Markets Update - 4/8/26

Update on US equity and Treasury markets, US economic data, the Fed, select commodities and a look at the upcoming day with charts!

Similar to the Week Ahead, I am reworking the nightly Markets Update to make it more streamlined and hopefully more useful. I’m making this week open to all subscribers so you can see the format and give it a try. As always, feedback is welcome.

Quick Summary:

Equities jumped higher and crude oil dropped following the announced two-week ceasefire between the US/Israel and Iran even as passage through the Strait of Hormuz remained at a standstill and issues emerged on several fronts.

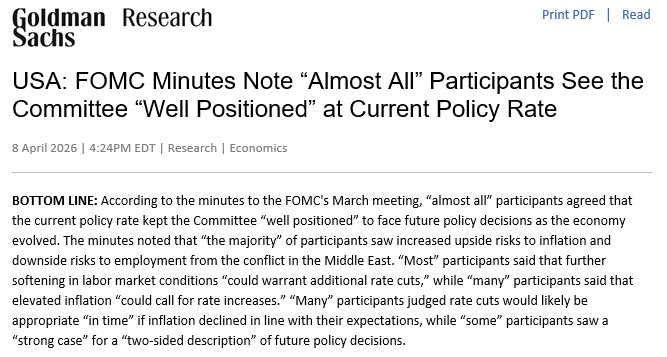

Minutes (summary) from the March FOMC meeting confirmed a continued shift towards a more cautious Fed with “the vast majority” noting “the risk of inflation running persistently above the committee’s objective had increased”. In addition “almost all” agreed that the current policy rate kept the Committee “well positioned” to face future policy decisions as the economy evolved.

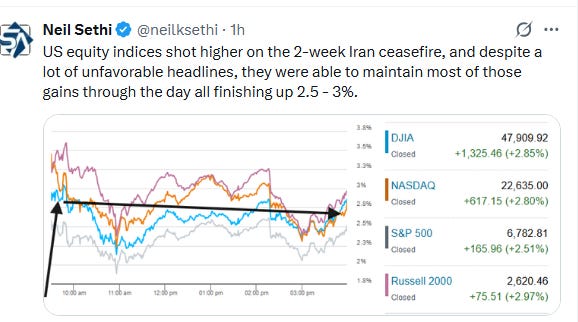

US equity indices opened trading Wednesday surging higher following the two-week ceasefire announced overnight by President Trump even as traffic through the Strait of Hormuz remained throttled by Iran and the sides seemed quite far apart on their demands for a lasting end to the hostilities as detailed in the morning post.

Things didn’t get any clearer during the session. Iranian state news agency Fars said that oil tanker traffic through the strait had ceased following an Israeli attack on Lebanon, while Iran’s parliamentary speaker Mohammad Bagher Ghalibaf also said the U.S. has already violated its two-week ceasefire agreement. But the White House insisted there was “an uptick of traffic in the strait today,” and reports to the contrary “are false.” It was also announced that US Vice President JD Vance will lead a delegation to Pakistan to hold talks on a peace agreement with Iran on Friday.

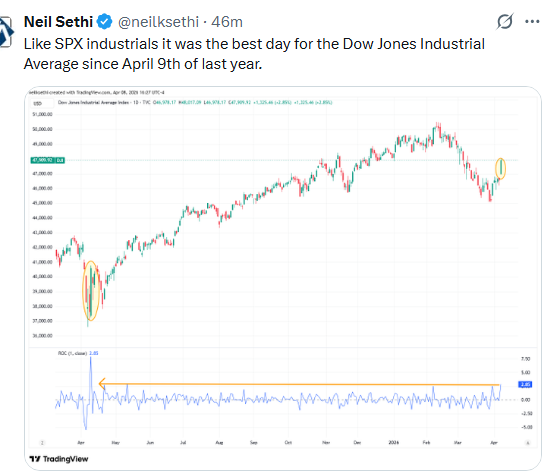

But despite the confusion crude prices fell sharply and equity indices held most (if not all) of their initial gains closing up by 2.5 - 3% with the Dow Jones Industrial Average seeing its best day since April of last year.

Elsewhere, bond yields and crude prices fell back as did the dollar (which gave back all of this year’s advance) and US natural gas prices. Copper, gold, and bitcoin all saw string gains (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was +2.5%, the equal weighted S&P 500 index (SPXEW) +2.4%, Nasdaq Composite +2.8% (and the top 100 Nasdaq stocks (NDX) +2.9%, the SOXX semiconductor index +6.3% (up 17% the last five sessions to an ATH), and the Russell 2000 (RUT) +3.0%.

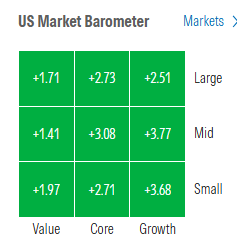

Morningstar style box showed strong gains across the style box led by growth.

Some market commentary:

““It wasn’t much of a surprise that there was an announced reprieve in the Iranian conflict. The market has gotten much better at sniffing out” Trump’s next move, said Jay Woods, chief market strategist for Freedom Capital Markets. “The concern now is if this all too familiar ‘two-week’ timeframe is going to lead to a resolution.”

“While market price action is still likely to remain hostage to short-term news flow regarding traffic into and out of the Strait of Hormuz and any signs of a re-escalation, it’s become more and more evident that President Trump wants an off-ramp,” Chris Senyek at Wolfe Research said.

Markets have been moving very quickly, setting us up for a relief rally,” said Neil Birrell, chief investment officer at Premier Miton Investors. “What will happen in the next few weeks — who knows? It’s hard to believe that this is a long-term resolution.”

“The ceasefire is a clear positive, but it’s not a resolution,” said Mark Hackett at Nationwide. “What stands out is how quickly the market flipped once the pressure eased. When positioning gets this crowded, it doesn’t take much to spark a reversal.” Equity strategists at Barclays Plc said they expected stocks to experience a “powerful short squeeze,” as hedge funds remove protections that were put in place to hedge the risk of further escalation. Hedge funds are rushing to close out bets against US stocks at a pace not seen since the market rebounded from the crash set off by the pandemic in March 2020, according to Goldman Sachs’ trading desk division.

