Markets Update - 2/6/26

Detailed update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day/week with lots of charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!),

Link to posts - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog. Also please note that I do often add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

Finally, if you see an error (a chart or text wasn’t updated, etc.), PLEASE put a note in the comments section so I can fix it.

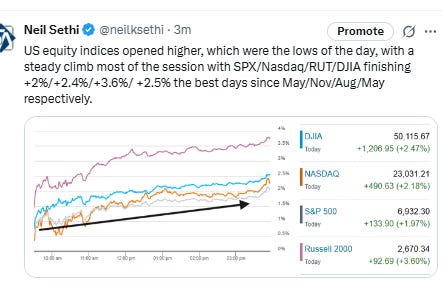

US equity indices opened today’s session solidly higher led by the small-cap Russell 2000 (RUT) even as as Amazon shares were sinking -8% (it would end -5.4%) after the ecommerce giant posted earnings per share slightly under analyst expectations and told investors to expect $200 billion in capital expenditures this year, well above expectations. Despite the issues with Amazon, other tech shares are higher: Nvidia rose 2% (a beneficiary of that spending, and it would extend that to +8%), and Microsoft was up by more than 1% (it would end +2%) after both companies had seen nearly double-digit percentage drops entering Friday’s session. Similarly some software names such as Oracle and Palantir Technologies also bounced back each rising 4%.

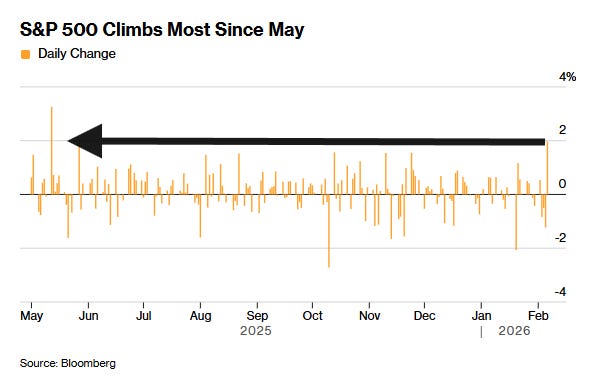

Those opening levels though would mark the lows of the session as indices saw a steady climb most of the day with the SPX, Nasdaq, Russell 2000 (RUT), and DJIA finishing +2%, +2.4%, +3.6%, and +2.5% respectively, the best days since May/Nov/Aug/May. For the week the gains were easily enough to push the RUT & DJIA positive, ending +2.2% & +2.5%, not quite enough for the SPX -0.1%, and not nearly enough for the Nasdaq -1.8% after sizeable losses Tues-Thurs.

Elsewhere, bond yields were slightly lower (chart) after breaking support Thursday, and the dollar was as well. Bitcoin, crude and copper recovered from early losses to close higher to join advances in gold and natgas. The first (bitcoin) jumped the most since Nov ‘24 after tumbling -16% overnight and briefly sinking below $61,000.

