Markets Update - 2/4/26

Update on US equity and bond markets, US economic data, the Fed, and select commodities with charts!

To subscribe to these summaries, click below (it’s free!).

To invite others to check it out (sharing is caring!),

Link to posts - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog. Also please note that I do often add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

Finally, if you see an error (a chart or text wasn’t updated, etc.), PLEASE put a note in the comments section so I can fix it.

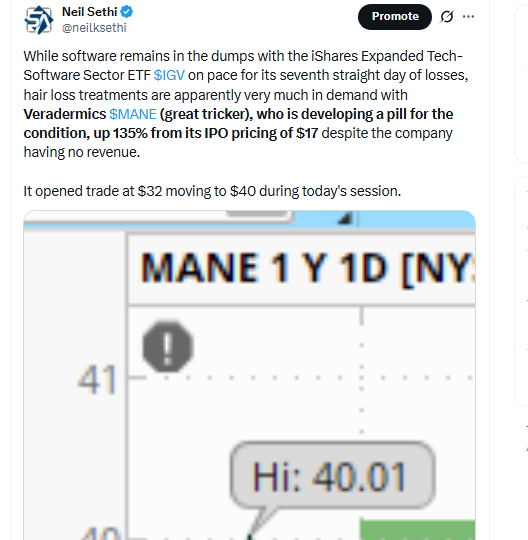

US equity indices opened today’s session mixed with continued weakness in tech pulling down the Nasdaq to a modest loss while the SPX and Russell 2000 are mildly in the green. Advanced Micro Devices shares dropped 9% after its first-quarter forecast underwhelmed some analysts (it would end -17%). Other names in the space such as Broadcom and Micron Technology dipped as well (and would lose -3.8% and -9.5% respectively). Software stocks also continued to face pressure. Oracle would end the day -5%. Chipotle shares fell nearly -6% after the restaurant chain reported falling traffic for the fourth straight quarter and projected flat same-store sales growth for 2026, but would rebound to end the day +2% higher.

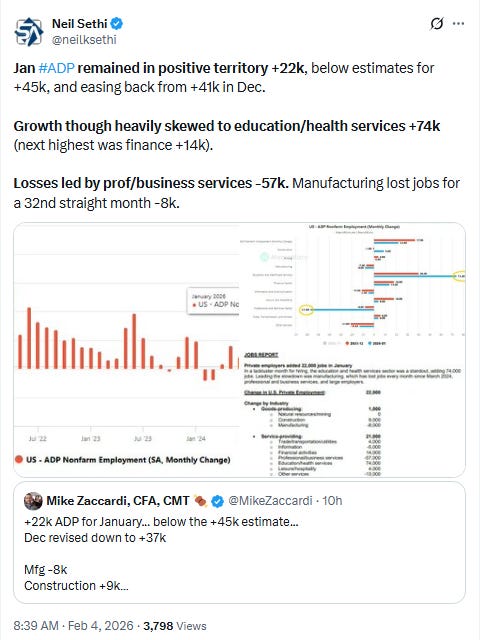

Before the market open we also got the monthly ADP employment report which came in below expectations, but still positive (see Economic Data below) with job gains remaining highly concentrated (a more full breakdown will be coming by tomorrow morning).

All of cap weighted indices deteriorated into early afternoon before bottoming weighed down by their biggest components. The indices cut losses but still finished lower: SPX-0.5%, Russell 2000 -0.9%, Nasdaq -1.5%. In contrast, the price-weighted DJIA was +0.5% and the equal-weighted SPX +0.9%.

Elsewhere, bond yields were little changed as the dollar edged higher. Bitcoin fell to the least since Nov ‘24, and copper pulled back, but crude, gold, and natgas all saw gains.

The market-cap weighted S&P 500 (SPX) was -0.5%, the equal weighted S&P 500 index (SPXEW) +0.9%, Nasdaq Composite -1.5% (and the top 100 Nasdaq stocks (NDX) -1.8%), the SOXX semiconductor index -4.4%, and the Russell 2000 (RUT) -0.9%.