“While there are valid questions around the durability of the ceasefire and the extent of economic damage already done, Brent has retraced almost half of its Iran-driven surge, while most equities have not recovered a similar share of their losses. This gap should support continued momentum in the risk rally.”

— Skylar Montgomery Koning, macro strategist.

A temporary truce in the war allowed global investors to begin to contemplate the restructuring of portfolios and a re-rotation of sector leadership in anticipation of a more long-lasting cessation of hostilities, according to Sam Stovall at CFRA Research. He noted that the response following the recession and bear market that coincided with Iraq’s invasion of Kuwait in 1990 may serve as a guide. Three months after oil prices peaked and then tumbled, the S&P 500 jumped 12.4%. “What’s more, sector leadership rotated from defensive holdings back into cyclical groups,” Stovall added. “A similar rotation could take place this time around should the ceasefire be maintained.”

Irrespective of the eventual agreement made, Iran has demonstrated the Strait of Hormuz chokepoint is at its mercy, says Bilal Hafeez, chief executive officer and founder of Macro Hive Research. Among his other hot takes on the cease-fire announced Tuesday, the former forex strategist at JPMorgan and Deutsche Bank said China made a low-key power play on Tuesday by voting against a UN resolution to protect commercial shipping in the Strait. Hafeez makes the point that China’s position in the Middle East has been strengthened by this crisis. Moreover, Pakistan’s influence should not be underestimated, both in acting as a mediator in the conflict and its growing alliance with China, he said. For Hafeez, however, the chief consequence of the war is the question mark placed beside the value of U.S. military support. NATO’s value is now dubious and countries from the Gulf to East Asia are wondering if the U.S. can provide enough defense in the face of China’s ascendance. Regional rearmament is likely to reaccelerate across the world and the long-term decline of the dollar is reinforced.

Some posts from today:

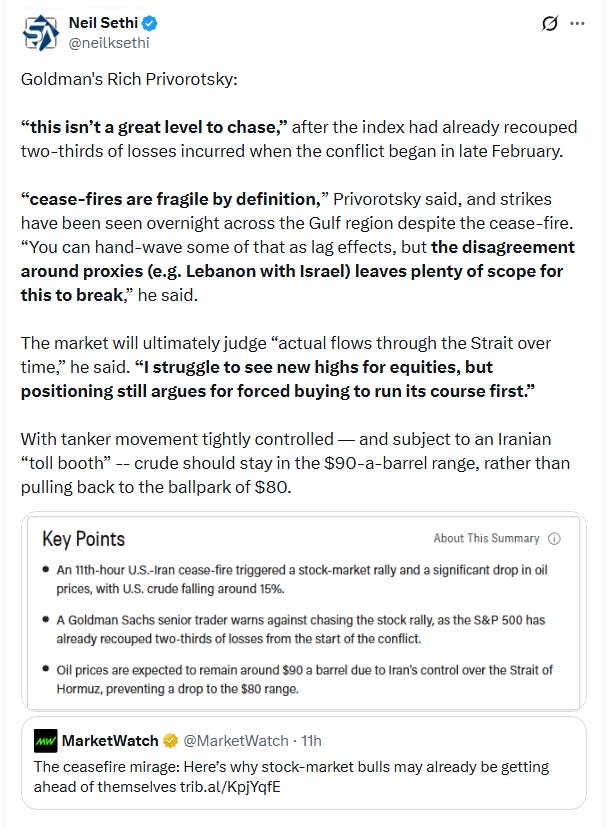

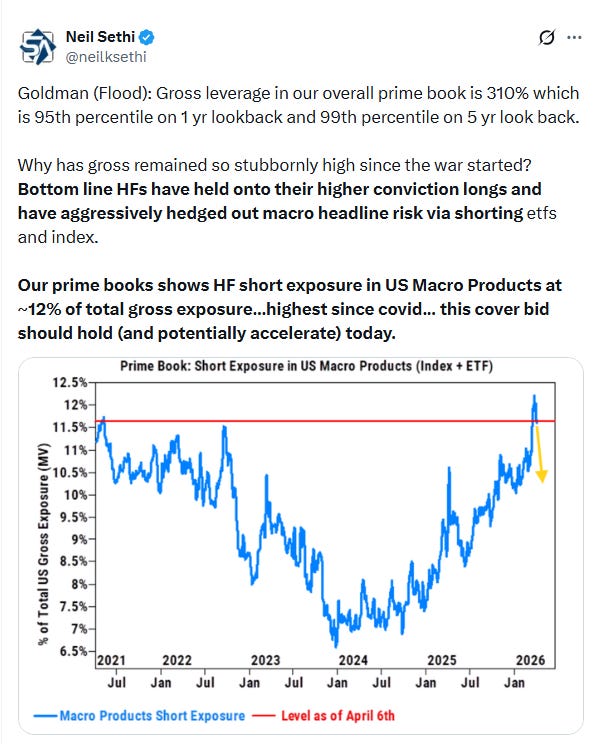

One top Goldman trader expresses caution in chasing today’s move, but he also notes that the current rally will need to “run its course” (meaning run through the burst of short covering, systematic releveraging, etc.):

And more on that likely short covering:

