Markets Update - 3/17/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!), here’s the button:

Link to posts on X - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog.

Also, if you see an error (a chart or text wasn’t updated, etc.), always appreciate a note in the comments section or email so I can fix it.

In that regard note I do make mistakes sometimes, and usually I catch them at some point and correct them, and/or I sometimes add new material, so it’s always safest to read from the website where it will have any updates.

US equity indices opened trading Tuesday like Monday higher, but the gains were much more modest as oil prices were again on the rise after Iran struck energy facilities around the Persian Gulf overnight, including setting a massive natural gas field in the United Arab Emirates on fire. Israel meanwhile said it killed Iran’s security chief, Ali Larijani, the highest profile assassination since the killing of the former Supreme Leader on the first day of the conflict.

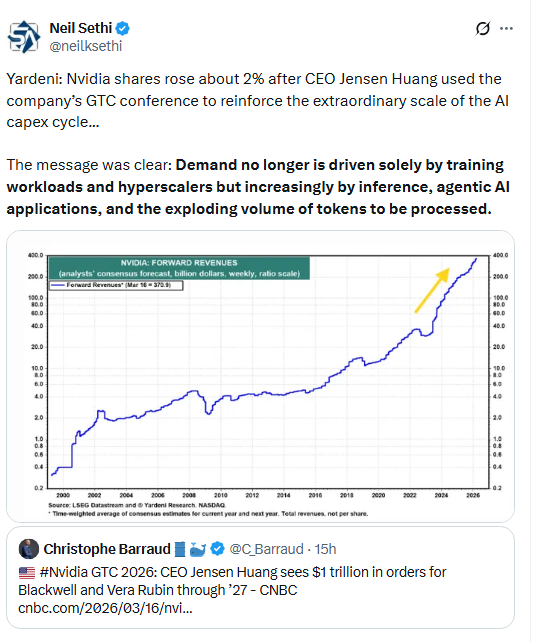

Supporting equities though was Nvidia after the firm said it expects to generate at least $1 trillion in sales from its flagship AI processors through 2027, and Delta Air Lines, which would advance more than 6%, after issuing an optimistic first-quarter sales target (and American would also raise its first quarter target saying travelers were rushing to lock in ticket fares). On the other hand Bank of America’s widely followed fund manager survey showed that investors are turning more bearish and holding more cash (see posts below).

Elsewhere, bond yields and the dollar were lower, as was copper, crude was higher, and gold, bitcoin, and natural gas were little changed (all covered in the subscriber section with charts).

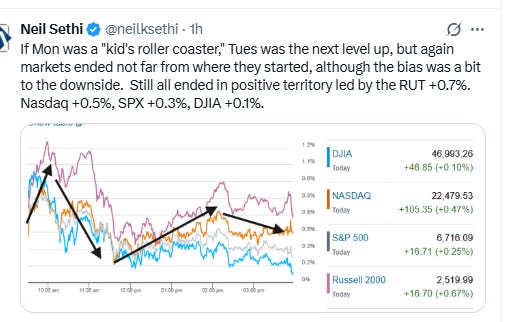

The market-cap weighted S&P 500 (SPX) was +0.3%, the equal weighted S&P 500 index (SPXEW) +0.5%, Nasdaq Composite +0.5% (and the top 100 Nasdaq stocks (NDX) +0.5%), the SOXX semiconductor index +0.5%, and the Russell 2000 (RUT) +0.7%.

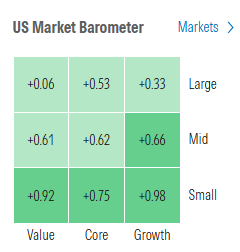

Morningstar style box shows every style in the green again today led by small caps.

Market commentary:

“Investors remain hopeful that a quick and relatively painless solution to the situation will be found, and that it will prove to be the latest in a long, relatively unbroken series of dip-buying opportunities,” said Steve Sosnick, chief strategist at Interactive Brokers. “There is also a fair degree of residual FOMO, which is why we small bounces morph into relatively substantial upward moves, even if a fundamental reason appears to be lacking,” he continued.

The stock market is trying to find a bottom amid this geopolitical-driven pullback, according to Rick Gardner at RGA Investments. While he says the conflict could go on for some time, that doesn’t mean the stock market would follow suit. “Stocks tend to move ahead of various events, like wars, well before they are over,” Gardner noted. “Valuations in stocks remain attractive, creating a potentially attractive entry point for investors looking to put new money to work.”

