Markets Update - 3/30/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!), here’s the button:

Link to posts on X - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog.

Also, if you see an error (a chart or text wasn’t updated, etc.), always appreciate a note in the comments section or email so I can fix it.

In that regard, I do make mistakes sometimes, and usually I catch them at some point and correct them, and/or I sometimes add new material, so it’s always safest to read from the website where it will have any updates.

Note: I’m still out of town, and I did this very quickly, so please excuse extra typos, etc. Also no opener tomorrow morning.

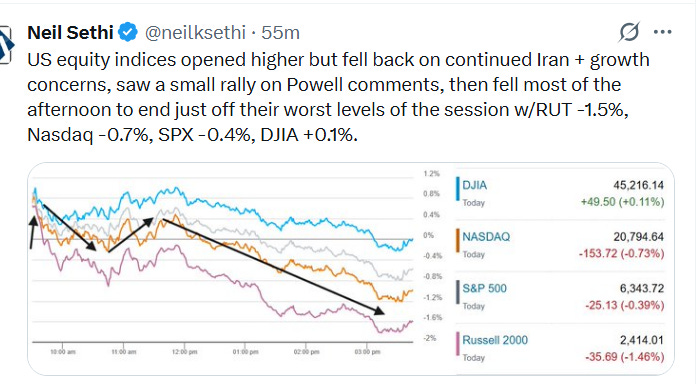

US equity indices opened trading for the week solidly higher (they had finished each Monday this month in the green) as oil prices eased off following Pres Trump posting this morning that “The United States of America is in serious discussions with A NEW, AND MORE REASONABLE, REGIME… Great progress has been made but, if for any reason a deal is not shortly reached, which it probably will be, and if the Hormuz Strait is not immediately “Open for Business,” we will conclude our lovely “stay” in Iran by blowing up and completely obliterating all of their Electric Generating Plants, Oil Wells and Kharg Island (and possibly all desalination plants!)…” The full post and all of the overnight developments were covered in the opening post this morning.

However, equity indices started to decline as soon as the cash market opened as investors started to consider a new potential issue in slowing growth. Positively that saw yields ease off despite a renewed rise in oil prices, but the stagflationary-like concerns around slowing growth and rising inflation kept equities under pressure all session, seeing a late morning rally on soothing comments from Fed Chair Powell which also though fizzled, seeing equities falling most of the afternoon to end just off their worst levels of the session with small caps and tech shares leading losses. The Russell 2000 finished -1.5%, Nasdaq -0.7%, SPX -0.4%, but DJIA +0.1%.

Elsewhere, as noted bond yields eased back, but the DXY dollar index still rose pushing to its highest close of the year. Crude oil prices also were higher with US WTI closing over $100 for the first time since 2022. Gold and bitcoin also rose while copper and US natural gas prices fell back (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was -0.4%, the equal weighted S&P 500 index (SPXEW) -0.2%, Nasdaq Composite -0.7% (and the top 100 Nasdaq stocks (NDX) -0.8%, the SOXX semiconductor index -4.2%, and the Russell 2000 (RUT) -1.5%.

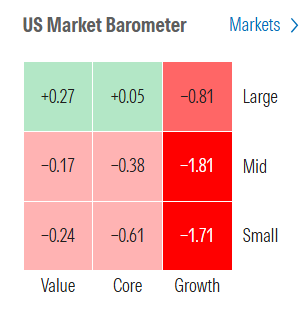

Morningstar style box all red with growth shares underperforming for a third session.

Market commentary:

“Stocks continue to fight an uphill battle against oil prices and political uncertainty. History shows most geopolitical shocks tend to have a relatively short-lived impact on the market, but without clear evidence of an endgame for the Iran war, stocks will find it difficult to see past the current volatility and sustain upside momentum. This week’s labor market data will likely take a back seat to developments in the Middle East,” E-Trade’s Chris Larkin said in written commentary.

“The market continues to be headline-driven as the Trump Administration has delivered a variety of messages surrounding de-escalation and re-escalation of the war in Iran,” said Chris Senyek at Wolfe Research. “As such, we maintain our defensively positioned posture.”

“Until there’s something more concrete on a ceasefire or diplomatic progress, any short-term moves against the prevailing trend should be treated with caution,” said Fawad Razaqzada at Forex.com.

There are two major themes “flying against each other” in the markets on Monday, according to Mark Hackett, chief markets strategist at Nationwide.

