Markets Update - 2/27/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with lots of charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!),

Link to posts - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog. Also please note that I do often add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

Finally, if you see an error (a chart or text wasn’t updated, etc.), PLEASE put a note in the comments section so I can fix it.

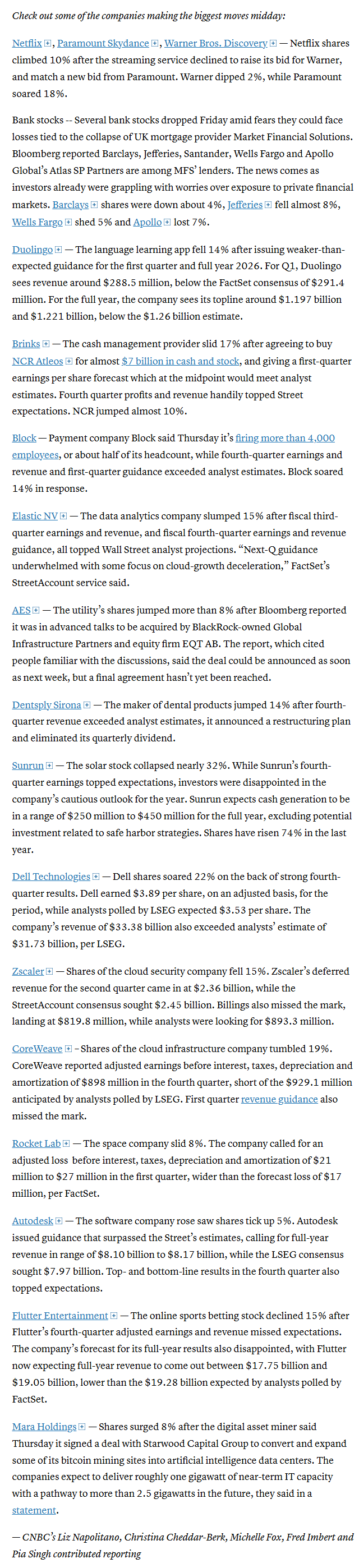

US equity indices opened trading Friday solidly lower following a much hotter than expected producer prices report (fueled by the largest monthly increase in trade services (wholesaler/retailer margins on record (meaning higher costs being passed on to consumers and businesses)).

