Markets Update - 3/24/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!), here’s the button:

Link to posts on X - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog.

Also, if you see an error (a chart or text wasn’t updated, etc.), always appreciate a note in the comments section or email so I can fix it.

In that regard, I do make mistakes sometimes, and usually I catch them at some point and correct them, and/or I sometimes add new material, so it’s always safest to read from the website where it will have any updates.

US equity indices opened trading Tuesday lower as questions remained over how effective ongoing talks, confirmed by the Wall Street Journal, would be to end the Iran conflict as Israel and Iran continued to exchange strikes overnight. The WSJ report stated that there was doubt expressed privately by Arab mediators at the prospect of both sides quickly reaching an agreement, as they were still far apart.

In terms of attacks, Iran launched overnight missile and drone strikes on the Israeli cities of Eilat, Dimona and Tel Aviv, as well as US bases in the Middle East. Saudi Arabia said it intercepted a drone in its eastern region, and Kuwait said some power lines were put out of service after an Iranian attack. In Iran, the Fars news agency reported US-Israeli attacks that damaged a gas pressure-regulation plant and an administrative building in the central city of Isfahan. There was also a strike on a pipeline supplying gas to a power plant in southwestern Iran.

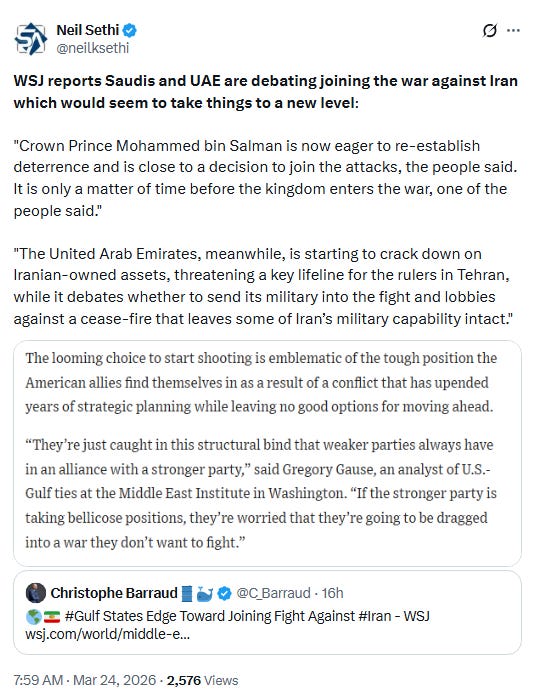

Meanwhile the WSJ also reported that US allies in the Persian Gulf may join the campaign against Tehran (more in the International Update portion of the morning update). Separately, the New York Times reported that Saudi leader bin Salman has told President Donald Trump during a series of conversations over the last week that the U.S. must continue its push to destroy Iran’s government. All of this saw oil prices, bond yields, and the dollar rebound from Monday’s losses, pressuring equities.

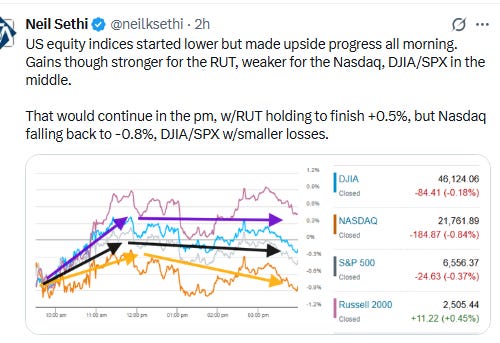

Despite that pressure, equities would rally most of the morning led by the small cap Russell 2000 (RUT) with the Nasdaq lagging on continued weakness in technology shares led by a renewed selloff in software and related equities. That would continue into the afternoon with the RUT holding its gains to finish modestly in the green +0.5% while the Nasdaq would lag finishing -0.8% lower. SPX and DJIA would also finish lower -0.4% and -0.2% respectively.

