Markets Update - 3/3/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with lots of charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!),

Link to posts - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog. Also please note that I do often add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

Finally, if you see an error (a chart or text wasn’t updated, etc.), PLEASE put a note in the comments section so I can fix it.

US equity indices opened trading Monday materially lower (at one point hitting the least since late Nov) as the conflict with Iran continues with no end in sight, heightening fears of a lengthy disruption to energy markets and a surge in inflation. President Donald Trump overnight insisted there was no fixed timeline, while Secretary of State Marco Rubio said “the hardest hits are yet to come.” President Trump has earlier warned that the conflict could continue for more than four weeks.

Brent crude rose 7% and briefly topped $85 a barrel for the first time since July 2024. WTI crude jumped 8% to above $77 a barrel after a 6% jump as well on Monday. Both would finish lower but still the highest since the spike in June during the previous Iran war. European gas would add 28% to Monday’s gains at one point up 100% from Friday’s levels as the world’s largest LNG export plant in Qatar stayed shut. Ten-year Treasury yields climbed six basis points to 4.10% and expectations for Federal Reserve cuts continue to be pulled back nearing the lowest this year.

The pressure was broader Tuesday extending to every sector of the market (none would finish green). Nvidia Corp. fell 2.8% in US premarket trading as officials consider capping the number of artificial-intelligence accelerators the company can export to any single Chinese customer (it would halve that loss though). Fellow chip supplier Broadcom was also down nearly 2%, while shares of Blackstone fell 5% (it would finish -3.8%) after the Financial Times reported that its private credit fund saw $1.7 billion in net outflows in the first quarter.

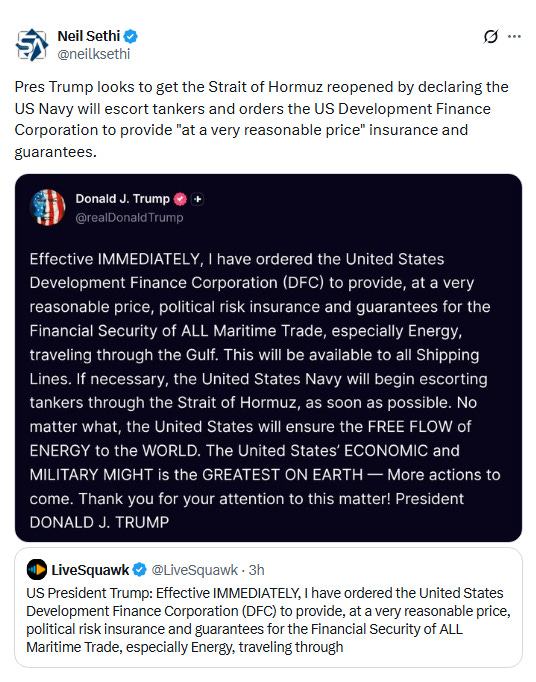

Towards the end of the session, Pres Trump indicated the US Navy would escort tankers through the Strait of Hormuz and a US department would assist with insurance and guarantees (see post below).

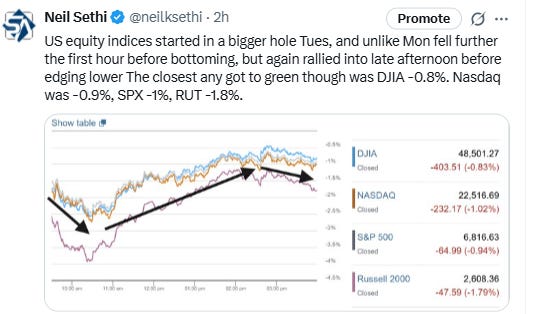

After starting in a bigger hole Tuesday, US equity indices fell further the first hour before bottoming. Like Monday they rallied into late afternoon before edging lower, but unlike Monday the closest any got to green was the DJIA’s -0.8%. Nasdaq was -0.9%, SPX -1%, RUT -1.8%.

Elsewhere, as noted bond yields were up, while the dollar hit the highs of the year before falling back. Crude saw continued gains, at one point touching the highest levels in a year, and natgas moved back over $3. Gold, copper, and bitcoin though all were lower (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was -0.9%, the equal weighted S&P 500 index (SPXEW) -1.2%, Nasdaq Composite -1.0% (and the top 100 Nasdaq stocks (NDX) -1.1%), the SOXX semiconductor index -0.9%, and the Russell 2000 (RUT) -1.8%.

