Markets Update - 4/7/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with charts!

Similar to the Week Ahead, I am reworking the nightly Markets Update to make it more streamlined and hopefully more useful. I’m making this week open to all subscribers so you can see the format and give it a try. As always, feedback is welcome.

Quick Summary:

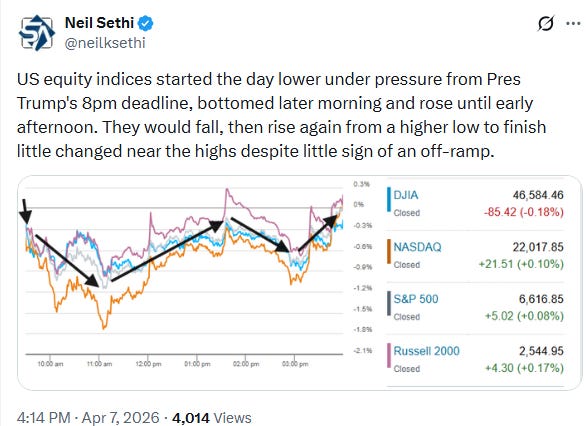

Equities again fought through a choppy session to end little changed with another day of shifting headlines around whether or not President Trump would follow through on his promise to attack Iran energy and infrastructure starting at 8pm this evening.