Late day President Trump said Iran had offered a lucrative “present” as a show of good faith in negotiations, noting it was related to Strait of Hormuz flows. Separately, Trump said the U.S. and Iran are “in negotiations right now” and suggested Tehran is eager to make a peace deal. “They’re talking to us, and they’re talking sense,” Trump said. Earlier Tuesday, Pakistani Prime Minister Shehbaz Sharif said in an X post that his country is willing to facilitate talks between the two countries. Trump shared a screenshot of Sharif’s post on his official Truth Social account Tuesday morning. Still, the Pentagon is also reportedly planning to deploy the 82nd Airborne Division to the Middle East, though the U.S. has not made a decision to put boots on the ground in Iran. Finally, as I write this, the New York Times is reporting that the US offered Iran a 15-point proposal for concluding the war which has equity futures higher and crude prices lower.

Elsewhere, bond yields moved higher ending near the highs of the year. The dollar also gained but remains further off its highs. Crude was up during the cash session but fell at 4.00pm ET after the above headlines. US natural gas saw a modest advance while gold, copper and bitcoin would end lower (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was -0.4%, the equal weighted S&P 500 index (SPXEW) +0.1%, Nasdaq Composite -0.8% (and the top 100 Nasdaq stocks (NDX) -0.8%), the SOXX semiconductor index +1.3%, and the Russell 2000 (RUT) +0.5%.

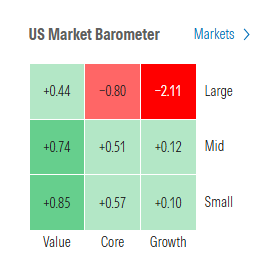

Morningstar style box shows how much large growth lagged the rest of the index.

Market commentary:

“We believe global economic risks are rising as basic materials and chemical inputs that support food production, electronics, manufacturing, and healthcare experience increasing supply chain disruptions due to the conflict in Iran,” writes Anthony Saglimbene, chief market strategist at Ameriprise. Still, he remains optimistic: “As most investors know, stocks have a long history of weathering unexpected shocks and dislocations.”

“Yes, markets can rebound if talks succeed but even in that case we’re expecting volatility to remain,” said Claudia Panseri, chief investment officer at UBS Wealth Management, who is “as defensive as possible” in Europe and cutting exposure to cyclical stocks like banks. “Oil reserves must be replenished, supply bottlenecks tackled, so things will not go back to where they were prior to the strikes. That means that there would still be an impact on growth and inflation.”

“It’s a very tricky situation,” said Arnaud Girod, head of cross-asset strategy at Kepler Cheuvreux. “If there’s a deal in five days then there’s a chance the market can bounce back and investors may be able to look through the crisis but if there’s not, a recession is a possibility. The range of outcomes is very large still, which explains the volatility.”

“It all comes down to the re-opening the Strait of Hormuz,” said Matt Maley at Miller Tabak. “So, if we hear that ‘good progress is being made’ in the negotiations at the end of this week, it won’t be enough, if the Strait remains very restricted.” Aside from the geopolitical risks, Maley also noted that the issues facing the private-credit market are not receding, so brushing these problems aside “is not a good idea.”

Monday’s optimism about the war in the Middle East ending without the US first making an attempt to secure and control the Strait of Hormuz, or without getting first more leverage in talks with Iran, still seems misplaced, according to Thierry Wizman at Macquarie Group. “The longer oil prices stay high, the longer central banks will feel obligated to sound as if they will tighten policy,” he said. Yet Wizman noted that hawkish policies that come in response to supply-side induced inflation have been proven to be the cause of much more financial stress than when monetary policy comes in response to an inflation that is demand-driven.

“If this proves to be a short-term disruption, as markets are currently pricing, then the baseline outlook still assumes moderate global growth,” said Tiffany Wilding and Andrew Balls at Pacific Investment Management Co. “However, a prolonged disruption would pose more significant challenges and increase global recession risks.”

“We still have a lot of wood to chop in terms of where oil prices end up shaking out; how those impact underlying economic conditions. So we think we’re okay for right now with this down 5% to 10% narrative, but we have to be on the lookout that the risks are still out there and are still pretty notable,” he said on CNBC’s “Closing Bell: Overtime” on Monday afternoon.

Markets remain firmly at the mercy of geopolitical headlines, and Trump’s constant social posts delivering mixed messages. The U.S. dollar, stock indices, gold and crude oil are all continuing to swing on every update tied to the Middle East conflict,” StoneX market analyst Fawad Razaqzada wrote in a note.

“Traders are hanging on any signals around whether ceasefire talks are even remotely on the table. Until there’s something concrete, it’s hard to see risk appetite improving in any meaningful way,” he added.

