Markets Update - 2/24/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with lots of charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!),

Link to posts - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog. Also please note that I do often add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

Finally, if you see an error (a chart or text wasn’t updated, etc.), PLEASE put a note in the comments section so I can fix it.

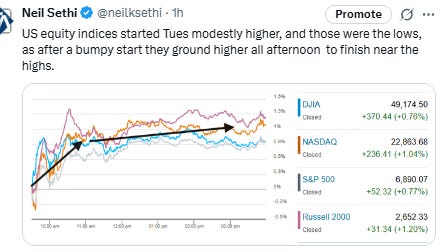

US equity indices started the day trading modestly higher with AMD shares up over 10% following Meta Platforms announcing a multi-billion dollar partnership (more below) which gave many tech names a much needed boost. Home Depot shares were also higher after an earnings beat. There was also some bounceback in some beaten down names such as IBM.

But in contrast to Monday, those opening levels were the lows of the session, and following a better than expected Conference Board consumer confidence report, the indices all ground higher in the afternoon to finish near the highs led by the Russell 2000 and Nasdaq up +1.2% and +1% respectively. The DJIA and SPX added around +0.8%.

Elsewhere, bond yields edged higher, and the dollar did as well. Copper was also up, but crude, gold, and natgas all fell. Bitcoin was little changed (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was +0.7%, the equal weighted S&P 500 index (SPXEW) +0.8%, Nasdaq Composite +1.0% (and the top 100 Nasdaq stocks (NDX) +1.1%), the SOXX semiconductor index +1.5%, and the Russell 2000 (RUT) +1.2%.

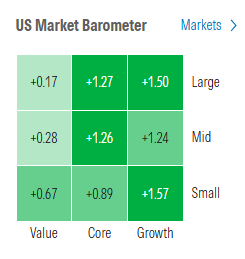

Morningstar style box flipped to all green although large value went from outperformer to underperformer.

Market commentary:

“Is consumer confidence starting to heal? That’s the question investors are asking after February’s survey topped expectations and January was revised higher. It’s a modest — but welcome — lift after a run of underwhelming GDP, retail sales, and inflation prints. And in a year already crowded with macro noise, geopolitical curveballs, and sector-by-sector whiplash, markets will take a little good news where they can get it,” eToro U.S. investment analyst Bret Kenwell wrote in an email.

The abrupt, widespread, and punitive nature of the new 15% tariffs–along with questions about how companies will ever be repaid for the illegal levies–mean that businesses are once again scrambling to figure out what’s next, as this is “going to open a new chapter in the trade saga, not end it,” according to Chris Larkin, managing director, trading and investing at E-Trade from Morgan Stanley. “In the near term, the rangebound market will have to search elsewhere for direction.”

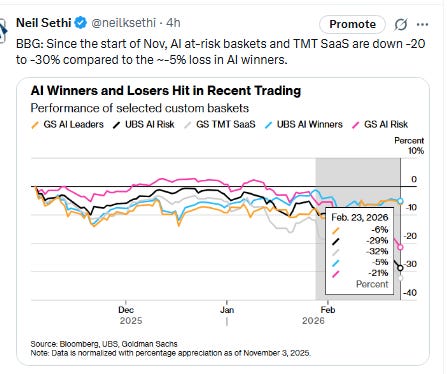

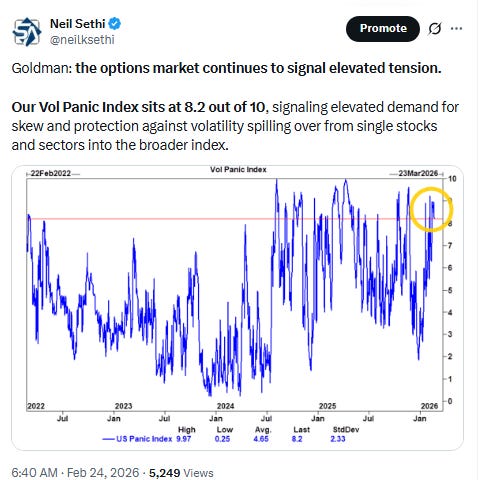

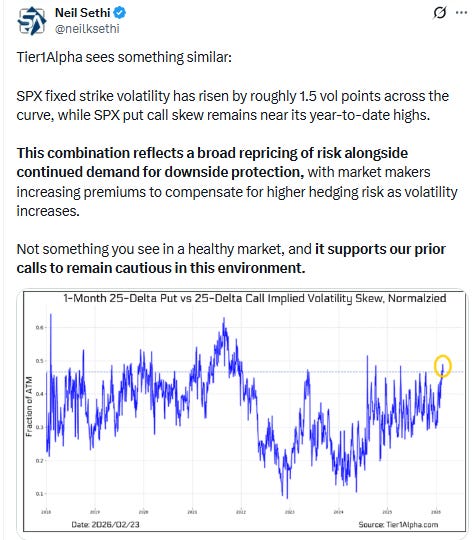

“We are reducing our risk levels by a notch,” wrote Mohit Kumar, chief economist and strategist for Jefferies International. “Ongoing concerns over AI disruption and the possible exposure to private credit and private equity have made investor sentiment fragile. If we do get an escalation in geopolitical risks, markets may face some wobbles.”