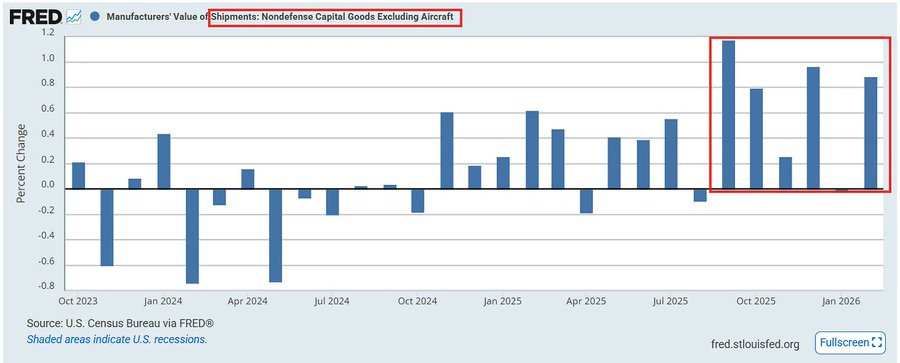

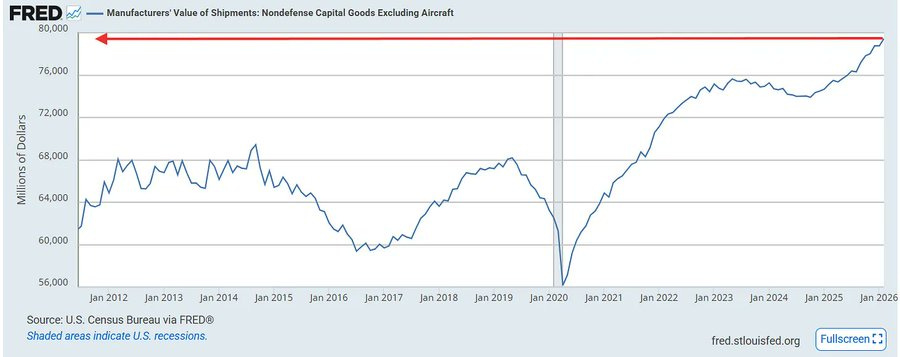

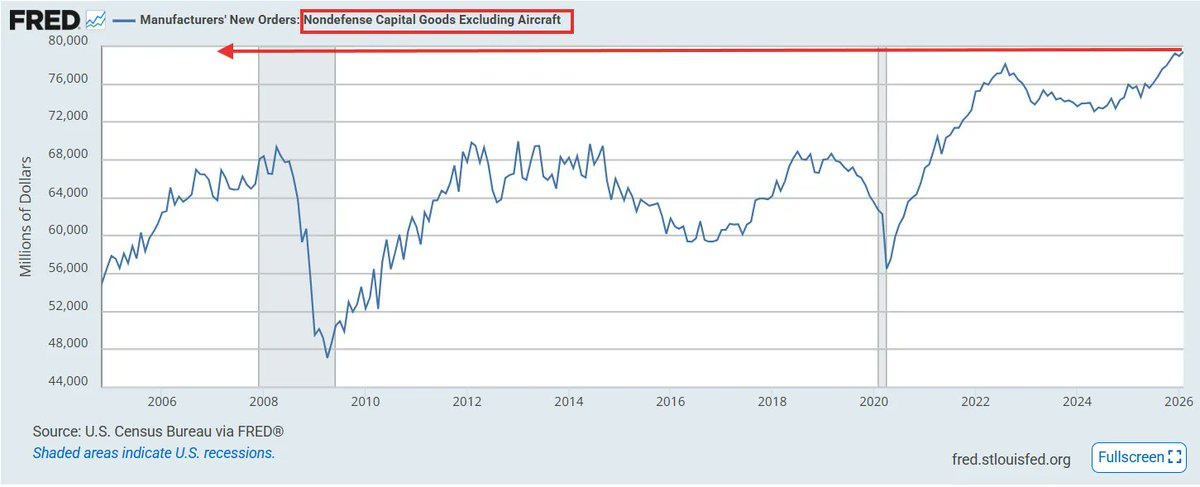

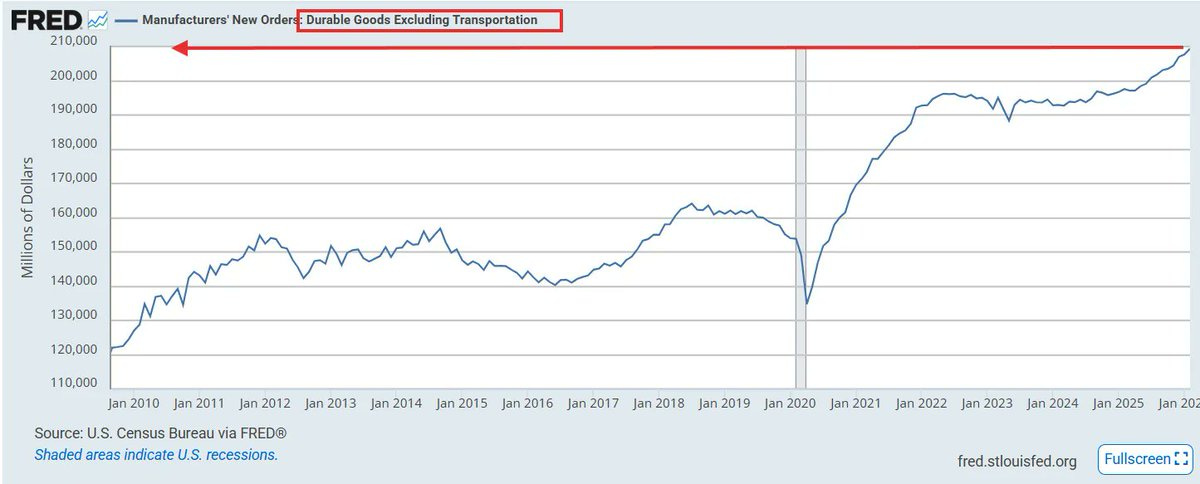

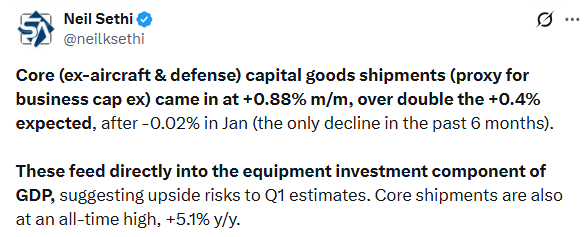

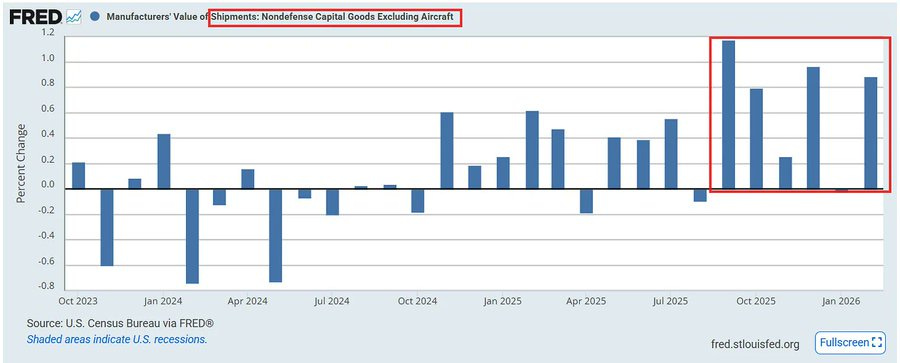

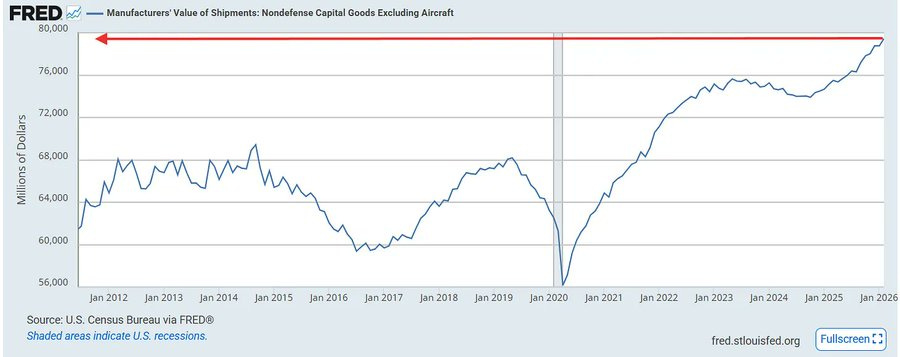

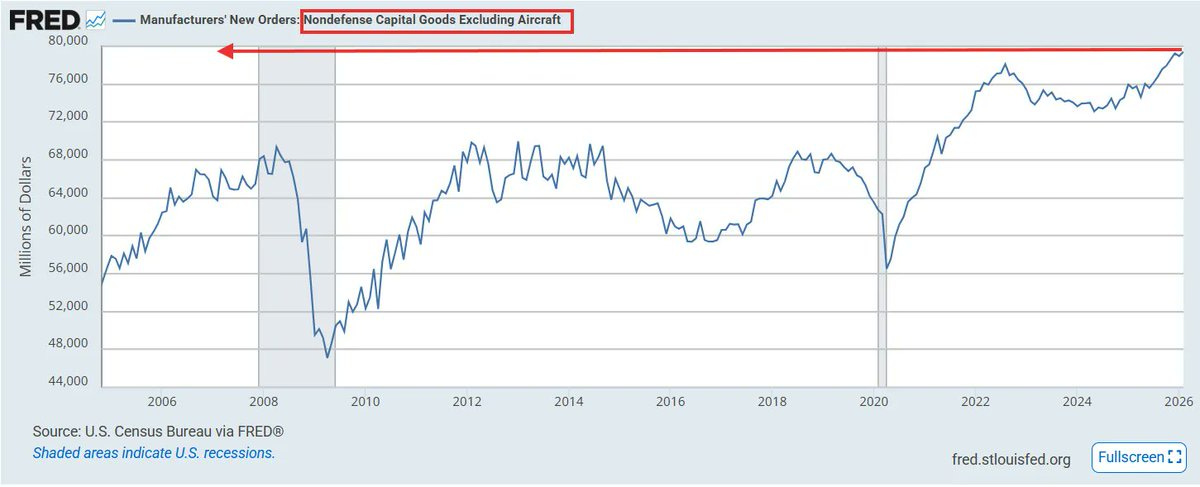

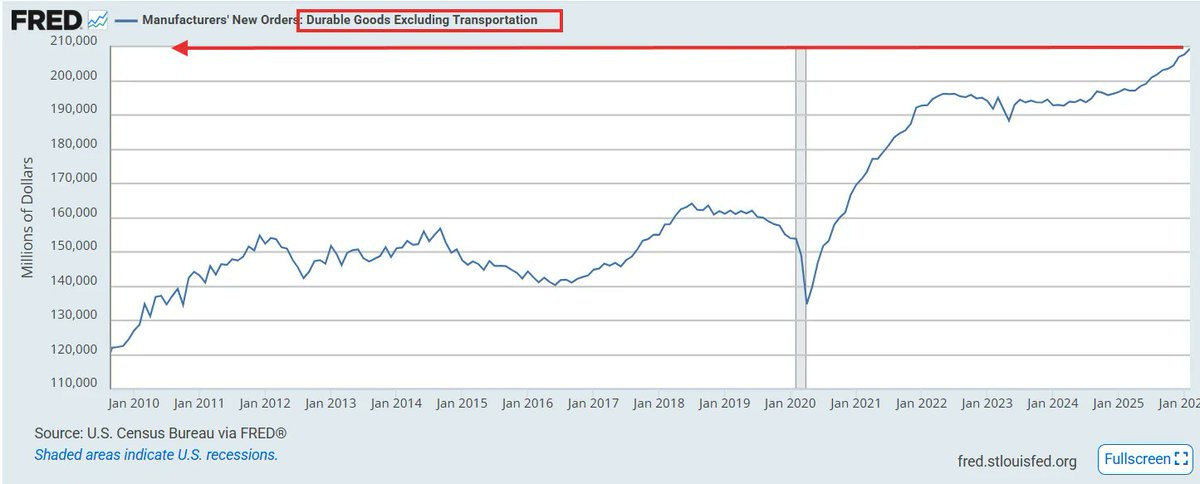

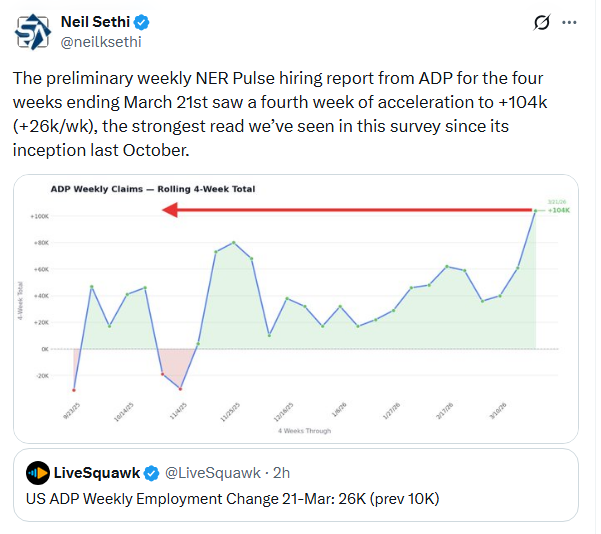

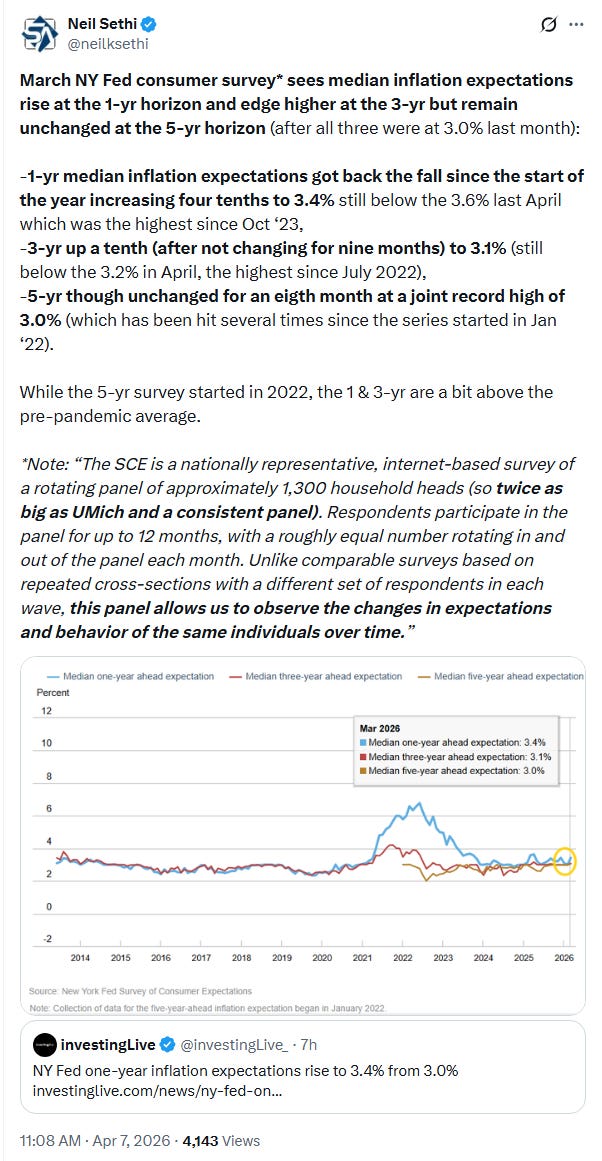

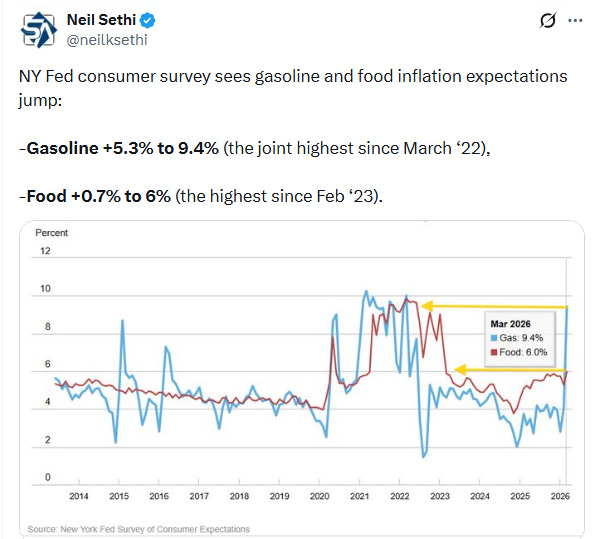

In US economic data we got a durable goods (goods lasting more than 3 years) report showing very solid core business spending, ADP’s weekly employment estimate with the strongest read to date (since inception in October), and the NY Fed’s consumer survey showing modest changes outside of a jump in short-term inflation expectations fueled by gasoline and food prices.

