Markets Update - 3/2/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with lots of charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!),

Link to posts - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog. Also please note that I do often add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

Finally, if you see an error (a chart or text wasn’t updated, etc.), PLEASE put a note in the comments section so I can fix it.

US equity indices opened trading Monday solidly lower as military strikes intensified across the Middle East, shipping was disrupted through the Persian Gulf, and oil saw its biggest surge in four years (it would pare some of those gains as the day progressed) stoking inflation concerns that could weigh on the global economy. In Europe, liquefied natural gas surged 52% after Qatar halted output at the world’s biggest export plant, and gasoil (diesel) jumped more than following Russia’s invasion of Ukraine.

So early on it was energy and defense names seeing all the gains (and they would hold most of them throughout the session), while travel was hit hard including airlines, hotels, and reservation platforms. Those losses would also mostly stick. But there also were early losses in much of Tech, and some of those would reverse. Nvidia turned into an upside leader finishing +3% while Microsoft was up over 1%. That said, as I’ll go over at length in the subscriber section, only four sectors were up on the day: energy, industrials, tech and real estate.

Also pressuring stocks was a jump in Treasury yields which rebounded on the aforementioned inflation concerns that were accentuated by a jump in input prices in a manufacturing survey (link to my Substack post) and a drop in Fed rate cut bets (covered in the subscriber section).

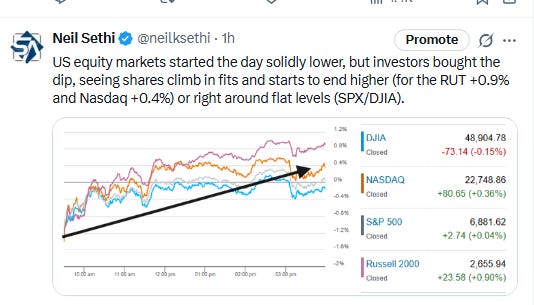

Investors though bought the dip, which saw equity indices climb in fits and starts to end near the highs of the day making it into positive territory for the Russell 2000 +0.9% and Nasdaq +0.4% to right around flat levels for the SPX and DJIA.

Elsewhere, as noted bond yields were higher, and the dollar rose to the highest since Jan. Crude as also noted jumped, and gold, natgas and bitcoin also saw gains, while copper fell back (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was UNCH, the equal weighted S&P 500 index (SPXEW) -0.2%, Nasdaq Composite +0.4% (and the top 100 Nasdaq stocks (NDX) +0.1%), the SOXX semiconductor index +0.5%, and the Russell 2000 (RUT) +0.9%.

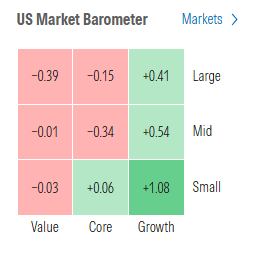

Morningstar style box mostly red Fri with just larger value names escaping.

Market commentary:

“The endgame remains highly uncertain, ranging from a relatively swift political exit to a broader regional spillover,” said Mathieu Racheter, head of equity strategy at Julius Baer. “In such a fog of war, markets tend to trade probabilities rather than shifting facts.”

“It is still very unclear what the duration of the conflict will be and more importantly, how the energy market reacts,” said Andrea Gabellone, head of global equities at KBC Securities. “One positive for the US is that the market has corrected since January, so we are not in overbought territory. It’s fair to say havens should continue to outperform.”

“Geopolitical events have taken place every couple of years, and U.S. investors have not really been rewarded for panicking,” said Chris Maxey, chief market strategist at Wealthspire Advisors. The buy-the-dip mentality among investors has been pervasive across the entire market, and it became “particularly true” during geopolitical events, since those moments of panic and selloff would ultimately recover and recuperate, Maxey told MarketWatch in a phone interview on Monday.

While Baird’s Ross Mayfield believes that a lot can still change with the conflict, he thinks the market is clawing back earlier losses because “there hasn’t been escalation from here.”

“If Iran were going to take the nuclear option of closing the Strait or really trying to do damage to energy infrastructure, we’d have a better sense that that was going to be their path by now,” the investment strategist said.

