Markets Update - 3/12/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with lots of charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!), here’s the button:

Link to posts on X - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog. Also please note that I do sometimes add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

Finally, if you see an error (a chart or text wasn’t updated, etc.), always appreciate a note in the comments section or email so I can fix it.

US equity indices opened trading Thursday with more significant declines pre-market after Iran launched a fresh wave of attacks on shipping in the Persian Gulf, pushing Brent crude back above $100 a barrel, which saw a continued rise in global bond yields. Adding to the pressure on equities today was more strains in the private credit market with Morgan Stanley and Cliffwater LLC becoming the latest to cap withdrawals from their multibillion-dollar private credit funds amid growing worries over the quality of loans.

Things would escalate during the session with Mojtaba Khamenei, who was appointed on March 9th as Supreme Leader saying that the Strait of Hormuz should remain closed as a “tool to pressure the enemy,” and Energy Secretary Chris Wright saying that the U.S. Navy is “not ready” to escort oil tankers through the Strait, though he said it will likely be able to do so by the end of the month. Brent’s close over $100 was the first since August 2022. Goldman Sachs Group warned that oil prices could exceed the 2008 peak if flows via Hormuz remain depressed through March. Brent rallied to a high of $147.50 that year.

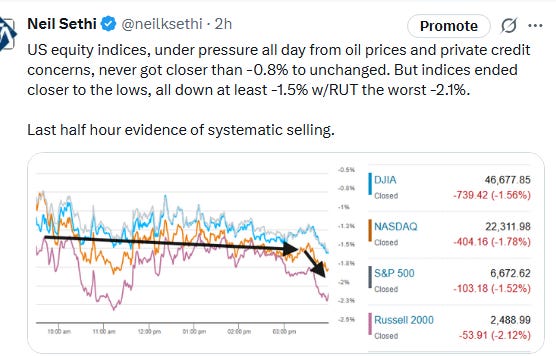

On the private credit front, Deutsche Bank flagged a $30 billion exposure to the sector. That added to pressures on financials, but the losses were broad with the industrial sector seeing its worst day since April, and all of the top 10 largest stocks other than Walmart closing lower. Indices never got closer than -0.8% to unchanged, and they ended closer to the lows than the highs, all down at least -1.5% with the small cap Russell 2000 the worst -2.1%.

Elsewhere, bond yields as noted continued their climb, and the dollar hit the highs of the year. Crude saw its highest close since 2022 as mentioned, and natgas was also higher. Gold, copper, and bitcoin would all end lower (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was -1.5%, the equal weighted S&P 500 index (SPXEW) -1.5%, Nasdaq Composite -1.8% (and the top 100 Nasdaq stocks (NDX) -1.7%), the SOXX semiconductor index -3.4%, and the Russell 2000 (RUT) -2.1%.

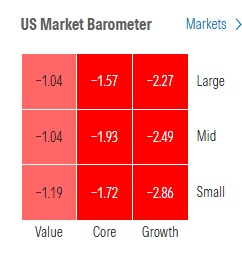

Morningstar style box shows no style losing less than -1% with all the growth styles more than -2%.

Market commentary:

“What you’re seeing is the market pricing a long-lasting scenario of high oil prices,” said Karen Georges, an equity fund manager at Ecofi in Paris. “The security of shipping in the region is a big concern while the release of emergency oil reserves can only provide temporary relief.”

For Francois Rimeu, senior strategist at Credit Mutuel Asset Management in Paris, the reaction in equity markets has been rather sanguine given how broad and impactful a worst-case scenario for the conflict could be. “The draw-down could really turn much lower should the conflict last longer, and the longer it lasts, the longer a return to business as usual will be,” Rimeu said. “If you ask me when is the right time to buy back, I would tend to say when one actually sees ships crossing the Strait of Hormuz again.”