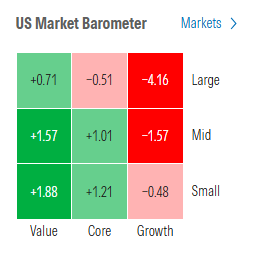

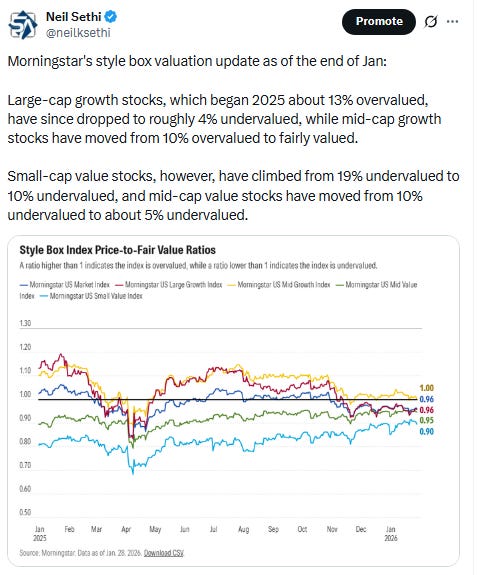

Morningstar style box continued to see growth on the weaker side of things.

Market commentary:

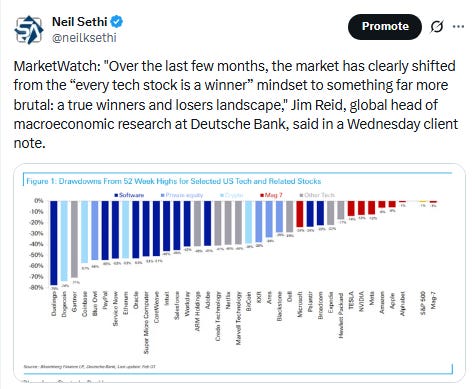

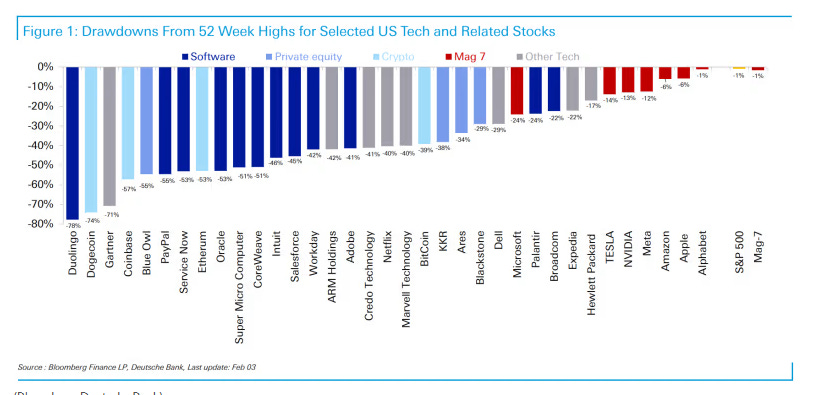

“[Tuesday’s] tech selloff was sharp, but it’s just the latest episode in a trend that was evident toward the end of last year, and which picked up steam recently,” writes Daniel Skelly, head of Morgan Stanley’s Wealth Management Market Research and Strategy Team. In that sense, a rotation away from some parts of tech is a “healthy development,” according to Skelly. “Furthermore, it’s notable that rotation is also happening within tech itself, as investors flee software because of continued AI-disruption fears, and move toward other momentum winners, like memory,” Skelly writes. “As new leadership emerged in Q4 and continued since the calendar year flipped, the overall index remains near all-time highs, despite tech pain as the baton is passed.”

“Bottom line, something I said back in late November, the GenAI tech trade is no longer a one way ride. We’ve transitioned it from ‘buy everything’ to ‘not everyone can win.’ I believe we are losing this trade in terms of its ability to carry the market but luckily so far investors have found other things to buy and that includes other parts of the S&P 500, small and mid cap and for sure international stocks,” said Peter Boockvar, chief investment officer at One Point BFG Wealth Partners.

“Toward the end of last year, you began to see the market differentiate between what the market perceived to be the winners and losers in the [artificial intelligence] space,” Scott Welch, chief investment officer at Certuity. “I think you’re seeing a continuation of that now.”

“It’s just a natural rotation,” Welch said. “It’s been such a large cap growth-dominated space for so long — value was just punished, small cap was punished and non-U.S. markets were just kind of ignored when, in fact, they basically doubled the results of the domestic market last year.”