“Futures markets overreacted to the Iranian conflict, creating an opportunity to buy the S&P 500 as it neared its 2026 lows,” said Jeff Kilburg, CEO of KKM Financial, who posted Sunday night that the market would turn green before the close Monday. “We remain in a bull market despite escalating geopolitical tensions.”

“In the end, the Iran military action should remove major uncertainty in the world, and the stock market is expected to have a relief rally as new, pro-Western leadership in Iran emerges and crude oil exports resume,” said veteran strategist Louis Navellier.

The current geopolitical escalation should ultimately be a buying opportunity in stocks as fundamentals remain positive, according to JPMorgan Chase & Co. strategists led by Mislav Matejka.

“We believe the market has already been pricing in the possibility of a conflict for a month, which may limit the size of a further move and may cause a quicker rebound when the market sees a likely path to resolution,” said Ryan Detrick at Carson Group.

RBC strategist Lori Calvasina though cautioned against paying too much attention to historical studies that recommend buying the dip on bad geopolitical news. While bulls are “technically correct,” she cautioned that “it is very difficult to look at geopolitical events in isolation when it comes to the stock market. What’s happening with geopolitics is usually a piece of a larger puzzle,” Calvasina said.

“The tail risk of a sustained conflict is higher than in 2024 or 2025, though we don’t see this war escalating to a point where it drastically changes the US outlook,” said Barclays’ Ajay Rajadhyaksha in a note. But he said early this week “is too early to buy any dip, especially with investors used to a pattern of quick de-escalation.”

“Broader uncertainty suppresses investor sentiment, which can broadly weigh on risk-assets globally,” said Adam Hetts, global head of multi-asset at Janus Henderson. “In a prolonged period of uncertainty, increases in oil prices could generate a global inflationary scare.”

“All told, we presume a shorter-term impact, but can’t rule out a more protracted friction to equities,” said Citi equity strategists in a note to clients about the Middle East conflict. “We also need to bucket this new volatility event alongside a growing list of concerns. Namely, the AI spending boom seems poised to persist, but the productivity promise is quickly facing off against AI-triggered business-model disruption.”

Jefferies global equity strategist Christopher Wood was straightforward on his assessment of the impact of the war against Iran on the stock market.

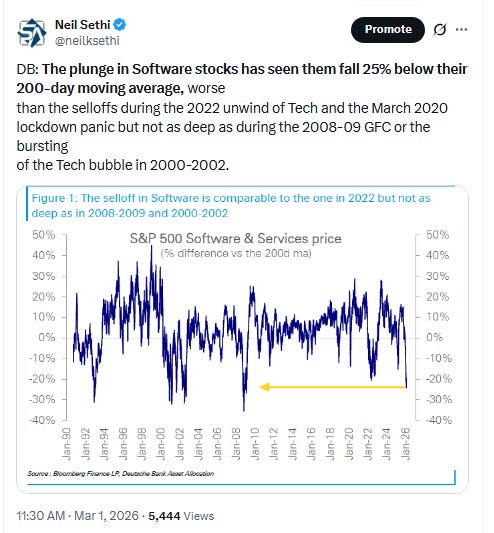

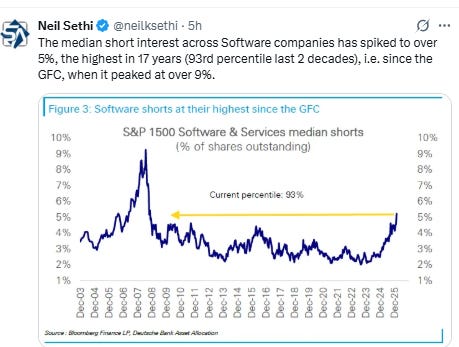

“The attack on Iran is no reason to sell stocks, in our view,” he says. But that doesn’t mean he’s a bull. “We see the questioning of the returns on AI capex, and the related disruption of the U.S. software sector, and the resulting collateral damage for private equity and price credit, as better reasons to be bearish.”

