Markets Update - 3/27/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!), here’s the button:

Link to posts on X - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog.

Also, if you see an error (a chart or text wasn’t updated, etc.), always appreciate a note in the comments section or email so I can fix it.

In that regard, I do make mistakes sometimes, and usually I catch them at some point and correct them, and/or I sometimes add new material, so it’s always safest to read from the website where it will have any updates.

Note: As a reminder I will be competing at the Pan-American Jiu-Jitsu Championships this weekend. I am going to send something out for the Week Ahead, but it definitely will be abbreviated. I am not sure yet if I will have any Monday/Tuesday Market Updates.

US equity indices opened trading Friday again in the red as bond yields and crude prices again climbed higher with no end in sight for the Iran conflict. See the morning update for more details on developments as of this morning. Adding to concerns during the day two Chinese ships were turned away from crossing the Strait of Hormuz early Friday, and a Thai-flagged cargo ship that had been hit in the waterway ran aground, Iran state media said. The US and Israel bombed Iranian nuclear and steel facilities, while Iran retaliated across the Persian Gulf.

Economists raised their estimates for US inflation through year-end, while trimming consumer spending, growth and employment projections as the war in Iran drives up fuel, food, and other costs, according to the latest Bloomberg monthly survey.

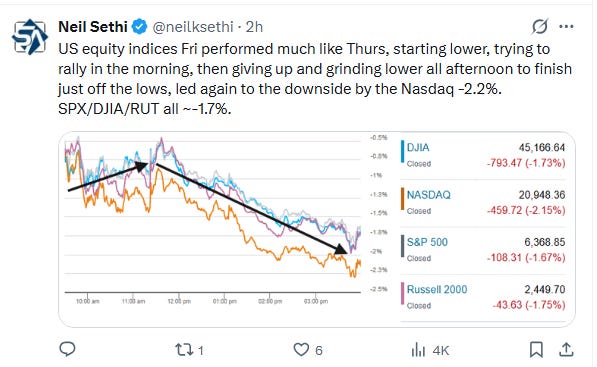

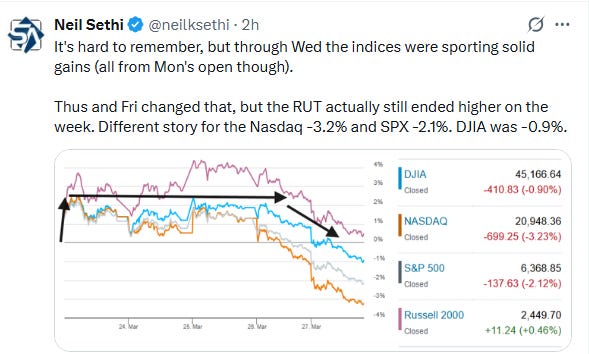

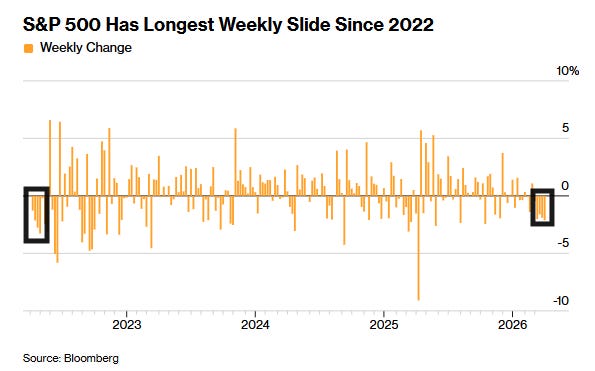

Equity indices like Thursday tried to rally in the morning, but again gave up and ground lower all afternoon to finish just off the lows, led again to the downside by the Nasdaq -2.2% which had entered correction territory Thursday. The S&P 500, DJIA, and Russell 2000 (RUT) all ended down around -1.7% with the DJIA also entering into a correction and the S&P ending lower for a fifth straight week for the first time since May 2022. For the week, the RUT actually ended higher, but the Nasdaq -3.2%, S&P -2.1% and DJIA -0.9% were lower.

Elsewhere, as noted long duration bond yields and crude oil prices pushed higher (the latter the highest since 2022) as did the dollar and US natural gas prices, unusually (for this month at least) joined by gold which is still though on track for its worst month since 2008. Copper was little changed while bitcoin fell to the lows of the month (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was -1.7%, the equal weighted S&P 500 index (SPXEW) -1.3%, Nasdaq Composite -1.9% (and the top 100 Nasdaq stocks (NDX) -1.9%, the SOXX semiconductor index -1.7%, and the Russell 2000 (RUT) -1.7%.