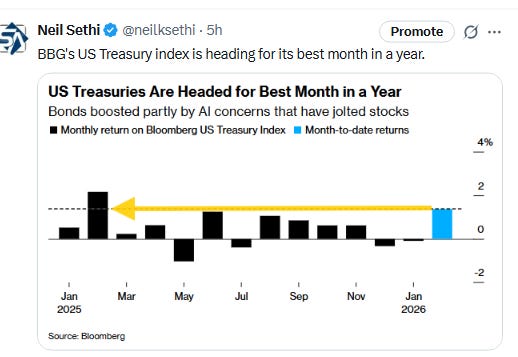

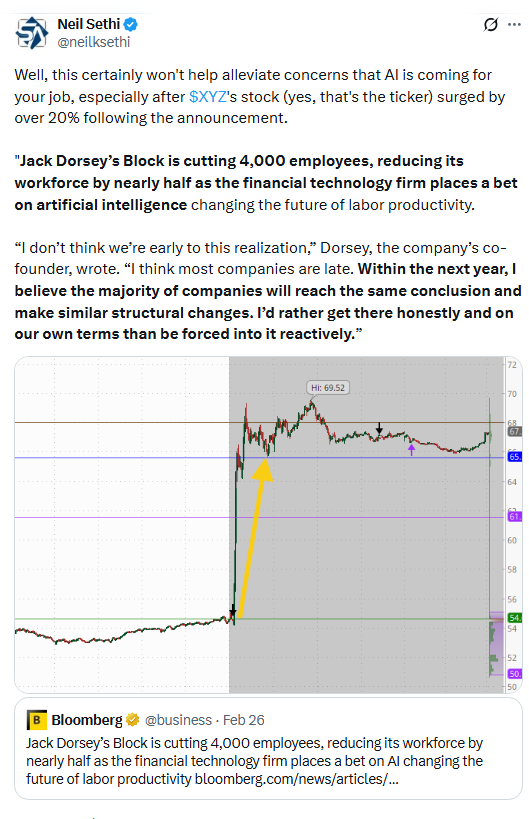

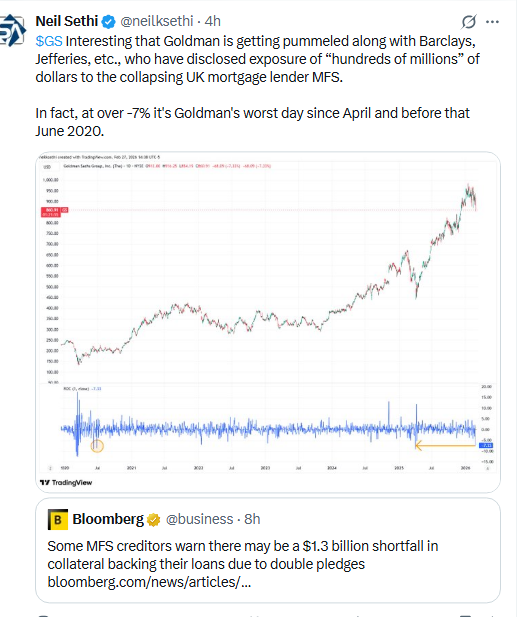

However any inflation concerns were more than offset by those around a recession following financial services firm Block announcing Thursday that it’s laying off more than 4,000 employees, or nearly half of its workforce, in a pivot to AI (and was rewarded with shares up 20%). Another credit blowup in a UK mortgage firm that ensnarled a number of US financials just added to concerns. That came after a BlackRock private debt fund cut its dividend, and a private credit fund overseen by Apollo Global Management marked down the value of its assets. 10-year Treasury yields fell to the lowest since October and 2-year yields the lowest since Aug ‘22 as Fed rate cut bets jumped (but most notably for 2027 (more on all that in the subscriber section)).

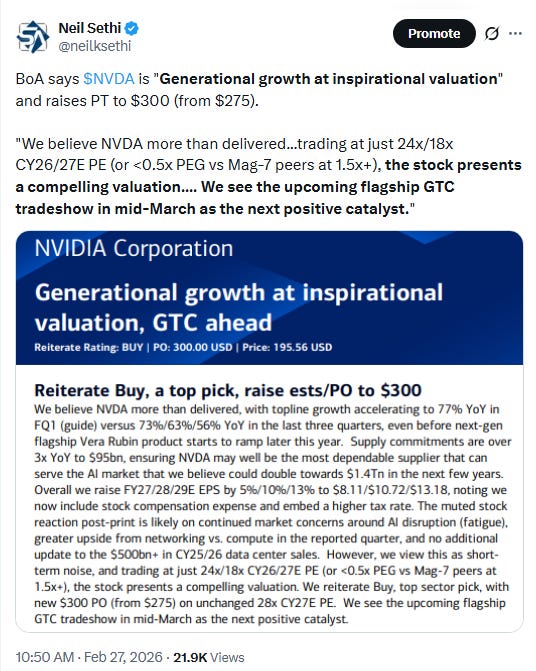

Also weighing on the indices was continued weakness in many Tech names with Nvidia extending its post-earnings slide from Thursday (it would finish down another -4% taking its two-day losses to nearly -10%). Notable software names also fell. Salesforce tumbled more than -2%, as did Microsoft, while Cybersecurity company Zscaler shed -12% after deferred revenue and billings in the fiscal second quarter missed expectations. CoreWeave fell -18% on disappointing guidance.

Also, keeping markets on edge was a surge in crude prices after the US (and other countries) authorized the evacuation of non-military personnel from Israel.

Indices mostly traded sideways from the open, with some upward bias at the large cap level (with large cap indices finishing -0.4% for SPX to around -1% for the DJIA and Nasdaq), but a downward bias for the small cap Russell 2000 (RUT) which finished -1.7%.

For the week, indices hit their lows on Monday, recovered into Wednesday’s close all getting into the green, remained up or close to it through Thursday, before falling back to near the lows of the week Friday, all finishing down around -1% except the SPX which “outperformed” -0.4%. For the month the SPX and Nasdaq were lower (-0.9% and -3.4% respectively, the worst since April) while the DJIA and RUT eked out fractional gains.

Elsewhere, as noted bond yields fell, and the dollar also was lower. Crude, gold, copper and natgas were higher, while bitcoin was down (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was -0.4%, the equal weighted S&P 500 index (SPXEW) though +0.1%, Nasdaq Composite -0.9% (and the top 100 Nasdaq stocks (NDX) -0.3%), the SOXX semiconductor index -1.2%, and the Russell 2000 (RUT) -1.7%.

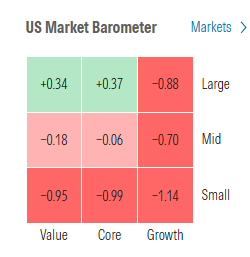

Morningstar style box mostly red Fri with just larger value names escaping.

Market commentary:

“Investors are pumping the brakes on positioning as the level of uncertainty is increasing,” said Sameer Samana, head of global equities and real assets at Wells Fargo Investment Institute. Samana remains confident that growth of the economy and companies’ earnings will lead the S&P 500 to overcome near-term issues and break higher from current levels.

“There is a flight to quality underway,” said veteran strategist Louis Navellier.