“In times like this my usual instinct is to fade the initial reaction to geopolitical developments, but today at least you could argue that the market in aggregate has been quite restrained...perhaps risking further flare-ups a bit further down the line.” — Cameron Crise, macro strategist.

“The tail risk of a sustained conflict is higher than in 2024 or 2025, though we don’t see this war escalating to a point where it drastically changes the US outlook,” said Barclays’ Ajay Rajadhyaksha in a note. But he said early this week “is too early to buy any dip, especially with investors used to a pattern of quick de-escalation.”

“Markets were well-positioned for risk aversion, even if the original drivers were not geopolitics,” Geoff Yu, senior macro strategist at BNY said. “We stress that the situation remains volatile. A ‘day-by-day’ approach will probably take precedence for now.”

“Broader uncertainty suppresses investor sentiment, which can broadly weigh on risk-assets globally,” said Adam Hetts, global head of multi-asset at Janus Henderson. “In a prolonged period of uncertainty, increases in oil prices could generate a global inflationary scare.”

For now, the global economy appears capable of absorbing a moderate, temporary rise in energy prices, but fragilities remain, according to Seema Shah at Principal Asset Management. “A sustained rise in oil prices would place renewed pressure on consumers while potentially delaying anticipated rate cuts,” she said.

Prashant Bhayani, chief investment officer for Asia at BNP Paribas Wealth Management, said the main questions traders are looking out for are how long the disruption lasts, developments in the Strait of Hormuz, any impact on oil infrastructure and whether Iran and the US can reach a negotiated settlement.

“Most geopolitical events have limited long-term impact on asset markets,” Bhayani said. “There is already a premium in oil of circa $7-$10 before today’s trading. Only in an extended conflict, with oil prices over $100, would it materially impact the global economy.”

Uncertainty about oil prices may play a big role in determining broader market sentiment, according to Chris Larkin at E*Trade from Morgan Stanley.

“There are more questions than answers right now, but a stabilizing energy picture could have a positive ripple effect, while concerns about a longer-term disruption could have the opposite,” he said.

“A long bottleneck there would present meaningful upside to oil prices as they sit right now,” said Ross Mayfield, Baird investment strategist. “A two-week shock to oil prices is not going to have a major impact on the U.S. consumer or how the Fed is thinking about interest rates, but a multi-month step-up in level would have an impact.”

“All told, we presume a shorter-term impact, but can’t rule out a more protracted friction to equities,” said Citi equity strategists in a note to clients about the Middle East conflict. “We also need to bucket this new volatility event alongside a growing list of concerns. Namely, the AI spending boom seems poised to persist, but the productivity promise is quickly facing off against AI-triggered business-model disruption.”

