Markets Update - 3/11/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with lots of charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!), here’s the button:

Link to posts on X - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog. Also please note that I do sometimes add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

Finally, if you see an error (a chart or text wasn’t updated, etc.), always appreciate a note in the comments section or email so I can fix it.

US equity indices opened trading Wednesday again with modest declines despite the consumer price index for February (so pre-Iran conflict), coming in as expected excluding food and energy at a tame 0.2% from January. From a year ago, it was unchanged at 2.5% — the slowest pace in nearly five years. Link is to my blog post summary.

The equity declines were also despite the International Energy Agency proposing the release of 400 million barrels of oil, more than double the agency’s biggest prior release in 2022. The proposal would be approved later this morning. Goldman Sachs said though the record release would offset just 12 days of their estimated 15.4 million barrels per day of export disruption (roughly equal to the disruption to date).

So despite the release (and announcement from Japan that they would also be releasing oil), crude continued to rally in another volatile session with Brent prices remaining above $90 (WTI just below), as the UK Navy said three vessels were hit with suspected projectiles in the Strait of Hormuz and Persian Gulf on Wednesday, it was reported that American forces had sunk 16 minelayers near the Strait of Hormuz as Tehran was seeking to mine the critical shipping route at the center of concerns around oil supplies, and Iran continued to increase its rhetoric saying it not only had no plans for surrendering, but that it would further escalate its attacks and would only stop if the US paid reparations and guaranteed neither it nor Israel will strike the country in the future.

The continued elevated oil prices saw bond yields continue their rise as Fed rate cuts fell to the lows of the year (with now just one cut priced through the end of next year) further pressuring equities (all covered in the subscriber section). And sentiment was also dented after the Financial Times reported that JPMorgan Chase & Co. marked down the value of loans and tightened lending and Bloomberg reported continued large withdrawal requests from other credit funds as concerns mounted over private credit.

Oracle shares though were a bright spot Wednesday, jumping 9% after the software vendor’s earnings and revenue for the fiscal third quarter exceeded analysts’ expectations. The company also raised its fiscal 2027 revenue forecast.

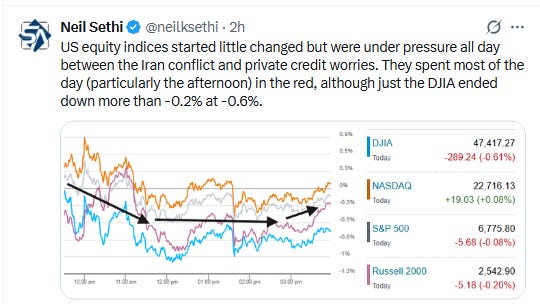

With the pressures noted above, indices spent most of the day (particularly the afternoon) in the red, although just the DJIA ended down more than -0.2% at -0.6%

Elsewhere, bond yields as noted continued their climb, and the dollar, crude, natgas, and bitcoin would all also end higher, while gold and copper were lower (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was -0.1%, the equal weighted S&P 500 index (SPXEW) -0.3%, Nasdaq Composite +0.1% (and the top 100 Nasdaq stocks (NDX) UNCH), the SOXX semiconductor index +0.6%, and the Russell 2000 (RUT) -0.2%.

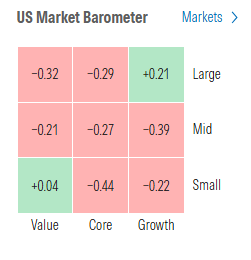

Morningstar style box shows no style moving more than a half percent.

Market commentary:

“[The IEA release] is helpful, but it’s more a short-term fix,” said Richard Saldanha, global equity fund manager at Aviva Investors. “The reality is, the way we’re going to avoid any kind of long-term shock is the Strait of Hormuz re-opening again.”

The decision made by the IEA “doesn’t solve the other issues that are going to affect the global economy,” according to Ron Albahary, chief investment officer at Laird Norton Wetherby. He cited refined products that flow through the Strait of Hormuz such as jet fuel as one of the problems posed. “I think the markets are wrestling with that idea of what is the off-ramp at this point,” he said to CNBC. “Both sides have dug their heels in, and it’s hard to see how this comes out positively on the other side in the short term.”

