Markets Update - 3/6/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with lots of charts!

To subscribe to these summaries, click below!

To invite others to check it out (sharing is caring!), here’s the button:

Link to posts on X - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog. Also please note that I do sometimes add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

Finally, if you see an error (a chart or text wasn’t updated, etc.), always appreciate a note in the comments section or email so I can fix it.

US equity indices opened trading Friday down sharply taking a leg lower after nonfarm payrolls fell by 92,000 in February, a sharp contrast from the downwardly revised January gain of 126,000 and far below the growth of 50,000 that economists on average expected for the month. The unemployment rate also rose to 4.4% from 4.3%. Separately retail sales came in around expectations with a weather influenced drop led by declines in autos and gasoline (links are to my blog posts with more details).

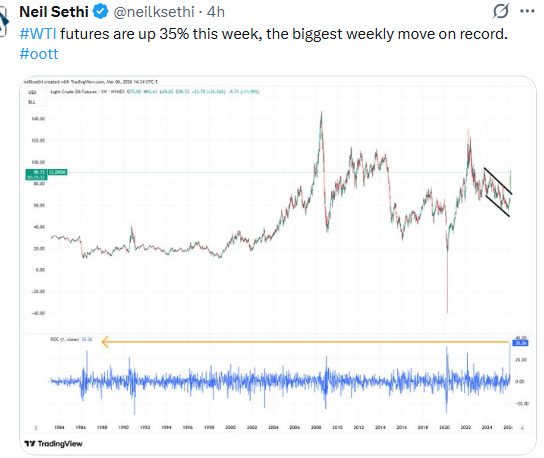

Also crude oil was surging (and would continue to surge as the day progressed to cap its biggest one-week percentage increase on record) after Pres Trump said he would accept only “unconditional surrender” from Iran while WSJ reported that Kuwait is slowing production as inventories have reached capacity. Earlier Qatar’s energy minister told The Financial Times that Gulf energy producers may need to call force majeure in the coming days, shutting down production in a move that could send oil to $150 a barrel. The conflict in the Middle East could “bring down the economies of the world,” he warned.

Adding to pressures was BlackRock Inc. curbing withdrawals from a private-credit fund that sent its shares down 7.7% and impacted the entire Financials sector, while chipmakers dropped as Oracle Corp. and OpenAI scrapped plans to expand an artificial-intelligence data center in Texas.