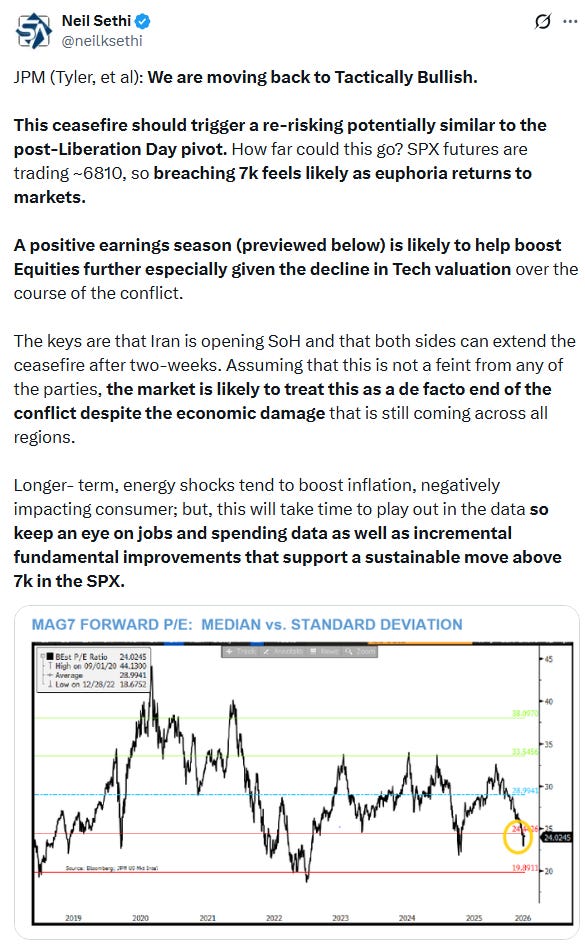

And JPM’s trading desk turns “tactically bullish” liking Tech:

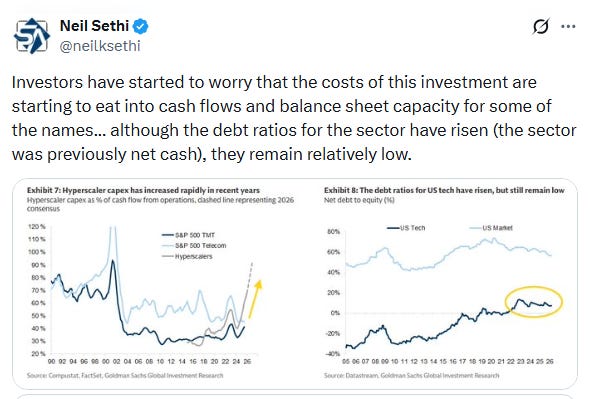

And more from Goldman on their liking of tech:

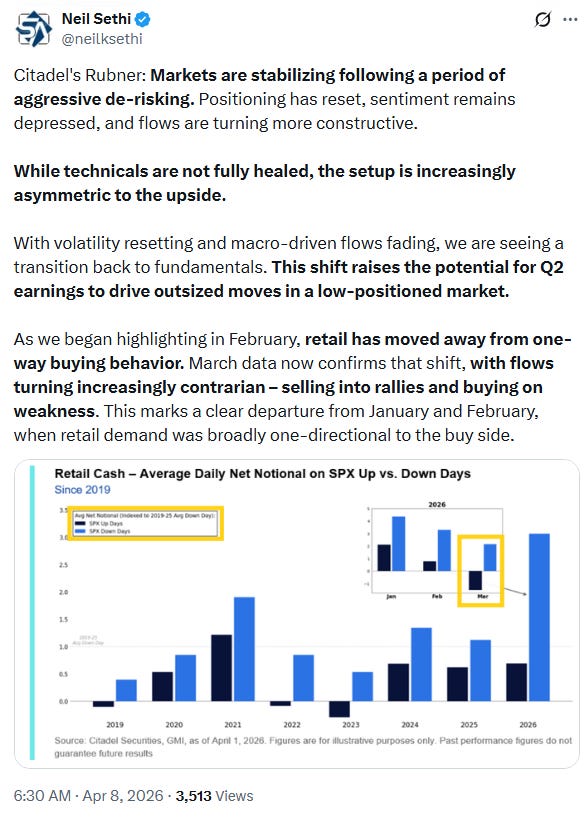

While Citadel’s Scott Rubner is seeing increasing asymmetry to the upside:

And BBG on the high volumes we’ve seen this year:

Link to X posts - Neil Sethi (@neilksethi) / X for full posts/access to charts.

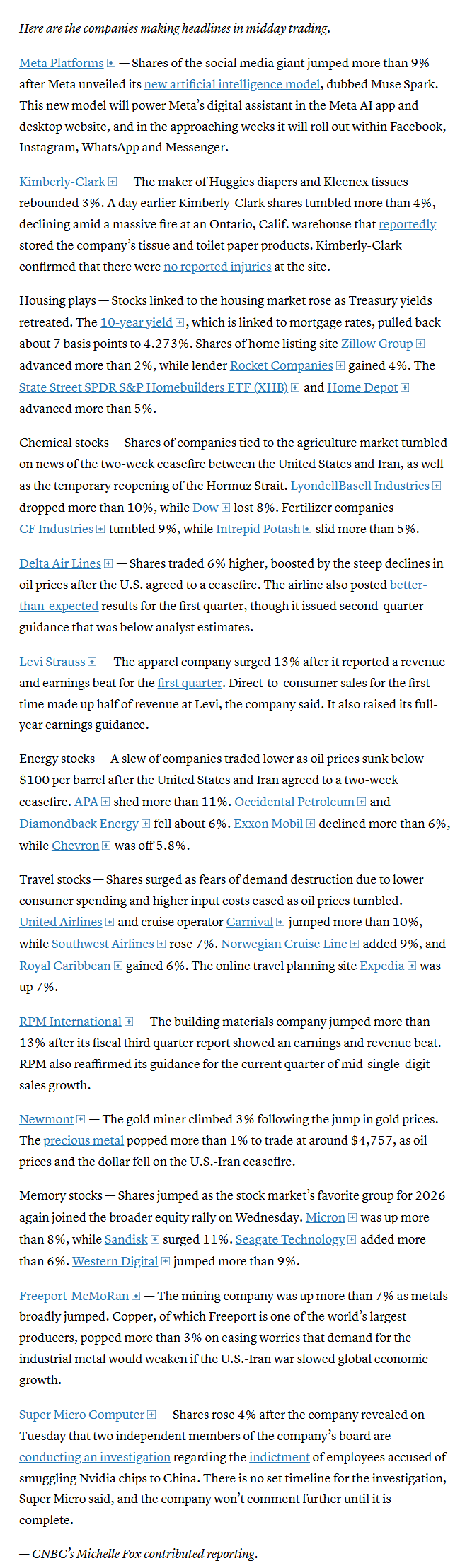

In individual stock action:

The industrials sector (+3.8%) led the advance, supported by strong gains across airline names such as United Airlines (UAL 96.30, +7.01, +7.85%) amid the retreat in oil prices. Delta Air Lines (DAL 68.08, +2.46, +3.75%) beat earnings expectations, and the company emphasized that it is not seeing any slowdown in summer travel demand despite higher ticket prices and macro headwinds, but gains were muted on announced capacity cuts.