“We’re set for days of upcoming volatility, as the conflict in the Middle East is far from being resolved,” said Roland Kaloyan, head of European equity strategy at Societe Generale SA. “Moving forward, there are high chances of seeing alternating risk‑on and risk‑off days.”

“Trump suggesting the war may be ending soon, post an extraordinary surge in oil volatility, may imply his ‘pain threshold’ has been reached, in our view. This has reinforced market expectations of a quick de-escalation,” wrote Emmanuel Cau, head of European equity strategy at Barclays, in a Wednesday note.

“The longer the oil spike persists, the higher the downside risk to earnings and valuations,” he also wrote.

“Clearly, energy traders are not convinced that the proposed release of 400 million barrels of emergency oil reserves will be sufficient to curb energy prices in the near-term, leaving the focus on the latest developments at the Strait of Hormuz,” said Ian Lyngen at BMO Capital Markets.

“Investors and the Fed are in uncharted territory right now, taking their cues from crude oil and tanker traffic in the Strait of Hormuz,” David Russell at TradeStation.

“February’s inflation numbers were heading in the right direction, but then along came the conflict in the Middle East and now the path is changing,” said Brian Jacobsen at Annex Wealth Management.

“At least going into this energy price shock, inflation does seem to be stabilizing and we are seeing some confirmation that the tariff effect on inflation is fading now,” said Sal Guatieri, senior economist at BMO Capital Markets.

February’s reading of the consumer-price index “wasn’t as bad as feared,” said Ross Mayfield, a Kentucky-based investment strategist at Baird Private Wealth Management. “This CPI doesn’t capture the recent energy spike, so people may be looking past it.” At a minimum, “it shows there’s not underlying inflation pressure building separate from the energy spike, and that may be providing a ballast,” he said in a phone interview. “There’s a real worry about stagflation risk at the moment. We’re kind of in a holding pattern waiting for updates on Iran all day.”

The good news is that February's CPI released on Wednesday "was very much inline with expectations," said Art Hogan, chief market strategist for B. Riley Wealth. "The bad news is that March’s inflation data is going to be a harder pill to swallow, as it will reflect the effects of the war with Iran," he wrote in an email.

“Despite the prospect of releasing oil reserves, continued uncertainty translates into continued upside risk for oil prices, and that translates into a Fed that will remain cautious about cutting interest rates,” said Ellen Zentner at Morgan Stanley Wealth Management.

While investors are far more focused on how the conflict in Iran feeds into inflation over the months ahead, the latest inflation data offers some reassurance that underlying price pressures were not moving in the wrong direction before the latest energy shock, according to Seema Shah at Principal Asset Management. “The Fed has historically looked through energy‑driven price spikes,” she said. “But with inflation having sat above target for almost five years, it may be harder to do so this time.” Her base-case remains two rate cuts in the second half of the year, though that outlook would be at risk if energy prices remain high and the conflict drags on.

Market-based expectations for the Fed haven’t changed in the near term, with a nearly zero probability of a rate cut next week being priced in, according to Jim Baird at Plante Moran Financial Advisors. “Nearly no one is expecting the Fed to ease, but there’s also nearly universal recognition that the Fed’s job has gotten harder,” he said.

“The violent move higher in oil and gas prices over the last week may have ripple effects on the consumer, airlines and industrials and may cause the inflation data to increase for the next few quarters,” said Skyler Weinand, chief investment officer at Regan Capital. Until the Strait of Hormuz is reopened and the turmoil in the Middle East simmers down, the Federal Reserve may “step away from any action” on interest rates, Weinand told MarketWatch in emailed commentary. Policymakers now have tariffs, potential tariff refunds, higher energy prices and weakening employment to sort through in order to get any kind of clarity on what to do next, he noted. “This may be the last year-over-year print we see around 2.4% for a while as CPI potentially moves back towards 3% or above,” he said.