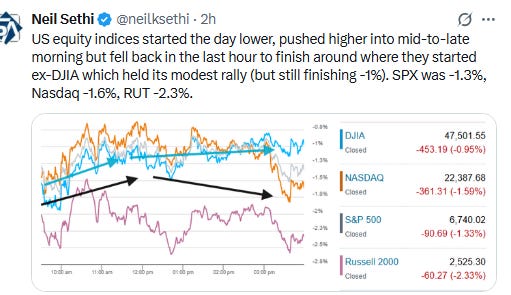

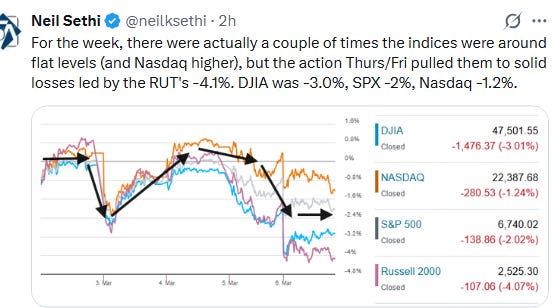

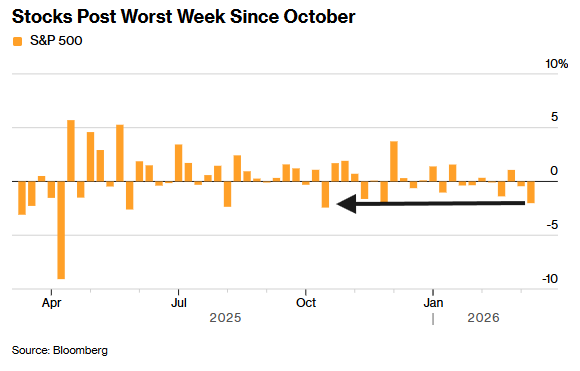

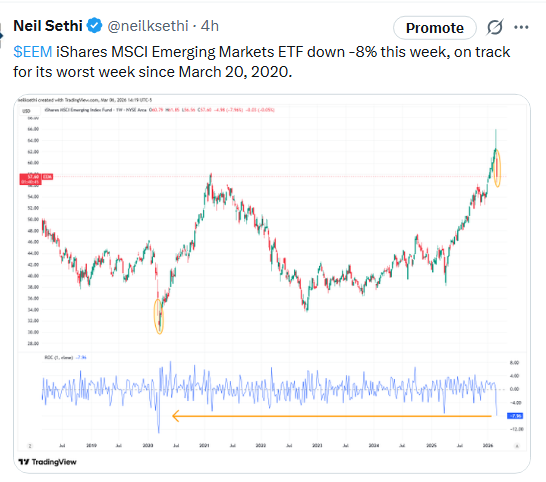

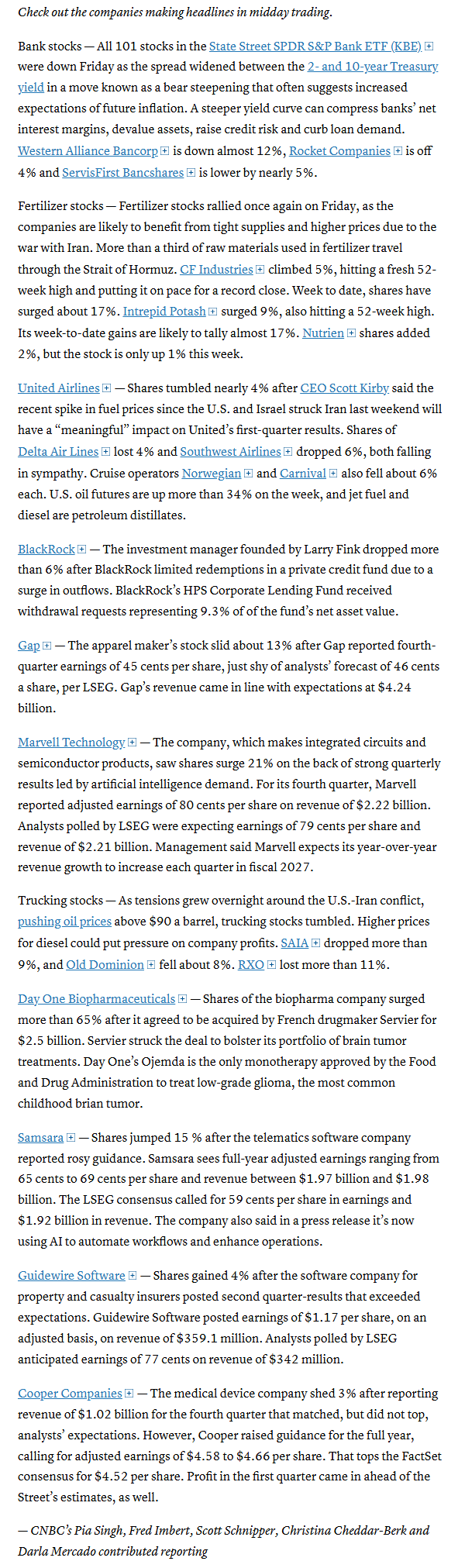

Equity indices would push higher into mid-to-late morning but fell back in the last hour to finish around where they started (except the DJIA which held its modest rally but still finishing -1%). SPX ended Friday -1.3%, Nasdaq -1.6%, and Russell 2000 (RUT) -2.3%. For the week, there were actually a couple of times the indices were around flat levels (and Nasdaq higher), but the action Thurs/Fri pulled them to solid losses led by the RUT's -4.1%. DJIA was -3.0%, SPX -2%, Nasdaq -1.2%.

Elsewhere, bond yields were up for a fifth session early as inflation outweighed recession concerns but pulled back later in the day to finish little changed, and the dollar reversed early gains to end solidly lower. Crude as noted was up sharply, and natgas, gold, and copper were also higher. Bitcoin though fell (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was -1.3%, the equal weighted S&P 500 index (SPXEW) -1.3%, Nasdaq Composite -1.6% (and the top 100 Nasdaq stocks (NDX) -1.5%), the SOXX semiconductor index -3.9%, and the Russell 2000 (RUT) -2.3%.