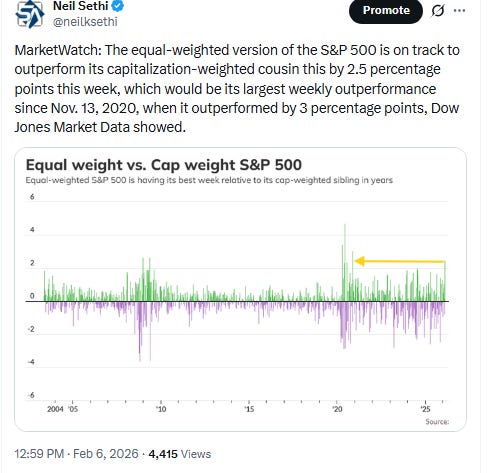

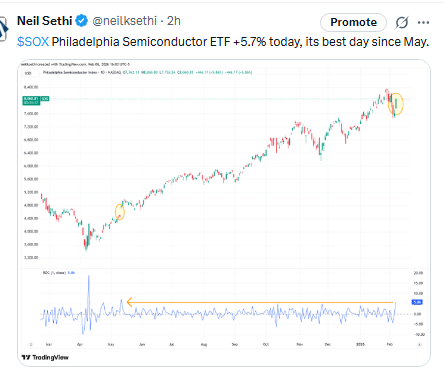

The market-cap weighted S&P 500 (SPX) was +1.9%, the equal weighted S&P 500 index (SPXEW) +1.9%, Nasdaq Composite 2.2% (and the top 100 Nasdaq stocks (NDX) +2.2%), the SOXX semiconductor index +5.7% (best day since May), and the Russell 2000 (RUT) +3.6%.

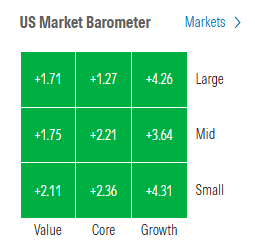

Morningstar style box not only all green but every style up over 1% with 6 of 9 up over 2%.

Market commentary:

“This is an opportunity for us as active investors to take the baby that has been thrown out with the bath water, because there’s still names out there that we believe will come out very well,” said Fabiana Fedeli, chief investment officer for equities, multi-asset and sustainability at M&G Investments.'

“Investors are rising to the occasion and aggressively buying the dip in stocks,” said Jose Torres at Interactive Brokers. “Basement ‘animal spirits’ are offering value hunters opportunities to accumulate shares amid a general sense on Wall Street that the selling has gone too far.”

“At 50,000, the Dow Jones Industrial Average grabs headlines, but it’s a reminder that milestones get louder even when less meaningful,” said Mark Hamrick at Bankrate. “The more meaningful S&P 500 is broader. It better reflects the performance of large US companies and is more relevant to many investors’ returns.”

“My view: this is overdone,” said Kenny Polcari at SlateStone Wealth. “This is the moment to keep your head on straight. It is not the time to panic. For long-term investors, this is the time to go shopping. A lot is on sale.”

The recent rout in technology stocks is a reason to buy the dip in the broader market as the US economic outlook remains robust, according to Anwiti Bahuguna at Northern Trust Asset Management. “It’s clearing off some of the froth in the markets,” she said. “We are actually seeing the use case for AI become clearer. From a macro sense, this is not the time to panic.”

“If AI begins to make entire, large sectors of tech no longer needed, that is a problem for the Nasdaq and the S&P 500 and that loss of earnings could offset AI efficiency gains in the short and medium term,” wrote Tom Essaye, president of the Sevens Report. “If AI blows up large market sectors, that won’t be good for the S&P 500.”

“The performance of tech is likely to determine if this early bounce in the broader market can hold,” said Tom Essaye at The Sevens Report. “If tech stocks can hold early gains and add to them, then we could see a solid bounce across markets.”

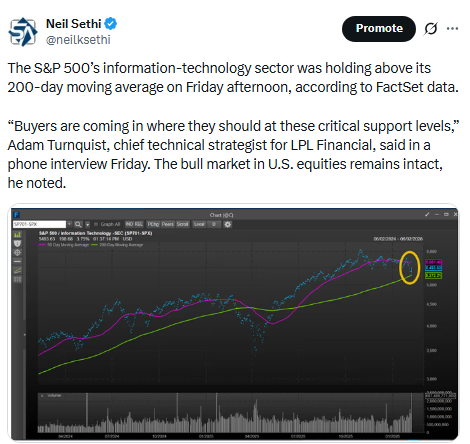

“For the broader market to make sustainable progress, renewed tech participation will likely be essential,” said Adam Turnquist at LPL Financial. “We expect the S&P 500 may have difficulty clearing the 7,000‑point milestone without stronger contributions from the tech sector — especially from software.”

