Markets Update - 3/31/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!), here’s the button:

Link to posts on X - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog.

Also, if you see an error (a chart or text wasn’t updated, etc.), always appreciate a note in the comments section or email so I can fix it.

In that regard, I do make mistakes sometimes, and usually I catch them at some point and correct them, and/or I sometimes add new material, so it’s always safest to read from the website where it will have any updates.

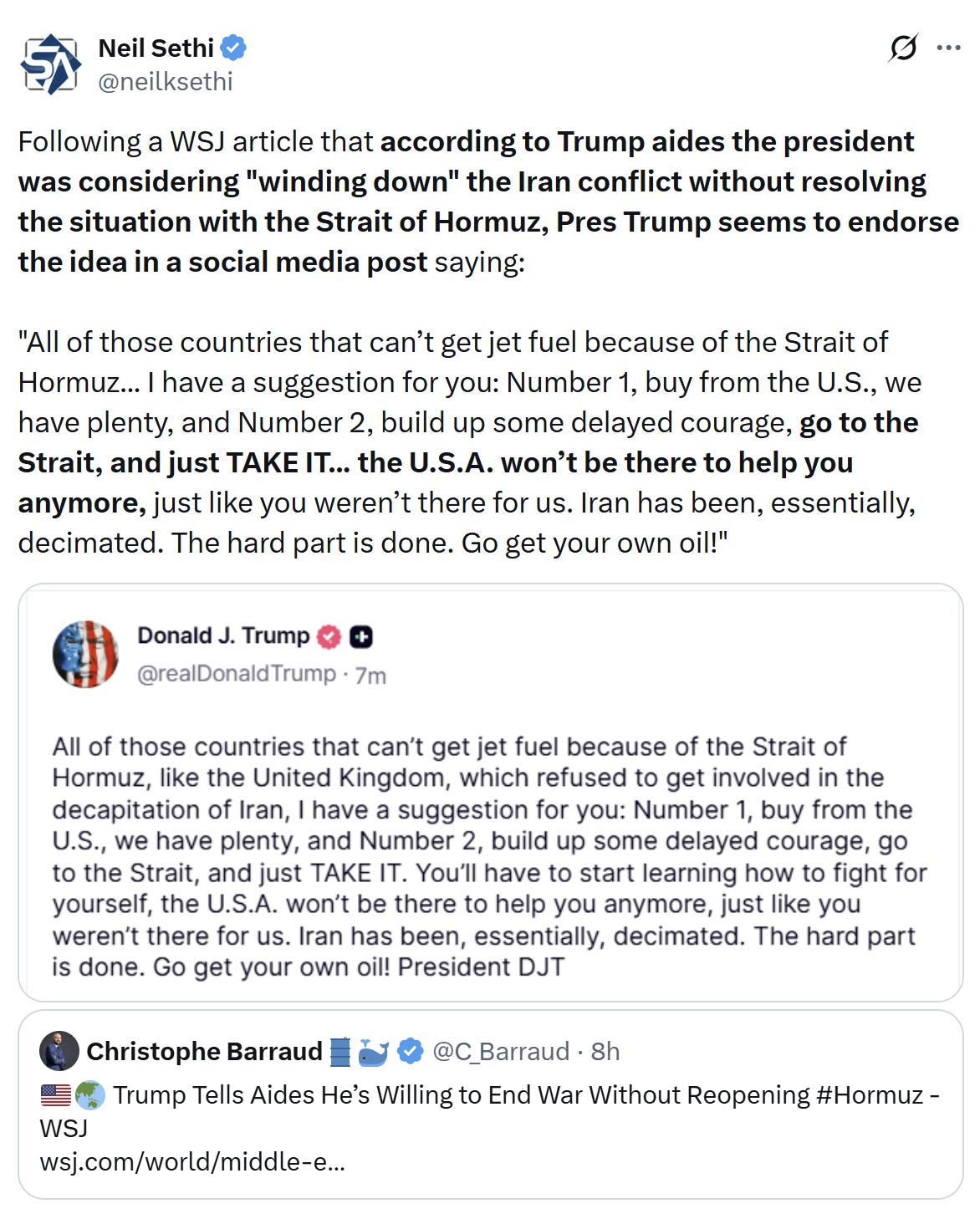

US equity indices opened trading Tuesday like Monday solidly higher, initially on a WSJ article that reported Trump aides said the president was considering "winding down" the Iran conflict even without resolving the situation with the Strait of Hormuz, and getting another lift after Pres Trump seemed to endorse the idea in a social media post saying: "All of those countries that can’t get jet fuel because of the Strait of Hormuz... I have a suggestion for you: Number 1, buy from the U.S., we have plenty, and Number 2, build up some delayed courage, go to the Strait, and just TAKE IT... the U.S.A. won’t be there to help you anymore… Go get your own oil!"

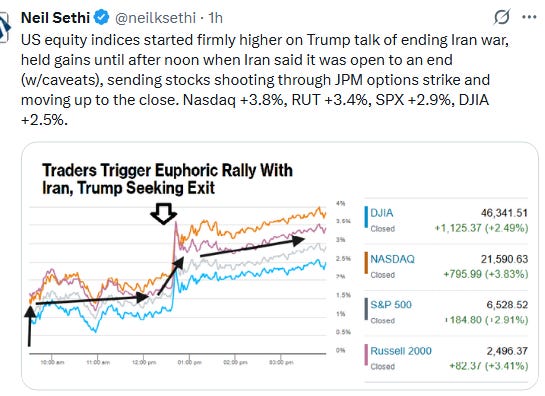

Equities eased off after Iran's Islamic Revolutionary Guard Corps issued a warning that it will target 18 American companies in the region for assisting with the U.S.-Israeli military operation, including Microsoft, Apple, Google, Intel and Boeing, but then shot higher after dual headlines, one from Iran’s state news agency reporting President Masoud Pezeskhian saying Iran has “the necessary will to end this war,” so long as it received guarantees “to prevent the recurrence of aggression,” and second a New York Post interview where Trump said “We’re not going to be there too much longer. We’re obliterating the s–t out of them right now, it’s a total obliteration.” As to the Strait, Trump said “Well, I think it’ll automatically open, but my attitude is, I’ve obliterated the country. They have no strength left, and let the countries that are using the strait, let them go and open it.”

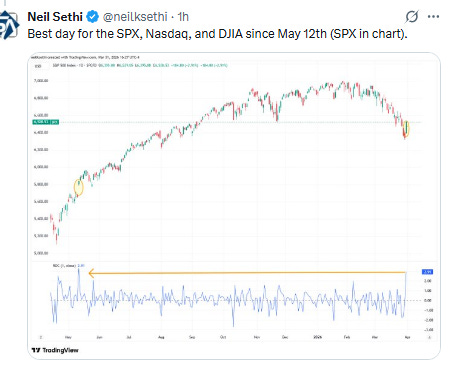

Equities shot higher at that point, wth the move likely exacerbated by a large options position held by a JP Morgan fund (see posts below), and they continued to rise most of the afternoon with the best gains since May for the Nasdaq +3.8%, SPX +2.9%, and DJIA +2.5%. The Russell 2000 +3.4%, saw its third best day since then. But all finished the monthly down the most since last March, with the DJIA down the most since Sept 2022.

After the close, Pres Trump tripled down on the “winding up” theme: “I would say that within two weeks, maybe two weeks, maybe three,” Trump told reporters in the White House on Tuesday. “We’ll leave because there’s no reason for us to do this.”

Elsewhere, bond yields eased back for a second day, as did crude prices, the dollar, and US natural gas. Gold, copper, and bitcoin all rose (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was +2.9%, the equal weighted S&P 500 index (SPXEW) +2.0%, Nasdaq Composite +3.8% (and the top 100 Nasdaq stocks (NDX) +3.4%, the SOXX semiconductor index +6.2%, and the Russell 2000 (RUT) +3.4%.

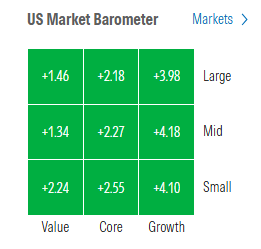

Morningstar style box saw strong gains across the board led by growth bouncing back after underperforming the prior three sessions.