“There is a growing sense that markets are trying to look through the current tensions,” said Fawad Razaqzada at Forex.com. “A credible multinational effort would likely push oil lower and equities higher — but the best outcome would be to end the war and soon.”

“Iran will be forced to capitulate at some point,” writes BCA Research Chief Strategist Marko Papic. “Its ability to keep Hormuz closed indefinitely is unrealistic. A global coalition of naval escorts will eventually be assembled, as it was in the 1980s during the Tanker Wars.” Meanwhile, the Trump administration, faced with rising costs at home, has plenty of motivation to bring gas prices down.

US stocks are flashing their strongest buy signal in almost a year, according to Barclays’ Alex Altmann. The Barclays’ Equity Timing Indicator, or BETI, dropped to its lowest since the April tariff turmoil, he wrote. It reached a threshold that has historically marked “highly attractive” entry points.

“Investors might want to remember that recent rallies often faded,” wrote Joe Mazzola, head trading and derivatives strategist at Charles Schwab.

“Market participants may be assuming this is very similar to the Liberation Day tariffs imposed by the U.S., and that this will be a short-lived problem that ends once the U.S. chooses to withdraw from the military conflict,” said Kristina Hooper, chief market strategist at Man Group. “I think that is a mistaken assumption. Tariffs are a relatively simple problem for markets because they can be unilaterally withdrawn whenever the U.S. chooses to do so. Wars, unlike tariffs, cannot be turned on and turned off like a switch.”

The equity market’s willingness to rise in the face of high oil prices reflects the strong demand for stocks and expectations for solid earnings as well as economic growth, according to Louis Navellier. “Investors should expect continued volatility until the energy situation stabilizes,” said the veteran strategist. “There’s a relief rally in the future when a return to ‘normal’ energy markets becomes clearer. The sooner the Iran conflict is resolved, the better.”

“The longer the oil price stays above $100 per barrel, the louder the alarm bells for the market over inflation risks,” said Dan Coatsworth, head of markets at AJ Bell.

“There are a couple of reasons to take any signals from this [FOMC] meeting with a pinch of salt,” notes James McCann, senior economist for investment strategy at Edward Jones. “First, a swing in oil prices in either direction could quickly change the Fed’s thinking, and second, markets might slightly discount messages from [Fed Chairman Jerome Powell] given this will be one of the last of his term.”

“The bias is certainly that central banks will be more hawkish that the markets wants them to be,” said Andrew Chorlton, chief investment officer of fixed income at M&G Investment Managers. “We don’t expect anyone else to raise rates but no one is going to cut rates and any remaining expectations of rate cuts are slowly diminishing.”

“Risk assets like US stocks and cryptocurrencies have held up surprisingly well despite all the turmoil,” said Bret Kenwell at eToro. “Depending on whether the Fed strikes a more dovish or hawkish tone, that could shape the near-term direction for both into quarter-end.” Still, with so much uncertainty, the Fed may be more inclined to stay the course than shake things up, he added.

“Fundamentals have not changed: higher energy prices are driving a stagflationary shock, the extent of which depends on how long prices remain elevated. With the equity market reaction still tepid, there is scope for further downside.” — Skylar Montgomery Koning, macro strategist.

Many are crediting a relatively strong economy, contained inflation and strong earnings for continued momentum behind the stock market, but Bartlett Wealth Management president Holly Mazzocca said on Monday that “risks to that growth story are mounting.”

“We came into this year with a pretty strong foundation, but especially the labor market has weakened pretty significantly. So that’s the big question for investors right now, is just being realistic that the overall risks to that continued growth story are higher today than they were just a few weeks ago,” Mazzocca said on CNBC’s “Closing Bell.”