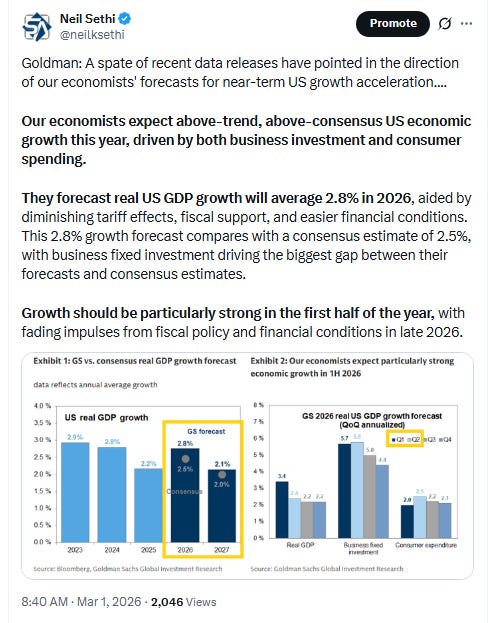

U.S. stock-market volatility is rising after the missile attacks on Iran over the weekend, but the main influence on equities remains investors’ sentiment around artificial intelligence, barring further escalation of the conflict in the Middle East, according to Tom Essaye, founder and president of Sevens Report Research. “At its current state, the Iran conflict is not a bearish gamechanger,” despite any short-term drop for stocks, Essaye said in a note Monday. “The main influence on stocks remains AI anxiety and barring any further escalation in the Iran conflict, that will remain the case.” While oil prices have risen, Essaye said the attacks from the U.S. and Israel on Iran probably won’t lead to a dramatic reduction in global oil supplies. Iran is “a marginal producer on the global stage and OPEC announced a larger than expected production increase over the weekend.” But if the U.S. and Israel invaded Iran with “boots on the ground,” that would probably “create sustainable upward pressure on oil prices, which would be negative for markets,” according to Essaye. For now, “the medium-term direction of this market” is still being determined by sentiment around AI as well as economic growth and expectations around the Federal Reserve’s interest-rate-cutting cycle, according to Essaye.

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

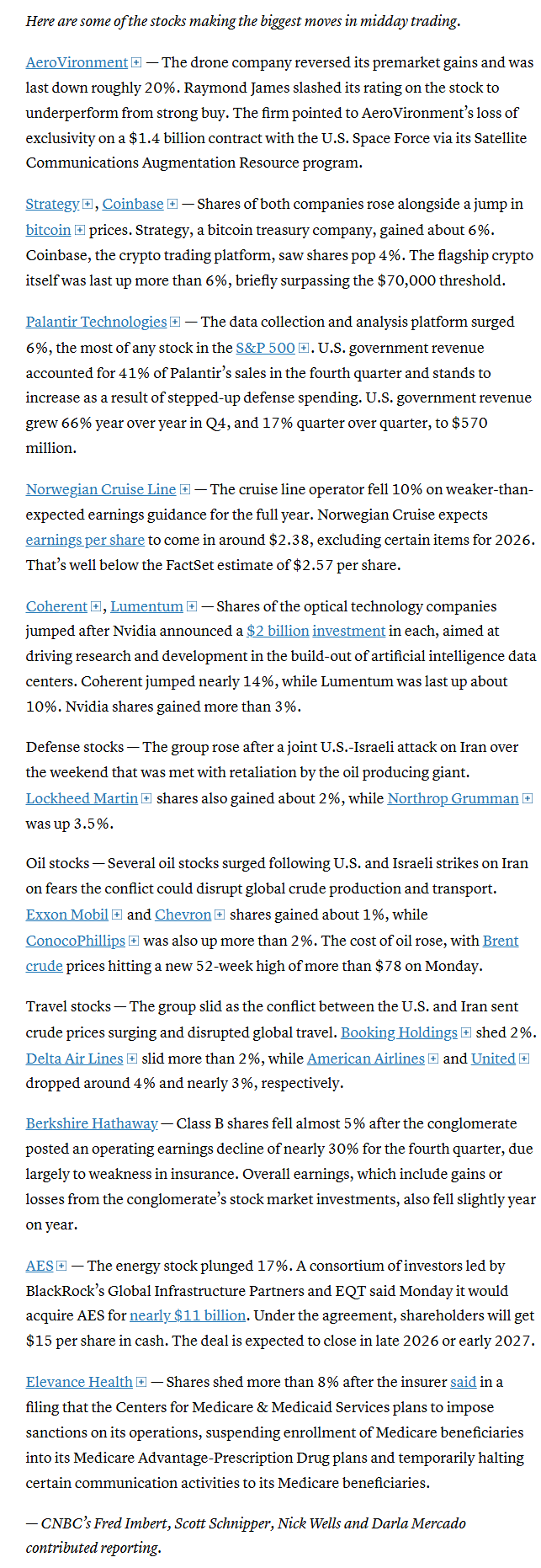

On top of tech, a rise in defense stocks helped the major averages recoup a chunk of their losses. Northrop Grumman advanced 6%, while Lockheed Martin climbed more than 3%. Energy shares including Exxon Mobil and Chevron saw gains as well.

Corporate news from BBG:

Anthropic PBC’s artificial intelligence chatbot Claude and related consumer-facing applications went down on Monday, with the startup saying it has been grappling with “unprecedented demand” for its services over the past week.

Nvidia Corp. agreed to invest $4 billion in two companies that develop data center optics that are essential for artificial intelligence.

