Markets Update - 3/23/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!), here’s the button:

Link to posts on X - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog.

Also, if you see an error (a chart or text wasn’t updated, etc.), always appreciate a note in the comments section or email so I can fix it.

In that regard, I do make mistakes sometimes, and usually I catch them at some point and correct them, and/or I sometimes add new material, so it’s always safest to read from the website where it will have any updates.

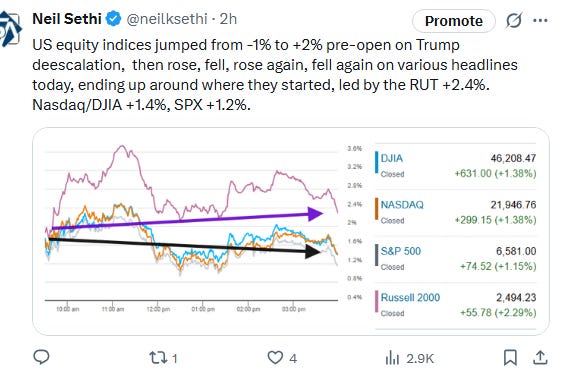

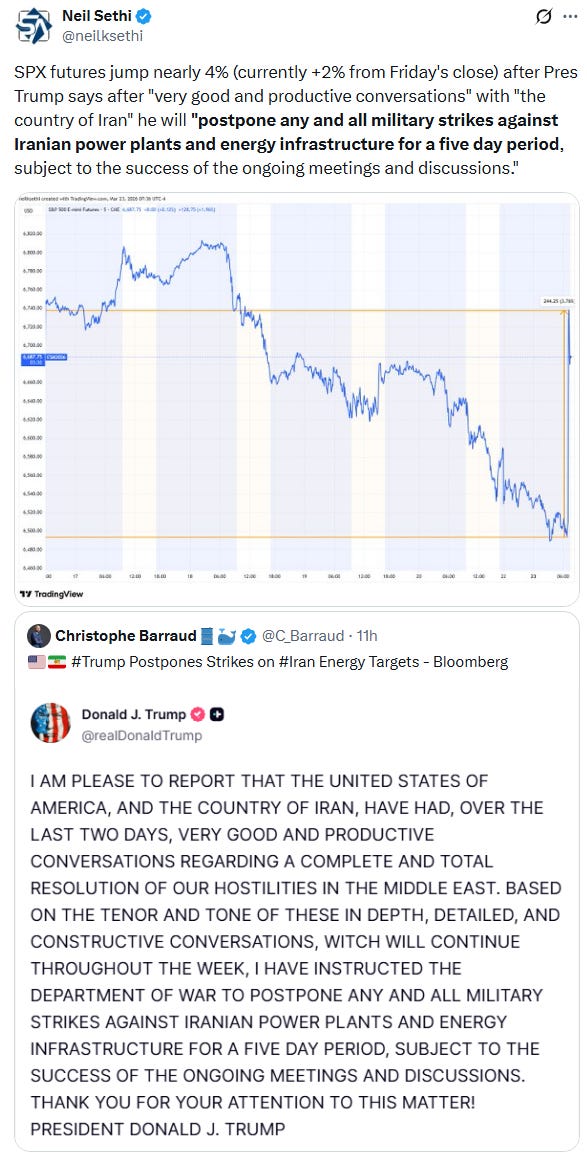

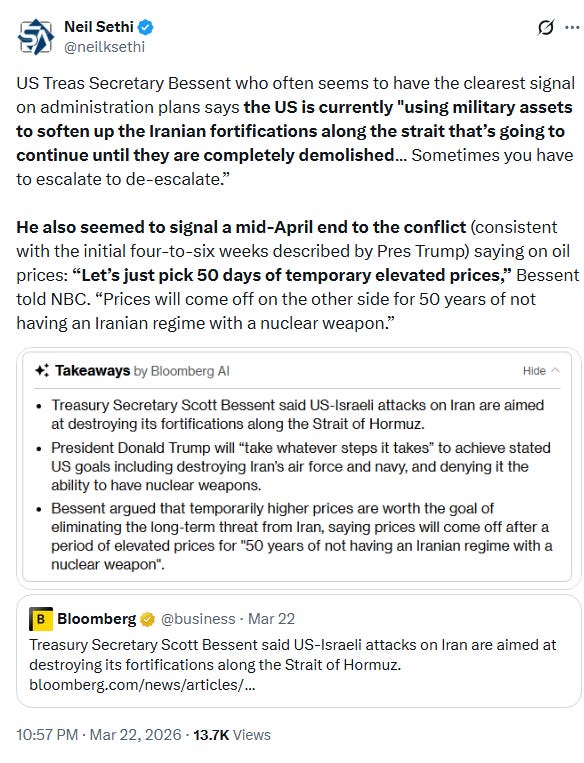

US equity indices opened trading for the week having reversed earlier losses that came after President Trump’s Friday declaration of a 48-hour window for Iran to reopen the Strait of Hormuz or face destruction of its energy facilities following a social media post Monday morning from the President (see below) that after “very good and productive conversations” with “the country of Iran” he will “postpone any and all military strikes against Iranian power plants and energy infrastructure for a five day period, subject to the success of the ongoing meetings and discussions.”