Similarly, cruise lines such as Carnival (CCL 28.03, +2.83, +11.23%) posted double-digit gains. Semiconductor makers vulnerable to supply chain disruptions also climbed, with the VanEck Semiconductor ETF (SMH) up more than 5%. Broadcom was higher by nearly that much, Micron Technology by more than 7%. On the other hand, energy stocks that have surged since the start of the conflict faltered. Shares of Exxon Mobil and Chevron slid more than 4%, each.

Corporate news from BBG:

Delta Air Lines Inc. expects to incur more than $2 billion in higher fuel costs through June because of the Iran war, prompting the carrier to tread carefully and stick to its previous full-year profit forecast.

Exxon Mobil Corp. lost 6% of its global production in the first quarter as the Iran war paralyzed oil and natural gas operations in the Persian Gulf.

Meta Platforms Inc. debuted its latest artificial intelligence model — its first since Chief Executive Officer Mark Zuckerberg embarked on an overhaul of the company’s AI organization to keep pace with rivals.

Mid-day movers from CNBC:

In US economic data:

Minutes (summary) from the March FOMC meeting confirmed a continued shift towards a more cautious Fed with “the vast majority” noting “the risk of inflation running persistently above the committee’s objective had increased”. In addition “almost all” agreed that the current policy rate kept the Committee “well positioned” to face future policy decisions as the economy evolved.

Non-mortgage consumer debt rose in February but credit card debt up the least since Nov and just +1.8% y/y (blog post).

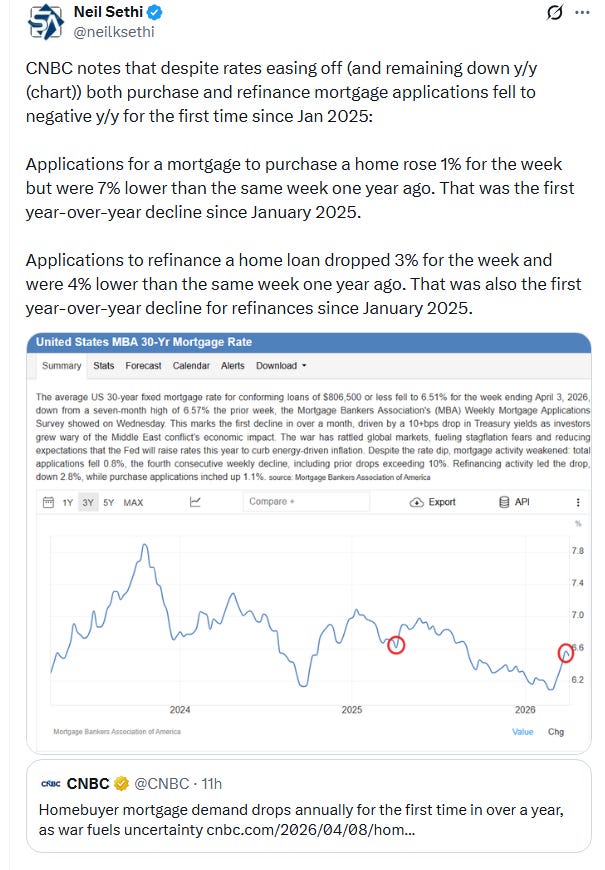

Mortgage applications fall back despite the decline in rates, down from year-ago levels for the first time since January 2025:

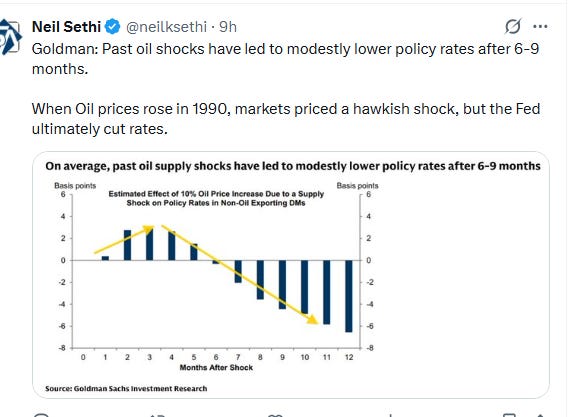

Goldman notes while oil shocks may lead to rate hikes in the near term, they often lead to rate cuts longer term:

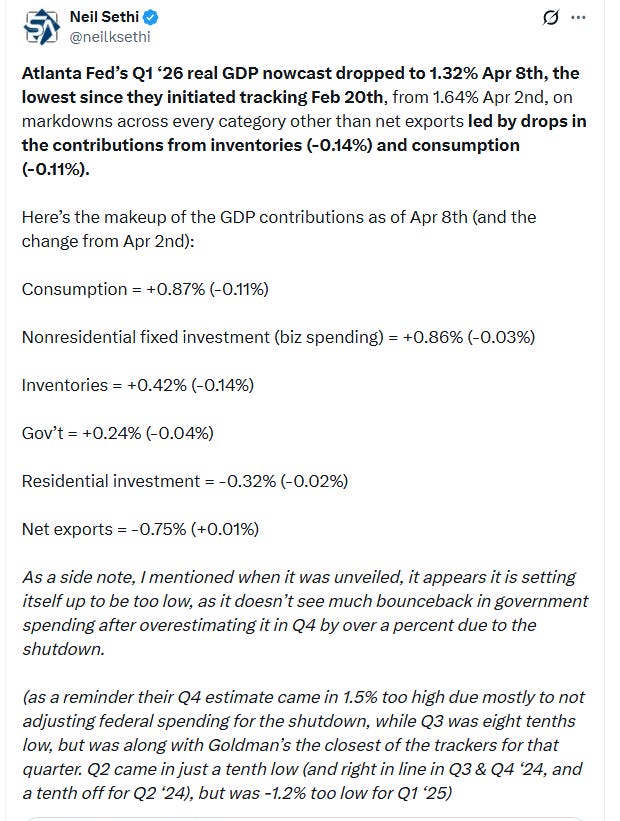

While Atlanta Fed cuts their 1Q GDP forecast further (which I think though is setting up to be too low as noted in the post):

Link to posts for more details/access to charts - Neil Sethi (@neilksethi) / X

Note on all charts the lines are moving averages (the average price over various lookback periods (days on the daily charts, weeks on the weekly charts, etc.))”