“All of this has been sort of coming for a while, and I think you’re just beginning to see that play out,” he added.Wednesday’s unwinding of technology-related stock positions is not likely to end overnight, given the likelihood of another three to six months of weakness in this area, according to Kentucky-based investment strategist Ross Mayfield at Baird Private Wealth Management. “Tech weakness and the rotation out of tech into more cyclical corners of the market has been a theme for the past couple of months,” Mayfield said in a phone interview. “But I wouldn’t bet against tech over the next year” or more. “If you can hold your nose, it’s a buying opportunity for investors.”

“Ultimately, we view this as another AI scare with software and related areas bearing the brunt of it,” said Chris Senyek at Wolfe Research. “Within tech, we’d use weakness to buy AI related semiconductor stocks, and our favorite sector for new money is discretionary. In particular, stocks levered to an uptick in spending as tax refunds hit in February-April.”

It’s not that AI is being abandoned by markets, according to Charu Chanana at Saxo. She says the issue is that it’s being “priced more carefully.”

It’s been a “sell-first and ask-questions-later mentality” in software stocks and in parts of the tech complex, according to Ryan Detrick, chief market strategist at Carson Group. “We continue to be impressed with how tech might lag, but other areas take the baton,” Detrick told MarketWatch on Wednesday. “Remember, the lifeblood of a bull market is rotation and we are seeing that.”

“The underlying breath is strong,” said Kevin Gordon, head of macro research and strategy at the Schwab Center for Financial Research, noting that seven out of the S&P 500’s 11 sectors were positive in February despite sharp declines in tech and software stocks. “If that holds, it’s further confirmation that this rotation has some pretty strong legs.”

“There might be a glass half full and a glass half empty perspective on the moves here,” said Kyle Rodda at Capital.com. “On the one hand, tech stocks are potentially too richly valued. On the other hand, the strength in the market is broadening out in a sign of improving economic fundamentals.”

“It’s been a tough week so far, but let’s keep in mind the broader picture here,” said Mona Mahajan at Edward Jones. “It is hard to get overly bearish when we are still looking at an economy that we think is growing above trend.” Mahajan also notes she’s looking at an earnings growth picture that is still double digits for 2026, driven by tech sectors but also non-tech sectors. “So a little broadening there,” she said.

“This is a rotation, not a rupture,” he said. “Seeing that shift near record highs highlights the market’s underlying strength.” Hackett also noted that the fundamental picture remains robust. Fourth-quarter earnings are set to extend the double-digit winning streak to five quarters, with elevated sales growth, record margins, greater breadth of the earnings strength, solid 2026 guidance and improving corporate sentiment, he said.

“While we remain positive on the outlook for US equities and expect the S&P 500 to move higher, we believe diversification is key to managing market risks and enhancing long-term returns,” said Ulrike Hoffmann-Burchardi at UBS Global Wealth Management. To position for a broadening rally, she likes financials, health care, utilities, and consumer discretionary in the US, and see attractive opportunities across Asia and Europe.

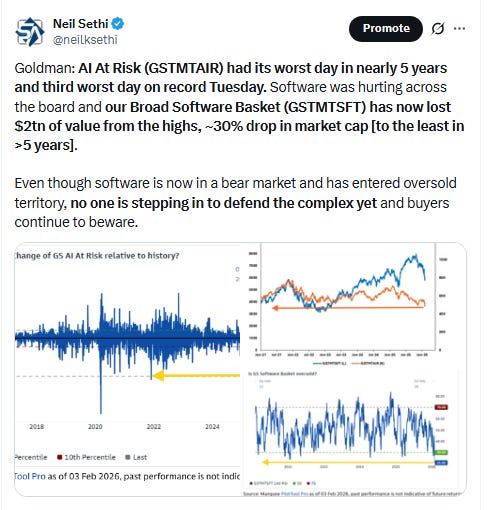

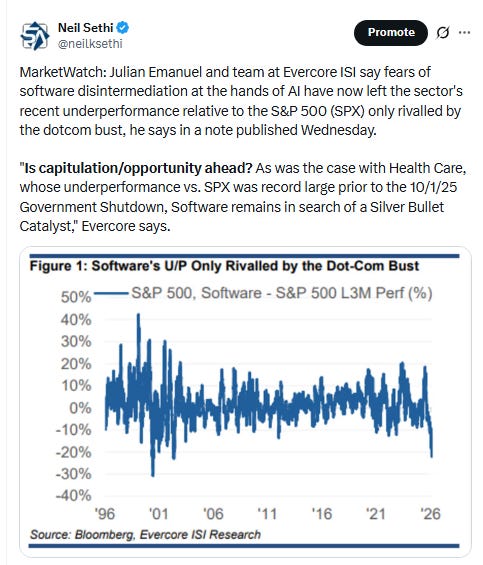

“Software stocks are being decimated as worries permeate over whether AI will cannibalize their businesses,” said Bret Kenwell at eToro. “However, while the long-term implications are still somewhat unknown, many of these firms continue to generate solid earnings and revenue growth, and analyst expectations for these metrics continue to trend higher.” Kenwell notes that the software space is quickly approaching “oversold” levels and likely “nearing capitulation.”