The reaction to the post was sharp with equities spiking nearly 4% before settling back. They would vacillate throughout the session on various headlines (Iran saying no talks were happening, Trump saying “I don’t know what they’re talking about,” Trump saying that both sides wanted to “make a deal”, that the two countries were “going to get together today by, probably, phone,” and suggesting the US and Iran could jointly control the Strait of Hormuz, adding the key waterway could be open very soon “if it works,” etc.) with indices ending not far from where they started led by the small cap Russell 2000 +2.4%. The Nasdaq and DJIA were +1.4%, SPX +1.2%.

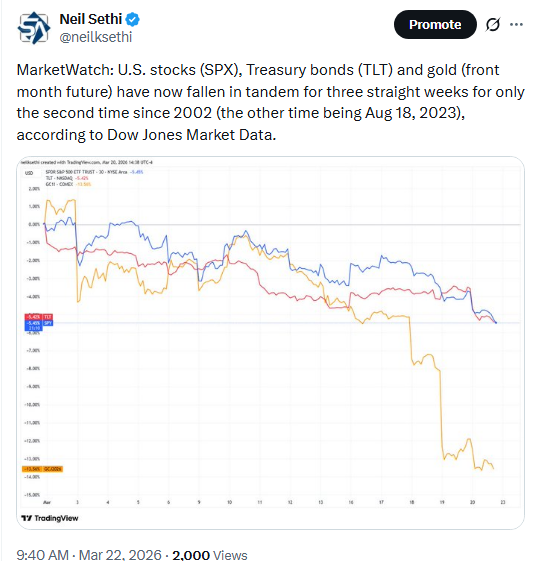

Elsewhere, bond yields eased off their highs to finish slightly lower, as did the dollar, while oil saw larger declines with Brent ending -14% and US WTI nearly -10%. Gold and US natural gas would also finish lower, while copper and bitcoin would end higher (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was +1.2%, the equal weighted S&P 500 index (SPXEW) +1.1%, Nasdaq Composite +1.4% (and the top 100 Nasdaq stocks (NDX) +1.2%), the SOXX semiconductor index +1.3%, and the Russell 2000 (RUT) +2.3%.

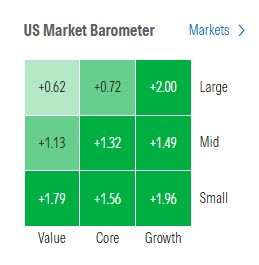

Morningstar style box shows all styles in the green with growth returning to outperformance.

Market commentary:

“The tone is more upbeat now. But it would be naïve to assume the situation will now be resolved to the satisfaction of all the main combatants and victims of hostilities. Further, negative effects from higher energy prices are now baked in. Stock dynamics will continue to remain negative while an abundance of potential pitfalls remain ahead.” — Simon White, macro strategist

“This feels very similar to Trump’s tariff playbook — delay, create optionality, and ultimately step back,” said Manish Singh, chief investment officer at Crossbridge Capital. “It suggests Trump is looking for an off-ramp, and that’s positive for risk assets.”

The positive reaction in stocks to a delay on strikes was not surprising given how “oversold” the market had been, according to Jay Woods at Freedom Capital Markets.

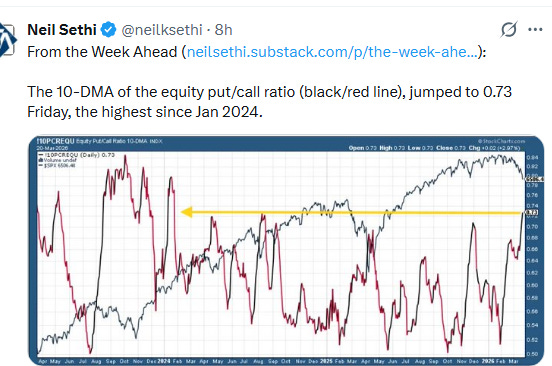

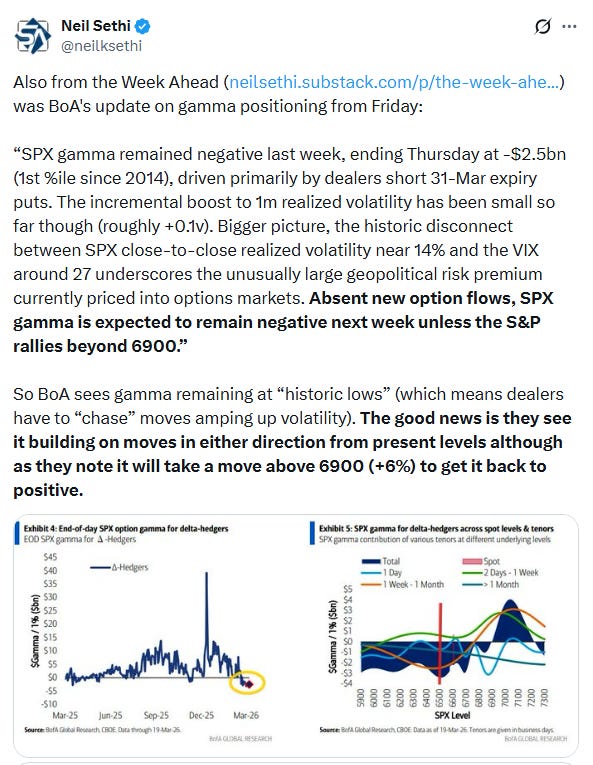

Entering Monday, more than 50% of stocks in the S&P 500 were “oversold” versus just 5.4% that were “overbought”, according to Bespoke Investment Group. The last time we saw readings this extreme was in April during the tariff tantrum.

