Markets Update - 4/13/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with charts!

Quick Summary:

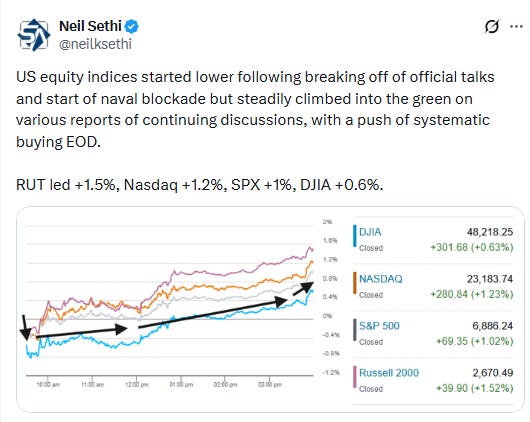

Equities started the day lower pressured by the breakoff of direct negotiations with Iran over the weekend and start of a US blockade in the Strait of Hormuz but climbed throughout the session on scattered indications (including from Pres Trump) that negotiations were continuing with Iran to finish firmly higher.

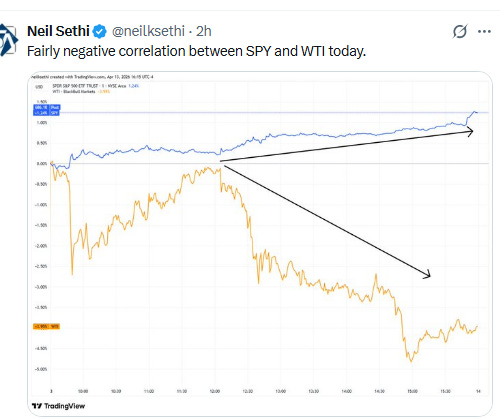

Crude oil would spike early but pare it gains helping the rally which was led by Financials and growth stocks.

In US economic data existing home sales fell to a 9-month low as the National Association of Realtors slashed their 2026 sales forecasts.

US equity indices opened trading this week under some moderate pressure but with losses much less than many expected after the ending of direct talks on Saturday which was followed by President Trump’s Sunday morning announcement of a blockade of Iranian ships (as well as any ships that have paid a toll to Iran) as covered in the Week Ahead which saw oil prices trading up sharply. Other overnight updates were covered in the morning blog post.

But equities would find their footing relatively quickly on a succession of headlines (even if some turned out later to be less than they appeared) that talks were continuing and gained some steam after President Trump said “We’ve been called this morning by the right people, the appropriate people [in Iran], and they want to work a deal.” “Right now we have a blockade. They’re doing no business,” Trump said.

Indices would finish solidly in the green, with a late session push from the systematic flows noted in the Week Ahead, led by the small cap Russell 2000 +1.5%,. The Nasdaq would gain +1.2%, S&P 500 +1%, Dow Jones Industrial Average +0.6%. It was the 9th consecutive positive session for the Nasdaq, the longest streak since 2023.

Elsewhere, bond yields edged lower despite crude prices going the opposite direction, while the dollar reversed from early gains to also finish down as did gold, bitcoin, and US natural gas (the latter two reversing from early gains). . Copper saw a solid advance (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was +1.0%, the equal weighted S&P 500 index (SPXEW) +1.2%, Nasdaq Composite +1.2% (and the top 100 Nasdaq stocks (NDX) +1.1%, the SOX semiconductor index +1.7% (up over 26% the last nine sessions to an ATH (post below)), and the Russell 2000 (RUT) +1.5%.

Some market commentary:

“Investors are now back to the drawing board trying to reassess the fair value of stocks now that it’s clear that there is no end in sight to the conflict in the Middle East,” said Clark Bellin, president and chief investment officer at Bellwether Wealth. “The Strait of Hormuz is key for oil prices and overall market sentiment, and it’s clear that there will be more saber rattling over this waterway between the U.S. and Iran this week.”

“There’s a belief that a lot of this is negotiation tactics,” said Billy Leung, investment strategist at Global X ETFs, referring to Trump’s announcement. “Markets have reached peak uncertainty. The reaction function is no longer as extreme as before.”

“I was expecting much worse both for the equity market and oil prices this morning,” said Mary-Sol Michel, director of discretionary portfolio management at Swiss Life Banque Privée. “The market sees the blockade as a negotiation tool, but nonetheless, I feel the impact on stocks is quite modest.”

“The oil retracement, in combination with bearish positioning, has fueled the equity rebound,” said JonesTrading Chief Market Strategist Michael O’Rourke. “Overall, investors doubt the veracity of headlines, but they don’t want to be caught on the wrong side of them either.”

“Time is playing against markets as each day that goes by with oil prices this high weighs on global growth and pushes inflation,” said Gilles Guibout, head of European equities at BNP Paribas Asset Management. “It’s difficult to see how markets could stage a sustainable rebound without a sustainable solution to this crisis.”

Tech stocks were outperforming the broader market on Monday, as “weakening economic fundamentals weigh on buyer engagement in most of the other equity sectors,” according to José Torres, senior economist at Interactive Brokers. “Participants want to be shareholders of companies that can weather elevated interest rates, climbing oil prices and a cyclical slowdown,” Torres wrote in a Monday note. Big Tech stocks met such critierias, he added.

Strategists at Trivariate Research led by Adam Parker argue the market is trading on fundamentals, just not those related to current-day earnings.

“Our view is that perhaps the market is trading on fundamentals, i.e. a distribution of earnings outcomes in 2030, not 2026,” they say. “Perhaps software is down because its 2030 sales outcomes are skewed to the downside. Perhaps industrials are expensive because many over-indexes toward end-markets that will likely grow above global GDP for the rest of the decade. Perhaps healthcare is down because government spending will eventually be arrested,” they say. They say to be underweight software, market-weight industrials and overweight healthcare.

The question is whether “this upcoming earnings season can be enough of a catalyst to dismantle the close link between stocks and oil, as corporate earnings are what traditionally drive stock prices,” wrote Clark Bellin, president and chief investment officer at Bellwether Wealth.