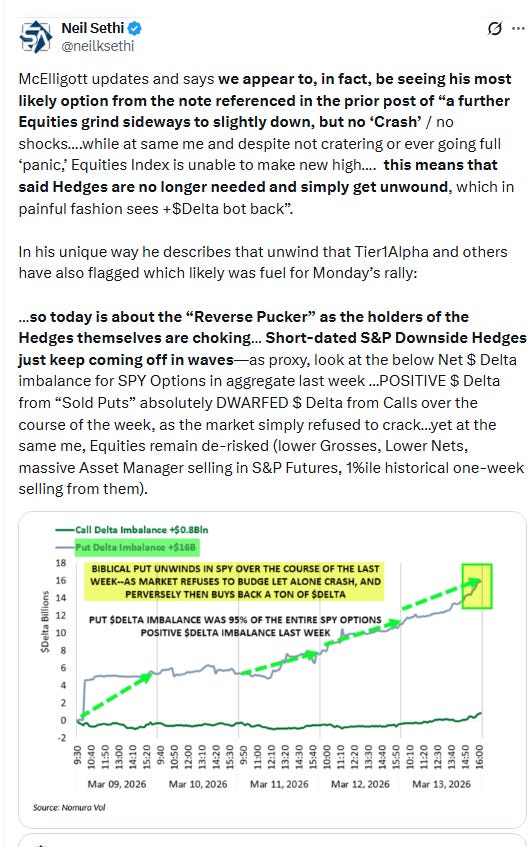

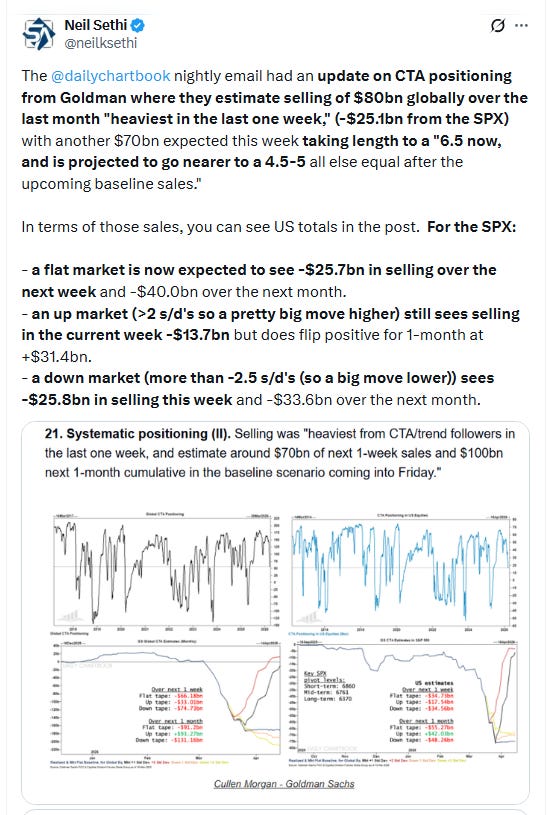

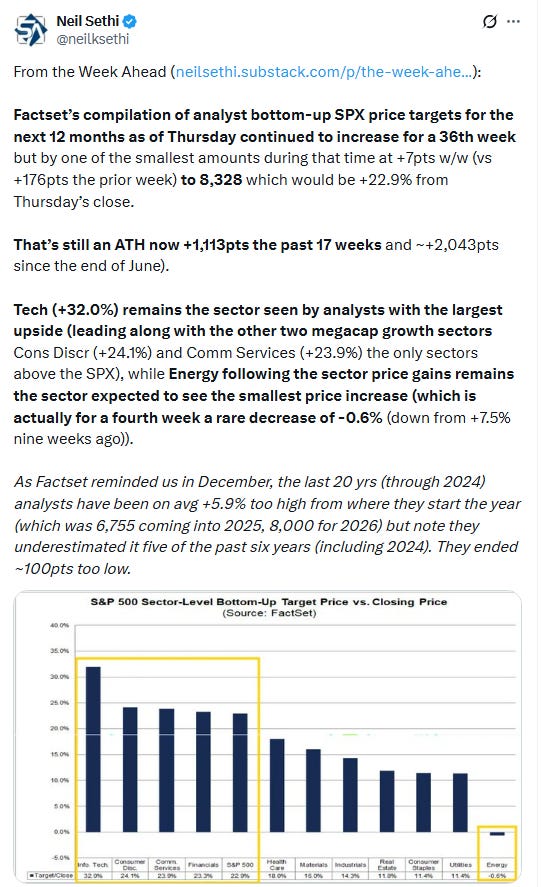

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

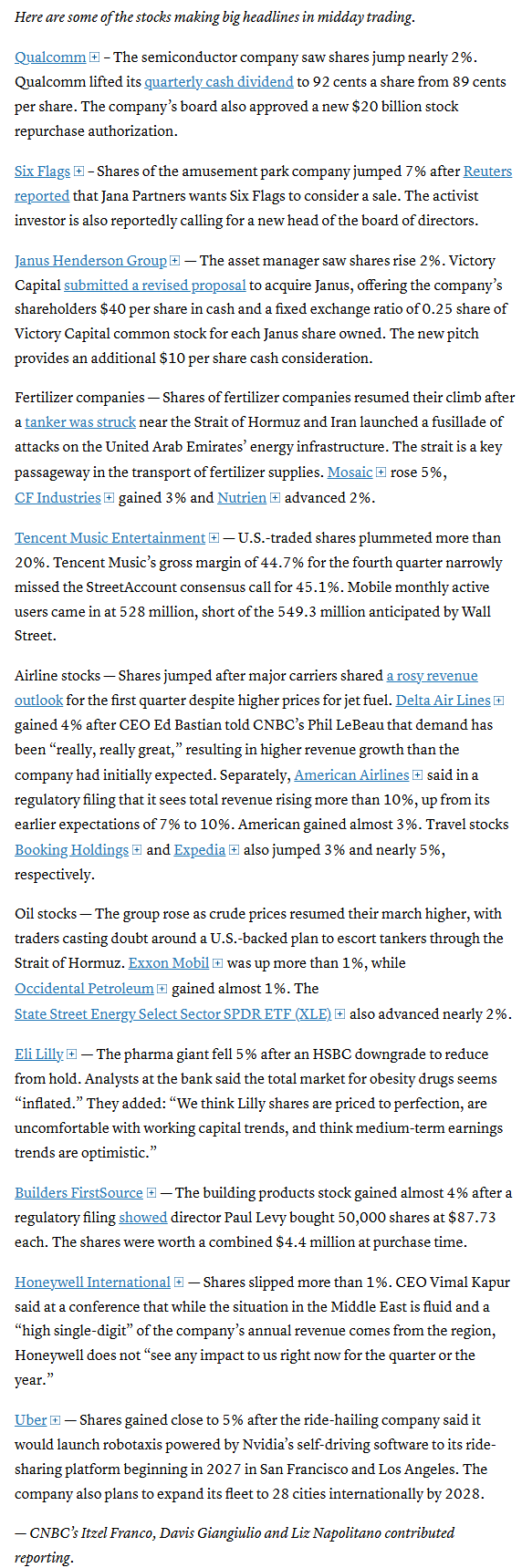

Despite the rise in oil prices, the S&P 500′s consumer discretionary group was notably up 1% on the day, led by gains in Expedia Group and Booking Holdings. Strong revenue guidance from airlines Delta and American boosted those names. The sector is down more than 2% this month, however.

Corporate news from BBG:

Nvidia Corp. Chief Executive Officer Jensen Huang said the company is firing up manufacturing of H200 AI accelerators for customers in China.

Qualcomm Inc. plans to buy back another $20 billion worth of shares and raise its quarterly cash dividend.

Boeing Co. signaled that several performance issues will weigh on its first-quarter results, from fewer-than-planned deliveries of its widebody aircraft and wiring defects on the 737 Max to the cost of turning around a key supplier.

Eli Lilly & Co. fell after HSBC turned bearish on the stock, saying investor expectations for weight-loss drugs are over inflated.

Mid-day movers from CNBC:

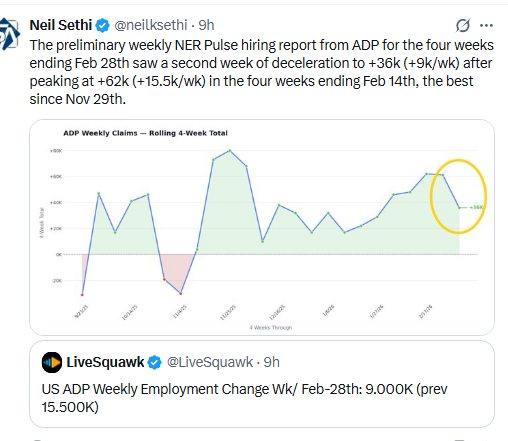

In US economic data:

Substack articles.

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X