“The conditions for a rally are very high — if geopolitical tensions ease — considering one of the largest short positions on US stocks that we’ve ever seen,” said Citadel Securities’ Scott Rubner.

“Although this change in rhetoric is an encouraging development, we think the clearest indication of meaningful de-escalation will be whether crude oil flows through the Strait of Hormuz are able to recover,” said Brock Weimer at Edward Jones.

“It’s important not to get too sucked in by the rally,” said Emma Moriarty, portfolio manager at CG Asset Management. “Markets have been pulled around in both directions off the back of headlines and there has to be a continued risk that a ceasefire does not come to pass.”

“The market has been desperate for any good news, and this appears to be, at least on the surface, the best news we can expect,” said Art Hogan, chief market strategist at B. Riley Wealth Management. “If we were able to see any downward pressure on energy prices, the market is like a coiled spring looking for a reason to move higher.”

U.S. stocks were surging Monday on a “glimmer” of good news regarding the Iran conflict, but the positive tone will need to last throughout the week, said Ryan Detrick, chief market strategist at Carson Group. “Of course, there is a long way to go,” Detrick said in a phone interview. President Trump said there has been progress in talks with Iran about potentially ending the conflict, but Iranian reports have denied any talks and ship traffic through the Strait of Hormuz remains effectively stalled. “This is nice to see some positive developments, but this has to stick,” Detrick said.

“The market woke up to some potentially good news out of the Middle East,” Larkin, a managing director, said. “But follow-through on any relief rally will likely require tangible follow-through on the geopolitical front.”

“We’re still living in a headline-driven market,” he said. “With a light economic calendar this week, the focus will remain oil prices and politics.”

The U.S. stock market isn’t necessarily poised for accelerated gains despite the S&P 500 bouncing sharply on Monday after four straight weeks of losses, according to Frank Cappelleri, founder of research firm CappThesis.

“We need to see not only buying but upside follow through,” Cappelleri said in a phone interview Monday. “That has been the missing link” since the S&P 500 first touched 7,000 on an intraday basis in January, he said, with the index posting “a series of lower highs” as “every intermittent rally has been cut short.”

“It is impossible to tell whether this signals genuine progress towards an off-ramp for the war, or Trump ‘zig-zagging’ to buy time and keep oil from breaking out towards $150,” said Krishna Guha at Evercore. “It should though offer at least a brief respite on rates – possibly more.” While it is not hard to see a no-cut scenario for the Fed in 2026, Guha continues to see cuts far more likely than a hike. “If we can find a durable off-ramp, bond market attention could return to medium term AI-led disinflation,” he said.

“The market’s move today is more about the direction that they can tell the administration wants to go, but I would view getting something done this week that just brings things back to normal with a heavy dose of skepticism, given all the various complications,” Ross Mayfield, Baird investment strategist, told CNBC. “What does Israel want? What does Iran want? What do our allies in the Gulf want? Has there been structural damage to LNG and crude oil exporting and refining facilities that — even if we end this thing this week — structurally alter the price of oil and put more of a premium on it?” he said.

“I think the war – just as Covid did – reminded us the importance of supplies,” Boockvar said in an interview with CNBC. “This is reminding us the importance of the supply of vital commodities. You’re going to see global hoarding in a variety of different things.”

“Oil is not going back to $65 where it was prior to this,” he continued. “At least with natural gas, Qatar said it could take three to five years for them to ramp up again their LNG facility, so a lot of things are going to stay elevated.” As a result, Boockvar said he would be buy the dip in oil and natural gas as well as agriculture, seeing that he doesn’t anticipate corn and fertilizer prices dropping “much more.” He also continues to view inflation as a problem. “I think central banks are sort of hand-tied here in the midst of that, but at least for now, we’re going to get a bit of a relief rally,” the investment head added.

Andrew Bishop, global head of policy research at the London-headquartered advisory firm, wrote in a note on Sunday that Trump’s 48-hour warning of obliterating Iran’s power plants if the Strait of Hormuz was not reopened could have been “to claim credit for forcing Tehran to stand down.” Bishop added that the firm is optimistic that the five-day pause in strikes announced by the U.S. on Iranian energy infrastructure could turn into “a more sustainable ceasefire.”

The market wants to see confirmation from Iran and Israel that talks are taking place to work toward ending the conflict, and that it’s not just the U.S. claiming these discussions are happening, Anthony Saglimbene, chief market strategist at Ameriprise Financial, said in a phone interview Monday. “Markets will react positively if they see Iran and Israel indicate that discussions are taking place,” Saglimbene said. He added that investors will be watching for signs of an agreement shaping up that would involve the reopening of the Strait of Hormuz and assurances that “Iran isn’t going to attack Gulf-state infrastructure.”