“Given the tall wall of worry — AI volatility, Nvidia-driven swings, tariffs, geopolitics and stubborn inflation — you’d expect a sharper drop,” said Mark Hackett at Nationwide. “That resilience suggests this is more of a pause than a turning point, and once it clears, the path of least resistance is higher.”

“The most-pressing issue facing the markets is now the situation in the Middle East,” said Matt Maley at Miller Tabak. “However, the concerns surrounding the tech sector and the credit markets are not far behind.”

“This morning’s higher inflation data is one more thing to worry about within the traditional economic analysis of price stability and full employment, even before investors factor in the disruptive potential of AI’s impact on the economy,” said Chris Zaccarelli at Northlight Asset Management. “The Producer Price Index (PPI) doesn’t typically get the attention that the CPI or PCE inflation readings get, but this morning the PPI was higher than expected across the board and that could upset markets,” said Zaccarelli. “For the past month the market has been worried about AI disruption and its impact on the labor market, so inflation hasn’t been top of mind, but this morning’s inflation readings could give the Fed another reason to be more patient with rate cuts and wait until the second half of the year before making any changes,” he added in written commentary.

“This is going to give more ammunition to the hawks on the Fed, and even perhaps push Fed members sitting on the fence to wait longer before cutting rates again,” said Sonu Varghese at Carson Group.

While PPI came in hotter than expected, companies have largely been able to absorb incremental costs, maintaining profit margins and minimizing the pass-through to consumers, according to Scott Helfstein at Global X. “Producer inflation is worth monitoring, but it has not necessarily translated into broader inflation across the economy,” he added.

To Gina Bolvin, PPI wasn’t a deal-breaker. “For investors, this is a volatility moment, not a turning point,” said the president of Bolvin Wealth Management Group. “Focus on pricing power, earnings strength, and selective opportunities as the Fed stays patient.”

Stephen Kolano, chief investment officer at Integrated Partners, views the PPI report as an additional complication for investors on top of the already-existing anxieties surrounding not just AI capex and the risk of its disruption to industries but also other factors such as stress in the private credit market. Noting that the inflation reading seems to be more services driven, he thinks it’s a sign companies are possibly starting to pass through the cost of tariffs to the end consumer in order to maintain their margins. “Inflation isn’t solved yet,” he said, adding that it creates this conundrum for the Federal Reserve of deciding whether to cut interest rates to spur growth or to hold steady to continue to fight inflation. “It just creates this uncertainty around which way is policy going to go in the remainder of the year.” That’s not to mention the state of the labor market as another worry, Kolano said. Even though job growth last month was much better than expected, the investment chief said he isn’t sure that the labor market is stabilizing given that layoffs have been picking up. In fact, Challenger, Gray & Christmas reported earlier this month that layoffs in January hit their highest total for that month since the global financial crisis. “I don’t see a clear sign that unemployment is not going to move higher just yet,” he said.

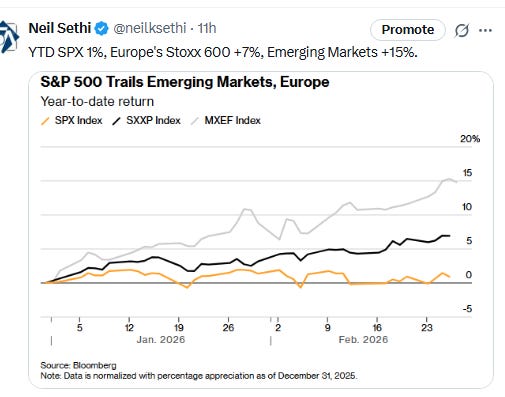

“I don’t see any major correction coming, but any hint of a recession linked to AI in the US would certainly trigger some unpleasant trading,” said Andrea Tueni, head of sales trading at Saxo Banque France. “Europe is currently better positioned than the US and outperforming as its tech sector is much smaller and there is much less uncertainty on monetary policy.”

“The outperformance [of ex-US] highlights the possibility of a lingering overvaluation in some asset classes in the US, as well as doubts about the independence of the Federal Reserve’s future monetary policy,” said Guillermo Hernandez Sampere, head of trading at asset manager MPPM. “Barring an economic downturn in Europe, the outperformance should continue.”