“Right now, investors are not asking themselves where the value is,” he said. “Instead, they’re throwing out all software stocks — even as many top firms within this space are doing just fine.” However, the bigger long-term risk may be on valuation, Kenwell said. Once this selloff is over and the stocks recover from their oversold condition, the question is: will there be a new ceiling on just how much investors are willing to pay for them? “If so, that could limit the upside and the recovery time for this space — high quality or not,” he concluded.

“The news for the software stocks gets worse by the day,” said Matt Maley at Miller Tabak. “However, no matter where they are headed over the intermediate and long-term, they are getting poised for a nice bounce over the near-term. Investors should be careful about negative bets over the short-term.”

“Of course, we have been saying for some time now that if the tech sector sees a broad decline — with the all the different groups within the sector falling in unison — it’s going to be very tough for the broad stock market to hold up in the face of that kind of scenario,” Maley said. However, we’re going to have to see more days like that before we can raise a “meaningful yellow warning flag,” he concluded.

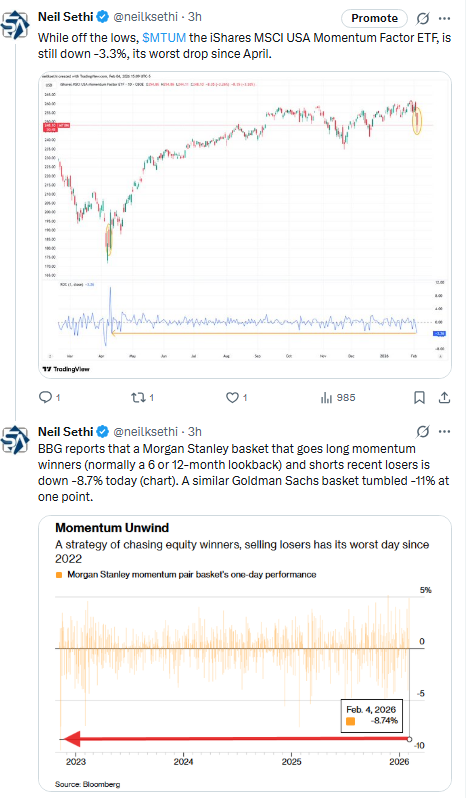

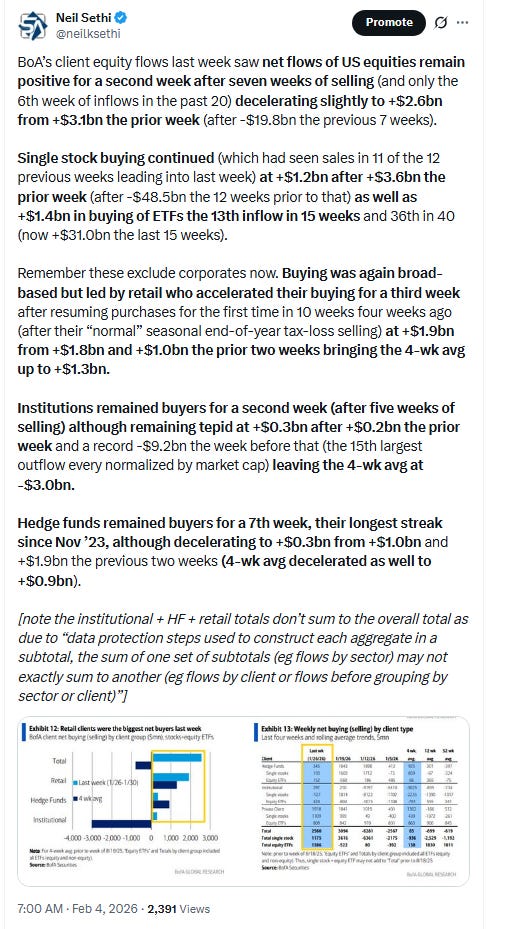