For Rory Sandilands, a fixed-income portfolio manager at Aegon Ltd., uncertainty over the disruptive nature of AI may linger as it remains too early to tell how effective the new tools are, or how quickly other software may become obsolete. “What we’re seeing in the marketplace is fear, because nobody understands really who the winners and losers will be,” Sandilands said. “There’s not enough cushion in credit spreads in aggregate to really to help soften that blow.”

“The reassessment of AI sentiment does not materially alter our constructive view on the fundamentals of the Big Tech companies at the center of the AI capex cycle,” said Barclays equity strategist Venu Krishna. “Their valuations remain compelling, and we continue to see their earnings profiles as resilient even as the market temporarily steps back from AI‑driven narratives.”

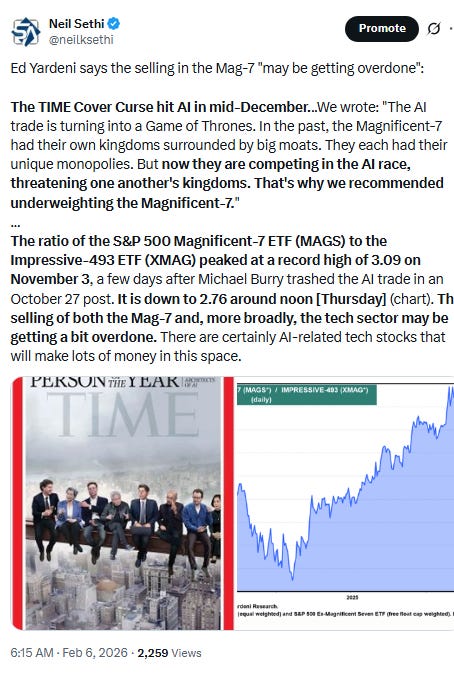

While many investors are worrying that such massive spending might not pay off, all that investment just this year will certainly provide lots of revenues and earnings to the companies that are vendors to the “hyperscalers,” said Ed Yardeni, founder of his eponymous research firm. The economy will also get a big boost from so much capex, he said, adding he “doubts” the sharp selloff in technology stocks this week the beginning of a “tech wreck.”

“We doubt it because this time, the industry has many more profitable companies benefiting from the enormous capital spending on AI infrastructure by hyperscalers,” the veteran Wall Street strategist concluded.

No matter what happens today, the issues surrounding the software companies — and the profitability of the AI industry — are not going to go away, according to Matt Maley at Miller Tabak. “Therefore, if they the tech stocks roll back over in a material way at some point over the next week or two, there will still be some meaningful risks to the tech sector going forward,” he said.

The issue here isn’t if AI will be profitable, but whether those profits are imminent, according to Florian Ielpo at Lombard Odier Asset Management.

“This temporal dimension constitutes a predominant market theme, and this week’s slight increase in risk aversion actually conceals a profound sector rotation, with investors moving away from the best-performing stocks of recent quarters,” he said.

“We’re in a gold rush right now with AI,” said Falcon Wealth Planning founder Gabriel Shahin. “You have the investment that Google is making, Nvidia is making, that Meta is making, that Amazon is making. There is money that will be deployed,” he also said. “It’s just the carousel [of money movement] sometimes scares people.” Shahin believes the market is in the midst of a “great recalibration,” where investors are going to move further out of growth stocks and into value. Over the coming months, his bet is on large-cap value names. That played out Friday, with investors buying up shares in areas such as industrials and financials.

“The question isn’t: Will AI be profitable?” said Florian Ielpo at Lombard Odier Asset Management. “But: are profits imminent? This temporal dimension constitutes a predominant market theme, and this week’s slight increase in risk aversion actually conceals a profound sector rotation, with investors moving away from the best-performing stocks of recent quarters.”

The February volatility is understandable since January was such a strong month, and corrections and pullbacks are relatively common during the month of February, according to Clark Bellin at Bellwether Wealth. “The bull market is not dead, but it is aging, and we are not be surprised to see investors paying more attention to corporate earnings and profitability,” he said. “Our message to investors is to remain opportunistic when stocks dip, but not necessarily during every dip. 2026 should still be a positive year, with plenty of opportunities to buy stocks on sale.”

