Markets Update - 3/26/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!), here’s the button:

Link to posts on X - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog.

Also, if you see an error (a chart or text wasn’t updated, etc.), always appreciate a note in the comments section or email so I can fix it.

In that regard, I do make mistakes sometimes, and usually I catch them at some point and correct them, and/or I sometimes add new material, so it’s always safest to read from the website where it will have any updates.

US equity indices opened trading lower Thursday, with futures steadily deteriorating overnight as hopes for a near-term resolution to the Iran conflict dimmed on a series of headlines detailed in the Morning Update. Events during the session didn’t do much to help with Iran reiterating what are clearly demands the US cannot accept and President Trump saying he wouldn’t commit to an agreement and threatening Iran anew with intensified military action, saying the US will “keep blowing them away,” until they agree to the US’ terms. Meanwhile Gulf countries issued a joint statement Thursday condemning Iran’s “criminal” strikes from Iraqi territory on their energy infrastructure. They added that they are ready to defend themselves going forward.

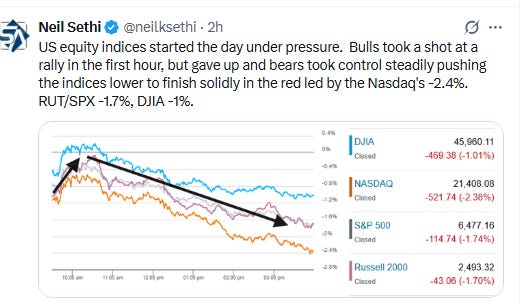

While indices attempted to rally in the first hour, that attempt was sold, and they spent the rest of the day pushing lower to end solidly in the red with the Nasdaq leading to the downside -2.4% as tech and related shares saw the worst of the selling, with the index entering into a correction (down over -10% from its high). The Russell 2000 and SPX ended -1.7%, the DJIA -1%.

Note: After the close of trading equities got a small lift as Pres Trump said he would extend a pause to attack Iran’s energy facilities to April 6, a little over a week after the original deadline that was set to end Friday. “As per Iranian Government request, please let this statement serve to represent that I am pausing the period of Energy Plant destruction,” Trump said in a Truth Social post. “Talks are ongoing and, despite erroneous statements to the contrary by the Fake News Media, and others, they are going very well.”

Elsewhere, bond yields and crude oil prices ended higher as did the dollar and US natural gas, while gold, copper, and bitcoin all were lower (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was -1.7%, the equal weighted S&P 500 index (SPXEW) -0.9%, Nasdaq Composite -2.4% (and the top 100 Nasdaq stocks (NDX) -2.4% (worst day since November)), the SOXX semiconductor index -4.8%, and the Russell 2000 (RUT) -1.7%.

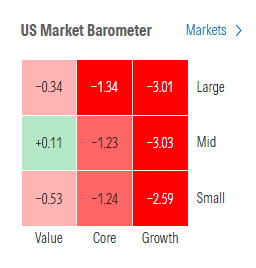

Morningstar style box showed the big underperformance of growth shares.

Market commentary:

“We may not be at the end of this situation, but we could be at the beginning of the end,” said Mona Mahajan, principal, head of investment strategy and asset allocation at Edward Jones. “Negotiations toward a resolution appear to be under way. The more important question is what happens with the Strait of Hormuz and oil prices.”

Thierry Wizman, global FX and rates strategist at Macquarie Group, said that a ceasefire is not imminent. “Rather, an intensification of military action by the U.S. as it tries to nudge Iran toward making important concessions is likely over the next two weeks, before major combat operations succeed, perhaps in mid-April,” said Wizman. “The War may now enter its third phase of ‘talk and fight,’ rather than talk only, or fight only,” he wrote in a note.

“If Iran were to signal willingness to negotiate and an end to the closure of the Strait of Hormuz became more likely, equity markets may quickly move back to previous highs,” said Wolf von Rotberg, strategist at Bank J Safra Sarasin. “Yet Iran has so far declined all offers to talk as time is on their side.”

“US stocks do not look adequately priced for a re-escalation. The implied probability for selloffs has risen, but not in a way that suggests a high likelihood of a much deeper decline. The comparative phlegmatism of stocks stands in contrast to the oil market.” — Simon White, macro strategist.

“The progress being made in the talks between the US and Iran seems to be sketchy at best,” said Matt Maley at Miller Tabak.