20 = green

50 = purple

100 day = blue

200 day = brownMACD = Moving average convergence/divergence line, a measure of a momentum that compares longer term and shorter term momentum to gauge if a move is strengthening or weakening,

RSI = Relative Strength Index (basically what it sounds like) = measures the strength of the move comparing gains to losses over the given lookback window (I use the standard 14-periods)

SPX shot higher, its 6th straight advance, jumping right over the 200-DMA as well as edging over the 50-DMA, although it couldn’t clear the 6800 level flagged Tuesday. I’d like to see it take and hold that level before stepping in, but now my sights are set higher and will also be watching for a dip to buy. A pullback to that 200-DMA would be a great place to do so. Daily MACD and RSI are now strongly positive.

The Nasdaq Composite remains a similar story (here I’d like a clearing of 23,000 or pullback to the 200-DMA or perhaps a little lower). Notably while the SPX closed above the open (green candle) the Nasdaq closed below (red candle).

RUT (Russell 2000) I have described the past few weeks as “easily the best looking chart of the three,” and that continued Wednesday, now through all of the major moving averages but getting stopped at one last trendline (from the all-time highs) that it needs to clear.

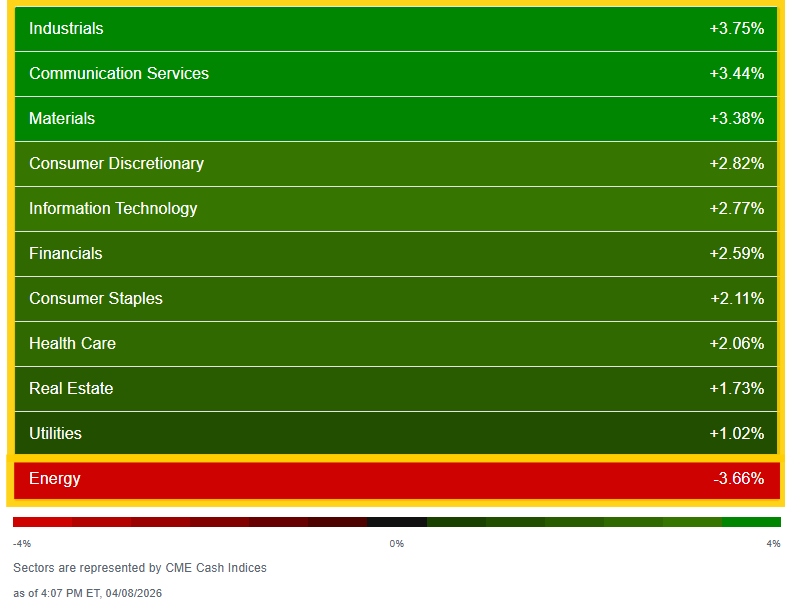

Sector breadth much improved as you’d expect with just Energy (which was -3.7%) finishing lower.

Every other sector (10 of 11) up at least 1% with eight up over 2%, and three up over 3% led by Industrials +3.8%, its best day since April of last year.

Stock-by-stock SPX flag from finviz_com consistent with bright green (>3% gains) across much of the flag. Just Energy, some software, and telecoms sat out the action for the most part.

In that regard, there were ~220 SPX components (around 45%) that were up at least 3%, the best this year.

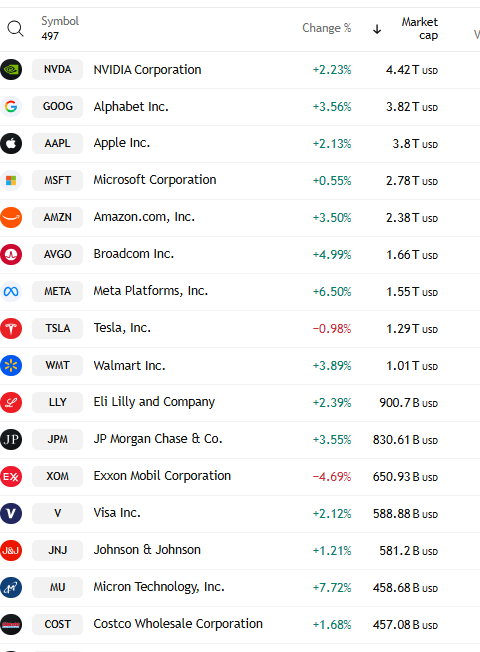

Out of the top 16 names, just Tesla and Exxon were lower.