“We maintain our view that opportunities in equities this year should expand across geographies, sectors, and structural themes, and investors with concentrated positions should diversify their exposure,” said Ulrike Hoffmann-Burchardi at UBS Global Wealth Management. “We acknowledge the risks reshaping software economics and believe investors should maintain roughly a 10% allocation to software within their broader tech exposure,” she said. “We continue to advocate a balanced positioning across the enabling, intelligence, and application layers of the AI value chain, and see particular value in companies and sectors that can use and apply AI to improve business outcomes.” Still, Hoffmann-Burchardi maintains her view that opportunities in equities this year should expand across geographies, sectors, and structural themes, and investors with concentrated positions should diversify their exposure.

Emotional deleveraging selloffs such as the one that took place earlier this week can be “unnerving,” but are “normal and healthy calibration” events, reminding us of the old proverb: “Trees don’t grow to the sky,” according to Mark Hackett at Nationwide. “At this point, the macro and earnings environment remain encouraging, suggesting this is more a positioning shift and technical pause rather than a fundamental crack,” he said.

“The theme of a ‘rotational bull market’ continues to hold true,” said Craig Johnson at Piper Sandler. “We continue to favor relative strength in sectors such as energy, materials (non-precious metals), industrials, transportation, healthcare, banks, and select areas of technology and discretionary.” The more this market rotates, the more it truly becomes a “stock picker’s market,” he added.

AI will remain a structural growth driver, but investor focus is shifting from broad-based enthusiasm toward differentiated business models, capital efficiency, and defensible revenue streams, said Bob Savage at BNY. Software companies that adapt toward client-specific solutions and integrate AI as an enabler rather than a replacement should regain investor confidence, particularly outside the US, where valuations remain more compelling, he noted. “At the same time, defense, space and energy infrastructure are converging as strategic investment themes, driven by national security priorities, power constraints, and technological ambition. FX dynamics, home bias and policy frameworks – especially around data sovereignty and energy security – will increasingly influence capital allocation,” Savage concluded.

A combination of the Trump administration’s focus on affordability and a weakening employment picture could open the door to further rate cuts, said Mohit Kumar, chief strategist for Europe at Jefferies. “Our view remains that we could get a scenario where growth is robust and yet employment is weakening due to the impact of AI,” Kumar wrote. “A Warsh-led Fed could end up being more dovish than what the market currently expects.” The policy shift would support small caps and the broadening rally beyond tech and AI, Kumar said.

“After a meaningful pullback this week, we’re ending on a high note,” said Louis Navellier at Navellier & Associates. “There is no doubt that AI is boosting productivity and also reducing jobs in corporate America.”

To Navellier, that will translate into Federal Reserve rate cuts that hopefully will boost consumer confidence in the upcoming months.

These will also be in the Week Ahead along with lots more on these topics.