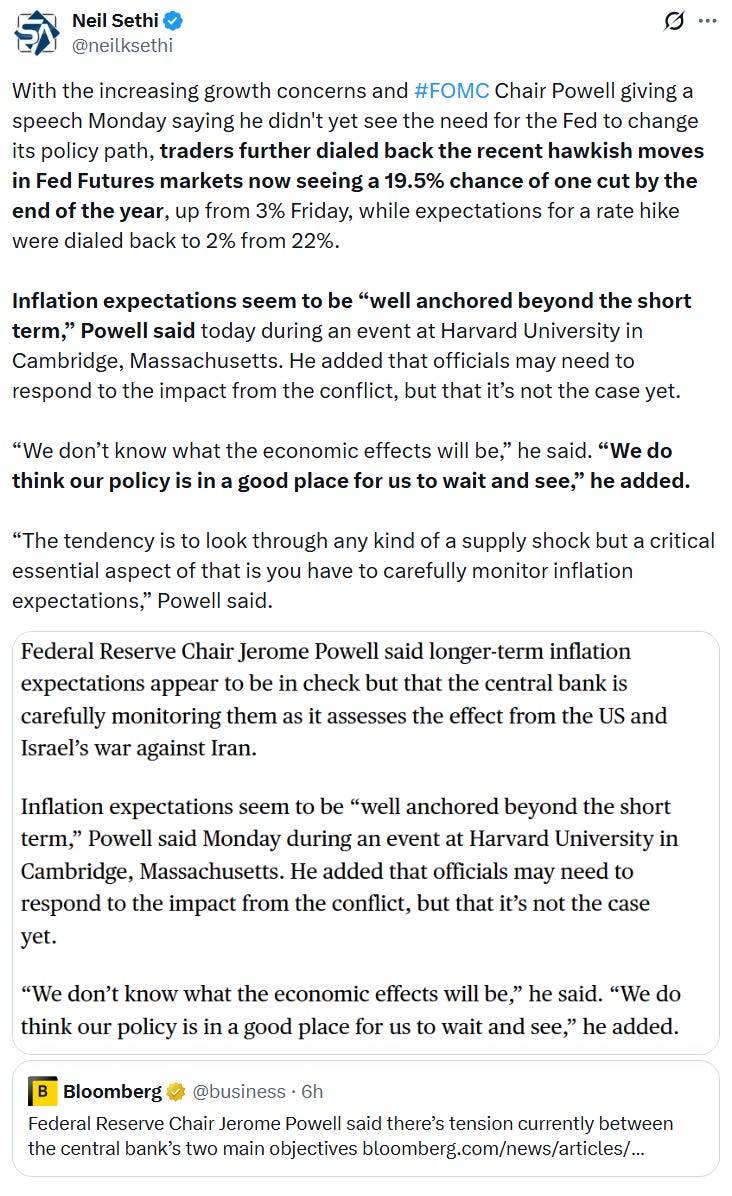

The bond market has been mostly reacting to Federal Reserve Chairman Jerome Powell’s comments, while the stock market is “entirely” focused on the Iran conflict, according to Hackett.

There could be more room for interest-rate expectations to change following Federal Reserve Chair Jerome Powell’s comments on Monday, according to Krishna Guha and Marco Casiraghi, analysts at Evercore. “Following Powell’s remarks, we are finally back to pricing one or more cuts as fractionally more likely than a hike this year. We think the probability of one or more cuts is much higher than the probability of a hike,” the Evercore analysts said.

While there may be a case for no rate cuts this year, the analysts added that the bar for a rate hike is high, especially considering Kevin Warsh’s expected succession as Fed chair in May.

“The second-order impact from the war in the Mideast [is the] most meaningful wildcard for 2026,” BMO’s Ian Lyngen and Vail Hartman remarked, noting that in the end, “the outlook for real spending will depend more on the employment landscape and consumers’ sense of job security” than it will the price impact from the supply shock. “Sentiment is surely waning,” Lyngen went on. “After all, over the last year, we’ve seen the trade war, government shutdown, budget deficit jitters, Fed independence struggles, private credit concerns, worries about overseas sponsorship for Treasurys, questions of the dollar’s standing as the reserve currency, and now a war in the Mideast.”

“While inflation remains a concern, the potential drag on growth and confidence should start to act as an offset, limiting further upside in yields,” said Francisco Simón, European head of strategy at Santander Asset Management. “Together with oil, we think the bond market is currently one of the clearest expressions of how markets are pricing the impact of the conflict on the macro outlook.”

“We still have this mindset that this is transitory, that somehow, yes, there’s going to be a short-term effect, but we should look through it,” Mohamed A. El-Erian, Allianz chief economic advisor, said on CNBC’s “Squawk Box” about sentiment in the equity market, adding that investors also aren’t pricing in “very limited policy flexibility” due to the war. “There’s a real question mark as to what the Fed is going to do, and we’re already running a 6% deficit,” he continued. “The market hasn’t quite realized that if this goes on, the policy offsets much less than what we’ve had before.” El-Erian believes the next tipping point economically speaking would be “physical shortages,” saying Monday that “if we start seeing that in Asia, that will impact the U.S.” He continued, “the U.S. will now import higher products in terms of prices, and the question is do we now see also a disruption in the availability of products?”

“Overall, it’s a walk not run type situation with equities but the starter’s pistol has gone off,” Christopher Harvey, head of equity and portfolio strategy at CIBC Capital Markets, wrote in a research note Thursday.