The situation in Iran is looking less dangerous than it did earlier, and PNC’s Yung-Yu Ma agrees with the market that there’s a decent chance tensions won’t spiral into a major crisis. “The market’s positive reaction is warranted,” the chief investment officer at PNC Asset Management told CNBC. “There’s still uncertainty … but what looked like a high likelihood of military escalation and increased economic disruption is at least moderated. A near-term off ramp is a realistic possibility. At a minimum, there seems to be recognition that the threatened step of widespread infrastructure damage across Iran and possibly all of the Middle East could have far-reaching economic effects.”

Investors got the positive sign they were hoping for on Monday with President Donald Trump’s announcement of talks between the U.S. and Iran, said Tim Pagliara, investing chief at CapWealth. “For several weeks, the stock market had been looking for any signs of a de-escalation with the Iran conflict,” Pagliara said. “It finally saw that on Monday, sparking a risk-on trade.” Pagliara said the market may be able to rebound before an end to the U.S.-Iran war, now in its fourth week, is officially declared. “The Iran conflict and oil price reaction are the main drivers of stock prices right now and will likely continue to be for some time,” he said. “While we expect continued market volatility, we believe the stock market can recover well before the conflict in Iran ends.”

“Equity markets finally found an off-ramp to the dramatic uncertainty and significantly oversold conditions due to the Iranian conflict,” Jeff Kilburg, founder and CEO of KKM Financial and manager of the Essential 40 Stock ETF (ESN), wrote after President Donald Trump’s latest announcement on Iran. “If this proves to be a foundation for peace in the Middle East, equities could get back to all-time highs.”

Michael Brown, a senior research strategist at Pepperstone in the U.K., had some initial thoughts on President Donald Trump’s statement that the U.S. and Iran were engaged in “very good” talks:

“This is clearly a positive development. The two sides are in discussions, and this is the first material sign of de-escalation that we have seen since conflict broke out at the end of February.”

“The war is not yet over. While positive, it is only strikes on energy infrastructure that have been ruled out at this stage, presumably meaning that kinetic action will continue elsewhere, at least for the time being.”

“There are caveats. Trump notes in his post that the five day pause will be contingent on the success of ‘ongoing meetings and discussions’, meaning that things could escalate once more, if talks were to fall apart.”