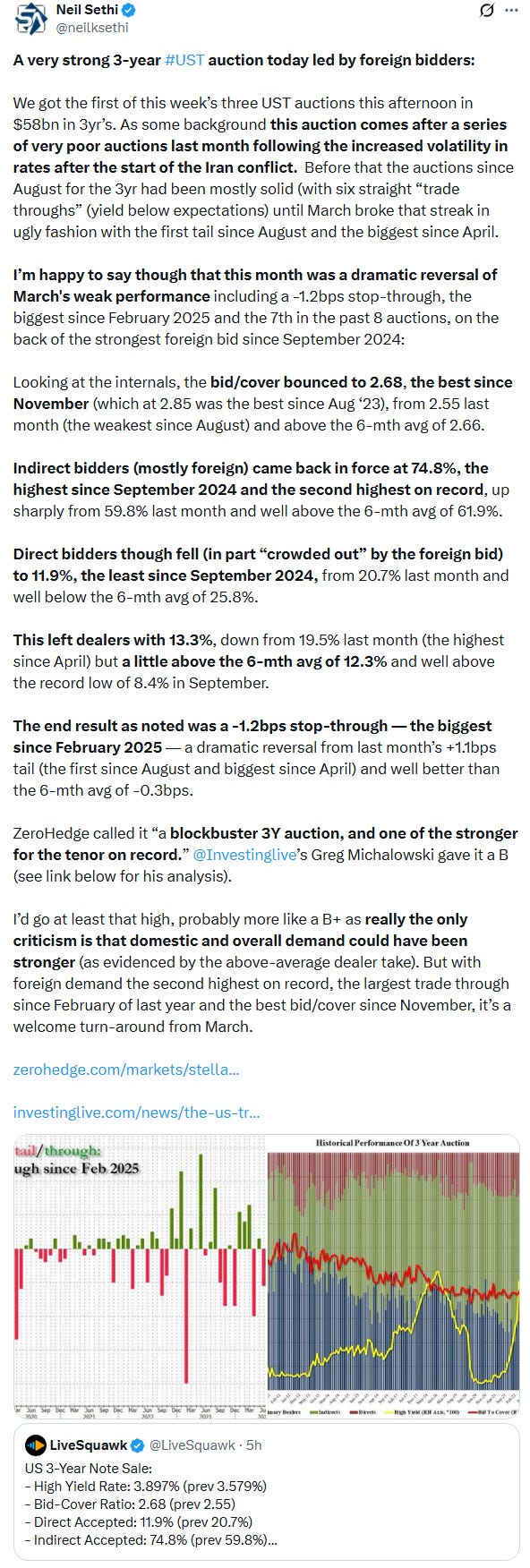

The 3-year Treasury auction today showed a return to foreign demand for US Treasuries that had softened in March.

US equity indices opened trading Tuesday modestly lower as they await President Trump’s 8pm ET deadline tonight for Iran to agree to a deal or face new attacks including on bridges and power plants. Pre-market developments were detailed in the morning blogpost including Pres Trump’s statement that “A whole civilization will die tonight, never to be brought back again. I don’t want that to happen, but it probably will,” but also leaving open the possibility of a pivot away saying “now that we have Complete and Total Regime Change, where different, smarter, and less radicalized minds prevail, maybe something revolutionarily wonderful can happen, WHO KNOWS?”.

As they did Monday, equities seesawed as they evaluated headlines including a report from the Wall Street Journal that Iran cut off lines of direct communication ahead of the deadline and Iran later threatened a list of regional energy infrastructure in the event President Trump followed through with his threats. Towards the end of the session, Pakistani Prime Minister Shehbaz Sharif requested that President Trump extend the deadline for two weeks and that Iran open the Strait of Hormuz for a corresponding period of two weeks. Pakistan is a key mediator in the negotiations. “I can’t tell you, because right now we’re in heated negotiations,” Trump said in a telephone interview with Fox News when asked about the Pakistani request.

In individual equities, Alphabet (GOOG 303.93, +6.27, +2.11%) was a mega-cap standout after announcing a long-term partnership with Broadcom (AVGO 333.97, +19.54, +6.21%), in which Broadcom will work to develop and supply custom Tensor Processing Units (TPUs) to Google.

Elsewhere, managed care names such as UnitedHealth (UNH 307.73, +26.37, +9.37%) and Humana (HUM 197.15, +14.50, +7.94%) rallied after the Centers for Medicare & Medicaid Services released its reimbursement rates which came in meaningfully better than expected. But the consumer staples (-1.8%) and consumer discretionary (-0.9%) sectors were today’s worst performers, with particular weakness across specialty stores and homebuilders.

Elsewhere, bond yields and crude prices fell back as did the dollar, copper and bitcoin. US natural gas prices were higher while gold futures were unchanged (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was +0.1%, the equal weighted S&P 500 index (SPXEW) -0.3%, Nasdaq Composite +0.1% (and the top 100 Nasdaq stocks (NDX) +0.1%, the SOXX semiconductor index +1.1% (up 11% the last four sessions), and the Russell 2000 (RUT) +0.2%.

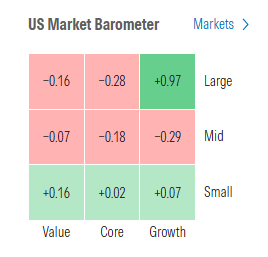

Morningstar style box was mixed with just large growth and small caps in the green .

Some market commentary:

“Hope remains that Trump’s brinkmanship will produce a last-minute agreement to resolve the situation, or perhaps another postponement of the threat to destroy Iran’s domestic infrastructure,” said veteran strategist Louis Navellier.

“The real issue is that even if there’s a climbdown, or TACO, the risk environment has already shifted in a way that leaves markets exposed to sharp, disorderly moves,” warns deVere Group Chief Executive Nigel Green.

“Investors are likely to remain on edge and markets unable to establish trends, probably until there is a clear outcome later this evening: a deal, the US-Israeli strikes intensify, or Iran’s retaliation becomes escalatory instead of proportional,” said Paul Christopher at Wells Fargo Investment Institute.

“As the deadline approaches, [Trump] wants to apply even more pressure to get them across the finish line,” Brian Jacobsen, chief economic strategist at Annex Wealth Management. The headline-driven sharp swings in the markets, however, have created opportunities for investors to reshuffle their portfolios for longer-term returns, Jacobsen said. “When geopolitical worries hit the market, it tends to move prices indiscriminately. That’s when a discriminating investor can upgrade their portfolio.” Jacobsen pointed to “decent entry points” in companies across industries, including utilities, financials, industrials, and technology, while naming defense and energy companies as the “first-order” beneficiaries in the wake of the conflict.

“Why are we not optimistic for a deal today? The U.S. and Gulf states will not accept the idea of the Strait being controlled by Iran. But Tehran’s calculus has shifted. Controlling the Strait of Hormuz is something Iran wants to keep no matter what the outcome of the war,” Jordan Rochester, head of FICC strategy EMEA at Mizuho, wrote in a note.

“Bigger picture, you’re starting to see equity investors get concerned about a longer-term enduring elevation in oil prices as a result of supply disruptions,” Gina Martin Adams, chief market strategist at HB Wealth told MarketWatch.

Ulrike Hoffmann-Burchardi, UBS CIO and global head of equities, wrote that markets this week are paying close attention to Trump’s 8:00 p.m. deadline Tuesday night for Iran, and that the bank has been advising traders to de-risk portfolios as energy prices remain high. “We have become more cautious on equity markets that are highly sensitive to disruptions to energy supplies, including Europe, the Eurozone, and India,” he wrote. However, investors shouldn’t get out of risky assets entirely, Hoffmann-Burchardi reminded. “Recent corporate and economic developments have also served as a reminder of why investors should remain engaged in markets, given the potential positives for risk assets over the medium and longer term.”

“The oil market is still indicating stress, with both WTI and Brent remaining elevated and rallying further today. Typically, commodity markets are more pessimistic than stocks. Commodities, and commodity traders, are likely to have a much better read on just how disruptive and long-lasting the damage to energy facilities and the (semi) blockade on the Hormuz Strait will be.”

— Simon White, macro strategist

“Everybody was betting that it’s going to be short term and I think the market still is, and frankly, I still am too,” Barbara Doran, founder and CEO of BD8 Capital Partners, said on CNBC’s “Closing Bell: Overtime” on Monday afternoon. “The market will say, ‘OK, it’s going to be over soon,’ and then we can resume where we’re going, which is starting the year very bullish. And now you have also continued fiscal stimulus from the defense spending.”

“We think this conflict could drive three lasting effects across the market: a renewed focus on energy security, a pivot toward diversification of energy sources, and a reshuffling of market share toward more stable producers,” Kenny Zhu, associate vice president of energy and commodities Research at Global X, wrote in a note. He added that the Iran war could also push investors to pay more attention to alternative-energy sources, such as nuclear power.

