Markets Update - 3/13/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with lots of charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!), here’s the button:

Link to posts on X - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog.

Also, if you see an error (a chart or text wasn’t updated, etc.), always appreciate a note in the comments section or email so I can fix it.

In that regard note I do make mistakes sometimes, and usually I catch them at some point and correct them, and/or I sometimes add new material, so it’s always safest to read from the website where it will have any updates.

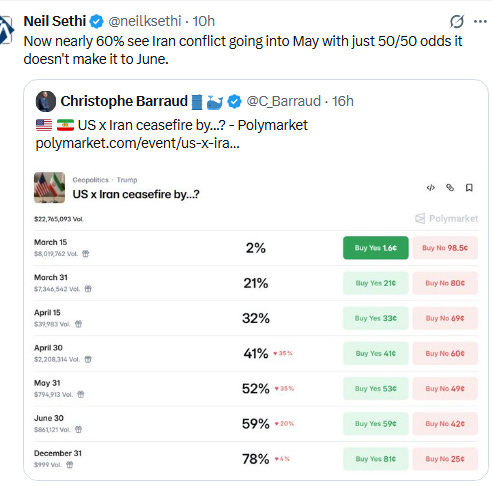

US equity indices opened trading Friday, in contrast to the last few days, somewhat higher pre-market helped by some modest softening in crude prices and a pause in the rise in bond yields, the latter in part due to a report that India had successfully sailed a tanker through the Strait of Hormuz. Also US Defense Secretary Pete Hegseth said during a press conference that Iran’s new supreme leader is wounded and likely disfigured. He also said Friday marked the largest attacks against the country. That was set against WSJ reports that Arab diplomats trying to find a diplomatic path out of the Iran conflict said Tehran has been emboldened by its ability to rattle the global economy and followed a statement from the Supreme Leader that the Strait should remain shut as a “tool to pressure the enemy”.