“It’s telling that despite the periodic equity-market rallies over the last few days, the SPX has yet to recapture the 6800-7000 range on a closing basis. One can’t help but wonder if the risk is that one of these days, the market will decline to bounce after a negative opening gap, and instead more forcefully embrace a more negative outlook.” — Cameron Crise, Macro Strategist,

“The concerns over private credit, which emerged well before the US strikes on Iran, are adding to the negative mood despite the fact that European banks have little exposure on that asset class,” said Jerome Legras, head of research at Axiom Alternatives Investments.

"Trouble in the private credit market continues to simmer, and investor angst is spreading to hedge funds," wrote Chris Low, chief economist at FHN Financial, in a Thursday client note.

“As long as the bottlenecks around the Strait continue, oil prices will remain elevated, raising the risk that the conflict makes its mark on the economy,” said Bespoke Investment Group strategists.

“Iran’s strategy of sowing economic chaos in the Gulf is working as tankers come under attack and Hormuz stays shuttered, pushing Brent up toward $100,” said Adam Crisafulli of Vital Knowledge. “The U.S. and Israel have military dominance and Iran’s missile/nuclear programs may be degraded, but Tehran’s hardline [government] is firmly entrenched, and it’s plan now seems to be leveraging oil to push Trump further down an offramp.”

“The number one issue facing the markets right now is obviously the war,” said Matt Maley at Miller Tabak. “The conflict in the Middle East is not abating. This caused crude oil to spike. We also have the issue of the growing stress on the credit markets.”

If history is any guide, retreating from markets during periods of heightened volatility is unlikely the best strategy over the long term, according to Ulrike Hoffmann-Burchardi at UBS Global Wealth Management “But we believe holding sufficient liquidity to cover foreseeable expenses can help investors avoid forced selling in the event of a market drawdown,” she said.

“If energy costs and gasoline prices remain at current levels or rise for a period due to developments in the Middle East, it may weigh on consumer sentiment and push affordability issues to the forefront as we get closer to the midterm elections,” said Anthony Saglimbene, chief market strategist at Ameriprise.

“That said, overall consumer balance sheets remain in solid condition, income and employment conditions are currently sound, and inflation continues to ease in important pockets, namely shelter,” he continued. “Over time, if inflation continues to ease (outside of temporary energy impacts) and markets and the economy hold on firm footing, Americans’ attitudes about their ability to afford everyday life could improve.”

“The most hawkish outcome would be if the Fed removed its easing bias from the statement, while the median projection shifted from one cut this year to no change,” said Stephen Brown at Capital Economics.

“Fed officials will sit on their hands until they get some clarity around how the war with Iran is playing out and which of its mandates, low and stable inflation or full-employment, is most in jeopardy,” said Mark Zandi, chief economist at Moody’s. “That could take weeks, if not two to three months.” R\

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

Morgan Stanley led financials lower after capping private credit fund withdrawals. Energy stocks, including Chevron and Exxon Mobil, were among the few stocks in the green.