“Rates are up a lot today, and oil prices are up as well. That’s all pretty directly related to what’s going on in Iran. The flow of oil being stopped is going to push inflation higher,” said portfolio manager Jed Ellerbroek at Argent Capital Management in St. Louis. “Higher inflation may mean no more rate cuts by the Fed — placing additional stress on credit for both businesses and consumers.”

“Everything going on in the world is the spark in the flame, or gasoline on the fire, of inflation,” Ryan Jacobs, founder of Florida-based advisory firm Jacobs Investment Management, said in a phone interview. “Treasury yields were ripe for increases.”

Fed-funds futures traders now see a reduced likelihood that the Federal Reserve will be able to deliver more than one quarter-point interest-rate cut by December, according to the CME FedWatch Tool. Jay Hatfield, chief executive of Infrastructure Capital Advisors in New York, said the rise in the 10-year yield was being driven "almost exclusively" by expectations of where the fed-funds rate will end up and that he sees a chance that it can rise to 4.3% "pretty quickly."

While the 10-year Treasury yield at its current level may not signal the market is worried about inflation, investors should be on guard if it surges from here, according to Paul Hickey of Bespoke Investment Group. “It’s been like the S&P 500 — it’s just moving up and down in a range,” he said on CNBC’s “Money Movers” on Wednesday. “If we were to go above 4.5% in short order, I think that would be a cause for concern.”

“If you see 4.5% at the end of the year, which I wouldn’t expect, that’d be less concerning, but if you see 4.5% in a month or two, that’d be a big concern,” he added.