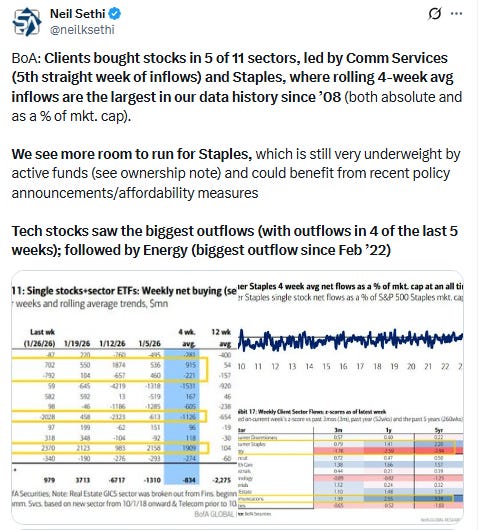

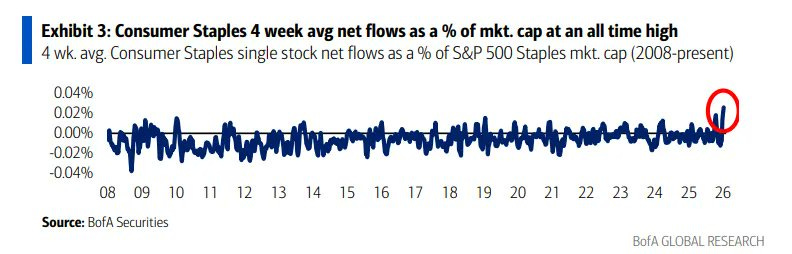

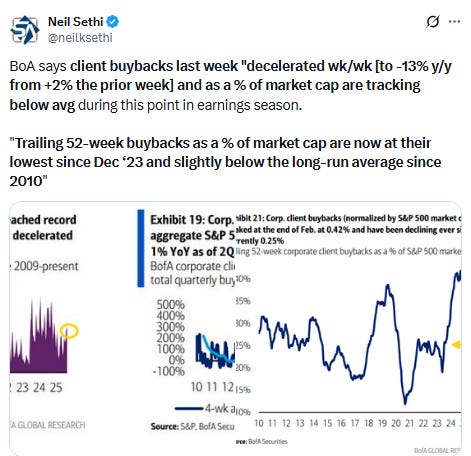

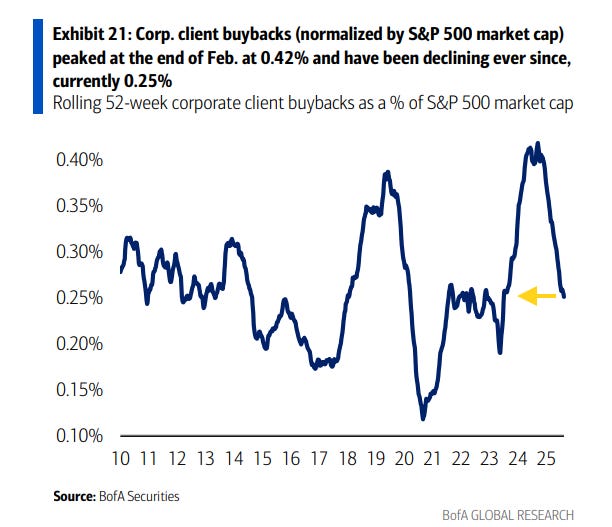

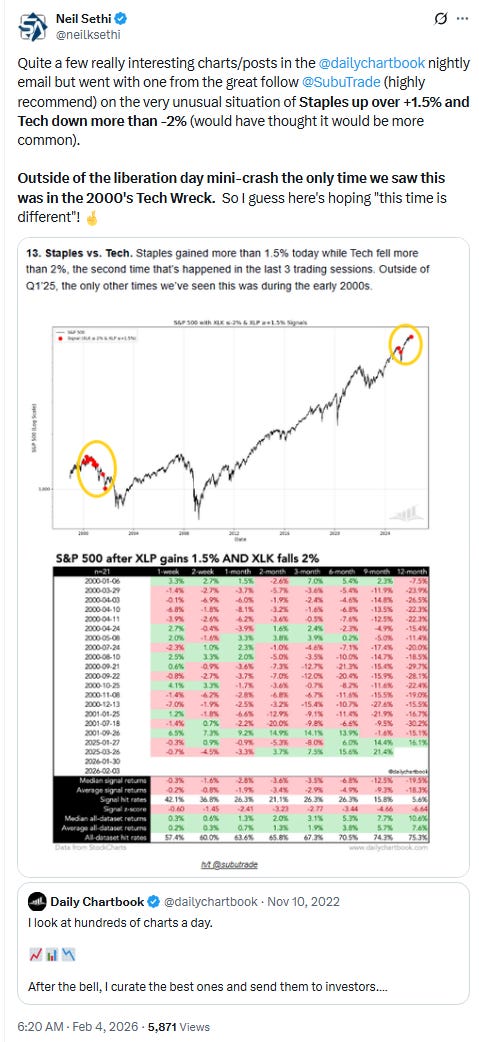

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

Shares of AMD weighed on the broader market, pulling back 17% after its first-quarter forecast underwhelmed some analysts. Defending the results, CEO Lisa Su told CNBC Wednesday that the company has seen an increase in demand in recent months, saying, “AI is accelerating at a pace that I would not have imagined.”

Still, other names in the chips space such as Broadcom and Micron Technology suffered losses as well. The former was down 3.8%, while the latter fell 9.5%. Some software stocks also continued to face pressure, including Oracle and CrowdStrike, which extended their decline from the prior trading day. Oracle shed 5%, while CrowdStrike lost more than 1%. While the group has been a source of weakness recently, certain names like Microsoft found stability Wednesday. That stock was up nearly 1%.

For the Dow, Amgen was among the names fueling outperformance. The biotechnology stock was higher by 8% after the company reported better-than-expected earnings and revenue for the fourth quarter. Honeywell also offered a boost to the index, rising almost 2% as investors moved from tech into more value-oriented names.