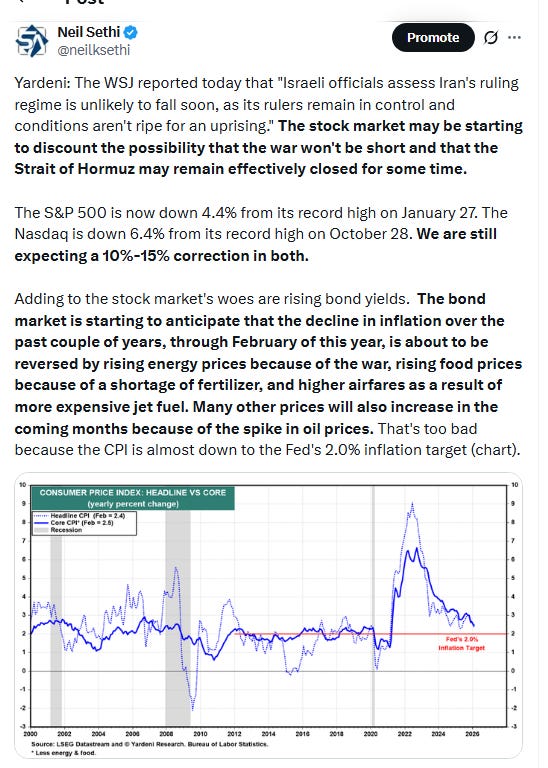

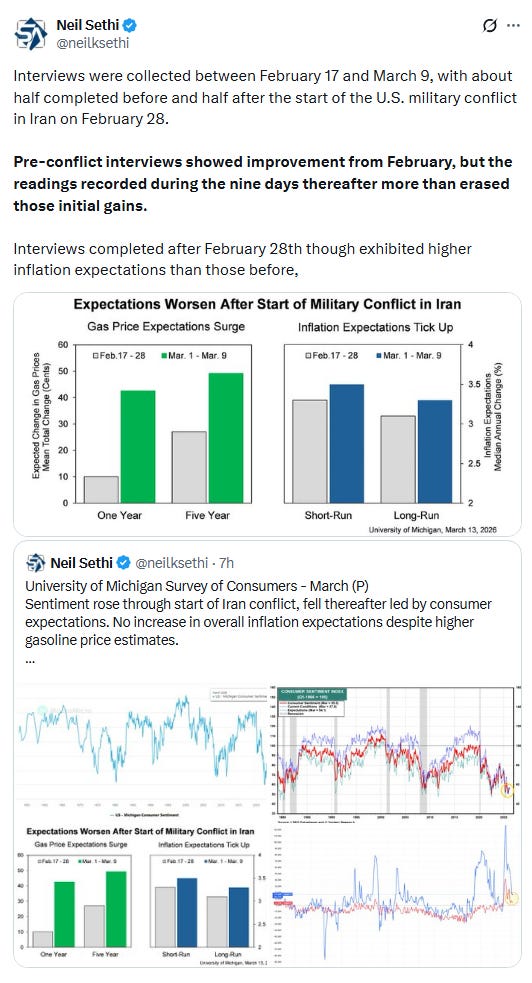

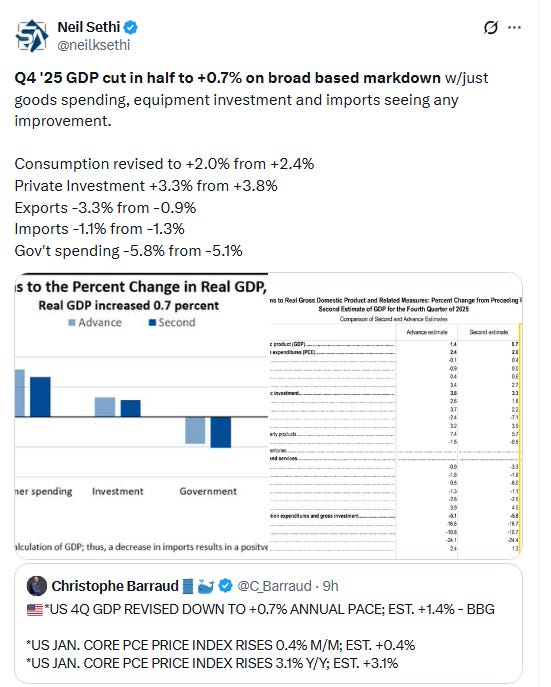

In economic data, US gross domestic product for the last quarter of 2025 was cut in half to a 0.7% annual rate (depressed by the shutdown), while in data for January the core personal consumption expenditures price index (which excludes food and energy items) — favored by the Federal Reserve — was up 0.4% from December and 3.1% from the prior year as expected (inconsistent though with near-term rate cuts). Inflation-adjusted consumer spending increased 0.1% from the prior month, slightly better than expected, but a weak reading. That would be followed after the open by the JOLTS survey for Jan showing a pickup in job openings but low hirings (and also low firings) and a consumer sentiment survey showing sentiment souring and inflation expectations picking up post-Iran conflict. Links in this paragraph are to my blog posts (posts on the other two reports to come).

Soon after the opening of trading though the softer crude prices and yields would reverse, and so would equities, falling into the red by late morning and continuing to fall into the afternoon, ending just off the lows, saved by an end-of-session buying spurt. Nasdaq led losses -0.9%, SPX -0.6%, DJIA/Russell 2000 around -0.3%. The SPX and Nasdaq closed the lowest since November, Russell 2000 since December.

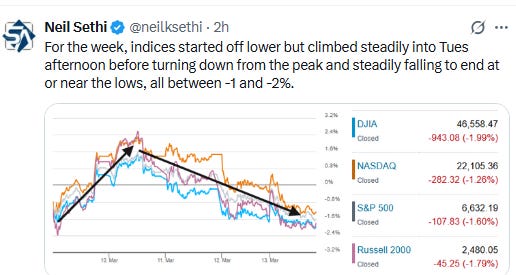

For the week, indices started off lower but climbed steadily into Tues afternoon before turning down from that peak and steadily falling to end at or near the lows, all between -1 and -2%.

Elsewhere, bond yields as noted continued their climb (10yr), and the dollar moved to the highest since May. Crude saw its highest close since 2022, and bitcoin was also higher. Gold, copper, and natural gas would all end lower (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was -0.6%, the equal weighted S&P 500 index (SPXEW) UNCH, Nasdaq Composite -0.9% (and the top 100 Nasdaq stocks (NDX) -0.6%), the SOXX semiconductor index +0.1%, and the Russell 2000 (RUT) -0.7%.

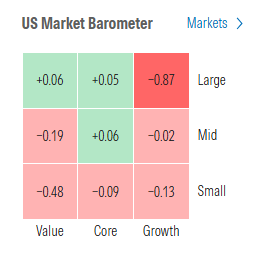

Morningstar style box shows most styles little changed, the main exception large growth, but even that was down less than -1%.