Some posts from today:

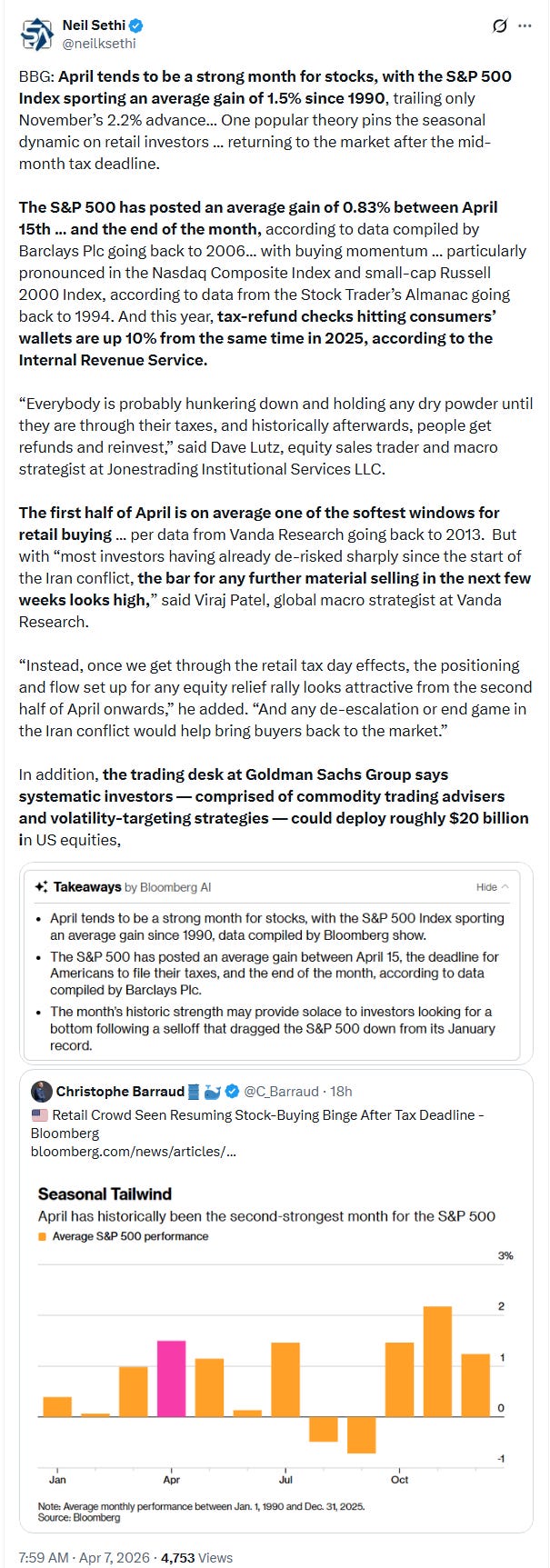

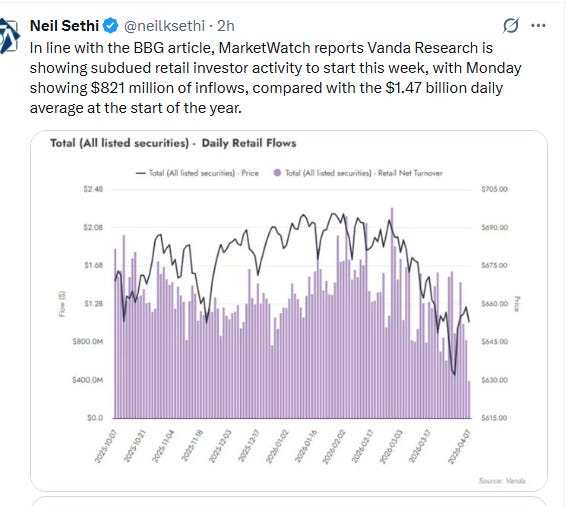

Retail buying tends to be subdued to start April but pick up after Tax Day:

UBS cuts its SPX targets:

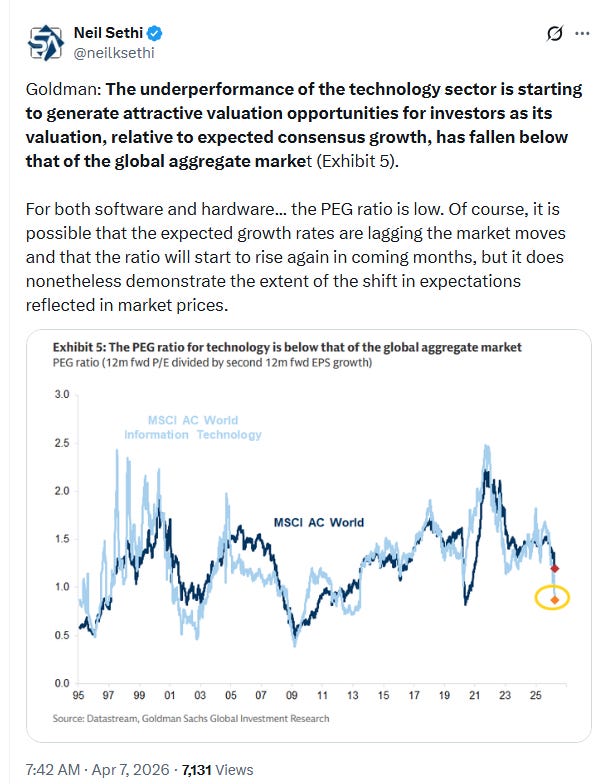

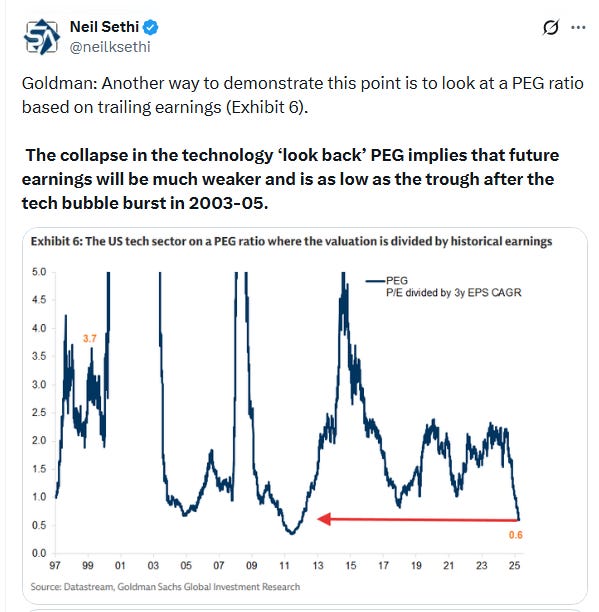

Goldman says tech stocks are a good value:

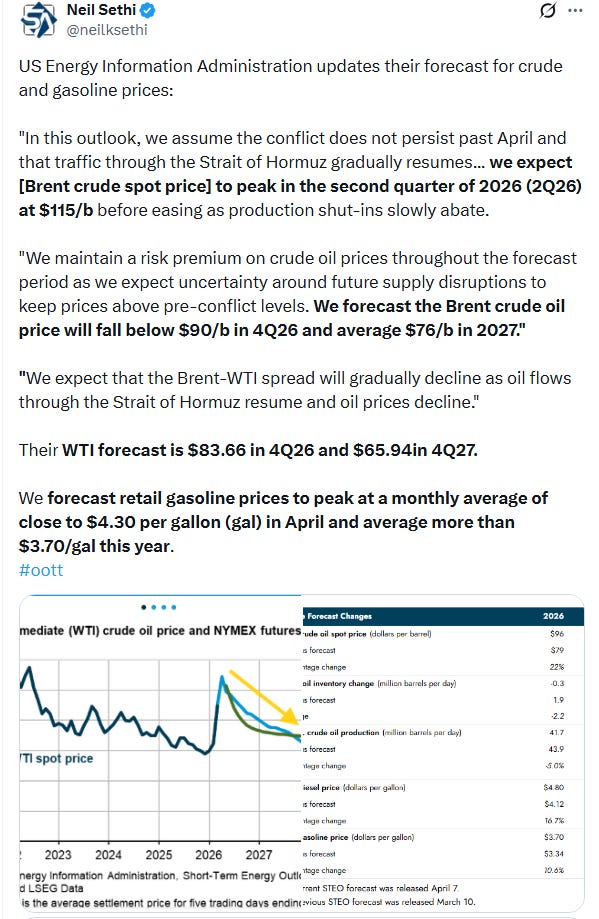

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

Corporate news from BBG:

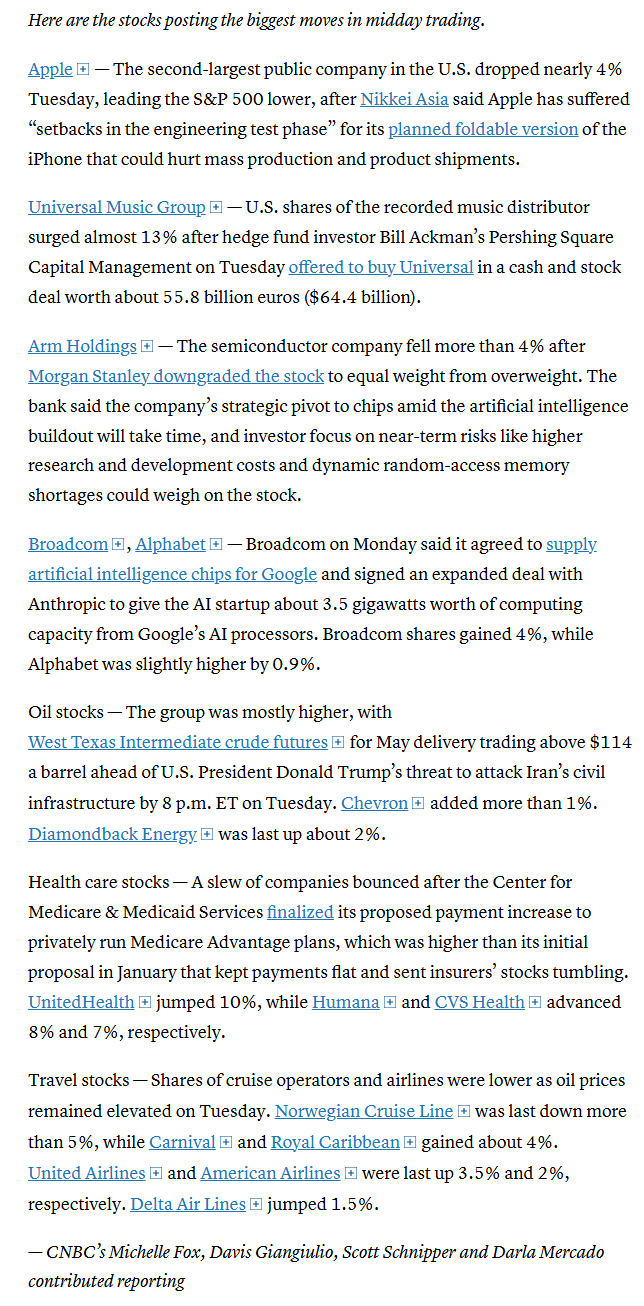

Apple Inc.’s first foldable phone is on track to arrive during the company’s normal iPhone launch period later this year, people with knowledge of the matter said, rebutting concerns about major manufacturing snags.

Intel Corp. is joining Elon Musk’s long-shot effort to develop semiconductors for Tesla Inc., SpaceX and xAI, marking a surprising twist in the chipmaker’s comeback bid.

Pacific Investment Management Co. is in talks with Bank of America Corp. to help provide roughly $14 billion of debt financing to build a massive Oracle Corp. data center in Michigan, according to people familiar with the matter.

Anthropic PBC said its revenue run rate has now topped $30 billion, up from $9 billion at the end of 2025, and confirmed plans to work with Broadcom Inc. and Google to power its burgeoning operations.

Bill Ackman is pitching a deal for Universal Music Group NV — the record label giant behind celebrities including Taylor Swift and Drake — that he’s claiming will dramatically boost the value of company largely by moving its listing to the US.

Shares of major insurance companies climbed as the US Medicare program will pay private insurers 2.48% more in 2027, a meaningful improvement over the initial rates the agency proposed in January.

Mid-day movers from CNBC:

In US economic data:

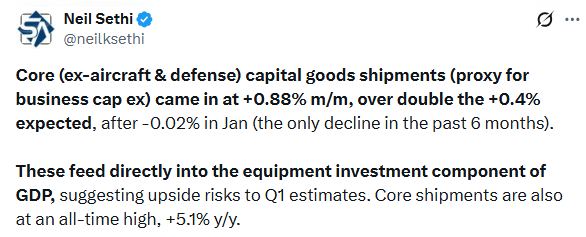

Durable goods orders fell back as expected on a drop in Boeing orders but otherwise it was a very strong, better than expected report with accelerating business investment and backlongs which all hit new record highs.

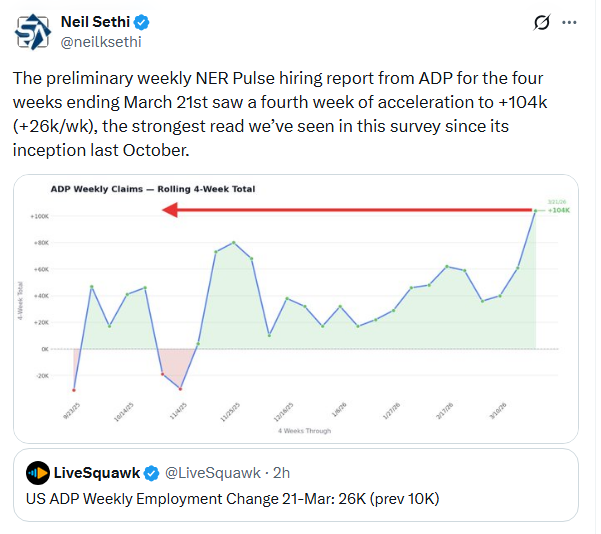

ADP’s hiring report for the four weeks ending March 21st saw a fourth week of acceleration to +104k (+26k/wk), the strongest read we’ve seen in this survey since its inception last October.

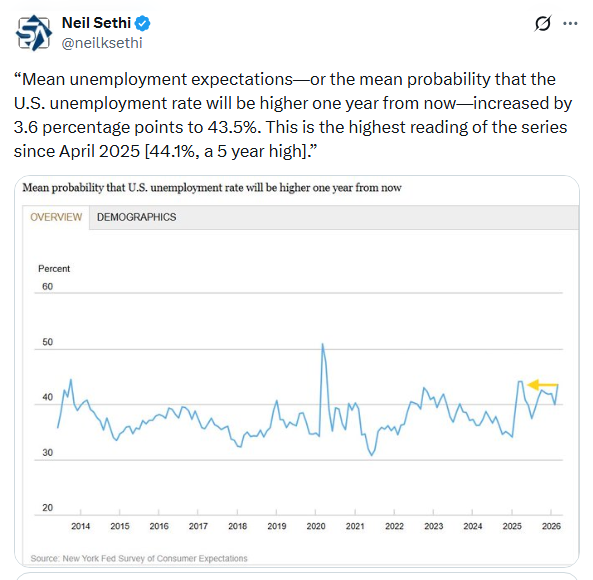

From the NY Fed consumer survey:

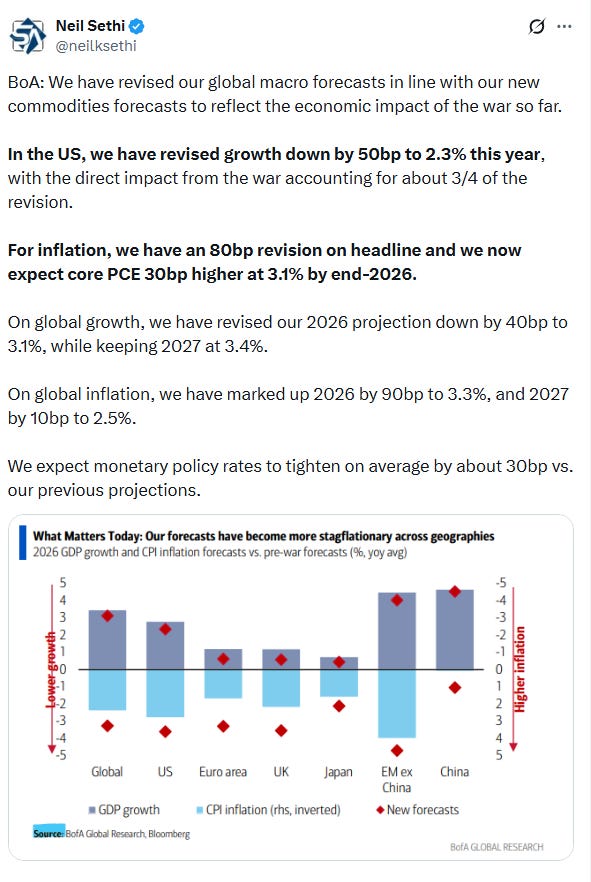

BoA lowers their 2026 US GDP forecast to 2.3% (y/y) and raises core PCE inflation forecast to 3.1%.