“No one wants to get cute ahead of another AI product reveal,” said Mizuho traders in a note. “Every new Anthropic headline has been treated as ‘incremental competition’ for existing software, whether that’s fair or not. So instead of trying to game the outcome, investors are choosing to step aside.”

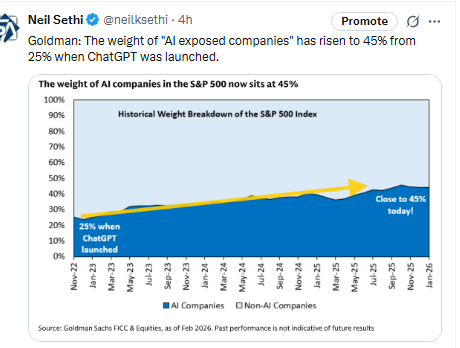

Weeks after Anthropic PBC sparked a market meltdown with the release of tools that raised questions about AI’s potential to render entire businesses obsolete, the startup said it’s expanding the reach of its Claude chatbot into new sectors. It also highlighted how Claude integrates rather than displaces existing systems, noted Adam Crisafulli at Vital Knowledge.

“This ‘we’re here to help, not hurt’ message from Anthropic is helping to trigger a fairly healthy rebound rally in software,” he said.

“AI disruption risk is not new information, but the catastrophizing seems overdone,” said Andrew Tyler, who runs the Global Market Intelligence team at JPMorgan Chase & Co.

While some of the concerns about AI displacing certain sectors could prove justified at the company level, the broader market effect has been a healthy moderation of optimism, according to Anthony Saglimbene at Ameriprise.

“This shift in investor psychology, if lasting, could help lower the odds of valuations becoming unanchored with reality and leave a more constructive environment for the long-term health of the market,” he said.

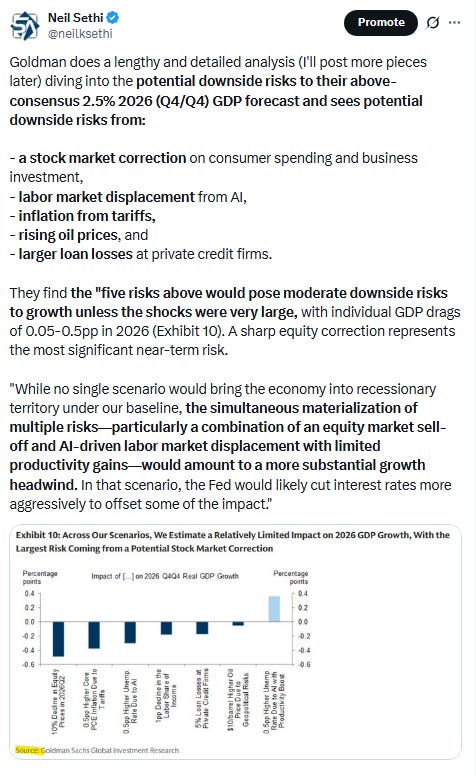

The business cycle should limit equity drawdown risk despite AI disruption and concerns over geopolitical shocks, according to Goldman Sachs Group Inc. strategists including Andrea Ferrario and Christian Mueller-Glissmann.

“While somewhat elevated valuations do increase the risk of smaller corrections, our current optimistic macro baseline and broadly supportive market sentiment should limit drawdown risk,” they added.

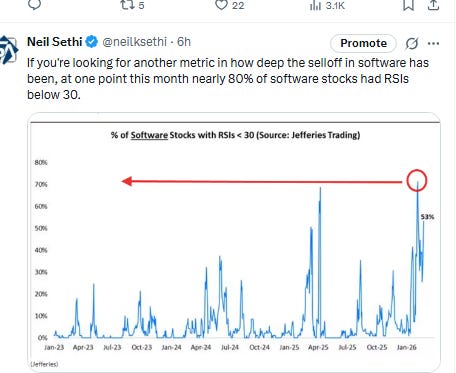

“Outperforming sectors get challenged,” Pete Mulmat, head of brokerage operations and strategy at IG North America, told MarketWatch. “There’s still an interest by traders to find what is potentially interesting or undervalued. There hasn’t been that general capitulation.” General capitulation would involve traders walking away from the market entirely, taking whatever losses they have to in order to get out. Despite tech’s recent decline, Mulmat, who oversees Tastytrade and its suite of products for active traders, said that investors on the platform are instead looking for new opportunities, diversifying and otherwise managing exposure.