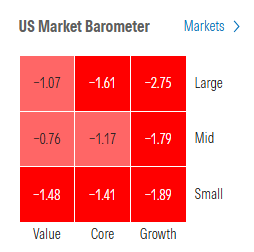

Morningstar style box all red with growth shares again underperforming.

Market commentary:

“I think we’re headed lower in the medium term until we get some more certainty,” Adam Parker, founder at Trivariate Research, told CNBC’s “Closing Bell” on Thursday. “You got to be cautious here and not take a ton of risk in the near term.”

Heightened uncertainty and headline-driven swings are pushing investors to cut risk, hedge more, and tighten liquidity, according to Mark Hackett at Nationwide. “Markets are reacting more to positioning and volatility than fundamentals,” he said. “The macro and earnings backdrop is still supportive and expectations have reset, but without clear resolution on the conflict and stabilization in energy markets, it’s hard to see a sustained move higher.”

“Risk aversion continues to dominate,” said Elias Haddad at Brown Brothers Harriman & Co. “Absent full US military control of the Strait of Hormuz, Iran effectively controls the escalation lever of this war, and the balance of risks point to a deeper unraveling.”

Keith Lerner, chief investment officer at Truist, argues that the range of outcomes related to Iran remain wide. With near-term market moves being driven by headlines, investors have a limited edge, according to Lerner.

“Still, we have seen an incremental reset in expectations, valuations, and technical conditions,” he writes. Lerner isn’t ready to make a high-conviction call that the worst is behind us. But he has observed oversold conditions in the market, pointing to 81% of S&P 500 stocks falling below their 50-day moving averages and the technology sector’s price-to-earnings ratio dropping to 21.1, compared with 32 times in October. “This supports a measured approach to putting some capital to work today,” he writes.

“After several glimmers of hope, fueled by comments from President Trump, which were quickly dashed, the market is becoming more demanding in terms of rhetoric,” said Amélie Derambure, senior multi-asset portfolio manager at Amundi. “The TACO trade is more difficult to do because a return to square one is not possible from here.”

“Even though the move might temporarily avoid escalation of the war between the US and Iran, it has prolonged the uncertainty around the length of the disruption to global oil supply,” said Ian Lyngen at BMO Capital Markets. “Reports that the US is sending additional ground troops to the Middle East have added to fears of escalation.”

“The logic of ‘escalation to de-escalate’ continues to play out, and this will dampen risk appetites ahead of the weekend,” said Marc Chandler at Bannockburn.

“Trump is unpredictable, so one doesn’t know whether he’s gaining time to send troops to invade the Strait of Hormuz or to negotiate further,” said Nicolas Domont, a fund manager at Optigestion in Paris. “The war could stop anytime and things could return to normal within a few months but one could also end up with oil at $200 in six months.”

The diplomatic dissonance between the US and Iran has dismayed investors, and risk appetite could not withstand the “fog of war,” according to Doug Beath at Wells Fargo Investment Institute. “Despite this week’s volatility, we still expect that the time pressure on the US will be a major factor in the war’s ultimate duration,” he said. Beath also noted that the traditional hedging strategies of investing in gold, Treasuries, defensive equity sectors and even a perceived global safe haven like the Swiss franc have not proven effective during this conflict. “Our view is that particular hedges are less effective than diversification and regular rebalancing when the risk is to the global economy,” he concluded.

“Traders are expressing extreme caution moving forward, given the situation in Iran is going to play out much longer than expected,” said Ryan Jacobs, founder of Florida-based advisory firm Jacobs Investment Management. “Oil prices are going to be higher going forward and that will mean logistics will be more expensive for the world moving from here.”

Even with Trump’s deadline extension, investors are at the point where they want to see a resolution to the conflict actually come to fruition as opposed to hearing there’s “just maybe” a resolution, said Jay Hatfield, founder and CEO at Infrastructure Capital Advisors. A resolution would be a boon for the stock market, which has tumbled since the U.S. and Israel attacked Iran’s energy infrastructure on Feb. 28. The three major averages have each fallen more than 7% month to date. “The longer the Strait is closed, the worse the oil market is going to get,” Hatfield said. “The price will go down a lot, but there’s still going to be an inventory issue when the Strait reopens, so if it takes another month to reopen the Strait, oil might stay at like $80 for a while until we can rebuild stocks.” “It’s bad if there’s no resolution, even if there is a path to resolution,” he continued.