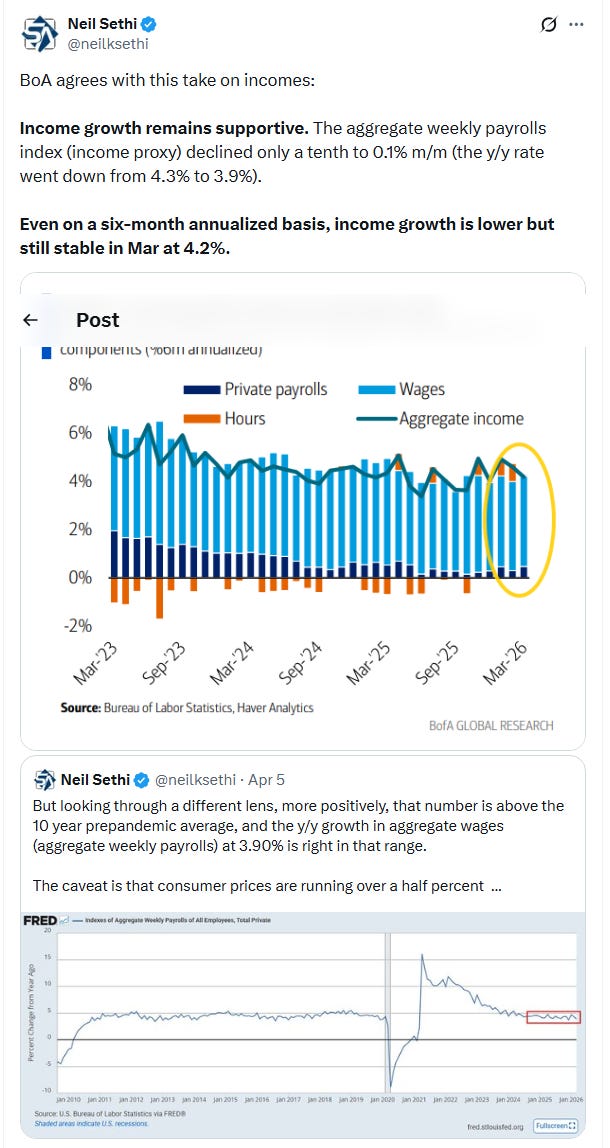

BoA agrees with my take that while softening incomes remain solid.

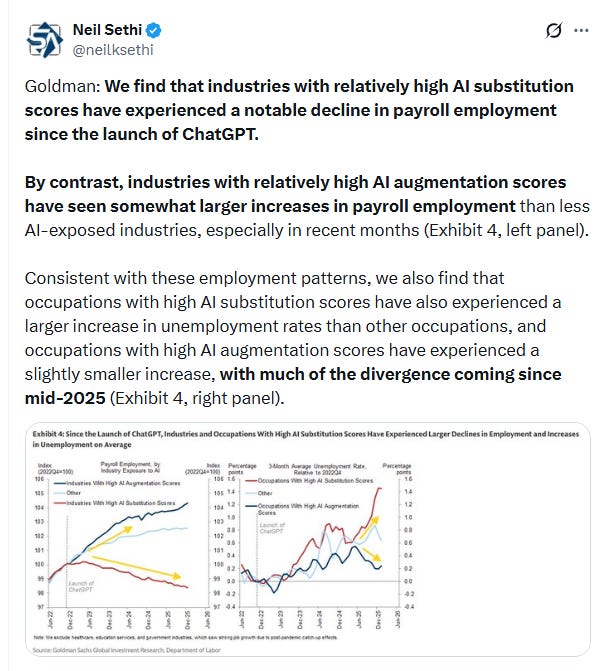

Goldman finds that AI is replacing employees who are replaceable not so for employees whose roles are augmented by AI:

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X

Note on all charts the lines are moving averages (the average price over various lookback periods (days on the daily charts, weeks on the weekly charts, etc.))”

20 = green

50 = purple

100 day = blue

200 day = brownMACD = Moving average convergence/divergence line, a measure of a momentum that compares longer term and shorter term momentum to gauge if a move is strengthening or weakening,

RSI = Relative Strength Index (basically what it sounds like) = measures the strength of the move comparing gains to losses over the given lookback window (I use the standard 14-periods)

SPX edged higher, its 5th straight advance. As mentioned Monday, “the real test everyone is watching at this point though is the 200-DMA (brown line). If it can clear that, investors will turn their eyes higher looking for the 6800 level. Until then, they will remain (appropriately) cautious. As noted Thursday we did see the daily MACD turn more positive, and the RSI is not far.”

The Nasdaq Composite remains a similar story.

RUT (Russell 2000) I have described the past couple of weeks as “easily the best looking chart of the three,” and that continued Tuesday, now coming up on its 100-DMA. Its daily MACD and RSI as mentioned Wednesday are supportive.

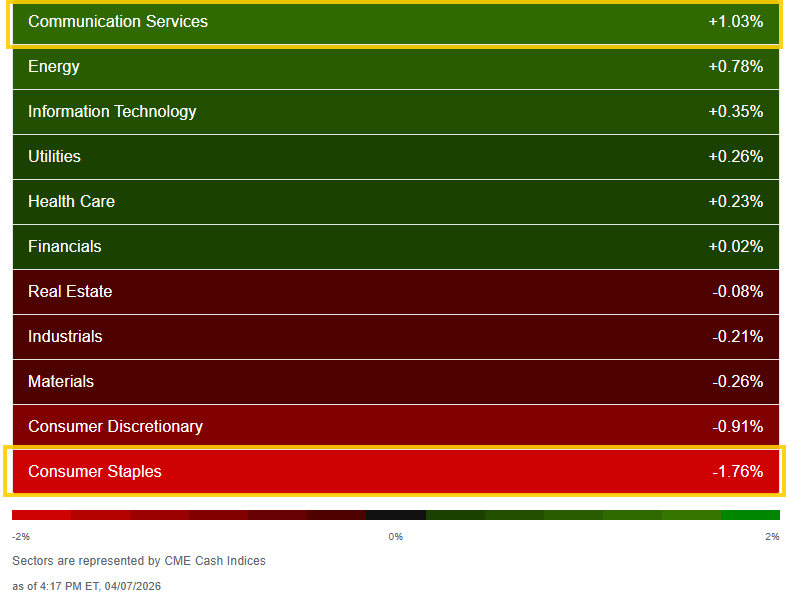

Sector breadth weakened but still saw 6 of 11 sectors higher (we haven’t seen fewer since March 27th), and one was up over 1% (barely, after none Monday) in Comm Services.

One sector down that much in Staples (-1.8%). Second was the other consumer sector Discretionary (-0.9%). No other sector down more than -0.3%.

Stock-by-stock SPX flag from finviz_com consistent with another mixed look but the red seems to be spreading and has overtaken the consumer sectors (top right).