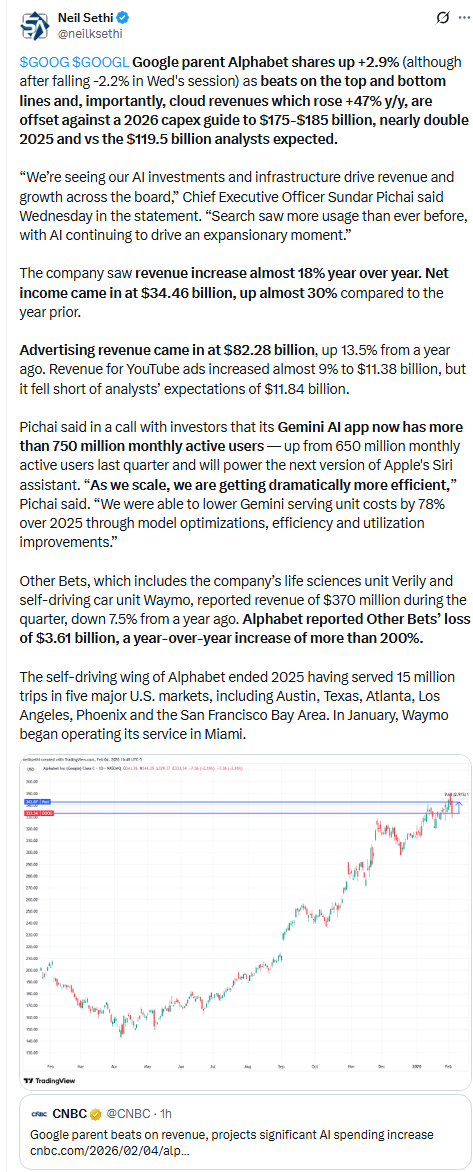

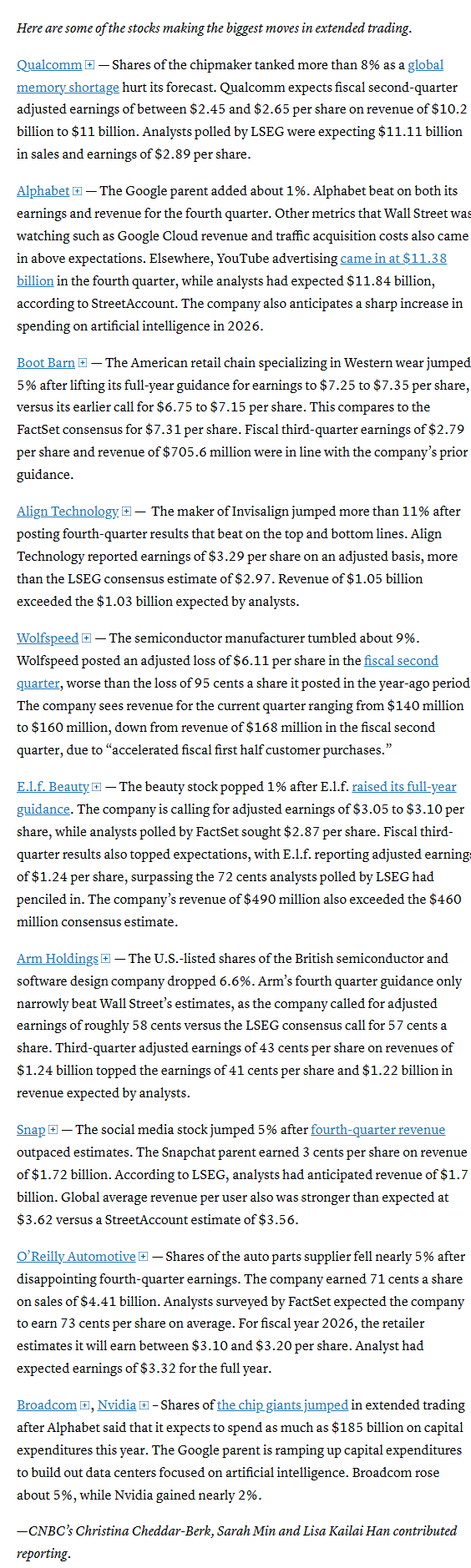

In late hours, Alphabet Inc. reported solid revenue, but said it plans to spend far more than investors expected in 2026. Qualcomm Inc. gave a tepid outlook. Arm Holdings Plc’s forecast fails to satisfy skeptical investors.

Companies making the biggest moves after-hours from CNBC.

Corporate Highlights from BBG:

Nvidia Corp. is nearing a deal to invest $20 billion in OpenAI as part of its latest funding round, according to people familiar with the matter, marking the chipmaker’s single biggest investment in the ChatGPT developer.

SpaceX held meetings with banks from outside the US for its IPO, according to people familiar with the matter, as Elon Musk’s rocket and satellite maker targets a listing this year on an ambitious timeline.

Amazon.com Inc. is taking the wrapper off its upgraded Alexa in the US, offering the AI-enhanced digital assistant to paying Prime customers and introducing a free version for everyone else.

Texas Instruments Inc. has reached an agreement to buy the US chip firm Silicon Laboratories Inc. for about $7.5 billion, deepening its exposure to several long-standing markets for chips including the home appliance, power, industrial and medical-device sectors.

Adobe Inc. ramped up its advertising in 2025, spending $1.4 billion to promote its brand in the face of steep competition and skepticism from Wall Street that the company is a loser in the age of AI.