Market commentary:

Although the U.S. has said it would release 172 million barrels from its Strategic Petroleum Reserve over 120 days, the “market’s lack of response implies that the release is interpreted as a belated and insufficient measure given the lack of credible solutions to the blockage of the Strait,” writes Marko Papic, chief strategist at BCA Research. “Economic and military solutions have so far been unable to clear the Strait and reduce energy prices…The world needs a political solution, not a military one.”

“There are two paths at this time for markets and the better outcome is a shorter war,” said Chris Zaccarelli at Northlight Asset Management. “Likewise, if the length of the military conflict stretches out much longer than expected, we could see even more negative impacts on the markets.”

“Inflation is actually ramping up as a big risk,” Tracy Chen, a portfolio manager for global fixed income at Brandywine Global Investment Management, said on Bloomberg Television. “Duration of the conflict is key. We have been raising US dollar weighting a little bit just to increase our hedge.

Sonu Varghese, chief macro strategist at Carson Group, had this to say about the January PCE data released Friday. “The latest personal consumption expenditures (PCE) inflation data tells us that the inflation picture wasn’t looking good even before the Middle East crisis. Core PCE inflation is now up 3.1%, the fastest pace in almost two years and this is only going to head higher as the energy shock comes through,” Varghese said in written commentary. "The market needs to hear the strait is open," said Varghese. “The oil needs to flow,” he said. “Every extra day it is closed, the problem becomes bigger.”

“Despite signs of economic softening, more sticky inflation data simply strengthens the idea that the Fed will remain on the sidelines,” said Ellen Zentner at Morgan Stanley Wealth Management.

Underlying inflation pressures will continue to boil under the surface and next month’s print will also be elevated, impacted by the war in the middle east, according to Jeffrey Roach at LPL Financial. “We expect the Fed to highlight the uncertainty on both sides of the mandate,” he added. “Inflation will be impacted by the war and unemployment will be impacted by the disruptions in the labor market. Expect to see some important revisions in the upcoming Summary of Economic Projections next week.”