Oil prices resumed rising on Tuesday after falling the day before. Michael Kantrowitz, chief investment strategist at Piper Sandler, pointed to the commodity as the primary market driver in recent days. “We continue to see this as just an oil-driven, one-variable market,” he said on CNBC’s “Closing Bell: Overtime” Tuesday afternoon. “Oil and interest rates are driving the equity market. And for now, I think markets are priced appropriately for where conditions are, and we’ll continue to move and react as conditions evolve.”

He added: “I’m less concerned about the economy. I think the U.S. economy can certainly handle $90, $100 oil. I’m a little more concerned about interest rates and the fear of persistent inflation weighing on equity multiples.”

The U.S. consumer remains fairly healthy, according to the latest macroeconomic data, but Loop Capital is taking a “wait and see” approach as the Iran war continues. ”[W]e believe the ongoing conflict in Iran is casting a major pall, as we think a prolonged period of high oil prices will not only reduce purchasing power but will also dent consumer confidence,” analyst Anthony Chukumba wrote in a note Monday.

“While the war understandably has come to the forefront in terms of media and market attention, the underlying forces of AI [disruption] and the concerns stemming from that have not gone anywhere,” said Jordan Rizzuto, managing partner and chief investment officer at GammaRoad Capital Partners. In fact, those trends have been “accelerating,” with the underlying financing concerns for Big Tech, particularly in private credit, further compounding that problem, Rizzuto told MarketWatch via phone.

Barclays Plc’s Venu Krishna raised his year-end S&P 500 target to 7,650 despite growing macroeconomic risks from the war, AI disruption and private-credit stress. “The macro backdrop has become more fragile,” he wrote. “But we believe the US continues to offer stronger nominal growth than other major economies and a secular growth engine in technology that shows few signs of stopping.”