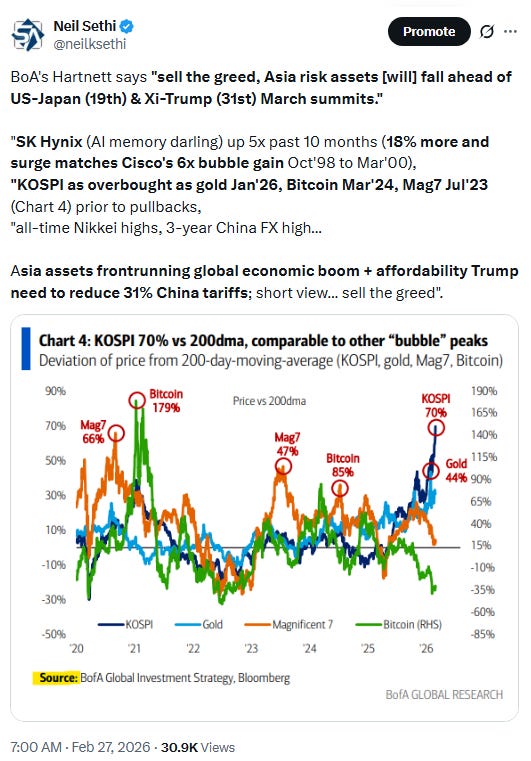

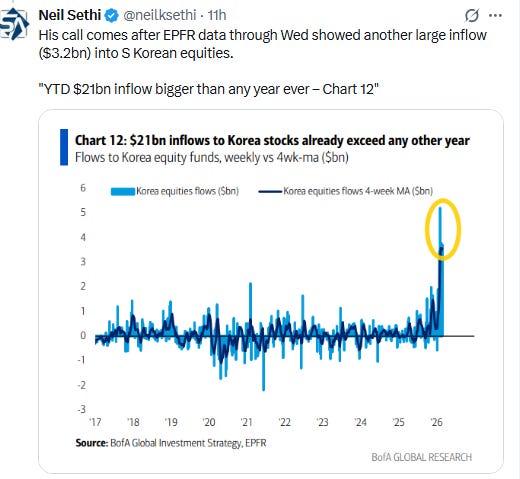

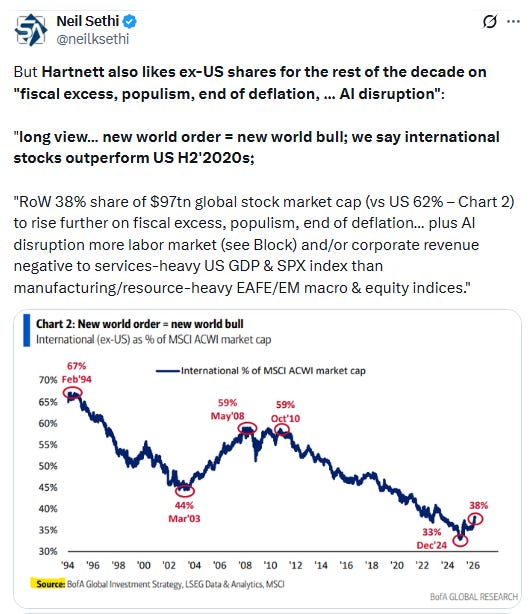

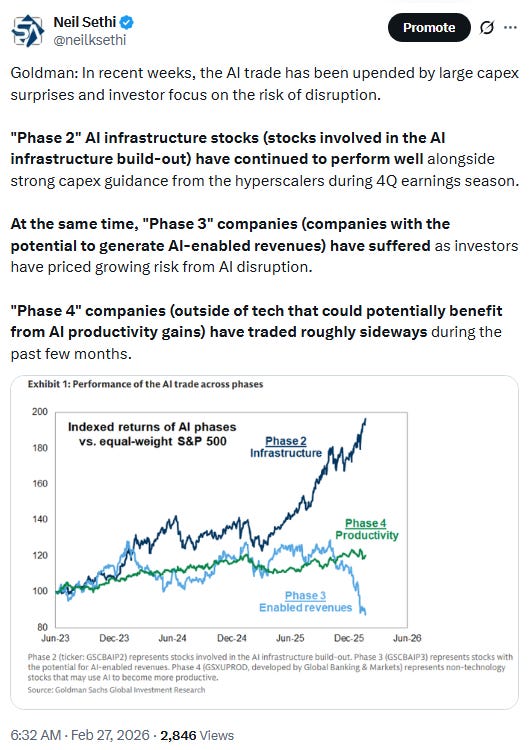

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

Dell Technologies Inc. was up +20% after giving an outlook for sales of its AI servers that exceeded estimates.

Corporate news from BBG:

Dell Technologies Inc. gave an outlook for sales of its AI servers that exceeded estimates.

CoreWeave Inc. reported a bigger-than-expected loss and boosted capital expenditures.

Paramount Skydance Corp. clinched its deal for Warner Bros. Discovery Inc., outmaneuvering Netflix Inc. after a months-long battle.

Block Inc. said it was reducing its workforce by nearly half in a bet on AI. Jack Dorsey’s firm also raised its outlook for gross profit.

Sweetgreen Inc. reported a weak fourth quarter and said annual sales would fall much more than Wall Street expected.

Duolingo Inc. said its drive to gain subscribers would mean slower earnings growth in the short term.Corporate Highlights from BBG:

Mid-day movers from CNBC:

In US economic data:

Substack articles.

None today but will have one or two over the weekend.

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X