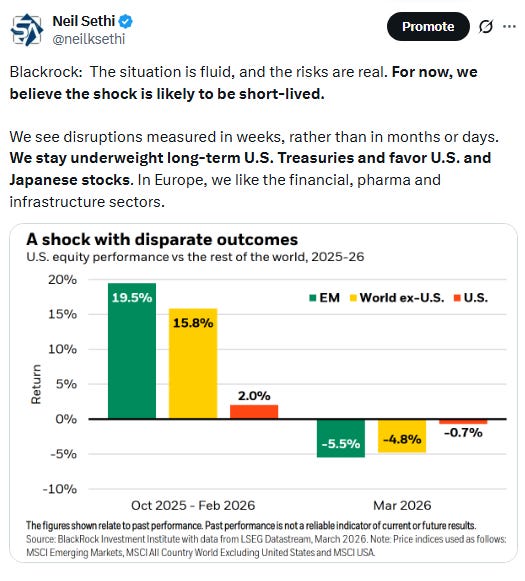

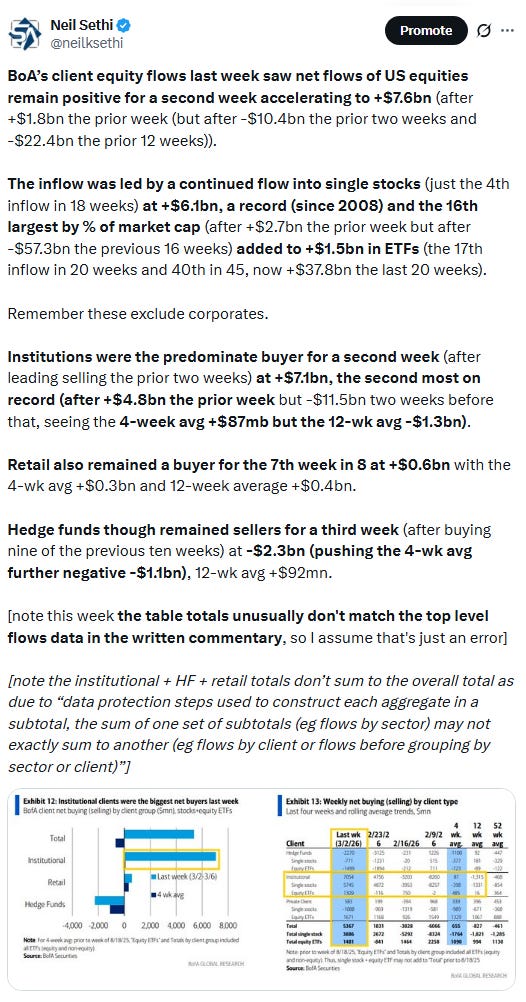

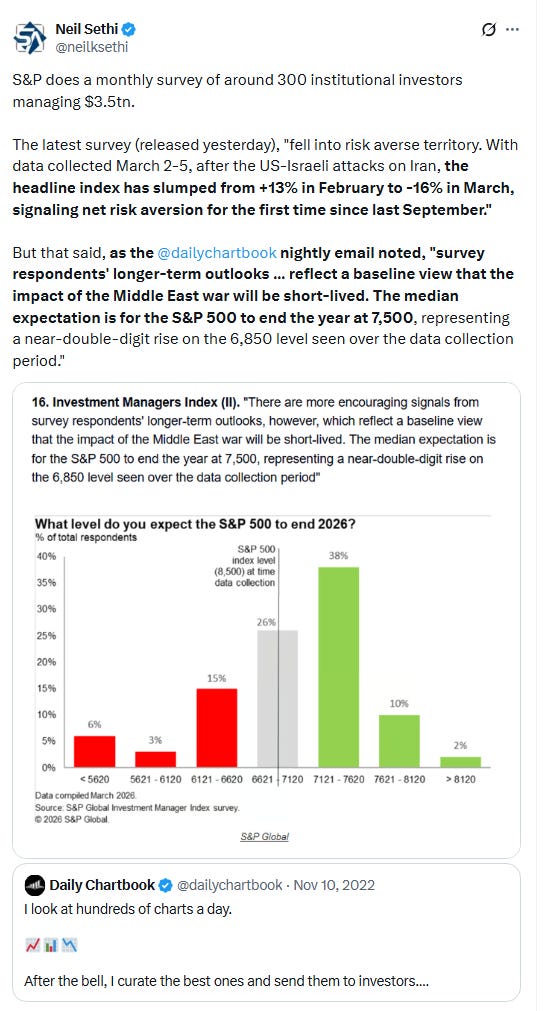

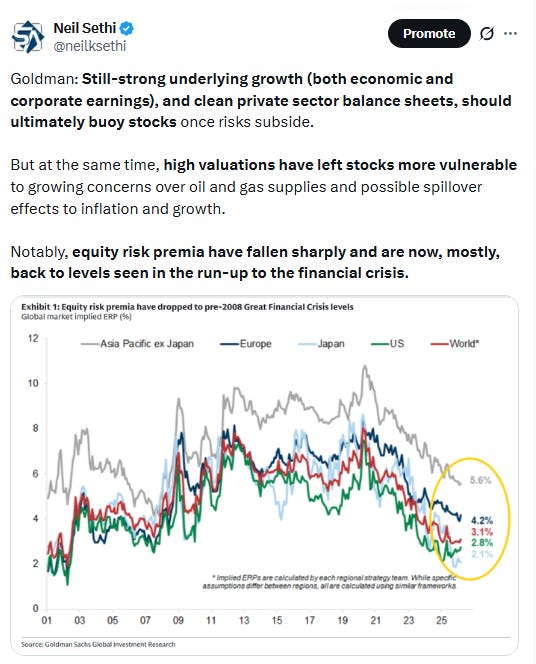

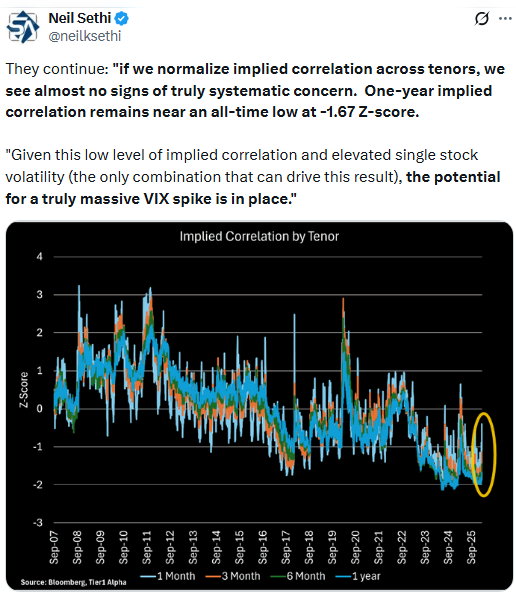