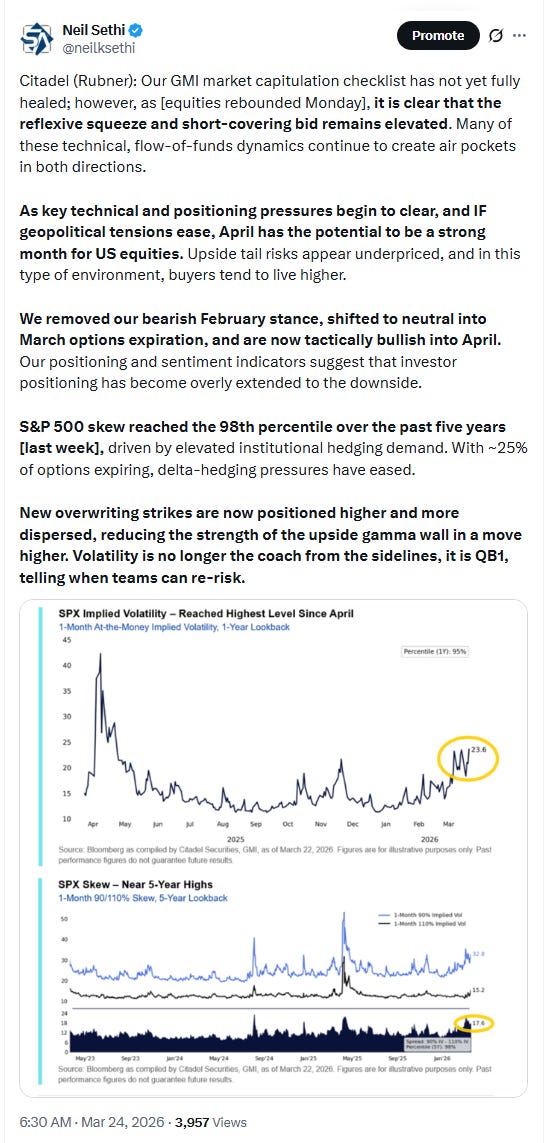

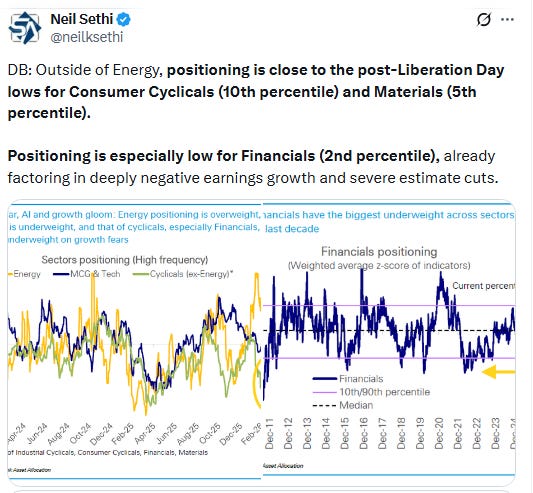

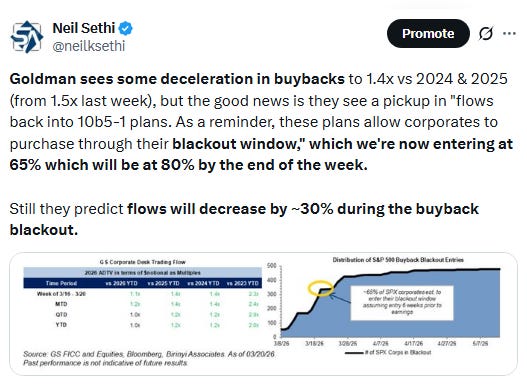

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

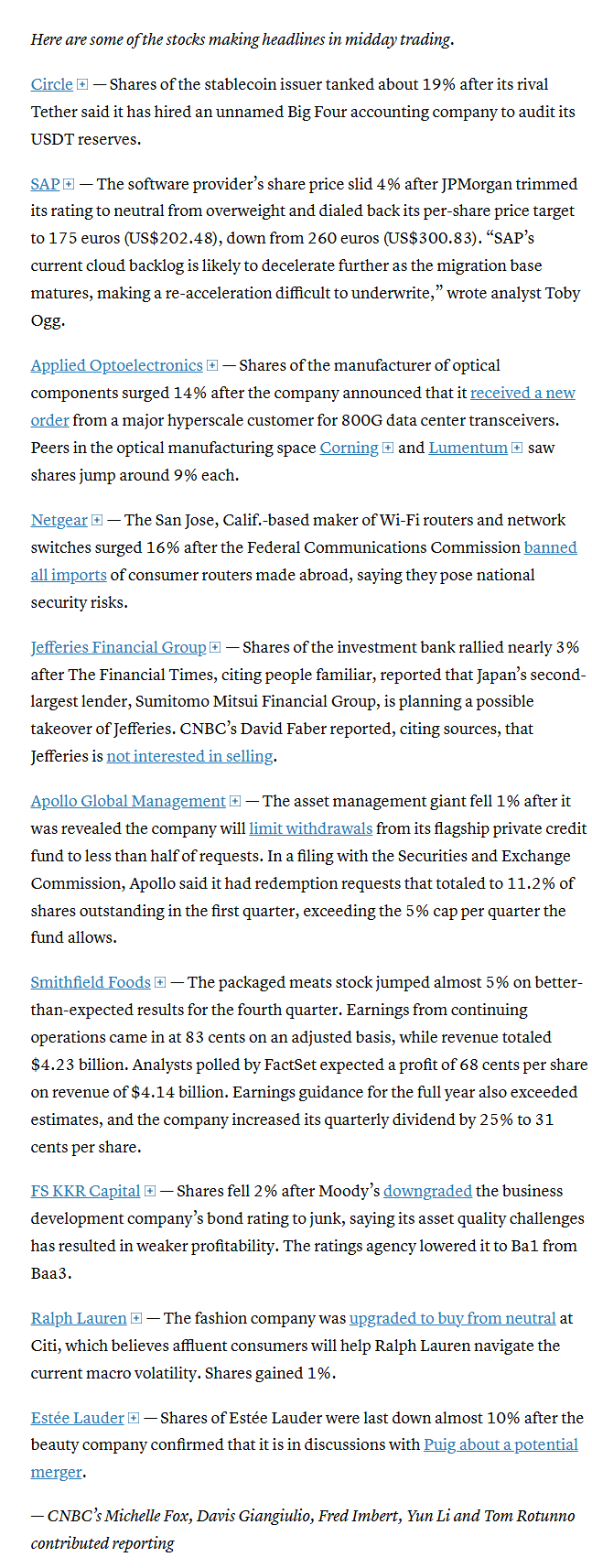

In individual stock action:

Two of the biggest names in private credit, Ares Management Corp. and Apollo Global Management Inc., blocked investors from getting even half of the money they wanted out of their funds, a sign of mounting strain in the $1.8 trillion market.