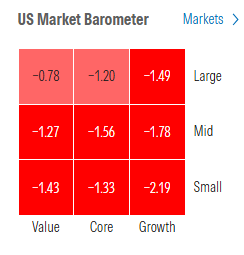

Morningstar style box all red with value styles outperforming.

Market commentary:

“There was definitely a degree of complacency in US equity market valuations at close yesterday, and a perception that military conflict in Iran was a self-contained geopolitical risk,” said Emma Moriarty, portfolio manager at CG Asset Management. “Comments from the White House yesterday suggest a will to make the conflict more durable and to do whatever it takes.”

“Markets are repricing for the risk of a more extended Iran war,” said Krishna Guha at Evercore. “The duration of higher oil and gas is key.”

“I do think the possibility of a more prolonged mission can weigh on markets for the next several weeks,” Jeffrey O’Connor, U.S. head of equity market structure at Liquidnet, said to CNBC, citing the possibility of high oil prices becoming sticky and investors having to navigate future moves in inflation, yields and interest rate cut expectations. “Historically, the U.S. market is able to overlook a geopolitical shock like this, but that said, the Strait of Hormuz is closed,” he continued. Given that about 20% of the world’s oil consumption moves through the Strait, O’Connor added that its continued closure “can’t be overlooked.”

“For now, markets are trading headline to headline,” said Fawad Razaqzada at Forex.com. “Much will depend on whether tensions stabilize — or whether this proves to be the start of a more prolonged disruption to global supply.”

“After initially taking the Middle East war in stride on Monday, market anxiety ratcheted higher overnight amid concerns that a decapitated and leader-less Iranian government and military will execute a prolonged retaliatory response aimed at sowing chaos throughout the region by targeting key economic and energy infrastructure for weeks to come,” said Adam Crisafulli of Vital Knowledge in a note. “While the US and Israeli militaries have complete dominance in the region, they can’t knock out every cheap missile and drone fired off by Iran, especially since interceptor stockpiles are rapidly depleting.” “Energy prices are surging further (especially European gas), placing upward pressure on global borrowing costs,” added Crisafulli

“I was surprised we didn’t see this selloff yesterday,” said Nancy Tengler at Laffer Tengler Investment. “What the market is reacting to today is that this is going to be more prolonged than anticipated, but I don’t think that’s true.”

While inflation and energy prices are probably going to be higher and some earnings are going to be lower because of a strong dollar, she noted volatility is still a buying opportunity. “I wouldn’t jump in here today. You do have to let these things settle and it could take a couple of weeks,” Tengler said, adding she doesn’t think this is the start of a bear market.

“Sentiment is gradually drifting from an orderly selloff to a panic selloff,” said Joachim Klement, head of strategy at Panmure Liberum. “We are now starting to see overreaction by investors. This increased panic selling may last for a little longer, but will eventually open up buying opportunities.”

“Geopolitics is difficult to trade,” wrote Mohit Kumar, chief strategist for Europe at Jefferies. “We are happy to be overweight cash right now, waiting for more clarity and then use market moves to buy the dip.”

“The Iran strikes were several days ago and the stock market is still grappling with some aftershocks, as investors digest the news and assess whether Monday’s muted initial stock declines and dramatic recovery was justified,” Robert Edwards, chief investment officer at Edwards Asset Management, wrote in an email. Conflict in the Middle East may continue, but Edwards noted that stocks tend to move on from geopolitical events. He projected that the S&P 500 would still hit 7,700 by the end of the year, implying that the war won’t affect the bull market in the long term.

Barring a prolonged disruption of oil supplies, the conflict is unlikely to end the cyclical stock bull market by itself, according to Ed Clissold and Thanh Nguyen at Ned Davis Research, which has tracked crisis events for decades.

The market has tended to decline during the event itself, by an average of 7% and a median of 3%, they noted. Once the crisis has passed, the market has recovered within a few months, on average. The exceptions have been when a crisis damages the economy.

Generally speaking, military actions cause a short-term disruption in markets, but as long as the economic damage is limited, they fully recover once there is more clarity in the scope of the intervention, according to Chris Zaccarelli at Northlight Asset Management. “It is too soon to tell how events will unfold this month, but we are looking for opportunities to present themselves if traders overreact and throw the baby out with the bathwater,” he said.