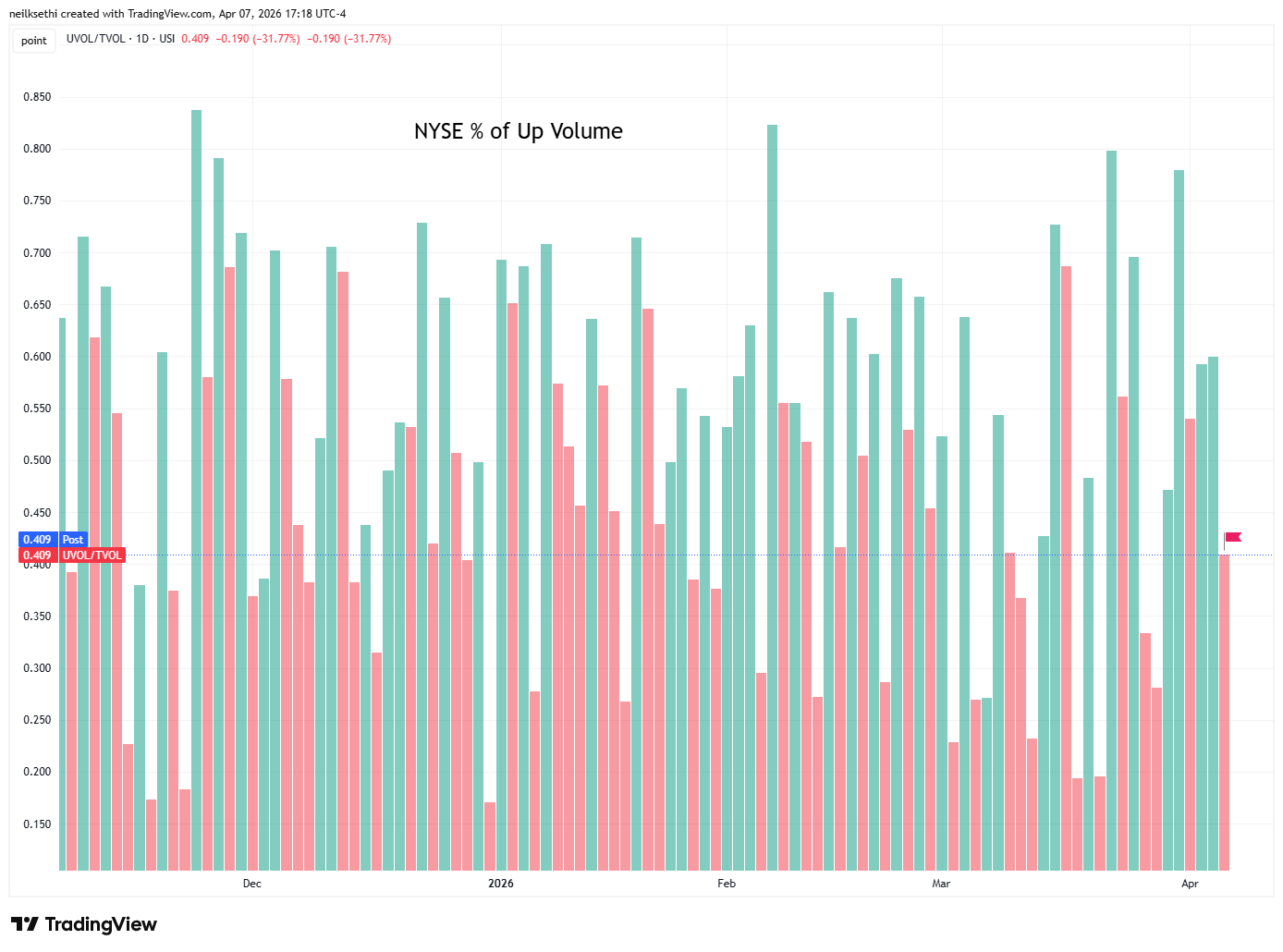

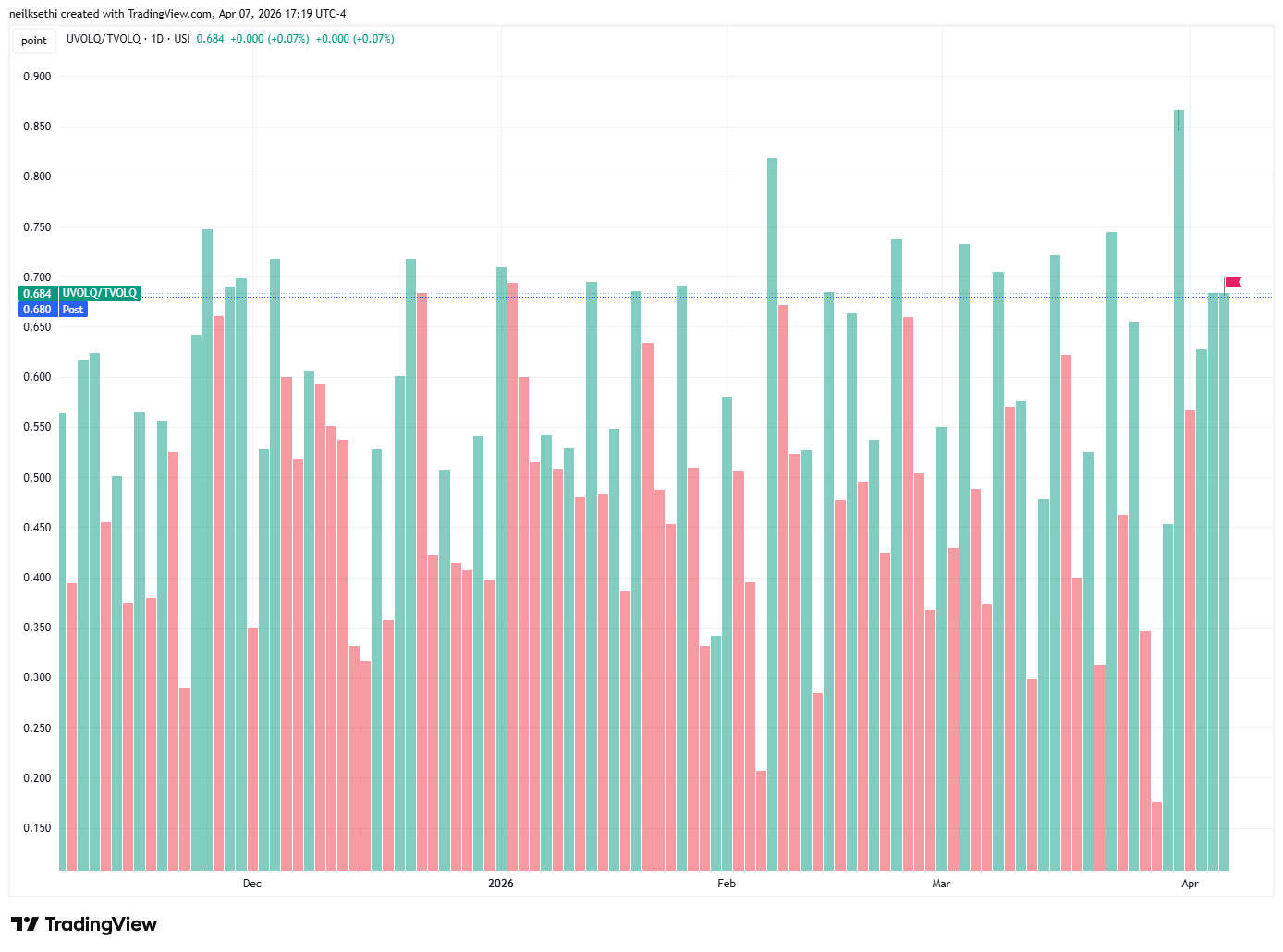

NYSE and Nasdaq positive-volume ratios (intensity of buying in stocks up on the day), which had been solid Fri/Mon turned much less so Tues on the former at 40.9% The Nasdaq remained very good at 68.0% although likely juiced by speculative volumes (see below).

Speculative activity on the Nasdaq surged Tuesday with the top 3 stocks by volume seeing over 2.7bn shares traded (1.6bn in penny stock RDGT) the second most of the year (after 4bn on Jan 14th. The next three were over 1bn which is more than we see normally for the top three. And nine(!) others traded over 100mn.

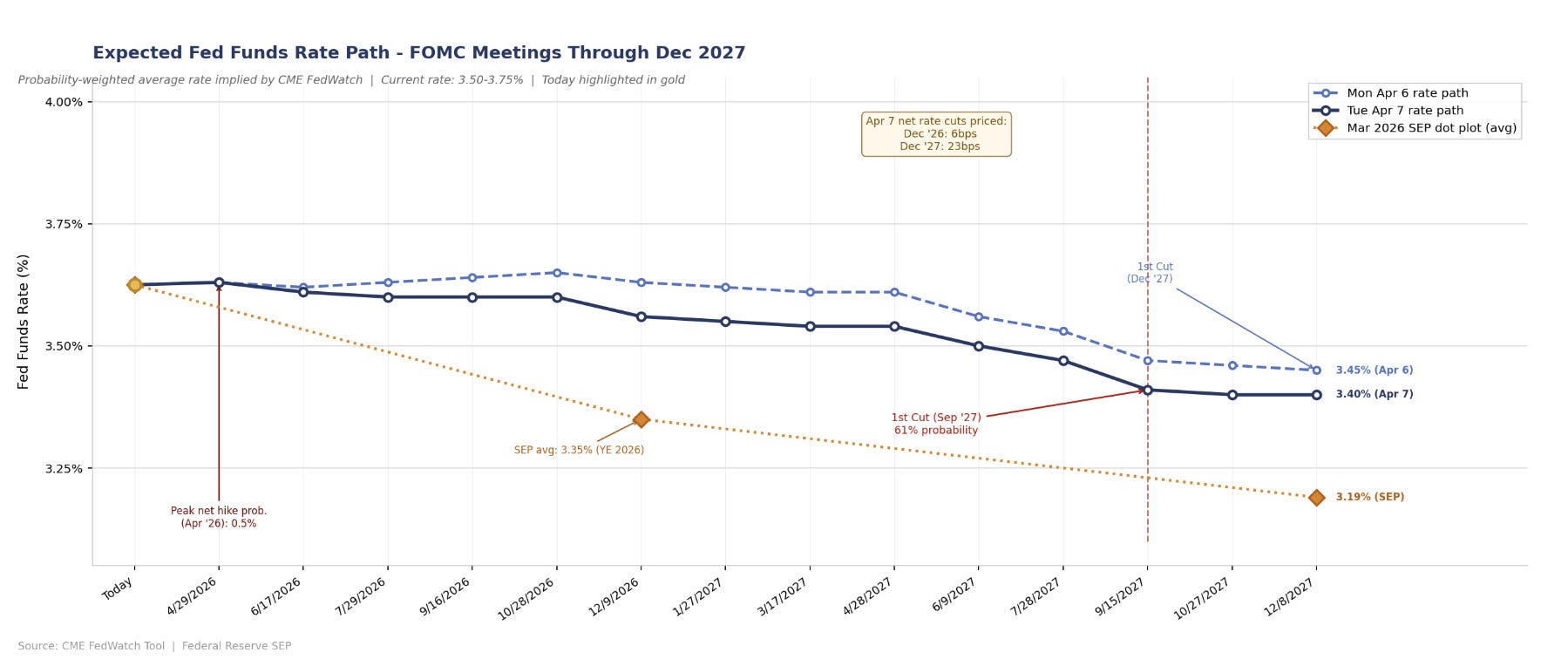

FOMC rate cut pricing eased back (more cuts) despite the relatively strong economic data and rise in inflation expectations (plus Cleveland Fed President Hammack was talking about rate hikes (I’ll have a post on that tomorrow)) according to CME’s Fedwatch tool with hike probabilities now basically off the table.

Still no cuts (assuming no hikes) though are priced until September 2027 (61%) but that’s up from 51% in December on Monday. A second cut remains off the board with Dec ‘27 at 23% (down from 44% Wednesday).