Corporate news from BBG:

United Airlines Holdings Inc. Chief Executive Officer Scott Kirby said ticket prices may have to go up by 20% if jet fuel prices remain elevated for longer.

Amazon Web Services is developing an AI agent to automate some of functions for sales, business development and other groups that have been targeted in the tech giant’s sweeping job cuts, the Information reported.

Arm Holdings Plc, which made its name licensing technology to semiconductor makers, will begin selling its own chips for the first time, adding a business that it expects to generate about $15 billion annually within five years.

OpenAI is nearing a deal to raise about $10 billion from venture investors, according to people familiar with the matter, bringing the total haul from its latest funding round to roughly $120 billion.

Mid-day movers from CNBC:

In US economic data:

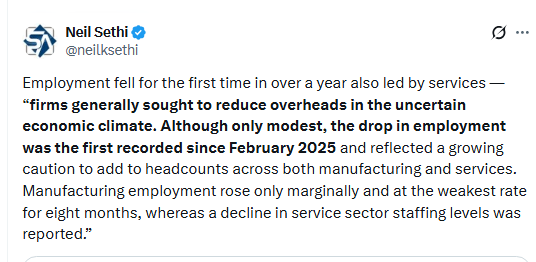

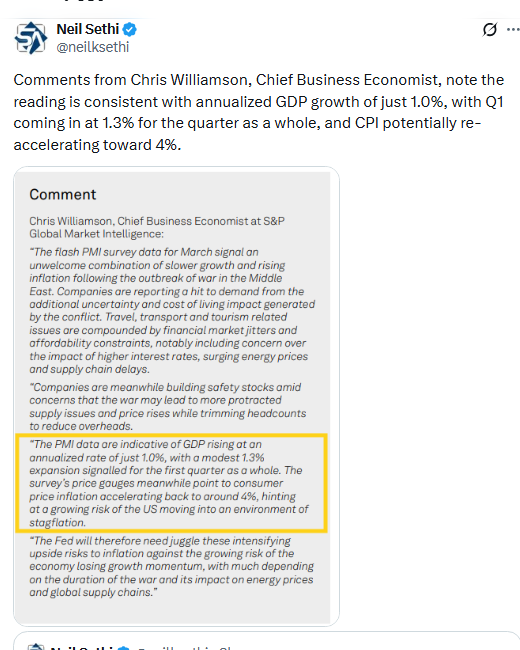

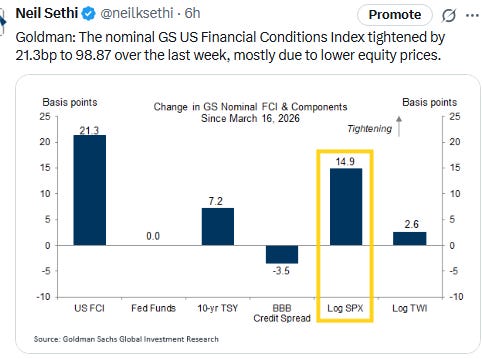

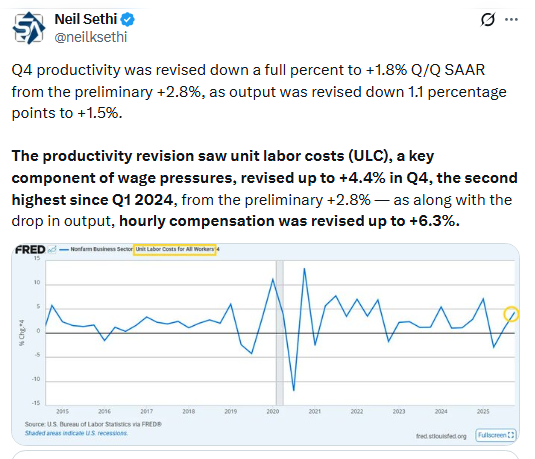

Substack articles - Note the productivity update was NOT emailed out.

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X