“While the rhetoric around de-escalation and dialogue is certainly preferable to outright conflict, the market appears to be growing increasingly numb to President Trump’s verbal reassurances,” Tony Sycamore, market analyst at IG, said. “By extending the deadline, it effectively kicks the can down the road, pushing back any concrete resolution regarding the reopening of the Strait of Hormuz. This, in turn, simply extends the uncertainty weighing on markets and the broader global economy.”

“China has learned that a confrontational approach on trade produces the most favorable outcome in negotiations,” said Wolf von Rotberg, equity strategist at Bank J Safra Sarasin. “The reciprocal action China has launched should be seen as a move to stake out its territory ahead of the Trump-Xi meeting.”

“Assets were already lagging the earlier move in commodities. This suggests there is room for further adjustment to catch up with existing price increases. As energy prices continue to rise, the outlook for both bonds and equities can only deteriorate further.” — Skylar Montgomery Koning, macro strategist

“The combination of inflation and recent strong labor data leaves the Federal Reserve with no justification to cut rates, which, in turn, strengthens the US dollar and causes widespread volatility in equities, bonds, and gold,” said Craig Johnson at Piper Sandler.

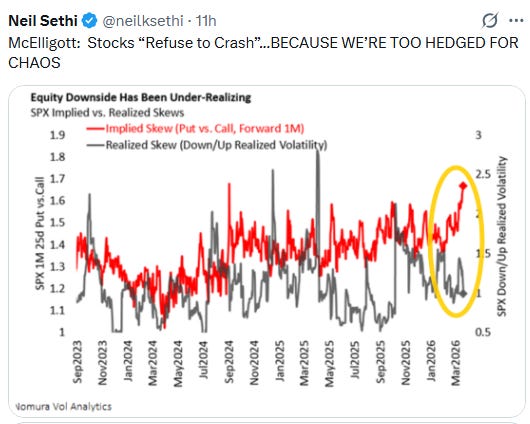

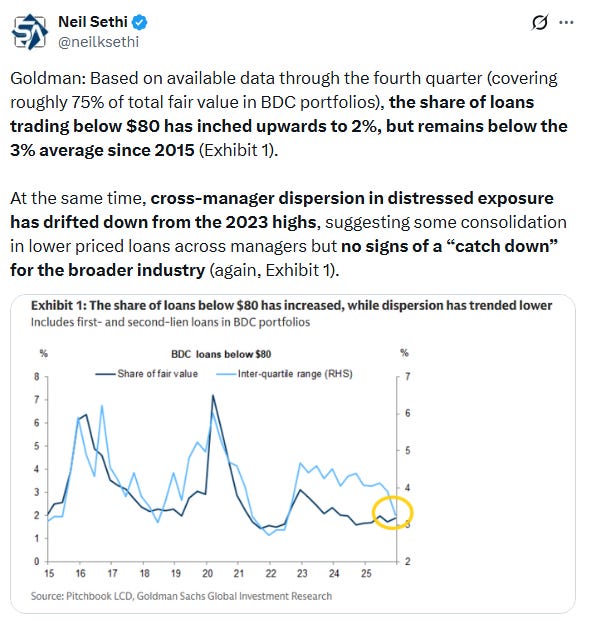

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

Meta Platform shares tumbled more than 4% after falling 8% Thursday. Meta suffered a rocky week, losing two pivotal court cases and announcing a round of layoffs across Facebook, Reality Labs and other departments. The stock is down more than 11% on the week, heading for its worst weekly performance since October.

Brown-Forman — Shares added 6% after the Kentucky whiskey maker confirmed on Thursday that it was engaged in merger discussions with Pernod Ricard, a French wine and spirits company. Brown-Forman said that any resulting partnership would be “akin to a merger of equals” and draw from the talent and expertise of both companies.

Corporate news from BBG:

Carnival Corp. cut its full-year profit outlook as surging crude prices are driving up fuel costs.

Anthropic PBC is considering going public as soon as in October, according to people familiar with the matter, as the artificial intelligence company races with rival OpenAI Inc. to hold an initial public offering.

Oaktree Capital Management is meeting all redemption requests it received for a $7.7 billion private credit fund aimed at retail investors, siding with managers that have decided against enforcing a cap on withdrawals.

Pernod Ricard SA and Brown-Forman Corp., the owner of Jack Daniel’s whiskey, are discussing a merger as the alcoholic drink companies look at ways to consolidate amid an industry downturn.

Mid-day movers from CNBC:

In US economic data:

Substack articles

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X