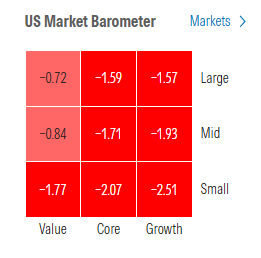

Morningstar style box all red today with larger cap value the only styles not down at least -1%.

Market commentary:

Morgan Stanley chief economist Ellen Zentner has weighed in on Friday’s disappointing jobs data. With oil prices screaming higher, more signs of a weakening labor market could put the Federal Reserve in a difficult position, she said. “Today’s numbers may have put the Fed between a rock and a hard place. Significant weakening in the labor market would support a rate cut, but given the risk that higher-for-longer oil prices could trigger another inflation surge, the Fed may feel compelled to remain on the sidelines,” Zentner said in written commentary shared with MarketWatch.

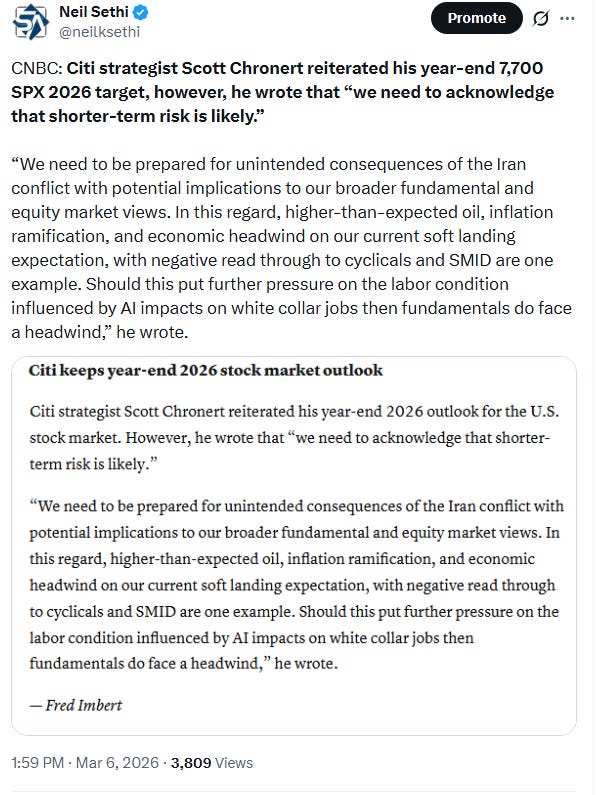

“Indications of labor market weakness are a reminder to the Fed that there could be a price to pay for delaying cuts, although near-term policy remains dictated by the ongoing Middle East conflict,” said Lindsay Rosner, head of multi sector fixed income investing at Goldman Sachs Asset Management, in emailed comments Friday.

“The headline number was very disappointing and will feed worries that the labor market — despite the strong January jobs report — is softening,” said Tim Holland, chief investment officer at Orion. “With energy prices moving higher of late, we wouldn’t be surprised to hear some talk on Wall Street of stagflation — that toxic ’70s mix of slowing growth and rising inflation.”

The market is struggling with a combination of a disappointing jobs report and higher oil prices due to the Iran conflict, said Mark Hackett, chief market strategist at Nationwide, in a phone interview Friday. Investors have shifted to “almost a stagflation mindset,” he said. “Now we have inflation worries and job-market worries.” Still, the U.S. stock market isn’t “necessarily collapsing,” according to Hackett. The S&P 500 on Friday was trading around “the lower end of this really defined trading range that we’ve been” in since late November, he said. “Since then we’ve been in a zig-zag motion sideways.”

“Modest increases in oil prices, even if sustained, have transitory effects on US headline inflation and minimal effects on US core inflation,” said Michael Gapen at Morgan Stanley. “The Fed can look through these increases, but with inflation above target as long as it has been, even modest oil price pressures could delay rate cuts.” Absent second round effects or rising inflation expectations, he believes Fed rate hikes have a high bar. A substantial rise in oil prices could weaken activity, acting like an uncertainty shock and putting rate cuts in play, Gapen noted.