At Truist Advisory Services Inc., Keith Lerner is encouraging clients to use pullbacks to buy large-cap stocks, among others, while keeping some cash on the sidelines in case geopolitical tensions push stocks even lower. “If you have cash, you don’t want to necessarily just wait for the perfect opportunity because it could be something that comes from a headline that you just aren’t going to be able to react to in time,” said Lerner, the firm’s chief investment officer and chief market strategist. “There might be an opportunity to be more aggressive if we get a true flush.”

“The risk-reward is improving as the market pulls back,” said Truist’s Lerner, adding that market retreats are the “price of admission” for investors to get into the market at compelling prices. He recommends positioning for a potential bounce by taking a slow and prudent approach to adding exposure to quality US mega-cap stocks. “Investors need to be aware – not try to be a hero,” Lerner said.US stocks are buttressed by what the analysts call an “acyclical investment cycle,” which includes AI-related capital outlays as well as defense and energy-related spending. US corporate earnings are also expected to grow 15% this year in the biggest advance since the aftermath of the Covid-19 pandemic. “There is a wall of worry – but it’s worth climbing,” Barclays analysts Ajay Rajadhyaksha and Amrut Nashikkar said.

To Wells Fargo equity strategist Ohsung Kwon, the setup creates an “upside pain trade” for investors, where mega-cap technology companies and the Nasdaq 100 are expected to outperform sharply.

Bill Ackman said the current market dislocation has created one of the most attractive entry points for high-quality companies in years, urging investors to look past macro fears and lean into what he sees as deeply discounted opportunities. “Some of the highest quality businesses in the world are trading at extremely cheap prices,” Ackman wrote in a post on X late Sunday. “One of the best times in a long time to buy quality. Ignore the bears.” Ackman argued that geopolitical concerns are being overstated. “One of the most one-sided wars in history that will end well for the U.S. and the world. And we have the potential for a large peace dividend,” Ackman wrote.