“The war in Iran and the resulting surge in oil prices continue to dampen risk appetite,” said Adam Turnquist at LPL Financial. “Any sustainable market recovery will require meaningful progress toward a peace agreement and a reopening of the Strait of Hormuz.”

Tobin Marcus, head of U.S. policy and politics at Wolfe Research, believes the recent market moves signal that investors are betting Iran is the one that could be “lying.” Markets “seem to be concluding that Iran’s negative public message may be a smokescreen for a more accommodating private posture,” he wrote in a note.

“It is a complacent market, and by that I mean investors are just inherently optimistic and willing to absorb bad news,” Jed Ellerbroek, portfolio manager at Argent Capital Management, said to CNBC. “The market wants to go up.”

Last week, the S&P 500 passed a key level when it broke below its 200-day moving average. According to HB Wealth Chief Market Strategist Gina Martin Adams, passing below this level tends to be indicative of more nervous markets.

“Sentiment is clearly, in the short run, being driven by headlines,” Adams said. She noted that investors have been hanging on to updates from political leaders on the latest in the Iran war. That can cause stocks to rally on good news and fall on bad news. Adams also said that investors are trying to anticipate the effect an energy shock will have on inflation. According to her, low inflation is more accommodative of high stock valuations.

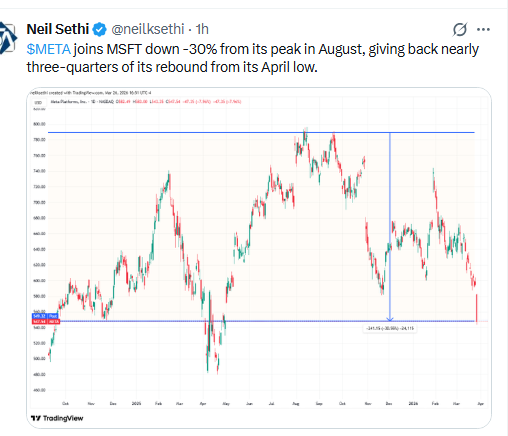

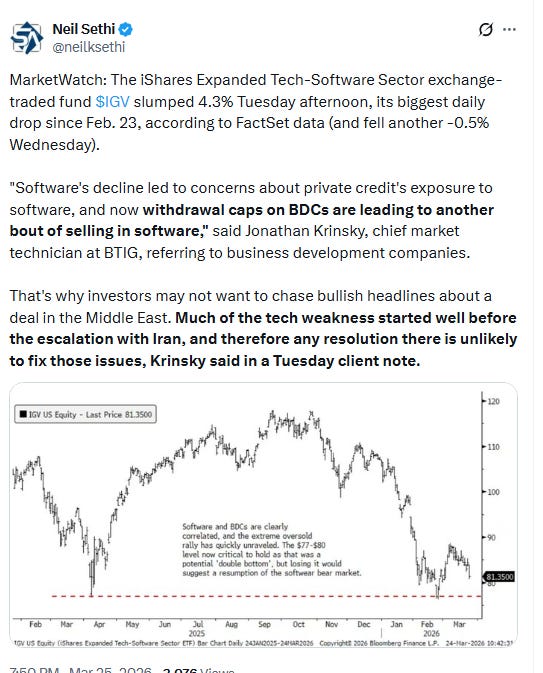

Tech stocks were leading the market’s losses on Thursday, with names across software, semiconductors and internet communication services dropping.

Hardika Singh, an economic strategist at Fundstrat Global Advisors, said this move is reflective of the rotation out of tech that has been happening since the start of the year. As markets move lower, investors sometimes react by selling recent winners to lock in those gains and then buy the dip elsewhere or reposition their portfolios defensively. “There’s a rotation trade taking place where investors are selling winners,” Singh said. “Everyone reached the consensus that we’re all overexposed to tech.”

"Markets are realizing that although the president may want to get out of this war, there's no easy way to do it," Singh said. She said it's no longer enough for investors to hang on to every word President Trump says in order to find the answers they're looking for.“Bond yields currently look much closer to fair value than they did a month ago, regardless of the war and simply due to underlying inflationary conditions and burgeoning budget deficits,” said Daniel Murray, deputy chief investment officer at EFG Asset Management. “The war may simply have accelerated the correction.”