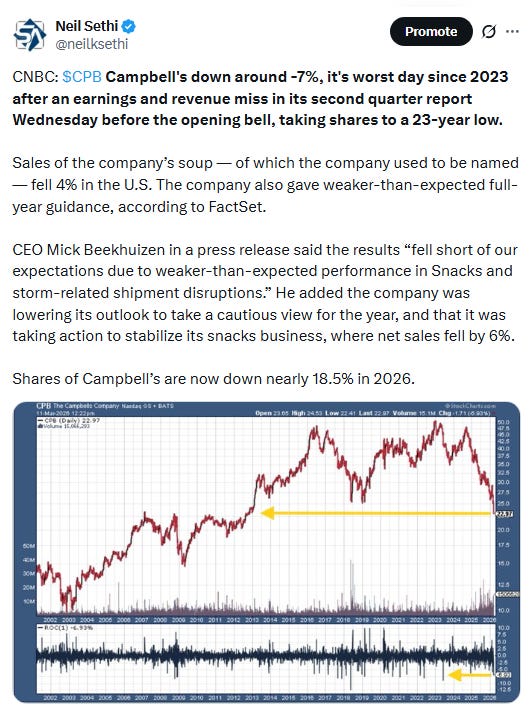

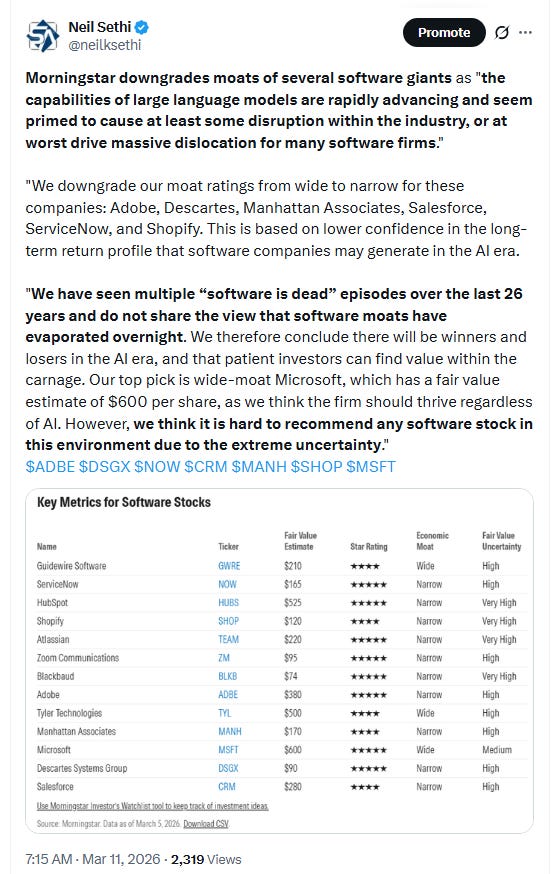

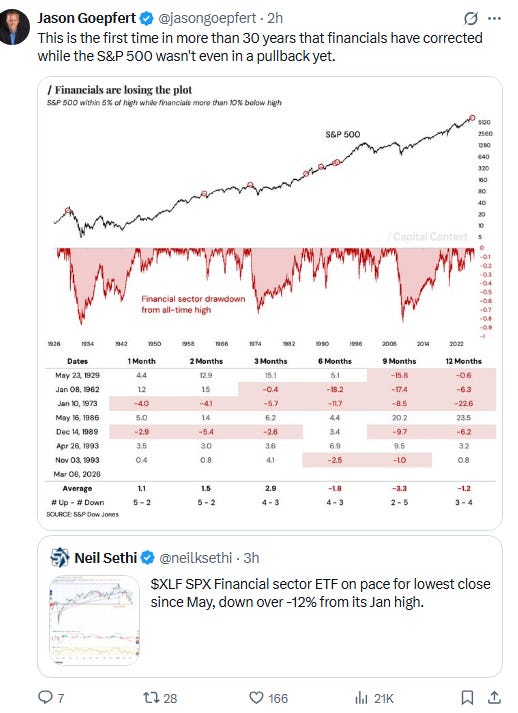

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

Corporate news from BBG:

Oracle Corp. soared after reporting strong sales and issuing an outlook that suggests little letup in demand for AI computing.

Nvidia Corp. will invest $2 billion in Nebius Group NV as part of a strategic partnership to develop and build AI data centers.

Salesforce Inc. drew lukewarm demand for its $25 billion bond sale amid concerns over its debt-funded share buyback and worries about software companies’ AI exposure.

JPMorgan Chase & Co. is restricting some lending to private credit funds after marking down the value of certain loans in their portfolios.

A cyberattack against medical technology maker Stryker Corp. crippled its global operations, according to a person familiar with the matter and a memo seen by Bloomberg News.

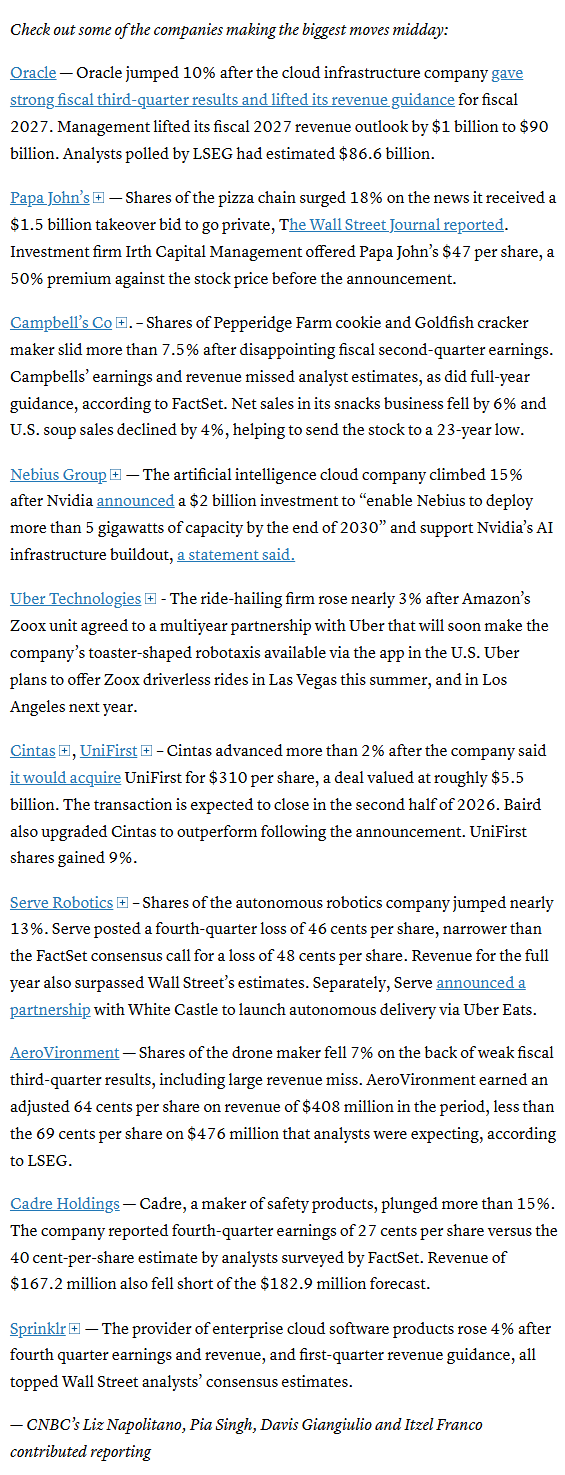

Mid-day movers from CNBC:

In US economic data:

Substack articles.

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X