“It seemed to me that that the market itself was in a sell-first, ask-questions-later mentality. It has been for some time, and that’s why you saw some of even the enterprise software guys take a rather large hit,” Anshul Sharma, chief investment officer at Savvy Wealth, said to CNBC. He added that the day’s moves are “a classic relief rally after that selling.” Sharma also said that he’s not quite convinced of the narrative that has been recently been circulating on Wall Street that AI is coming to replace a lot of enterprise software right away.

“It’s unbelievably risky from a liability perspective for very large companies to say, ‘Okay, we’re going to now move away from enterprise software — which has been tried and true, which has been tested and which aligns with our risk parameters — and then build it in house, and this is all going to happen in the next couple of months, next couple of quarters,’” he said. “The drawdown in software was a very immediate reaction.”

For Emmanuel Cau, head of European equity strategy at Barclays Plc, fears about labor-market disruption need to be counterbalanced by the job creation that typically accompanies technological progress. As for software stocks, which have now been mispriced, “it’s very hard to go prove the market wrong on that,” Cau told Bloomberg TV. “What we are trying to do from an equity allocation standpoint is to be exposed to some of these old-economy, more tangible parts of the market.”

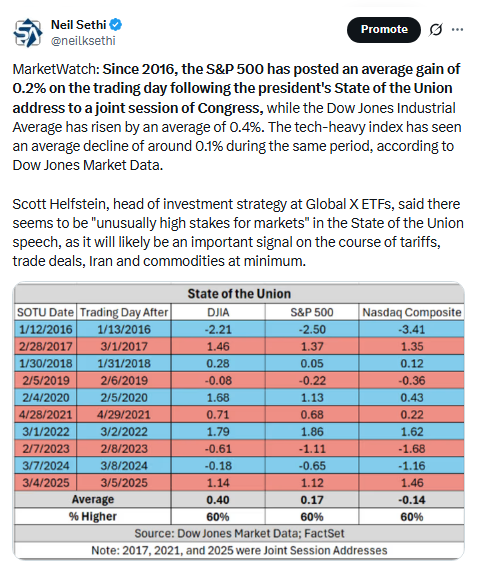

“The focus for investors [in the State of the Union] will be on three issues: tariffs, Iran and the Fed,” said Joachim Klement, head of strategy at Panmure Liberum. “Any hint that a military strike against Iran is imminent should trigger another rally in oil and gold prices. If Trump uses his platform to bully the Supreme Court or the Fed, Treasury markets will not take that lightly.”

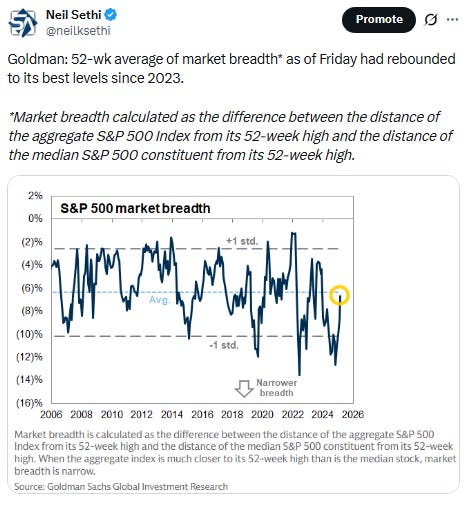

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

Shares of AMD jumped 8.8% after Meta Platforms announced a multiyear deal with the semiconductor company. The new partnership entails deploying up to 6 gigawatts of AMD’s graphics processing units for AI data centers. Meta will also invest in AMD through a performance-based warrant for up to 160 million shares of the chipmaker.

The move comes a week after Meta said it’s using millions of Nvidia’s chips in its data center buildout. Shares of Nvidia rose 0.7% ahead of its earnings tomorrow. Docusign was also a winner, increasing more than 2% after Anthropic said that its Claude Cowork is now able to be connected to Docusign as well as organizations’ other existing tools like Google Drive and Gmail. The move offered some optimism to investors that AI might be able to complement software companies rather than take their place.

That extended to other areas of the software space. Shares of Salesforce — which has been working with Anthropic as well — and ServiceNow were up 4% and more than 1%, respectively. The iShares Expanded Tech-Software Sector ETF (IGV) was higher by close to 2%, though it still remains more than 30% below its 52-week high.