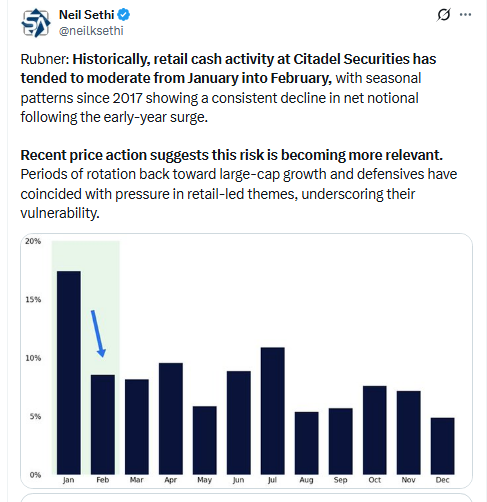

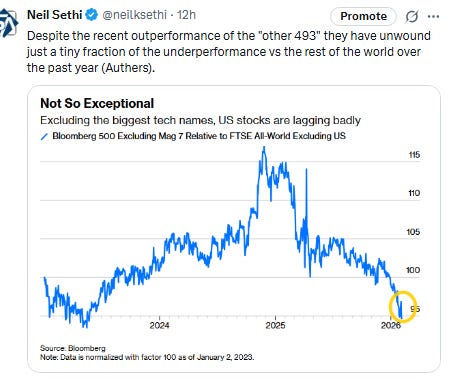

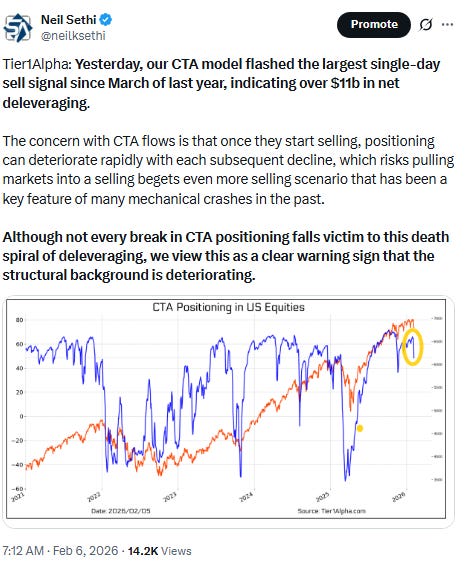

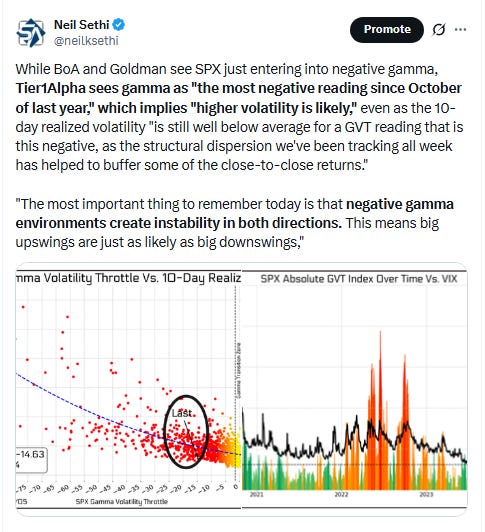

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

Caterpillar and Goldman Sachs were standouts, supporting the Dow’s outperformance with their rise of 7% and 4%, respectively.

While Oracle and Palantir Technologies bounced back (as did the overall IGV Software ETF which finished +3.5%), some key software stocks like ServiceNow — which has been the epicenter of the tech sell-off because of an artificial intelligence disruption fear of software — remained weak on Friday.

Companies making the biggest moves after-hours from CNBC.

None today.

Corporate Highlights from BBG:

Apple Inc. is preparing to allow voice-controlled artificial intelligence apps from other companies in CarPlay, according to people familiar with the matter, a move that will let users query AI chatbots through its vehicle interface for the first time.

Tesla Inc. isn’t waiting around to see if Elon Musk’s 100-gigawatt solar ambition is feasible — it’s already acting on it. The company is evaluating multiple sites across the US to begin manufacturing solar cells, according to people familiar with the matter.

JPMorgan Chase & Co., Goldman Sachs Group Inc. and Bank of America Corp. boosted their bonus pools for bankers and traders by at least 10%, as the businesses benefited from a banner year in dealmaking and market activity.

Exchange operator Cboe Global Markets Inc. plans to roll out options contracts that will enable binary bets on event outcomes, in a bid to enter the fast-growing prediction markets.

Exxon Mobil Corp. and Chevron Corp. are setting their sights on expanding production in nations tied to OPEC, including some of the world’s riskiest geopolitical hotspots, as President Donald Trump’s assertive foreign policy helps them strike deals.

ConocoPhillips Chief Executive Officer Ryan Lance’s priority in Venezuela is recouping billions his company is owed almost two decades after its oil projects were nationalized, rather than drilling new wells.

Biogen Inc. forecast 2026 profit above Wall Street’s expectations, signaling that steep cost-cutting measures are cushioning the impact of shrinking sales from its multiple sclerosis franchise.