Market commentary:

Art Hogan, chief market strategist at B. Riley Wealth Management, said that the recent pullback may reflect a typical market reset rather than anything out of the ordinary. “There’s a couple of narratives going on, but I think long term investors should keep in mind that 10% corrections are normal. They happen all the time. On average, every two years we have a 10% correction,” he said to CNBC. “It’s also important for investors to understand that the volatility in equities is the price you pay for the higher longer-term returns.”

“We’ve had a smattering of positive days when there’s some whiffs of good news,” he added.

“Markets have taken it on the chin for over a month and expectations may have hit a low enough point that any glimmer of hope is now much more valuable,” said Michael Bailey at FBB Capital Partners.

“One can’t exclude a swift resolution, but it won’t mean going back exactly to where we were in February,” said Kevin Thozet, a member of the investment committee at Carmignac. “Investors are seeing the glass half-full. During the past 15 years or so, buying the dip has been absolutely key.”

“There’s clearly some complacency across the market; there’s no capitulation whatsoever to be found in flows, fundamentals or through a technical analysis,” said Karen Georges, an equity fund manager at Ecofi in Paris. “Despite the rise today, I would say the market is reluctant to take a strong directional bet.”

“The improved mood in the rates market can only be temporary. The idea that Brent crude offers some relief simply because it has fallen to levels below $110 a barrel overlooks both the regime shock we have had in prices and the still-dour outlook for supply disruptions.” — Ven Ram, macro strategist

“Any steps toward ending the war overall, the stock market likes, and so, you are getting that relief rally,” said Eric Diton, president at The Wealth Alliance. “But no, we’re not out of the woods.”

“The bottom line is, if we haven’t solved the oil problem, then that continues to put pressure,” Diton added.

“While Trump may be considering an end to hostilities, the key issue — the status of the Strait — remaining unresolved will be what’s more important from the market’s point of view,” said Fawad Razaqzada at Forex.com. “It’s difficult to see Iran stepping back without extracting concessions.”

StoneX analyst Fawad Razaqzada said that conciliatory tones from Washington could help boost stocks and tamp down rising oil prices, but a rally based on sentiment alone may not last. “The danger, however, is that this proves yet another false dawn. If that’s the case, equities and risk-sensitive currencies could quickly find themselves back under pressure,” he said.

“Sometimes the headlines make you scratch your head,” said Bespoke Investment Group strategists. “If the US just walked away from the Middle East with the Strait still blockaded, energy markets would likely remain incredibly supply-constrained, keeping prices high. Maybe the market expects that if the US pulls back, the Strait would reopen.”

“Trump’s rhetorical gymnastics are seen increasingly as part of an effort to manage Iran’s expectations and traders’ expectations simultaneously. Doing that requires that threats of War alternate with the promise of peace,” Macquarie Group strategist Thierry Wizman wrote in an email. “But that shouldn’t be confused with TACO, which we haven’t seen yet.” Wizman said there are signs that the war may broaden out before it ends, pointing to the increasing U.S. military presence in Iran.

“Ultimately, both investors and consumers need to see notable de-escalation in the Middle East and some relief at the gas pump before confidence can rebound significantly,” said Bret Kenwell, U.S. investment analyst at eToro. “From here, investors will look to Friday’s jobs report in hopes that it can offer signs of some stabilization in the labor market.”

“There do appear to be some early signs of stabilization in both consumer confidence and job openings after a clear fourth-quarter downtrend,” said Bret Kenwell at eToro. “While that doesn’t yet signal a meaningful rebound, it may suggest the consumer and labor backdrop are no longer deteriorating at the same pace.”