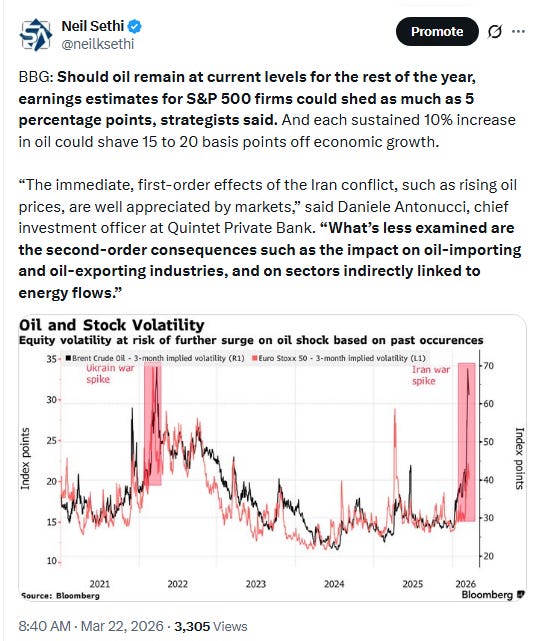

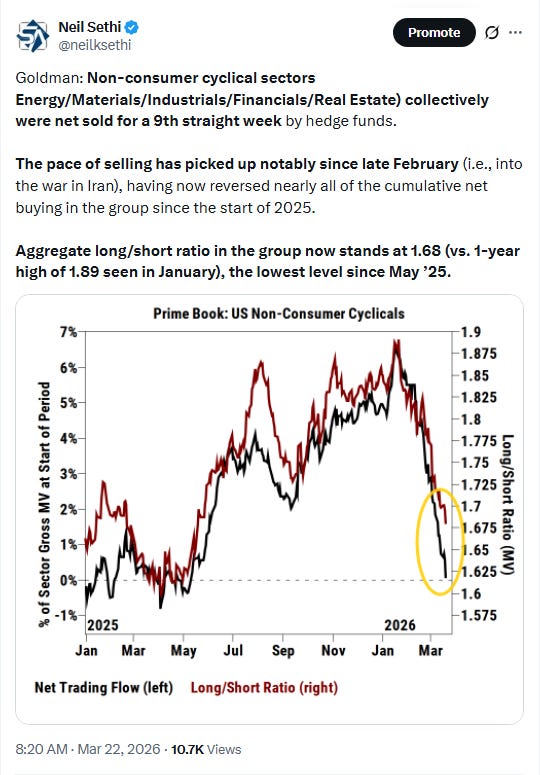

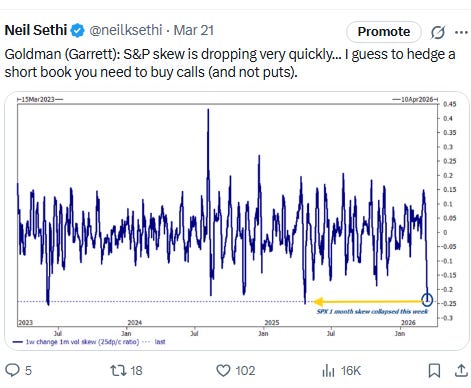

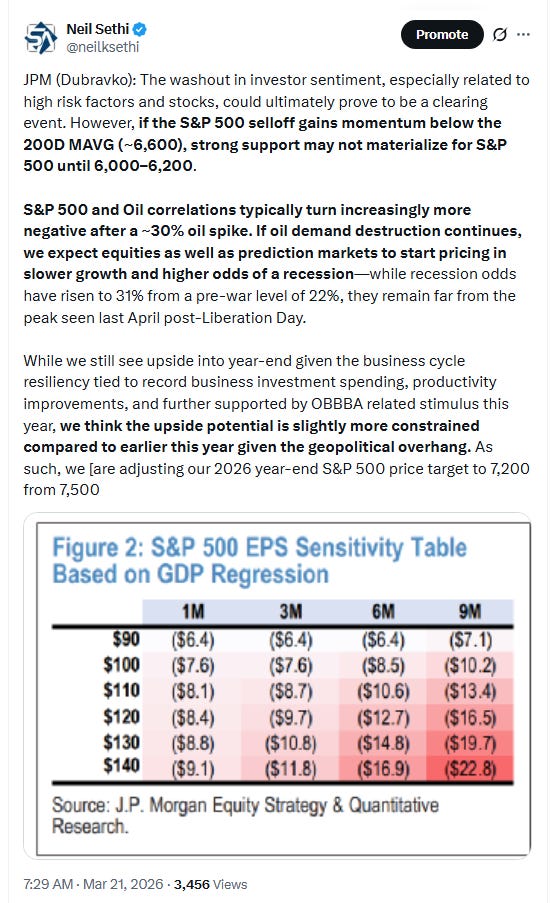

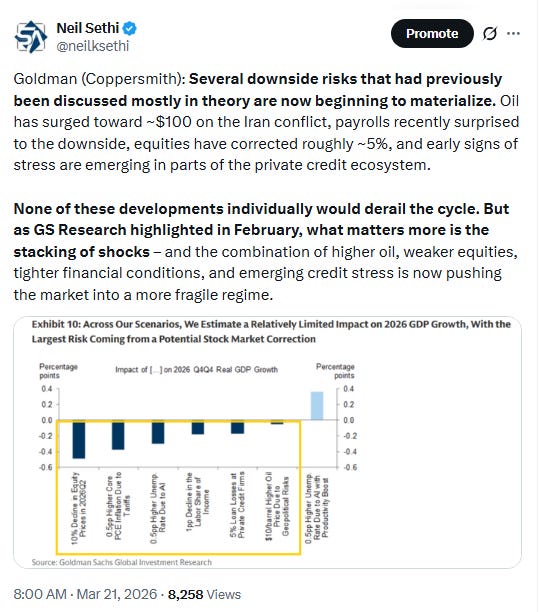

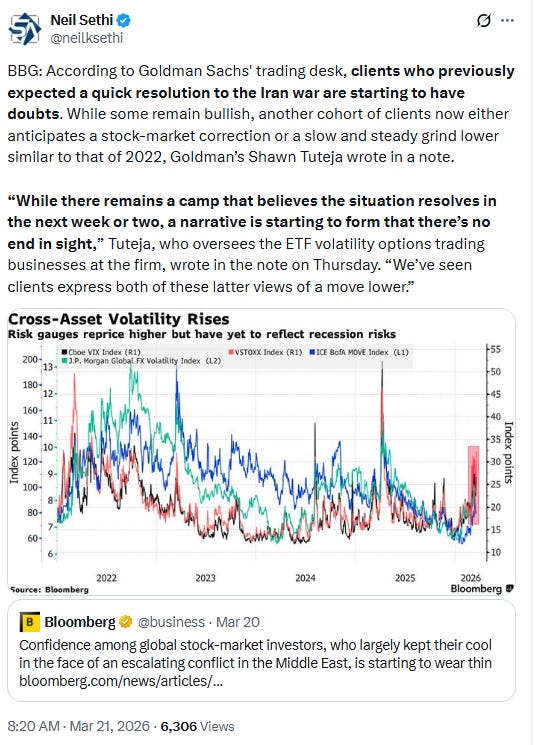

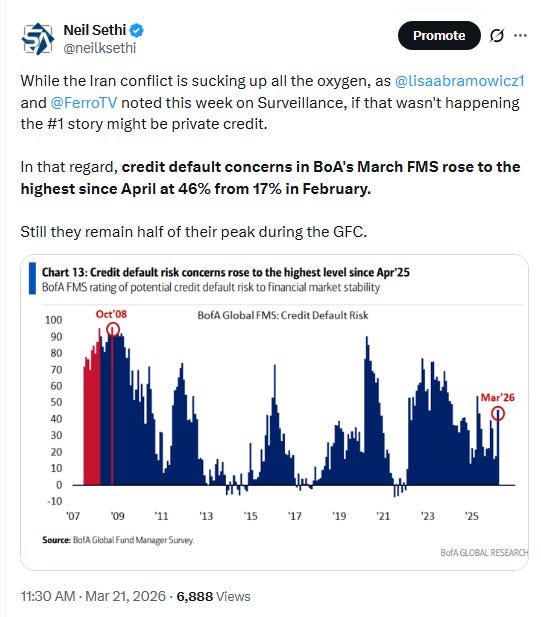

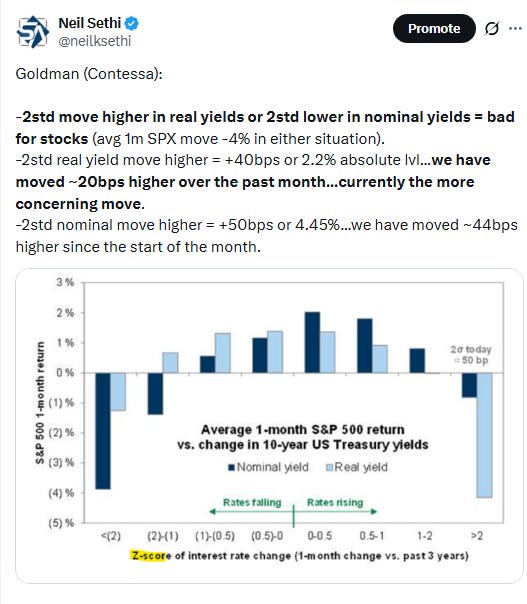

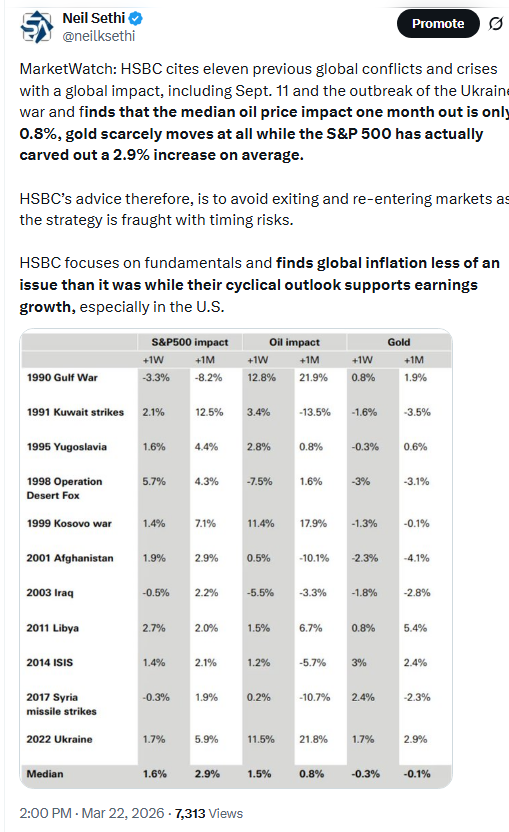

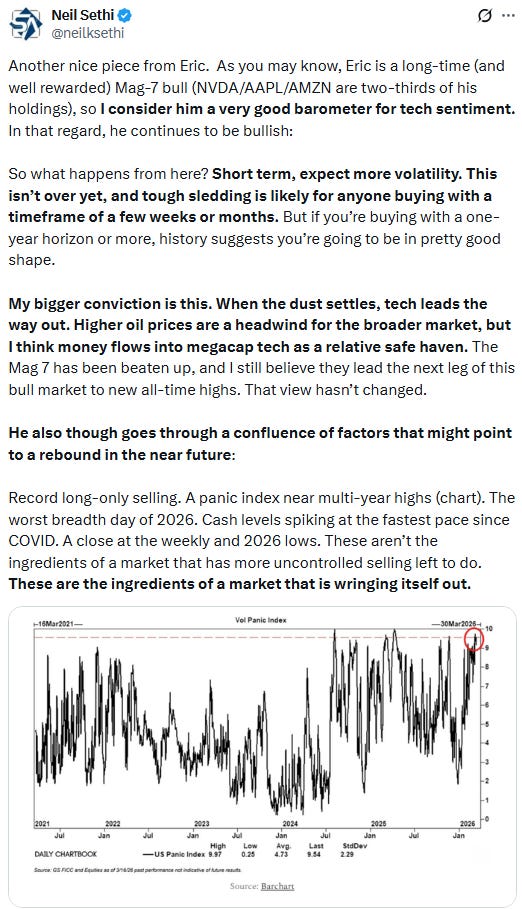

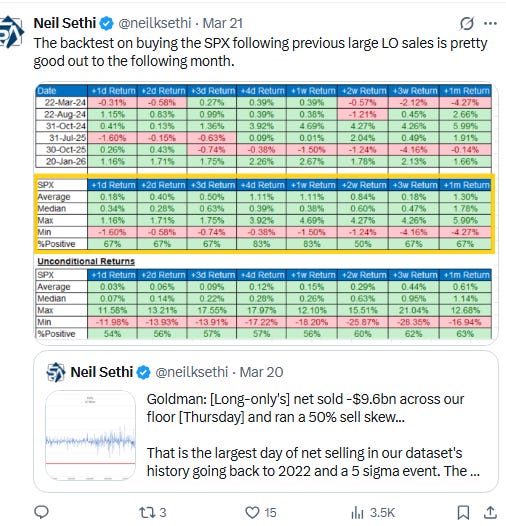

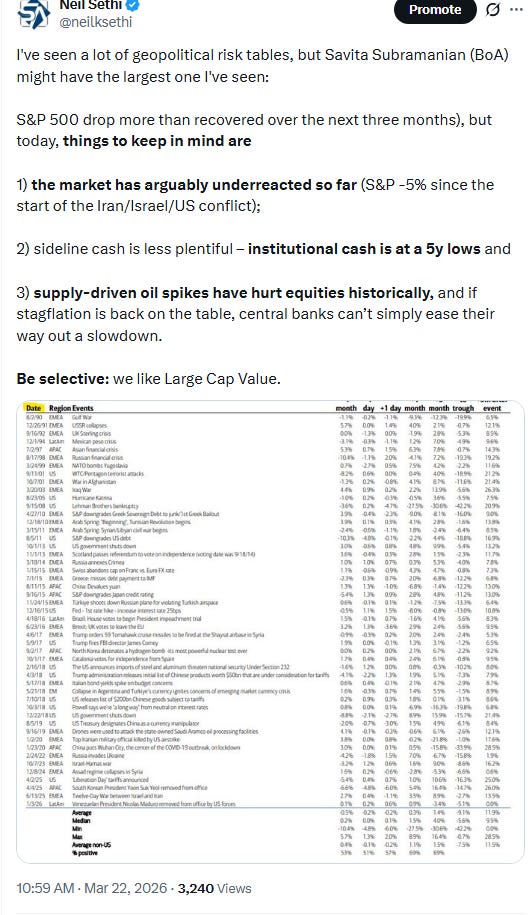

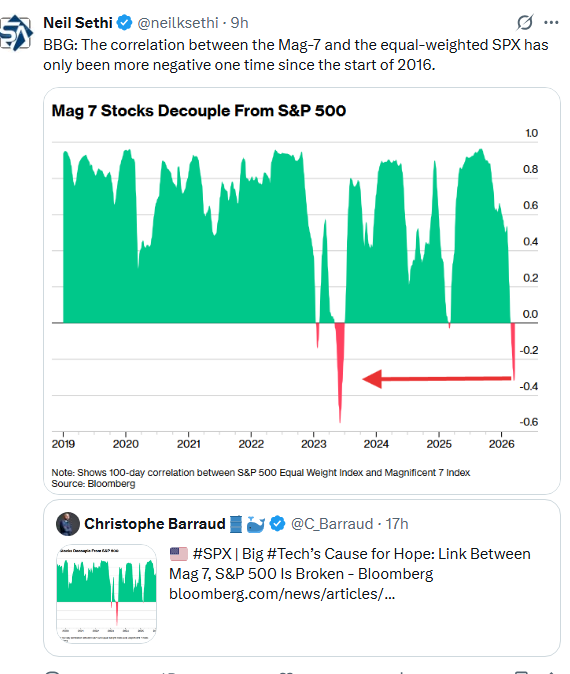