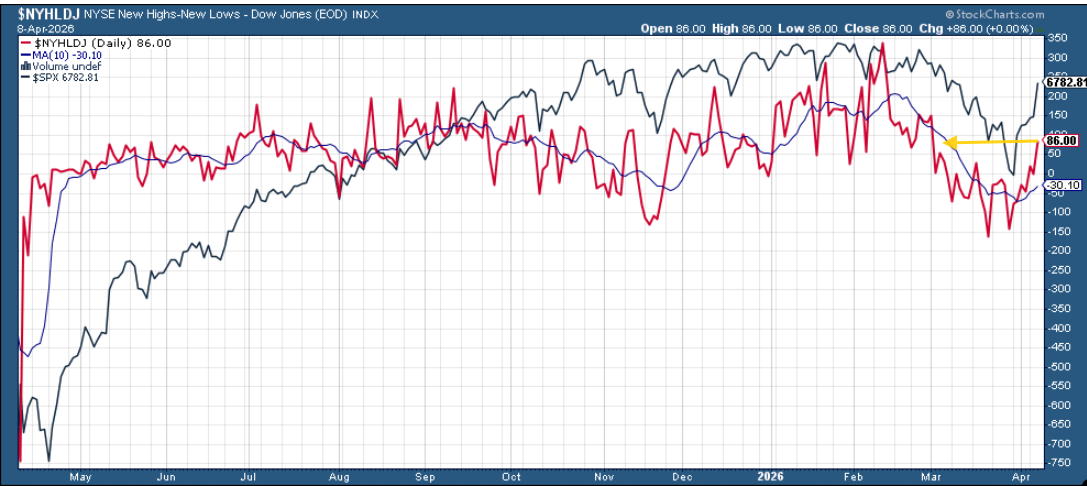

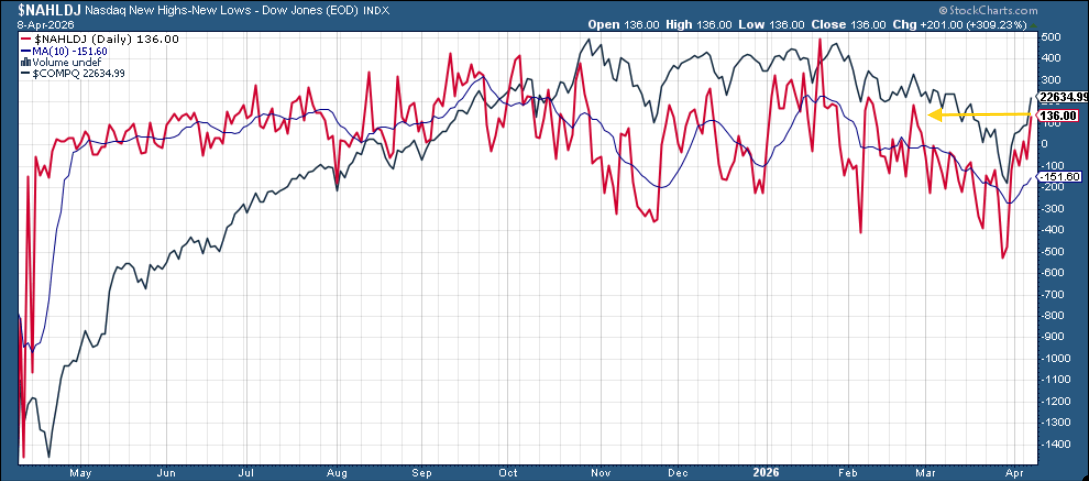

And new highs-new lows (red lines) are following index prices to the highest since February on the NYSE and Nasdaq.

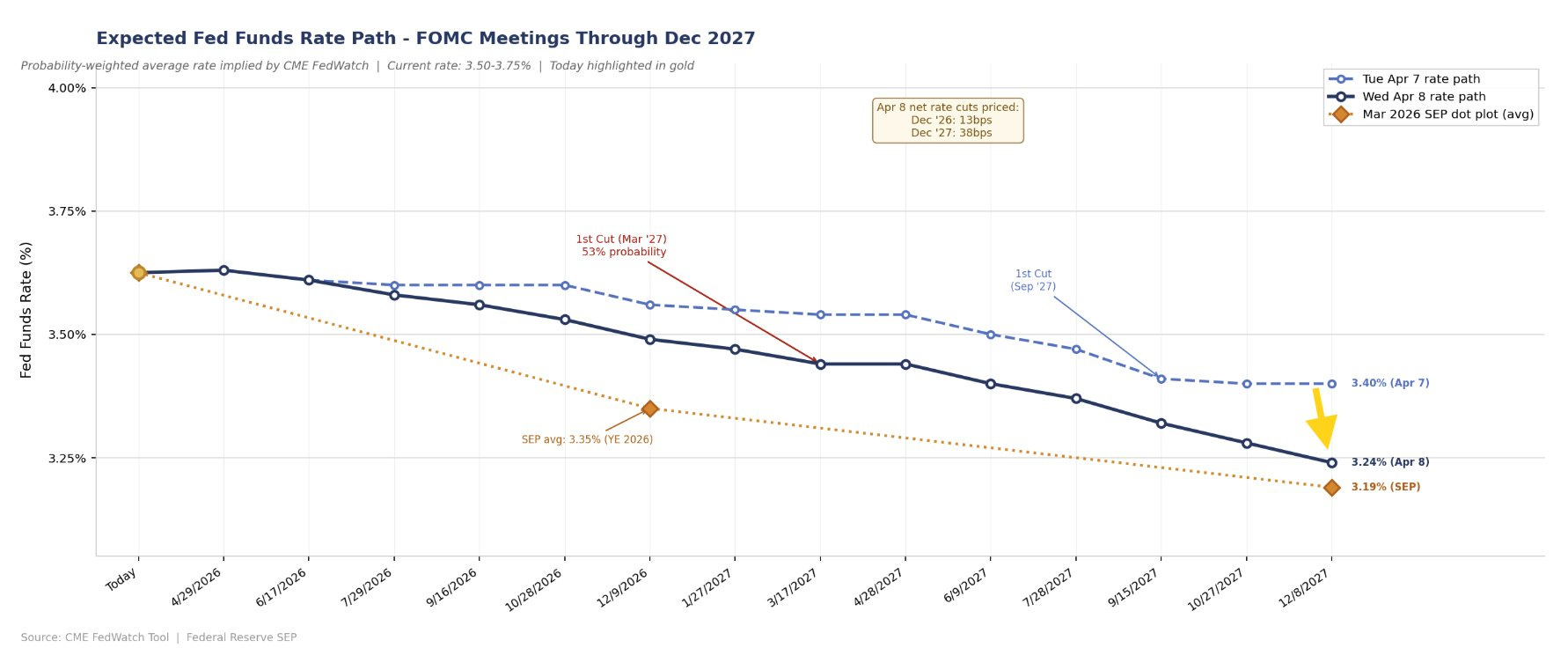

The CME Fedwatch tool is all screwed up currently but I happened to run it this morning, and as of then FOMC rate cut pricing had jumped higher (more cuts). That said, based on the action in the 2-year yield (see below), I have a feeling this moved more hawkishly after the FOMC minutes.