Pricing for 2026 now has +6bps of cuts (still well under the average dot on the dot plot of +28bps in cuts). 2027 is at +23bps of cuts from current levels (still down from the +35bps priced last Wednesday and compared to +43bps of cuts from current levels for the average dot on the dot plot), corresponding to a terminal rate of 3.40% up from 3.28% Wednesday, but down from 3.45% Monday.

Change from Monday. Note includes the dot plot average in orange.

The 10yr UST yield fell back to the lowest close in nearly three weeks at 4.30%, down -13bps from the highest since July hit at the end of March. I had said March 19th we might test 4.5% and we touched 4.48% March 27th, close enough?

The 2yr yield, more sensitive to FOMC rate cut pricing, fel back towards the lows of last week at 3.80%, still +18bps above the Effective Fed Funds rate (red line), consistent with no Fed cuts over the 2-year window.

The $DXY dollar index (which as a reminder is very euro heavy (57%) and not trade weighted) fell below the 20-DMA and uptrend line from the Jan lows, the latter the first time since then. If we see it fall a little further Wednesday, I’ll turn more bearish. The daily MACD is already pointing in that direction.

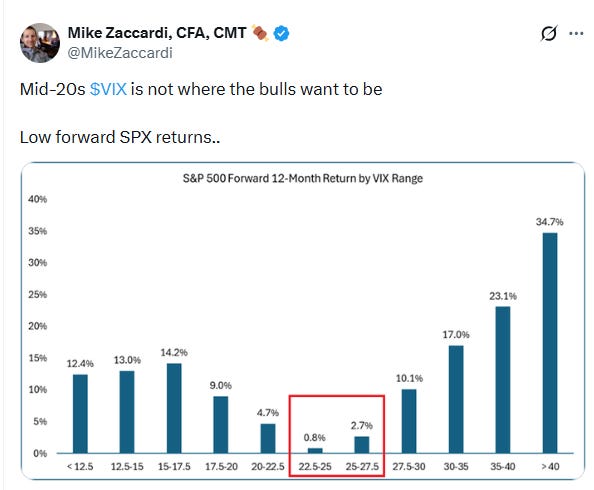

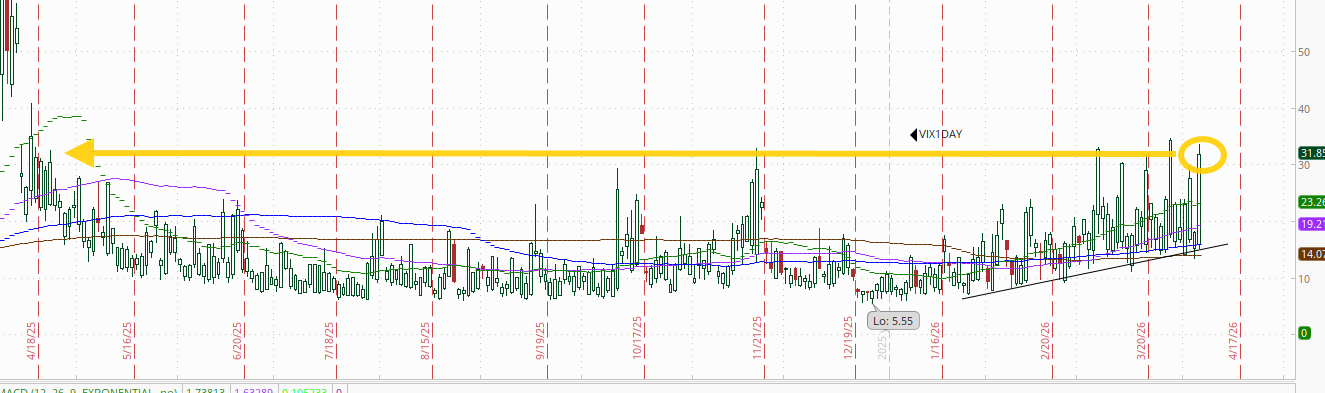

VIX little changed remaining a little elevated at 25.8, but not high enough that it’s a buy signal (actually at current levels forward returns are generally weak (see post below)). The current level is consistent w/~1.61% average daily moves in the SPX over the next 30 days.

The VVIX (VIX of the VIX) little changed at 117.3, remaining under its uptrend line from the December lows for a fourth session but for now holding the 50-DMA.

The current level is still consistent with “elevated” daily moves in the VIX over the next 30 days (historically, normal is 80-100, but we’ve been above 90 most of the time since July ‘24)). Above 100 is the level flagged by Charlie McElligott as indicating higher stress.

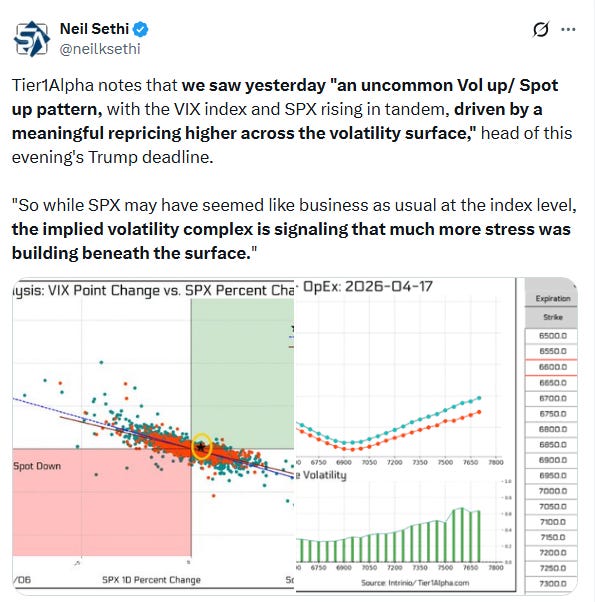

With the Trump deadline tonight, as flagged yesterday the 1-day VIX jumped to 31.9, the highest non-Friday close since last April (and the highest since then pre-March). That’s consistent with a move of 2% in the SPX next session.

WTI as noted eased back a little but remained above $100 just off the highest close since 2022.

Gold futures (/GC) literally no change today (a little odd) remaining in their old channel from early 2024 that they left at the start of 2026 for a couple of months. The technicals are mixed with the MACD in a mild “cover shorts” reading but the RSI is still under 50 so as noted Monday “hard to say which way it goes from here.”

US copper futures (/HG) fell back. Like gold, the daily MACD is in a “cover shorts” positioning, but the RSI is still under 50..

Natural gas futures (/NG) were higher but remain near the least since August. The daily MACD is now dead flat, and the RSI is around 40 so not much to get excited about, particularly with winter in the rear-view mirror.

Bitcoin futures fell back after their best day in a month although, overall remaining in their the range since the start of February (the blue box). The daily MACD remains in a mild “go long” reading, but the RSI is under 50.

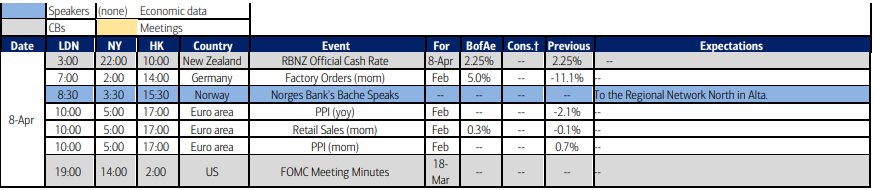

The Day Ahead

We get a pause from major US economic data Wednesday before a busy Thursday/Friday with just weekly mortgage applications and US petroleum inventories.

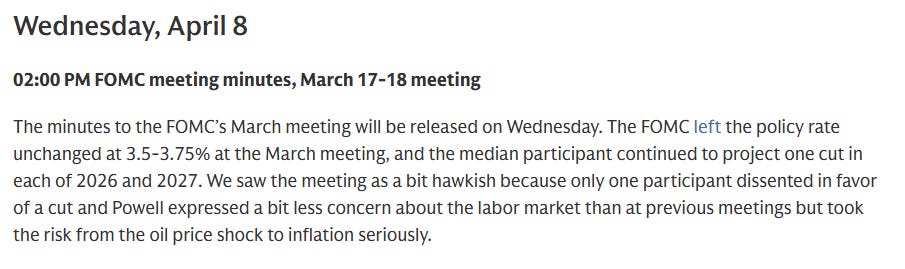

Fed speakers continue with San Francisco Fed President Daly. More importantly, we’ll get the minutes from the March FOMC meeting where we will get more context on their thinking around the Iran conflict and its repercussions, etc.

Non-bill Treasury auctions (>1yr in duration) continue with 10-year notes (reopening).

We’ll get our only SPX reporters of the week Wednesday with Delta DAL and Constellation Brands STZ.

Ex-US highlights are policy decisions in New Zealand, Norway, and India, Japan labor earnings and trade balance, Germany factory orders, UK house prices, France trade balance, and Eurozone retail sales.

Link to X posts - Neil Sethi (@nelksethi) / X

To subscribe to these summaries, click below (it’s free!).

To invite others to check it out,