The owner of the Nasdaq 100 Index is proposing to speed up the inclusion of newly listed, large-cap firms in the widely followed equity benchmark as a flurry of technology giants are slated to go public this year.

New York Times Co. tumbled after its results raised concerns on Wall Street about a jump in spending. Operating costs rose by more than 10%, which the company partially attributed to growing litigation costs, higher compensation expenses and new product development.

The Washington Post, owned by billionaire Jeff Bezos, began a round of job cuts on Wednesday that will shrink nearly all of its news departments, an effort to pare losses and restore the struggling newspaper to profitability.

Target Corp.’s new chief executive officer, Michael Fiddelke, acknowledged in his first town hall that the big-box retailer has lost trust with shoppers and employees and pledged to rebuild that connection.

Chipotle Mexican Grill Inc.’s doldrums are set to extend into 2026, with the burrito chain offering a full year-sales target that fell short of Wall Street’s expectations.

Uber Technologies Inc. issued a mixed forecast and promoted an outspoken driverless-vehicle bull to be its new chief financial officer, signaling further investment in a closely watched area of the ride-hailing company’s business.

Ford Motor Co. has held discussions with China’s Zhejiang Geely Holding Group Co. about sharing manufacturing capacity in Europe, with the US carmaker seeking new global partnerships as it overhauls its electric vehicle strategy.