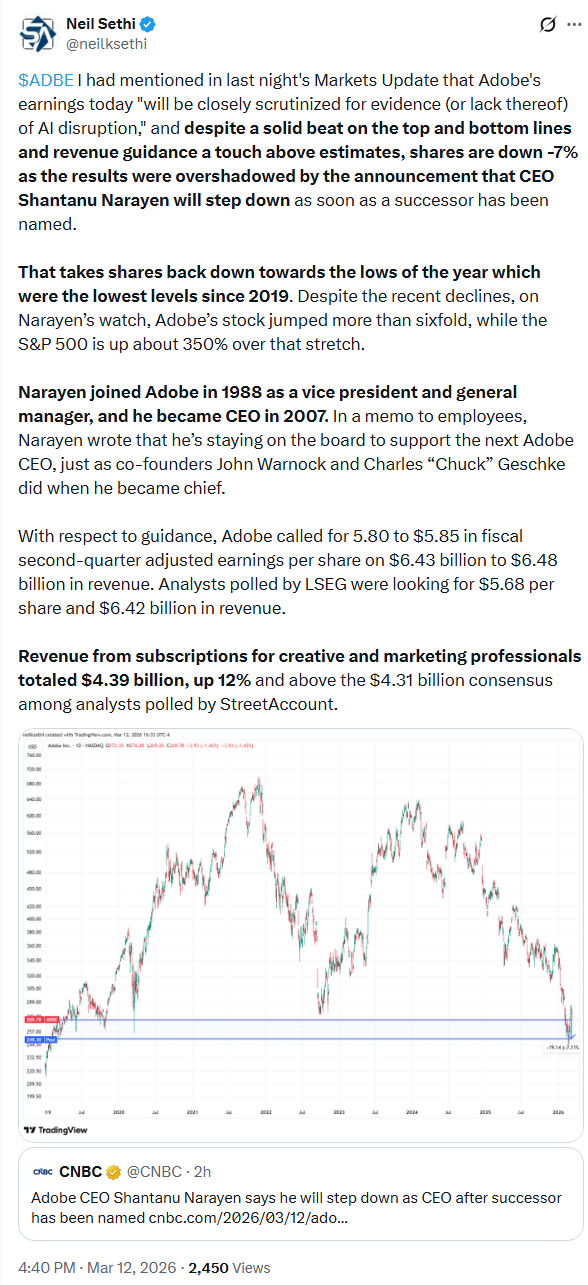

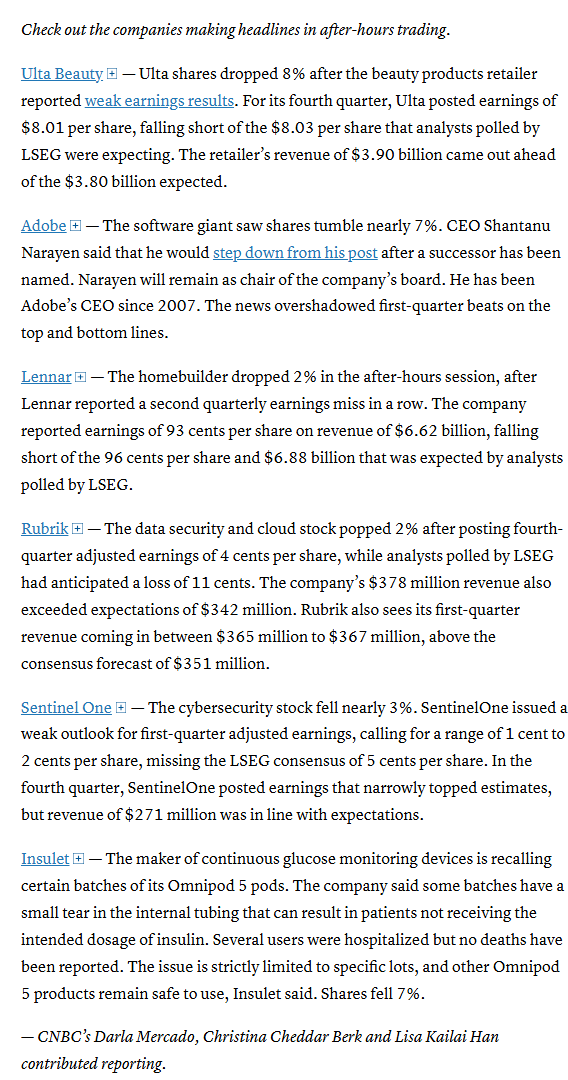

In late hours, Adobe Inc. gave a tepid outlook and said its chief will resign.

Stocks making the biggest moves after hours from CNBC:

Corporate news from BBG:

Energy producers climbed while CF Industries Holdings Inc. and Mosaic Co. paced a surge in fertilizer stocks as disruptions to the Strait of Hormuz tighten supply. Airlines sank on worries about higher fuel prices.

Blue Owl Capital Inc. defended its recent sale of $1.4 billion of loans from three of its funds, arguing the transaction contained no backstops or hidden incentives, as the asset manager remains a primary target of bets on a private-credit reckoning.

Tesla Inc. received government clearance to convert its investment in Elon Musk’s xAI into a small stake in SpaceX ahead of the rocket maker’s planned IPO.

Bumble Inc. soared on an upbeat outlook and the unveiling of a new AI-powered assistant designed to act as a personal matchmaker.