Philip Morris International Inc. reported higher profit in the fourth quarter, helped by strong sales of smoke-free products such as Zyn nicotine pouches.

Molina Healthcare Inc. forecast 2026 profit that was less than half of Wall Street’s expectations, on higher medical costs and insufficient government repayments.

Roblox Corp. reported fourth-quarter users and bookings that beat analysts’ expectations thanks to a slate of hit games.

Carlyle Group Inc. exceeded its goals for fee-related earnings and asset growth in 2025, while posting fourth-quarter results that surpassed Wall Street estimates.

Compass Inc. lost a bid to temporarily block a Zillow Group Inc. ban on listings that have been advertised elsewhere first, after a judge ruled in favor of the home-search site in its legal battle with the largest US real estate brokerage.

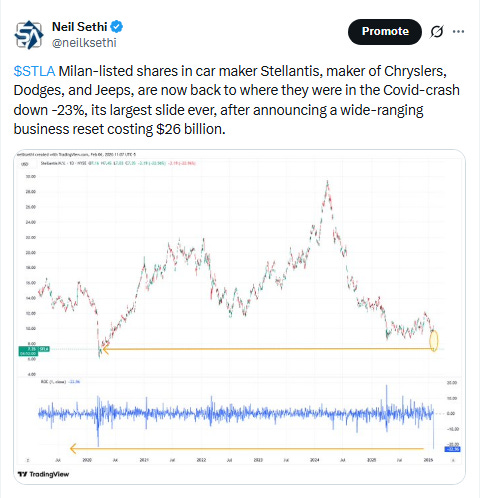

Stellantis NV is taking more than €22 billion ($26 billion) in charges mainly linked to reversing course on its electric vehicle strategy, prompting a plunge in the Jeep and Fiat owner’s shares.

BNP Paribas SA is considering raising bonuses for its global markets division by close to 10%, giving traders some of the biggest increases across the bank after a record year for the division, according to people familiar with the matter.

Orsted A/S plans to reinstate dividends and ramp up spending this year, even after a string of expensive setbacks in the US clouded the company’s turnaround efforts.

Tata Steel Ltd.’s profit grew eight fold in the third quarter led by robust demand and output at its Indian operations that helped the steelmaker overcome rising costs.

ByteDance Ltd.’s TikTok has been warned by the European Union that it needs to overhaul the design of its platform over fears addictive features could “harm the physical and mental wellbeing of its users.”

Mid-day movers from CNBC:

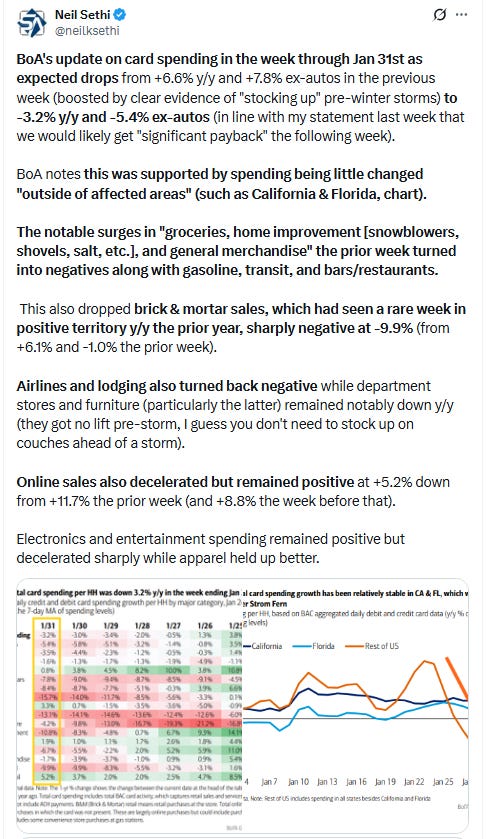

In US economic data:

Substack articles:

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X