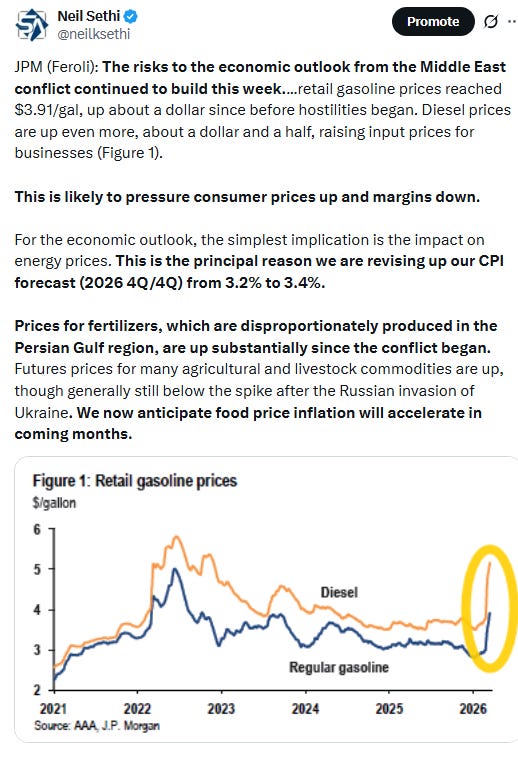

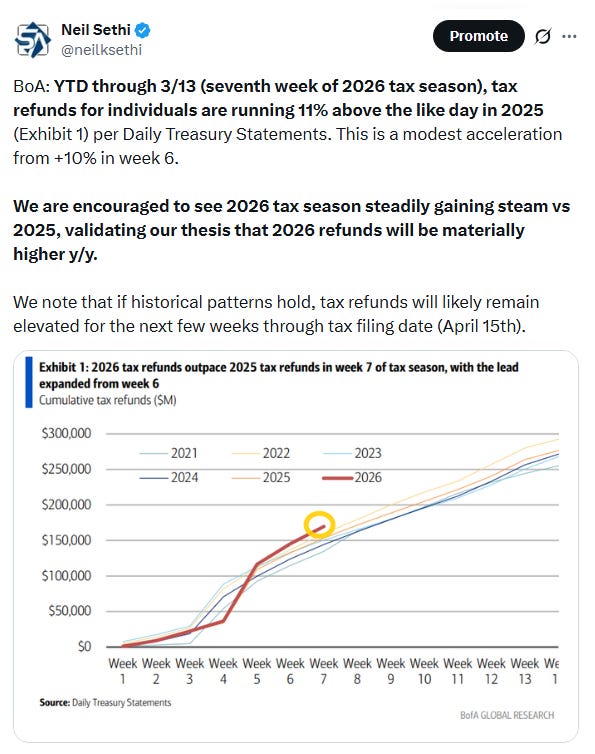

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

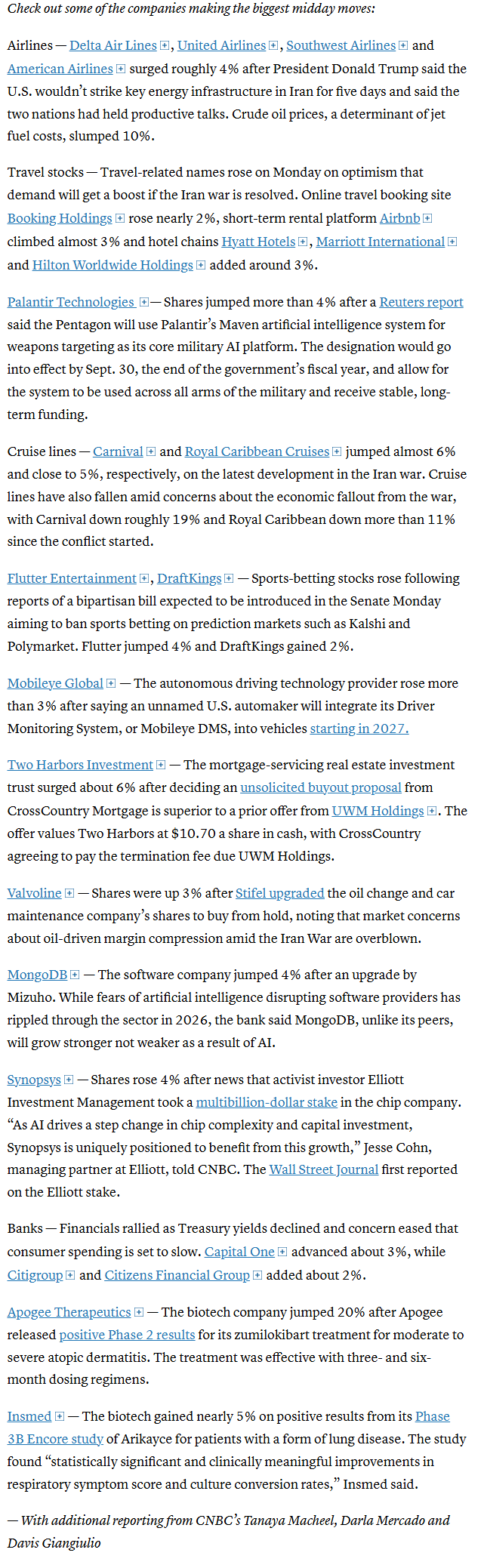

In individual stock action:

It was a broad rebound during the session, with cyclical shares such as banks and industrials surging as well as technology shares. JPMorgan Chase climbed more than 1%, while Morgan Stanley was nearly 2% higher. Caterpillar added 3%, while Deere climbed more than 1%. Nvidia and Apple were each higher by more than 1%. Airline stocks Delta Air Lines and United Airlines were up more than 2% and 4%, respectively, as oil prices slid.

Corporate news from BBG:

Mid-day movers from CNBC:

Apple Inc. announced plans to hold its annual Worldwide Developers Conference from June 8 to June 12, when the company is poised to unveil a make-or-break collection of AI features.

Banks led by JPMorgan Chase & Co. have kicked off an $8 billion junk-bond sale to fund the record leveraged buyout of Electronic Arts Inc., again shifting around the debt mix for the deal to navigate fluctuating risk appetite.

DraftKings Inc. and Flutter Entertainment Plc rose as the Wall Street Journal reported US senators are set to introduce bipartisan legislation to ban sports bets on prediction markets.

Activist investor Elliott Investment Management has made a multibillion-dollar investment in Synopsys Inc. and plans to push for changes, according to people familiar with the matter who asked not to be identified because the discussions are private.

In US economic data:

Substack articles - note the Construction Spending report was NOT emailed.

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X