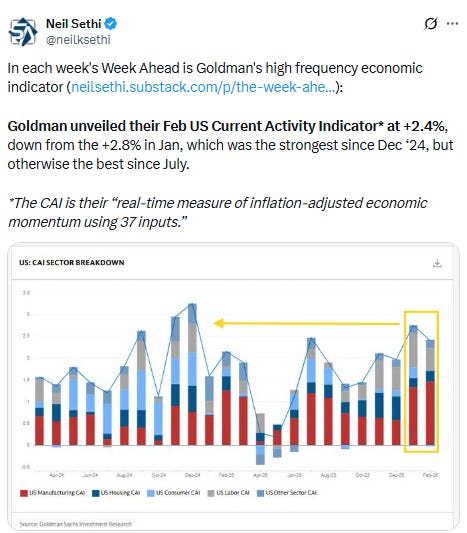

Substack articles (I’ll try to catch up on more of this week’s economic data (there was a lot) over the weekend/next week which is lighter).

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X