The Dow was supported by a nearly 2% rise in Home Depot shares after the company’s earnings beat expectations for the first time in a year. IBM shares, which tumbled in the prior trading day as a result of aforementioned AI fears, also added to the Dow’s gains.

Texas Instruments Inc. though slid on concern about heavy capital spending.

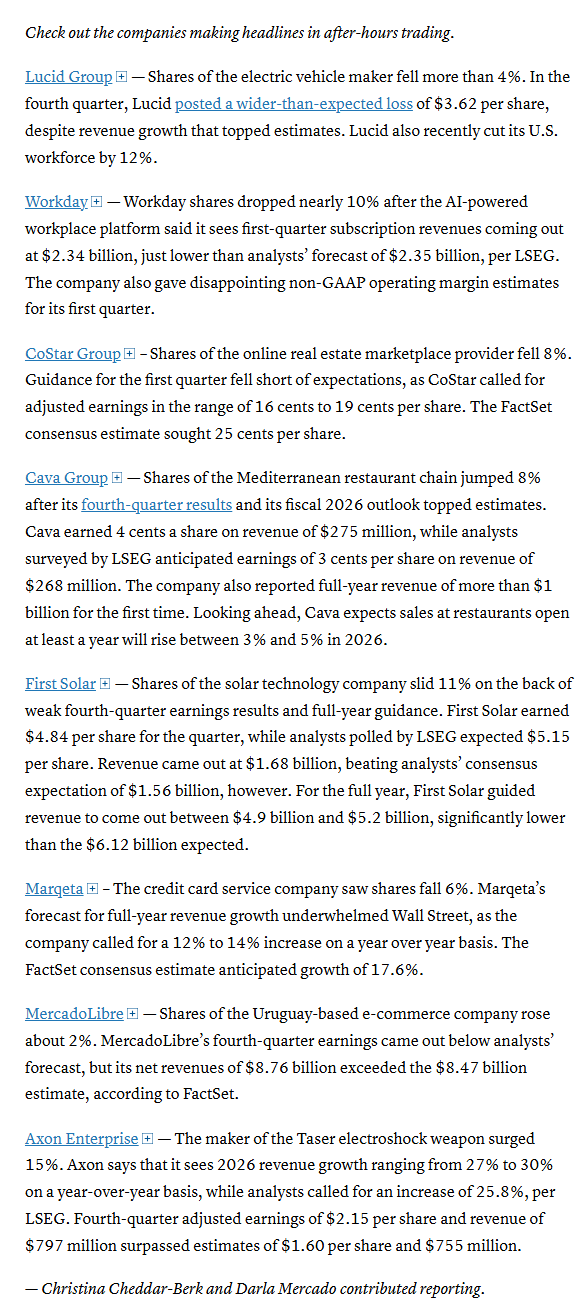

Companies making the biggest moves after-hours from CNBC.

Corporate Highlights from BBG:

The Pentagon warned Anthropic PBC that it would terminate the company’s military contracts on Friday if the artificial intelligence startup failed to meet government terms for use of its technology, according to people familiar with the matter.

Warner Bros. Discovery Inc. is considering a new takeover proposal from Paramount Skydance Corp., the latest salvo in a battle for control of one of Hollywood’s most-famed studios.

Home Depot Inc. reported a key sales metric that beat expectations in the latest quarter on steady demand, though the retailer cautioned that macroeconomic challenges remain.

Novo Nordisk A/S plans to slash the US list prices for its blockbusters Wegovy and Ozempic next year as the drugmaker struggles to claw back a larger share of the obesity market.

Mid-day movers from CNBC:

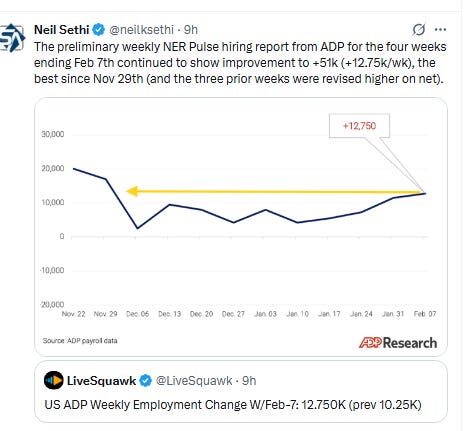

In US economic data:

Note there appears to have been a data error in the MicroMacro chart in the Pending Home sales report (not taking into account revisions to prior months) I sent earlier which led to me saying pending home sales were near the lowest on record when they were actually the lowest on record. I fixed it, and the post on the blog is correct (link is below).

Substack articles.

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X