“The massive flattening of the global yield curves has only just begun. Bonds are just waking up to the reality that the war in the Middle East will stoke inflation all over again. Front-end maturities are taking the biggest hit thanks to a more hawkish re-pricing of central bank trajectories.” — Ven Ram, macro strategist.

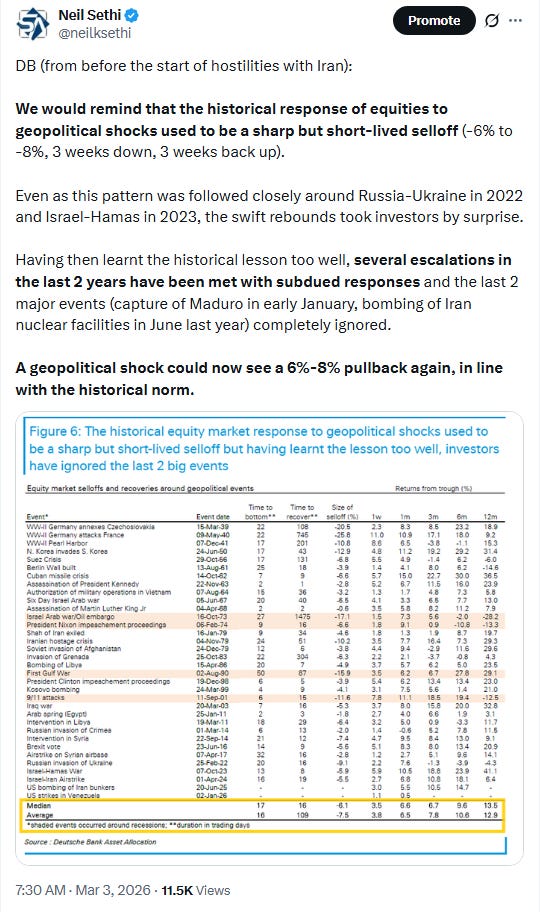

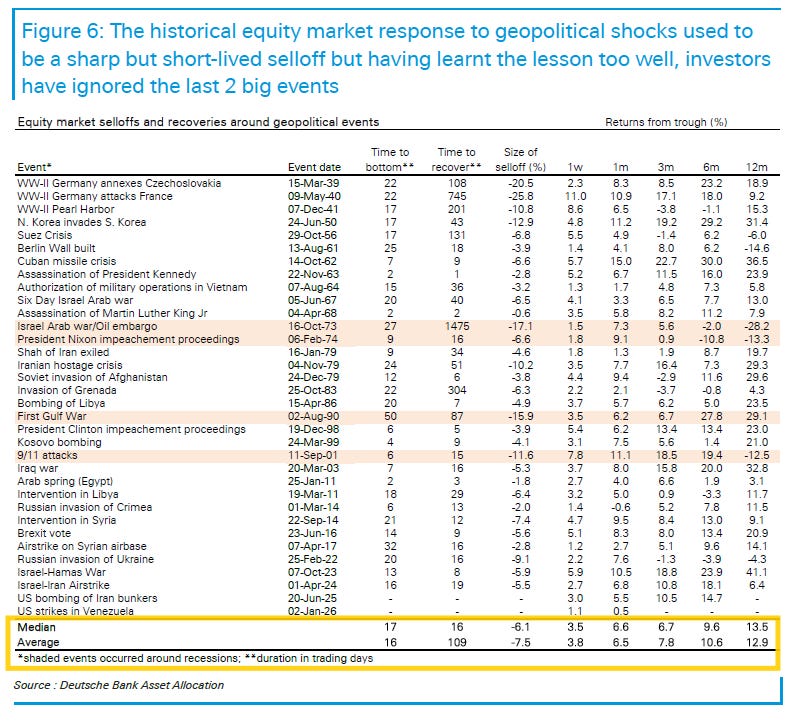

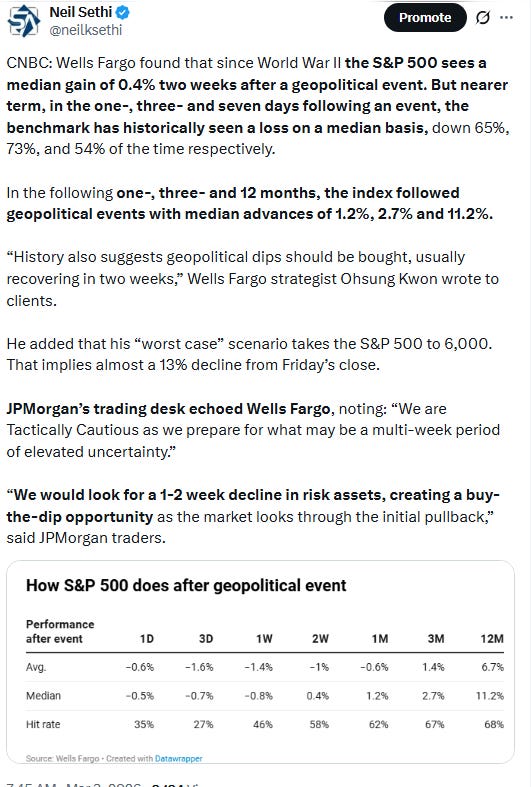

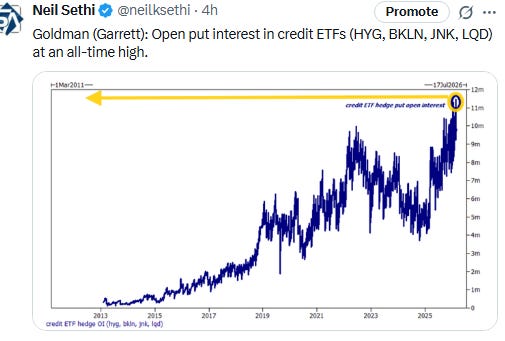

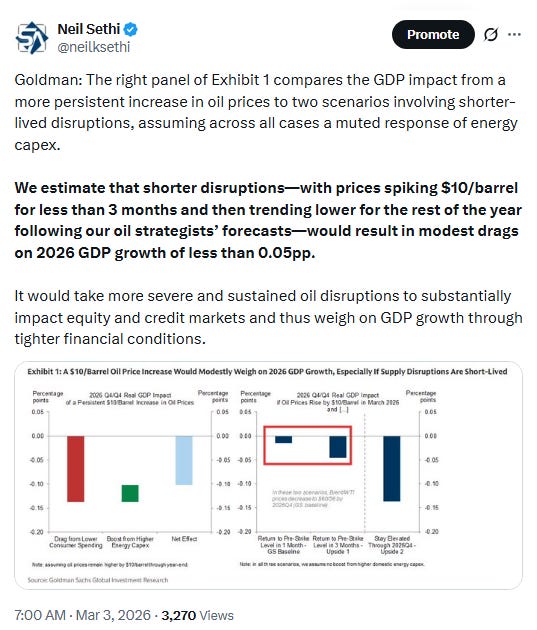

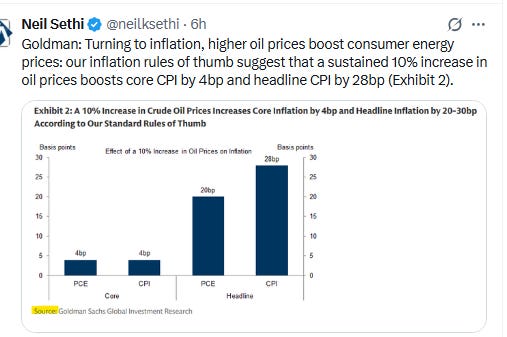

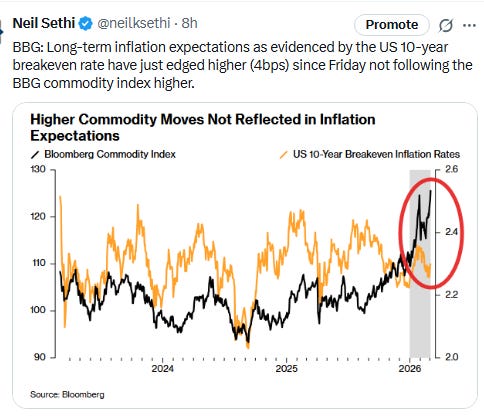

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

Corporate news from BBG:

CrowdStrike Holdings Inc. projected quarterly sales that were roughly in line with estimates.

Target Corp. forecast better-than-expected profit for the full year.

Best Buy Co. reported profit for the holiday-shopping season that beat estimates.

Apple Inc. updated the MacBook Air and MacBook Pro, adding faster processors and raising prices.

Mid-day movers from CNBC:

In US economic data:

Substack articles.

None today, several tomorrow.

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X