The first cut (assuming no hikes) moved to March 2027 up from 50/50 in December on Monday. A second cut remains off the board but just barely at 49% for Dec ‘27.

Pricing for 2026 now has +14bps of cuts (up to half of the average dot on the dot plot of +28bps in cuts). 2027 is at +39bps of cuts from current levels (now just a little below the +43bps of cuts from current levels for the average dot on the dot plot), corresponding to a terminal rate of 3.24%, down from 3.45% Monday, but also up from 2.80% pre-war.

Change from Tuesday. Note includes the dot plot average in orange.

The 10yr UST yield recovered all of its losses to end unchanged (but still the lowest close in nearly three weeks) at 4.30%, down -13bps from the highest since July hit at the end of March.

The 2yr yield, more sensitive to FOMC rate cut pricing, consistent with the commentary above recovered most all of its losses to finish little changed at 3.79%, still +17bps above the Effective Fed Funds rate (red line), consistent with no Fed cuts over the 2-year window.

The $DXY dollar index (which as a reminder is very euro heavy (57%) and not trade weighted) dropped sharply but was able to bounce from its 200-DMA to cut some of its losses. Still it’s now conclusively below the uptrend line from the Jan lows, but I guess as long as it holds the 200-DMA I won’t turn super-bearish. As noted earlier, though, the daily MACD is already pointing in that direction and now the RSI is as well.

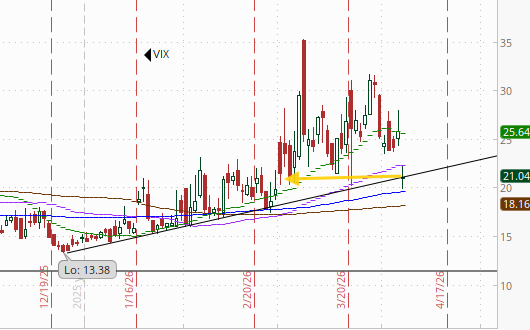

VIX dropped to the lowest close since the start of the war at 21.0, a favorable development, although the current level is still consistent w/~1.31% average daily moves in the SPX over the next 30 days. It’s now on its uptrend line from the December lows as well.

The VVIX (VIX of the VIX) at 111.1 while not at the least since February like the VIX, is under its line from the December lows, which perhaps means we might see the VIX do the same?

The current level is still consistent with “moderately elevated” daily moves in the VIX over the next 30 days (historically, normal is 80-100, but we’ve been above 90 most of the time since July ‘24)). Above 100 is the level flagged by Charlie McElligott as indicating higher stress.

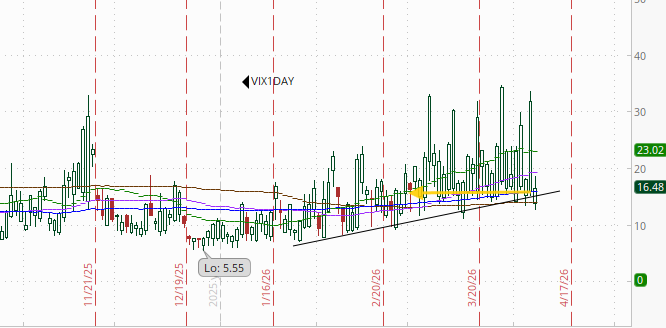

With a ceasefire at least theoretically in the works, like the VIX the 1-day VIX fell to the least since February at 16.5. That’s consistent with a move of 1.03% in the SPX next session, half the move implied at Tuesday’s close.

WTI dropped sharply but cut some of those losses to make it back to $90. Still it’s broken its uptrend line and as noted earlier the technicals are not favorable. Its path from here likely depends mostly on whether the ceasefire holds and the Strait of Hormuz reopens.

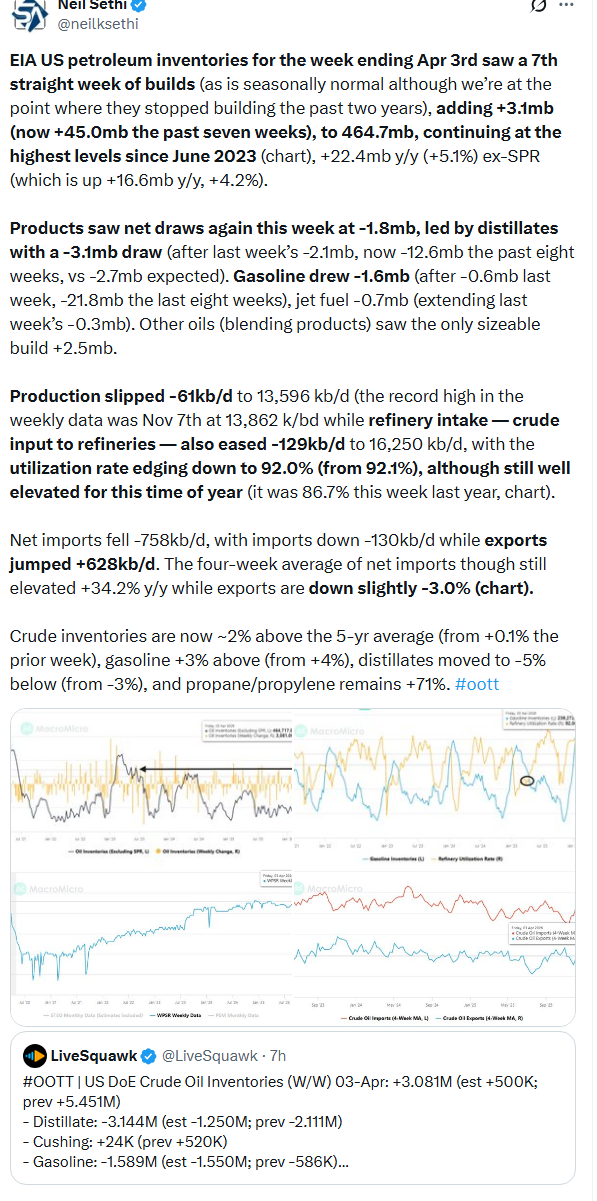

While much of the world is drawing down crude inventories, it’s a different story in the US:

Gold futures (/GC) jumped higher but pared back much of those gains. Still finished up 2% but not even a 1-week high. They remain in their old channel from early 2024 that they left at the start of 2026 for a couple of months. The technicals are mixed with the MACD in a mild “cover shorts” reading while the RSI is around 50 but it seems to ironically have liked the dialing back of the geopolitical tensions.