BlackRock Inc.’s Global Infrastructure Partners LP and EQT AB agreed to buy AES Corp. for about $10.7 billion in cash as the market heats up for power plant developers that can provide electricity for AI data centers.

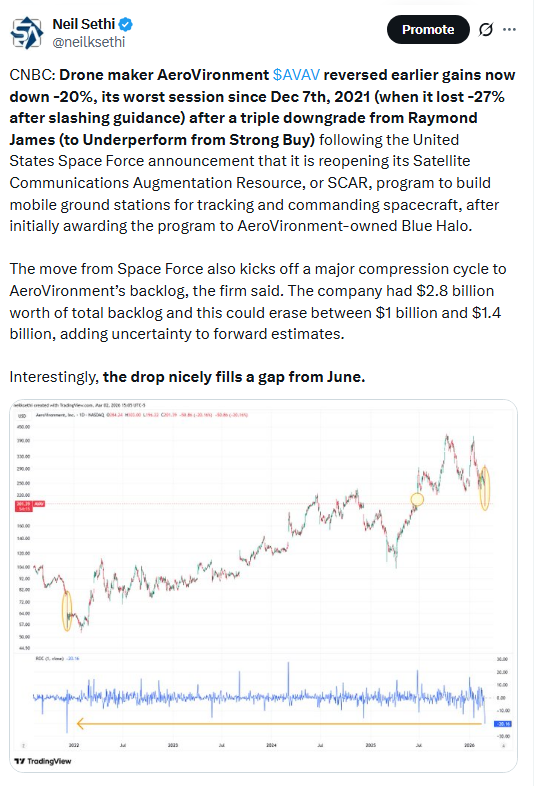

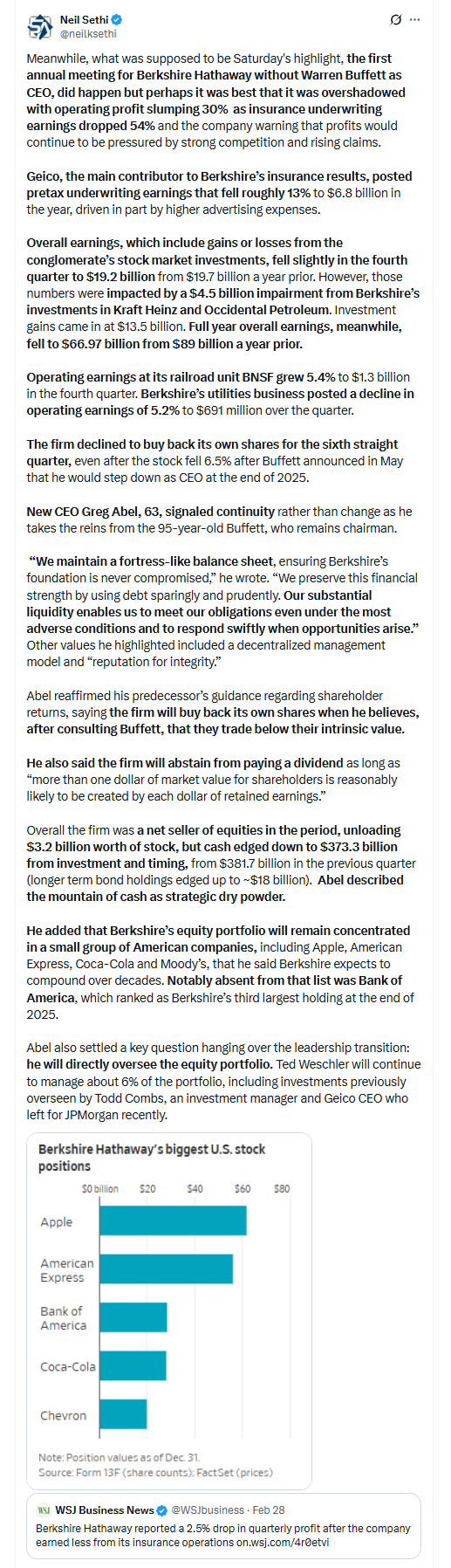

Mid-day movers from CNBC:

In US economic data:

Substack articles.

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X