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

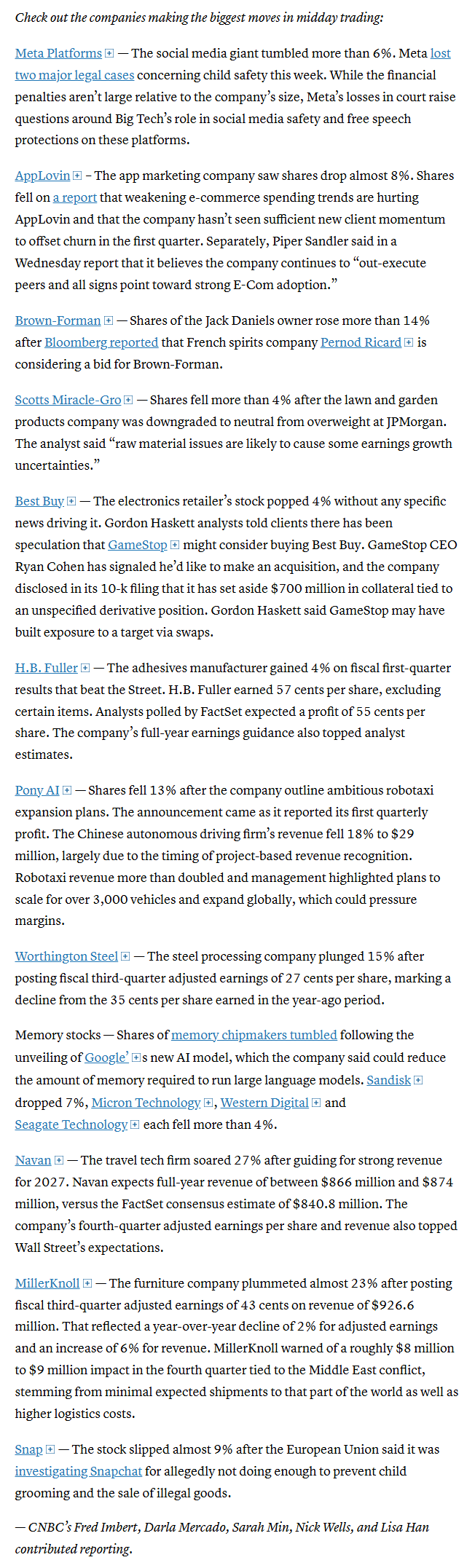

In individual stock action:

Memory chip stocks extended their losses on Thursday after Alphabet Inc.’s Google publicized research on a new algorithm that could allow more efficient use of the storage needed for artificial-intelligence development.

Meta Platforms — The social media giant tumbled almost 8%. Meta lost two major legal cases concerning child safety this week. While the financial penalties aren’t large relative to the company’s size, Meta’s losses in court raise questions around Big Tech’s role in social media safety and free speech protections on these platforms.

Corporate news from BBG:

Memory chip stocks extended their losses on Thursday after Alphabet Inc.’s Google publicized research on a new algorithm that could allow more efficient use of the storage needed for artificial-intelligence development.

Microsoft Corp. executives in recent weeks told managers at major divisions to suspend new hiring, The Information reported, citing three current employees with direct knowledge of the decision.

Apple Inc. plans to open Siri to outside artificial intelligence assistants, a major move aimed at bolstering the iPhone as an AI platform.

Macy’s Inc. has launched an AI-powered shopping assistant that’s upped spending online among those using the new tool, part of the company’s multiyear effort to reverse a sales decline.

Hertz Global Holdings Inc. and Avis Budget Group Inc. climbed as chaos at US airports due to the partial government shutdown spurred speculation that more travelers would rent cars instead.

Mid-day movers from CNBC:

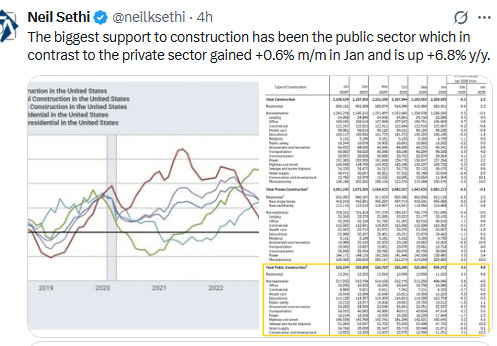

In US economic data:

Substack articles

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X