Prudential Financial Inc. said it expects its decision to halt new life insurance sales in Japan to result in a $300 million to $350 million impact on its profit this year, Chief Executive Officer Andy Sullivan said Wednesday.

Eli Lilly & Co. provided an upbeat sales forecast for the year Wednesday as strong demand for its weight loss drug cemented its position at the top of the obesity market.

Novo Nordisk A/S’s chief executive officer asked investors to stick with him after a dire sales forecast caused a share price rout, saying a surge in prescriptions for cheaper obesity drugs will eventually revive growth.

AbbVie Inc. forecast 2026 profits above Wall Street’s expectations, though investors saw vulnerabilities in some of the company’s key brands.

GSK Plc’s new chief executive officer plans to speed up research and development and look for acquisitions as the British drugmaker tries to convince investors it can offset a looming patent cliff.

SAS AB is in talks with Boeing Co. and Airbus SE about making a large purchase of widebody jets as the Scandinavian carrier bets on increasing demand for long-haul travel from its hub in Copenhagen, the airline’s chief executive officer said.

First Brands founder Patrick James and his brother Edward pleaded not guilty to fraud charges and face a July 13 trial in New York stemming from the multibillion-dollar collapse of their auto-parts supply business.

D.E. Shaw & Co. criticized the board of CoStar Group Inc. in a letter to the company, putting further pressure on the real estate analytics group as it faces a separate campaign from activist investor Dan Loeb.

Enphase Energy Inc. said that the looming expiration of federal tax credits for clean electricity investments is boosting consumer demand.

Johnson Controls International Plc sees its adjusted earnings per share rising at the fastest pace in a decade after strong quarterly order growth.

Clear Street Group Inc., a Wall Street broker built on cloud computing technology, is looking to raise as much as $1.05 billion in an initial public offering.

Brookfield Asset Management named Connor Teskey chief executive officer, marking the final step in Bruce Flatt’s long-held plans to replace himself at the helm of the $1 trillion asset manager.

UBS Group AG posted a stronger increase in 2025 trading revenue than several of its US rivals, even as the Swiss company was forced to implement new capital rules ahead of almost all global banks.

Stellantis NV is facing delays to some electric models due to manufacturing difficulties at one of the company’s battery makers, according to people familiar with the situation.

Infineon Technologies AG said it will ramp up its investment in technology for artificial intelligence, working to diversify its business in a prolonged slump in auto and industrial chip demand.

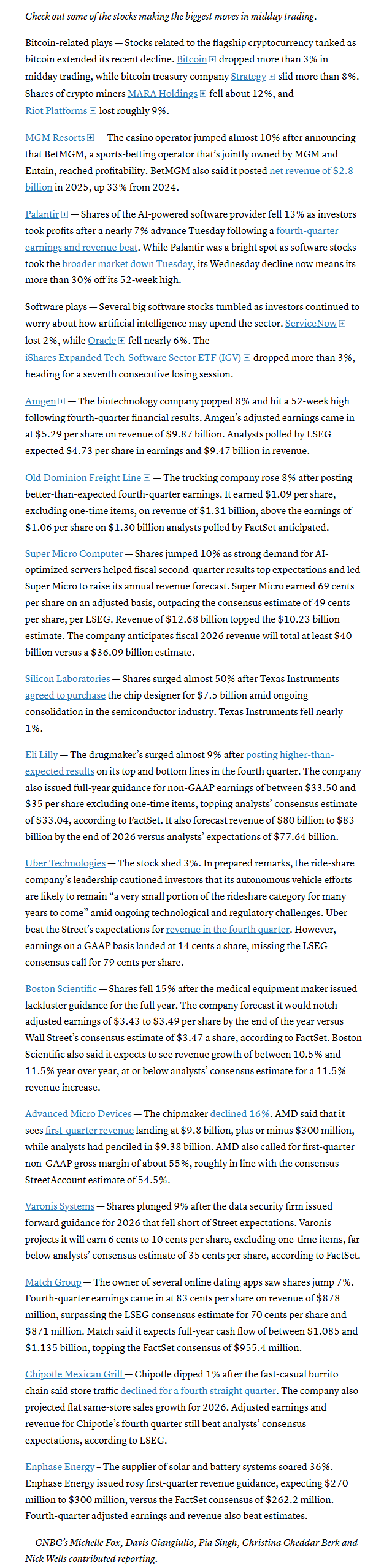

Mid-day movers from CNBC:

In US economic data:

Substack articles:

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X