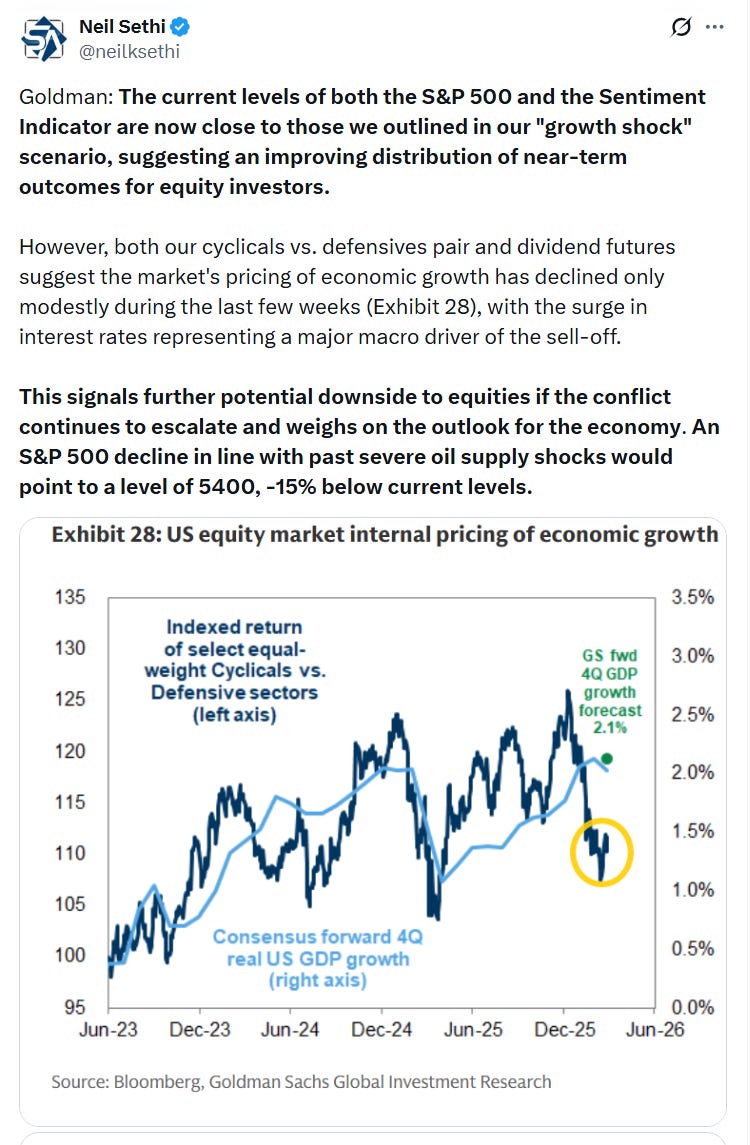

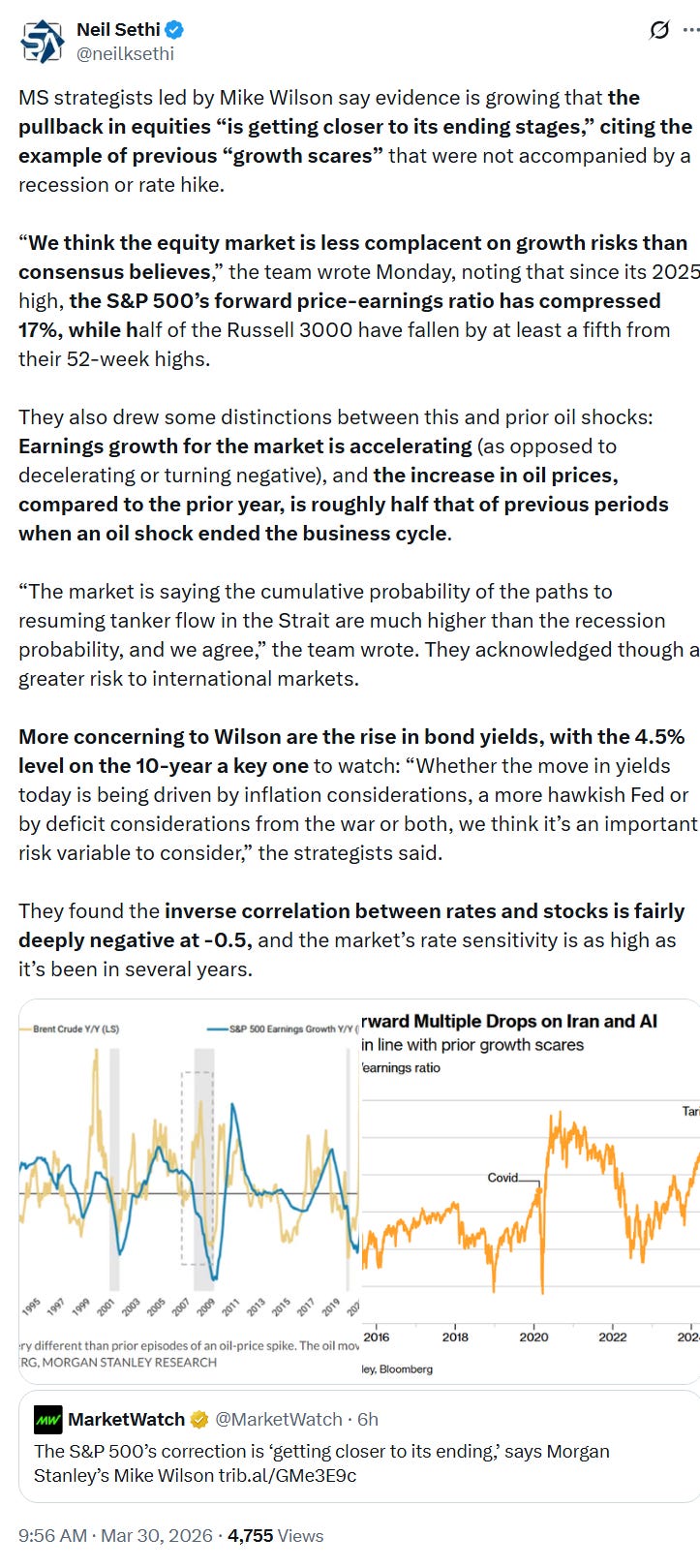

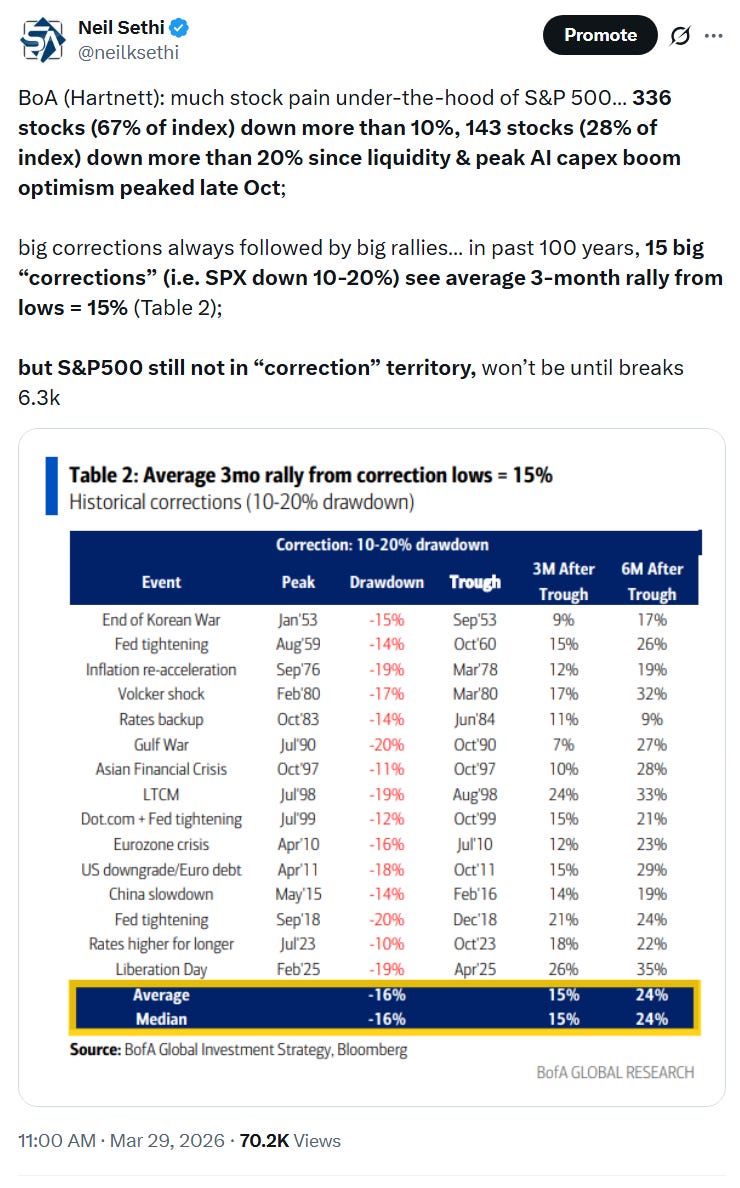

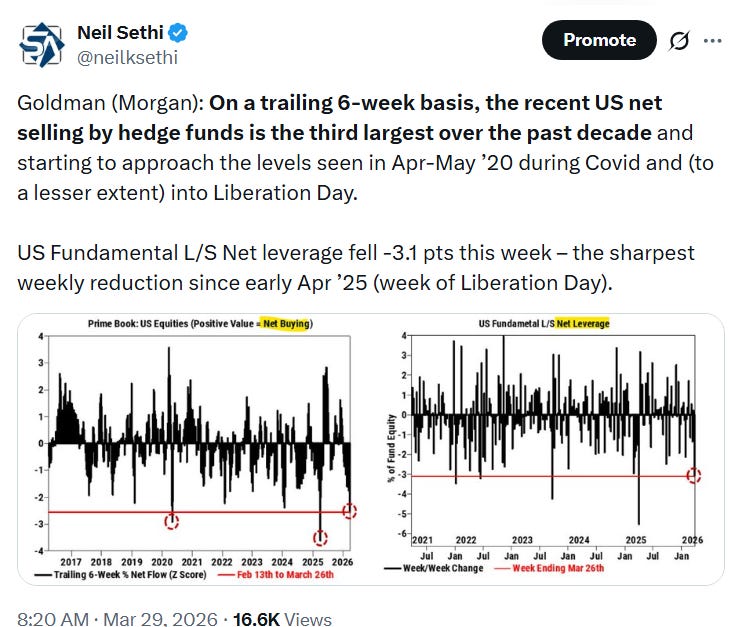

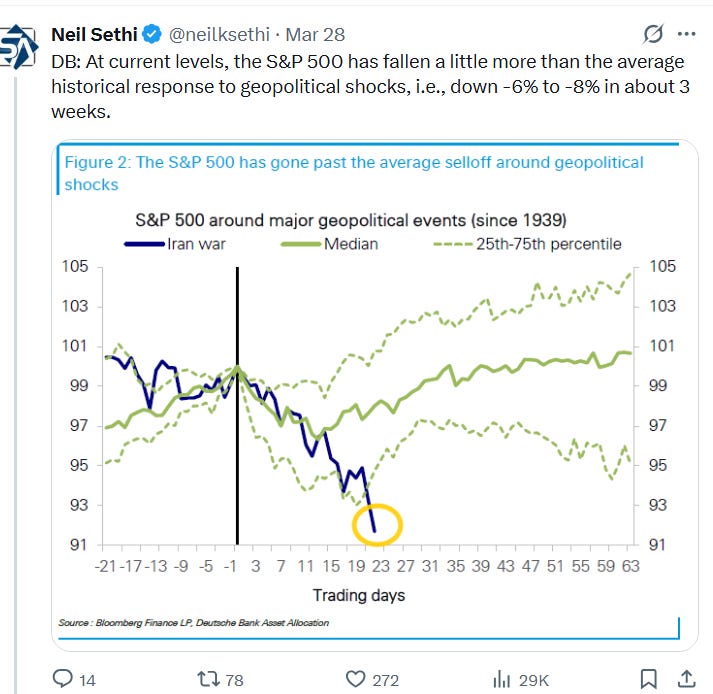

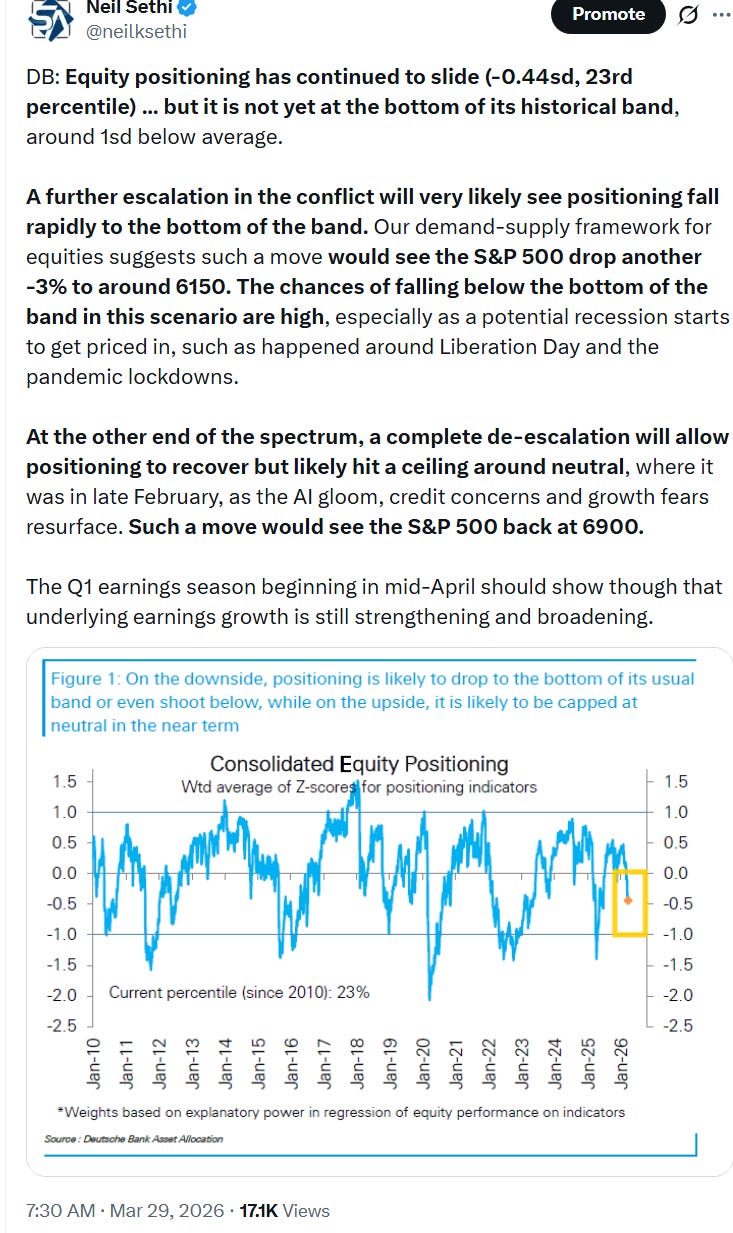

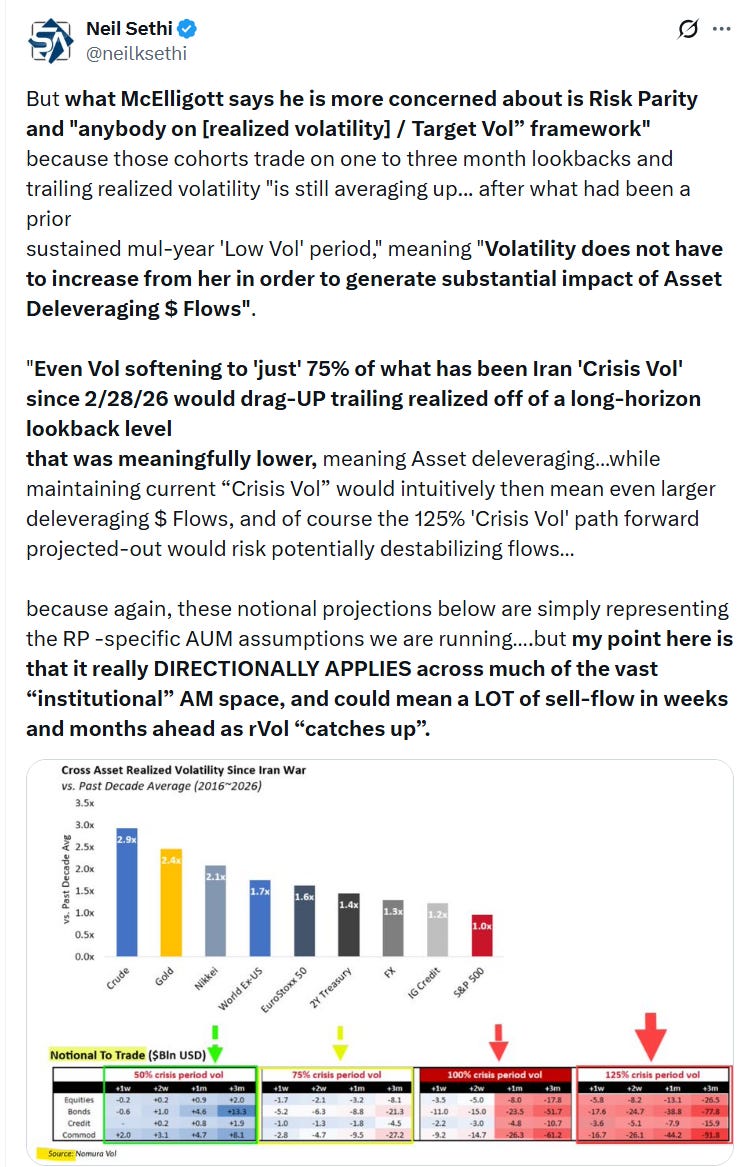

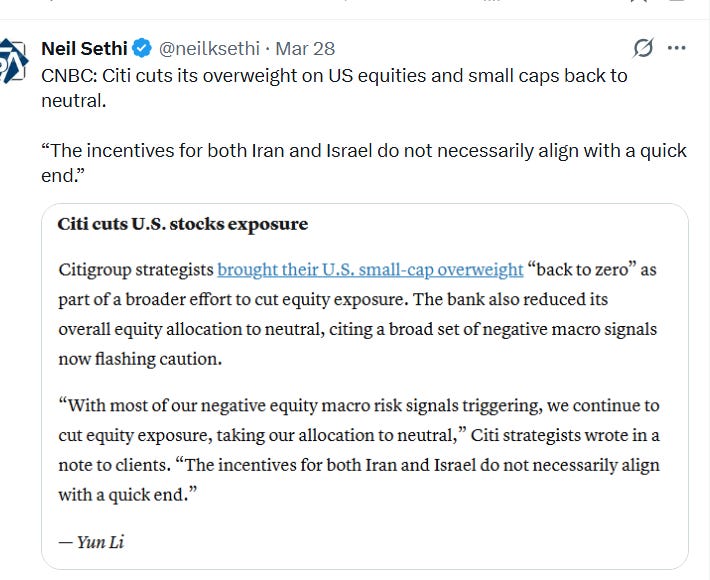

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

Shares of Micron were off 10% in late Monday, now barely in positive territory for the year after being up more than 60% as of the middle of March. In the last eight trading sessions, Micron has now fallen over 30%

Corporate news from BBG:

Morgan Stanley’s E*Trade unit is in talks with SpaceX to lead the sale of IPO shares to small investors, potentially being favored over rival brokerage platforms from Robinhood Markets Inc. and SoFi Technologies Inc., Reuters reported, citing two people familiar with the matter.

Fannie Mae and Freddie Mac pared a months-long slide after Bill Ackman, who has bet heavily on the companies, called the mortgage-finance giants “stupidly cheap.”

Sysco Corp. is acquiring Jetro Restaurant Depot LLC, the closely held wholesaler founded by billionaire Nathan “Natie” Kirsh, for $29.1 billion including debt in a deal that will create one of the largest food-service groups in the US.

US regulators have approved a high-dose version of Biogen Inc.’s drug for a rare muscle disorder, giving the company a boost as it competes with a gene therapy from Novartis AG.

Mid-day movers from CNBC:

In US economic data:

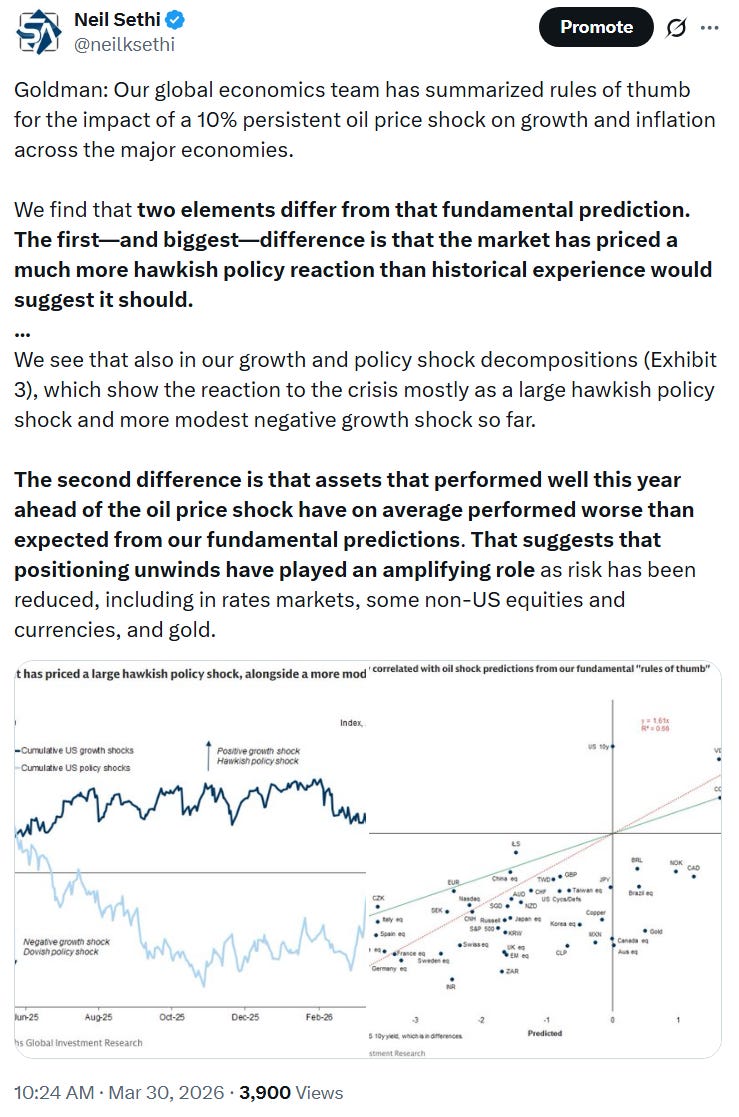

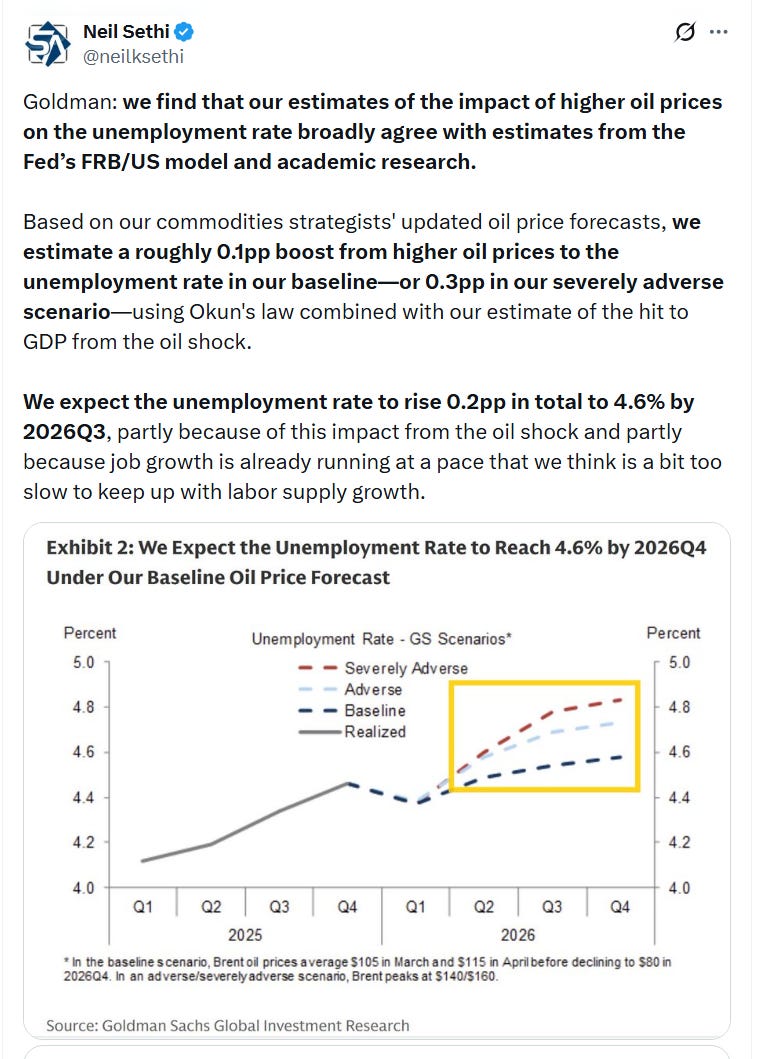

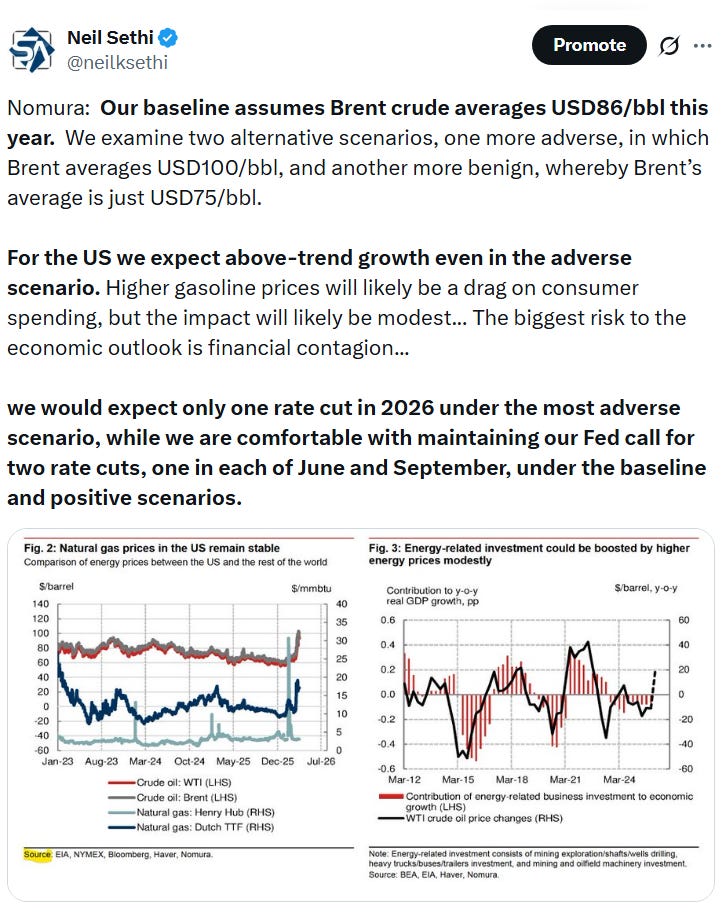

Substack articles

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X