Dick’s Sporting Goods Inc. forecast full-year sales growth across the company’s namesake brand stores and the newly acquired Foot Locker chain.

Dollar General Corp. forecast sales in-line with analyst estimates, slowing momentum for a company that had been exceeding expectations.

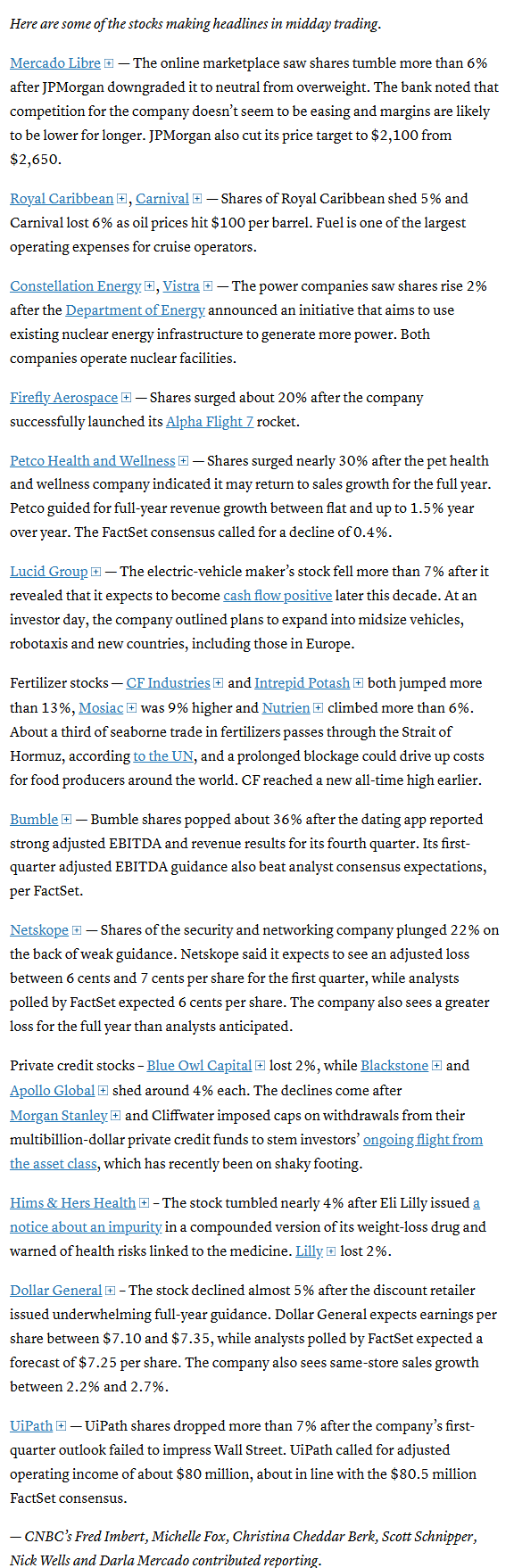

Mid-day movers from CNBC:

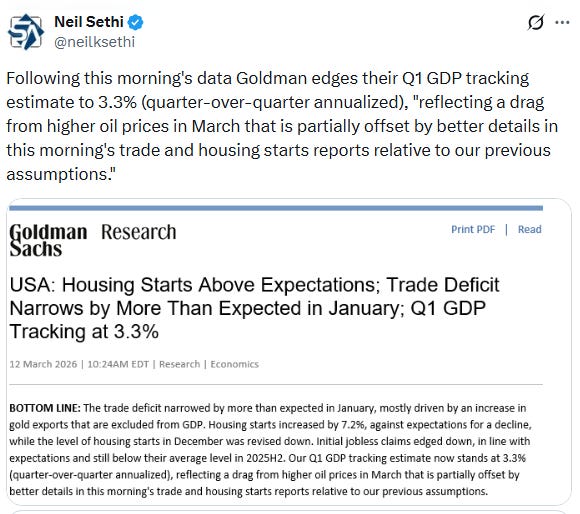

In US economic data:

Substack articles.

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X