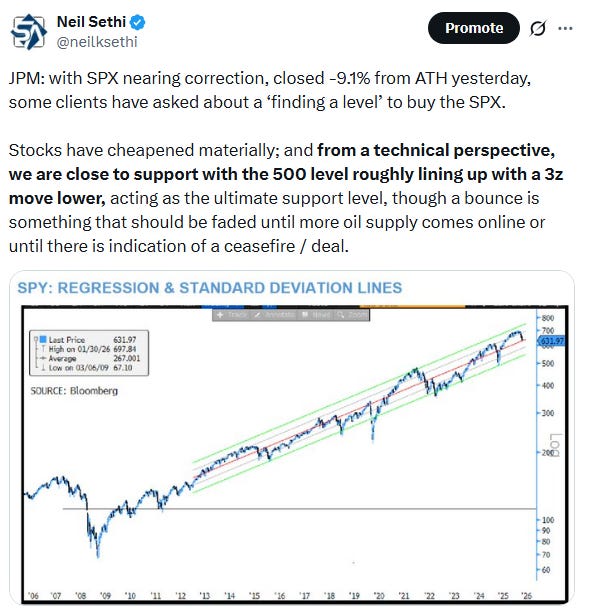

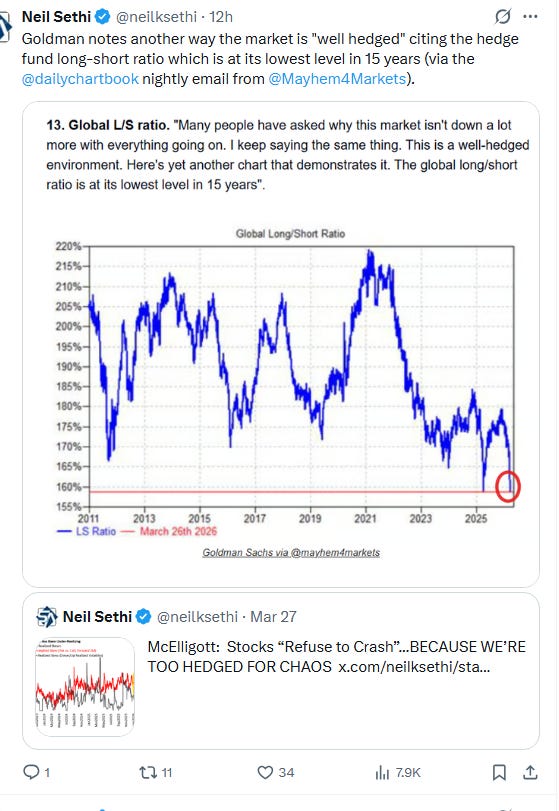

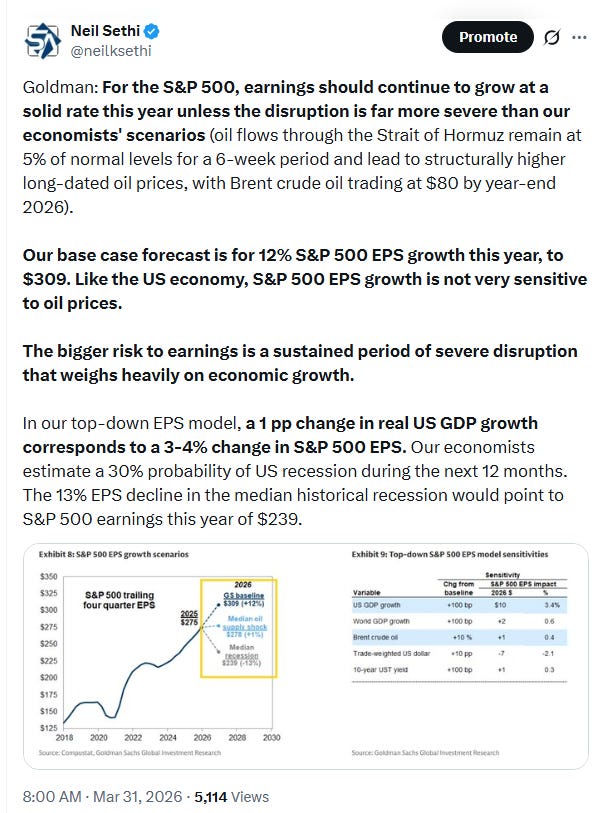

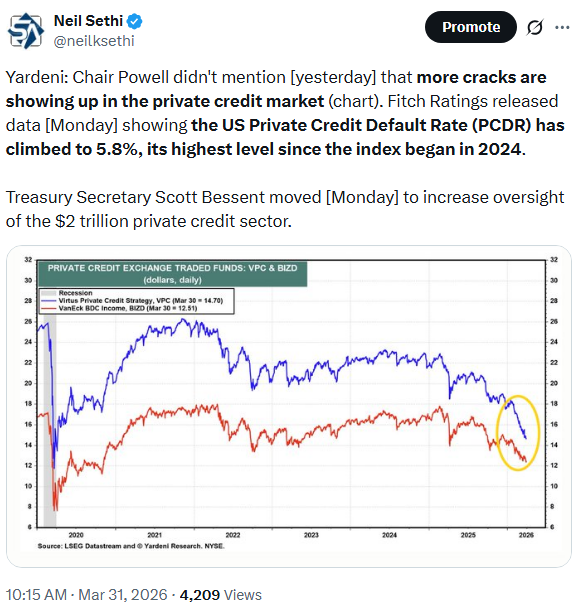

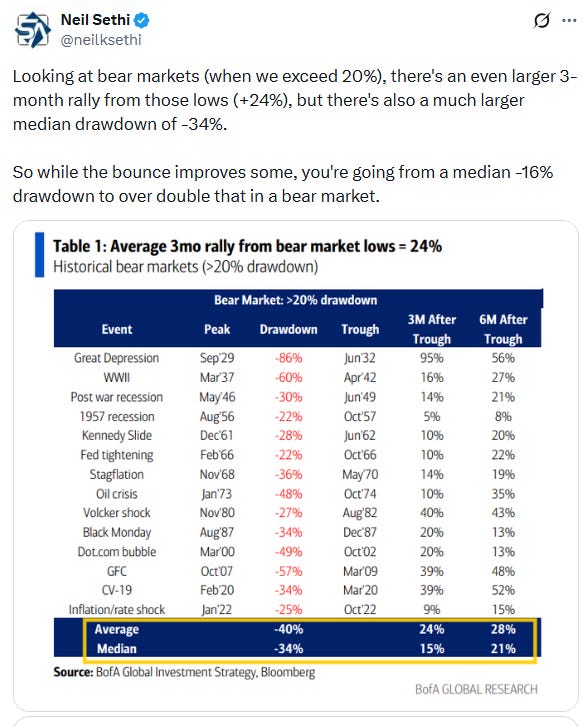

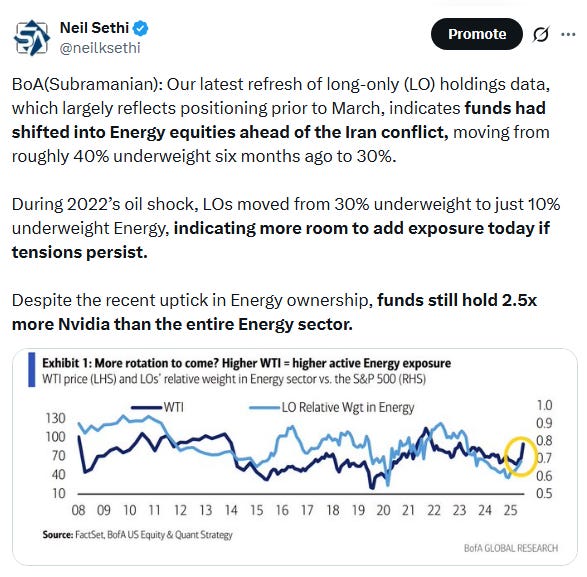

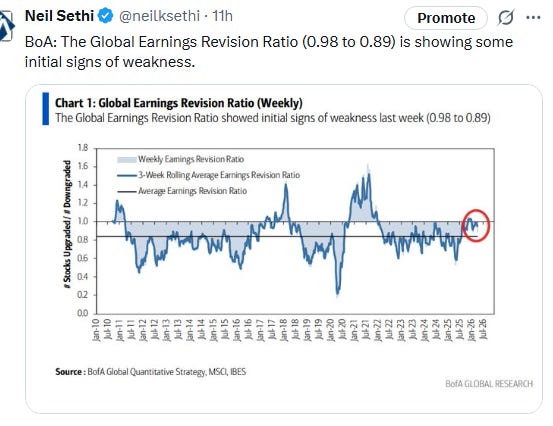

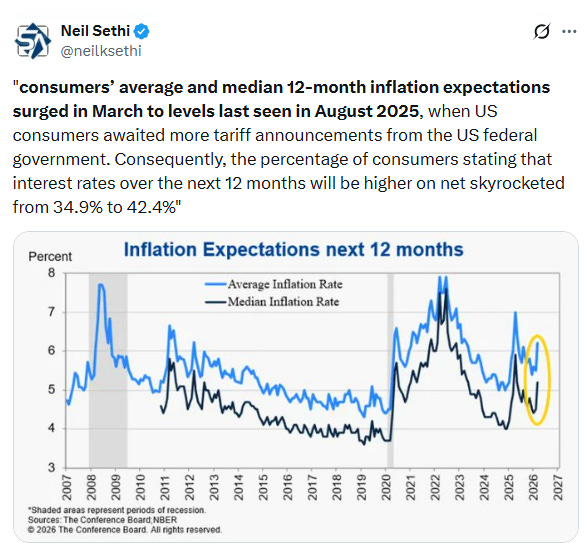

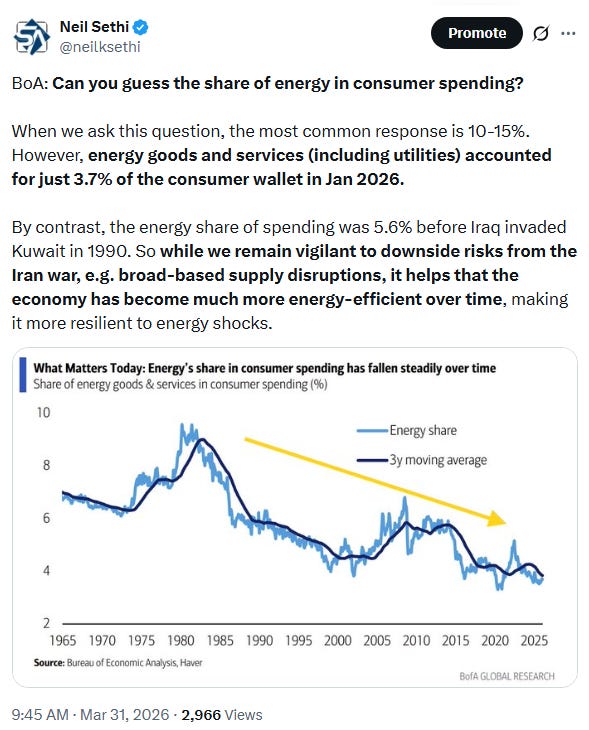

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

The Technology Select Sector SPDR Fund (XLK) closed more than 4% higher. Nvidia climbed 5.6%, and Microsoft advanced 3.1%. Airlines jumped while energy producers slipped.

Stocks making the biggest moves after hours from CNBC:

Corporate news from BBG:

Nvidia Corp. is taking a $2 billion stake in Marvell Technology Inc. and is opening up its system to allow Marvell to integrate custom AI chips and networking equipment on the platform.

CoreWeave Inc. has raised $8.5 billion from a group of banks and investors to help finance an expansion of its cloud computing capacity.

Eli Lilly & Co. agreed to buy sleep drugmaker Centessa Pharmaceuticals Plc in a deal worth up to $7.8 billion, a sign the weight-loss medication giant is looking to bulk up its treatment pipeline for other conditions.

Biogen Inc. has agreed to acquire Apellis Pharmaceuticals Inc. for $5.6 billion, expanding its treatments in immunology and rare diseases.

Unilever Plc agreed to combine its food business with spice maker McCormick & Co. in a $44.8 billion deal that will create a global seasonings, sauces and condiments company.

Mid-day movers from CNBC:

In US economic data:

Substack articles

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X