US copper futures (/HG) a stronger session than gold up nearly 4% taking them to their 50-DMA. Like gold, the daily MACD is in a “cover shorts” positioning, but the RSI is stronger.

Natural gas futures (/NG) dropped -5% to the least since August (and close to the least since Oct ‘24). The daily MACD remains flat, and the RSI is under 40 so as I said last week “not much to get excited about, particularly with winter in the rear-view mirror.”

Bitcoin futures up over 3%, but for now remaining in their the range since the start of February (the blue box). The daily MACD remains in a “cover shorts” reading, and the RSI is back over 50, plus it cleared the 50-DMA so could see it test the top of the range again at least.

The Day Ahead

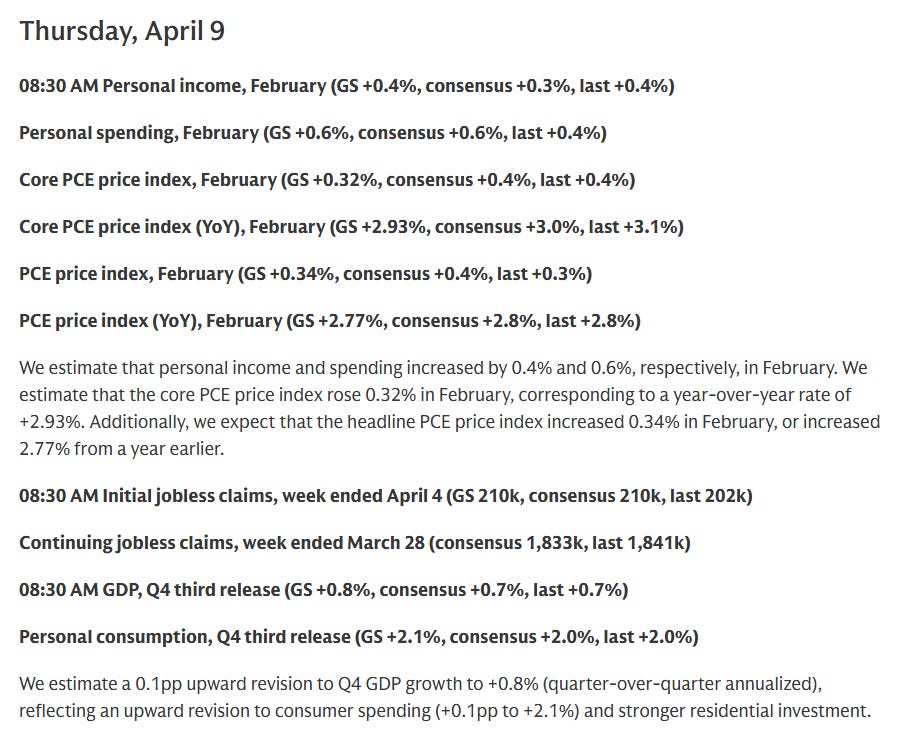

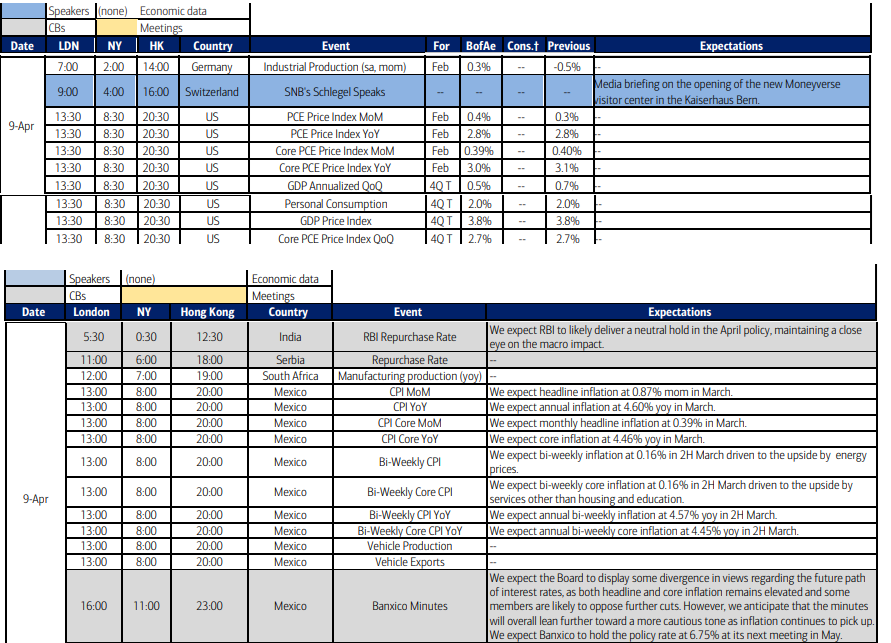

US economic data picks back up Thursday with what might be our top monthly report if it didn’t come so late in the February personal income and spending report which contains PCE prices (the Fed’s preferred inflation gauge). We’ll also get the second revision to 4Q GDP (which should come with our best look at economy-wide corporate profits), wholesale inventories, and weekly jobless claims.

No Fed speakers on the calendar, but we’ll see if we don’t get an interview or two.

Non-bill Treasury auctions (>1yr in duration) wrap up with 30-year bonds (reopening).

SPX reporters are done for the week (but pick up in a big way next week).

Ex-US highlights are Germany industrial production, trade balance, Banxico minutes and Mexico CPI.

Link to X posts - Neil Sethi (@nelksethi) / X

To subscribe to these summaries, click below (it’s free!).

To invite others to check it out,