If the labor market keeps losing steam, it becomes a more delicate backdrop — especially with geopolitical uncertainty on the rise and energy prices capable of acting as an added tax at the gas pump, according to Bret Kenwell at eToro.

“This may not change the Fed’s decision this month, but a visibly weakening jobs market is the kind of trend that can pull the Fed in a more dovish direction as 2026 unfolds,” he said. “Regardless of interest rates, a deteriorating jobs market is not what investors want to see — particularly while volatility has already been on the rise.”

“It’s a stagflationary trade right now,” said Jose Torres, market economist at Interactive Brokers. “You have a weaker economy and oil prices at the highest level since 2024, blocking progress for Treasurys. Treasury yields can’t go down with oil prices this high.”

“I’m very cautious,” said Wharton professor emeritus Jeremy Siegel on CNBC’s “Closing Bell.” “If we don’t get some breakthrough over the weekend, I think we’ll see $100 oil next week.”

The bands between the high end and the low end of oil prices “have widened out significantly,” according to Jed Ellerbroek, portfolio manager at Argent Capital Management. Even if you haircut al-Kaabi’s $150-a-barrel projection by 20%, prices are still at levels that are “scary as hell,” he added.

Fed Gov. Christopher Waller was on Bloomberg Television says the spike in gasoline is unlikely to cause sustained inflation. He said it only will matter if the energy costs are sustained higher for a long period of time. Waller points out in 1973, the price of oil quadrupled overnight, and that there were multiple shocks that decade. “It’s more like a one-off event than what we saw in the 1970s,” said Waller, who was one of the President Donald Trump’s candidates to become the next Fed chief.

“Markets remain in risk‑off mode as worries grow about the duration of the conflict and potential disruptions to energy supply,” Angelo Kourkafas, senior global investment strategist at Edward Jones, said. He said that the spike in U.S. oil prices is adding to inflation concerns that could put consumer spending under pressure. To be sure, Kourkafas added, “structural shifts have reduced U.S. vulnerability to oil shocks. Oil would likely need to remain above $100 for an extended period to meaningfully slow economic growth, in our view. The U.S. has been a net exporter of oil since 2019, and the economy is far less energy‑intensive than it once was.”

“The market is trying to reprice risk” this week, as the Iran conflict remains unresolved and investors consider Friday’s surprisingly “weak” U.S. jobs report covering February, said Gary Pzegeo, chief investment officer of CIBC Private Wealth US, in an interview Friday. “The assumption heading into today was that you had a pretty solid economy to fall back on if oil prices were high for a short amount of time,” he said. “Now that’s been thrown into question.”

“This is an anxiety not only about how long the conflict goes on, but what kind of effect it’s going to have on the mix between growth and inflation,” Peter Oppenheimer, chief global equity strategist at Goldman Sachs Group Inc., told Bloomberg TV. “The issue really is 20% of world supplies are going through that channel, it’s obviously very, very significant.”

“Unless there can be some real political breakthrough that leads to a ceasefire, the dollar won’t be ready to resume a decline anytime soon,” ING Bank strategist Chris Turner wrote in a note. “The story will remain one of governments trying to handle the fallout of high energy prices, a negative for bond markets around the world.”

“The dollar has rallied amid the latest downturn in risk sentiment. The poor showing of other perceived safe-haven assets should keep it in the ascendancy. Government bonds are likely off the menu, as long as the market narrative is being driven by rising energy costs and the upside risk to inflation.”

— Conor Cooper, Macro Squawk

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

In individual stock action:

Shares of Royal Caribbean, which tumbled more than 10% this week amid increasing fuel costs, fell again on Friday, dropping 1%. Caterpillar shares, which also suffered this week, were down more than 3% at the end of the session.

Companies making the biggest moves after-hours from CNBC:

None today.

Corporate news from BBG:

Boeing Co. is closing in on one of the largest sales in its history, a 500-aircraft order for 737 Max jets set to be unveiled when President Donald Trump travels to Beijing for his first state visit to China since 2017, people familiar with the matter said.

Marvell Technology Inc. soared after delivering a bullish sales outlook, saying that data-center demand was growing even faster than anticipated.

Gap Inc. sank after reporting sales and profit that came in slightly below expectations as two of its apparel chains underperformed.

Mid-day movers from CNBC:

In US economic data:

Substack articles.

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X