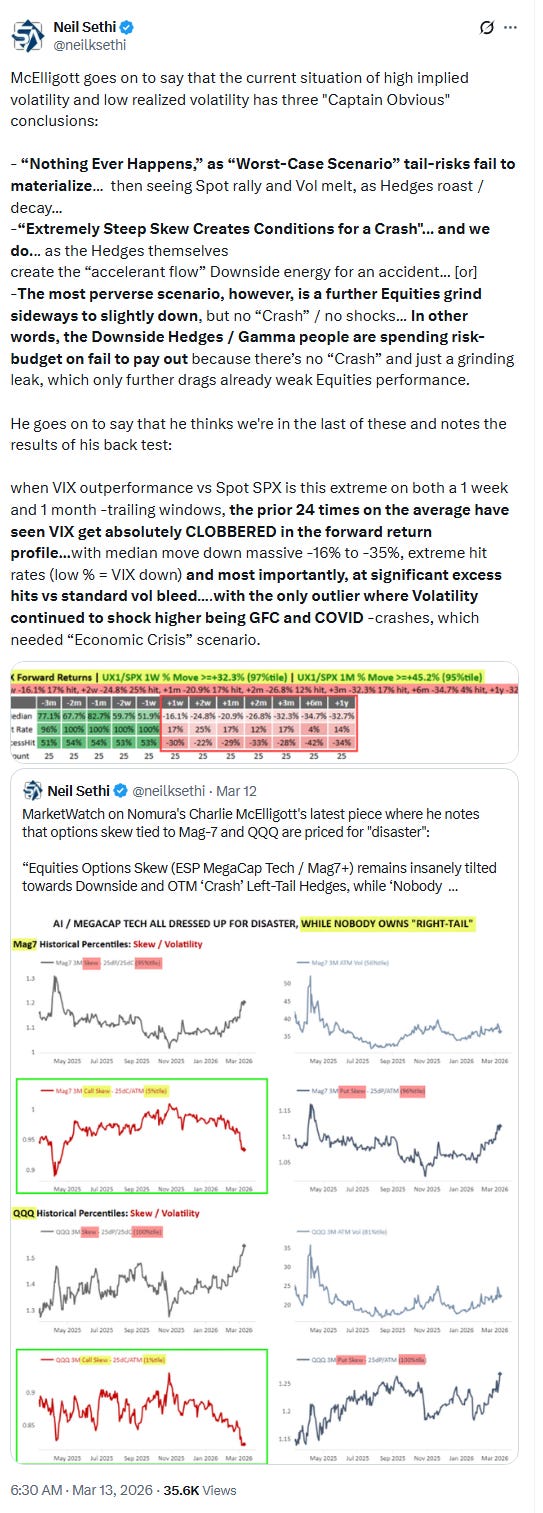

“Markets have sailed through the last quarter with an optimistic bias, sticking to a buy-the-dip mantra, but this spike in volatility is likely to put an end to this,” said Benoit Peloille, chief investment officer at Natixis Wealth Management. He added that even if the conflict doesn’t last much longer, “it may already have a palpable negative impact on economic growth and inflation.”

“On a very-short-term basis, it will likely continue to be a ‘headlines-driven’ market,” said Matt Maley at Miller Tabak. “Investors are staring to worry that the situation in the Middle East could drag on for a long enough period of time for it to have an impact on the economy.”

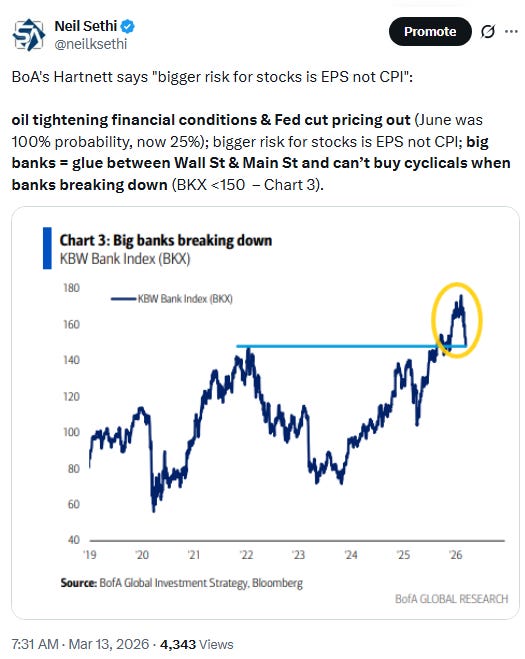

Higher oil prices, along with several other key hurdles in the market, have been causing investors pain, according to Chris Toomey, managing director at Morgan Stanley Private Wealth Management. Rising crude prices and growing inflation fears have also dampened investors’ expectations for Federal Reserve interest rate cuts this year. “You’ve got the [artificial intelligence] buildout, you’ve got private credit … and this energy situation,” he said on CNBC’s “Closing Bell.” “I think the energy situation is the thing that we’re most concerned about.” Toomey added that if Strait of Hormuz sees sustained impairment beyond two or three months, that “becomes a real problem.”

Stock markets are down this month as oil surges on fears over ongoing military strikes in the Middle East, yet equity investors are still pricing in “a short conflict with limited economic fallout,” according to Seema Shah, chief global strategist at Principal Asset Management. “So far, earnings expectations remain resilient, but a prolonged energy shock would begin to erode that foundation, negatively impacting risk assets with greater severity,” Shah said in emailed comments Friday.

“Earnings are pretty good, but sentiment is difficult,” said David Aspell, chief investment officer of global macro at Mount Lucas Management. “The oil part of the sentiment and equity valuation embeds an interest rate path which is now being questioned.

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

In index tracking the Magnificent-7 is now down -13% from its highs last October.

Corporate news from BBG:

Charles Schwab Corp. expects revenue growth of around 16% for the first quarter as retail investors remain engaged despite uncertainty about the direction of the economy and the war.

Boeing Co. is repairing damaged wiring in as many as 25 undelivered 737 Max jets, disrupting near-term deliveries of the aircraft, people familiar with the matter said.

Apple Inc. is lowering the fees it collects from app developers in China, a major concession in a hugely lucrative market where the company faced the risk of antitrust intervention by local regulators.

Adobe Inc. slipped as Chief Executive Officer Shantanu Narayen will resign from his position atop the creative software giant amid deep skepticism about the company’s ability to thrive in the AI era.

Carvana Co.’s board approved a 5-for-1 stock split, a move to bring down the automotive retailer’s lofty share price following a staggering multiyear rally from the depths of the pandemic.

Ulta Beauty Inc. sank after the cosmetics retailer offered guidance for the current year that was toward the low end of Wall Street’s expectations.

Mid-day movers from CNBC:

In US economic data:

Substack articles.

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X