Markets Update - 5/11/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

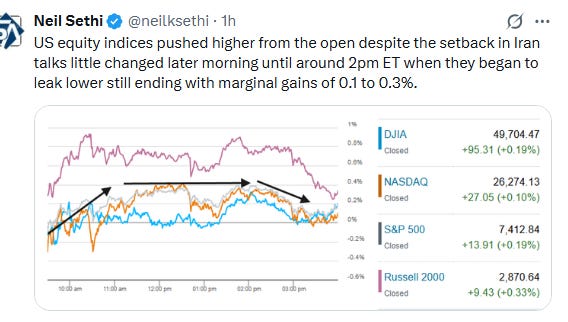

US equity indices recovered from overnight losses following the setback in Iran talks discussed in the morning post to open little changed and would push into the green despite no progress on that front led by the small cap Russell 2000 (RUT). Indices would hold their modest gains until around 2pm ET when they began to leak lower, although still ending a little higher with gains of 0.1% (Nasdaq) to 0.3% (RUT). It was enough for the 16th all-time high for the S&P 500 this year (charts in subscriber section).

President Donald Trump on Monday said “I would say the ceasefire is on massive life support, where the doctor walks in and says, ‘Sir, your loved one has approximately a 1% chance of living.” He added “I would call it the weakest, right now, after reading that piece of garbage they sent us — I didn’t even finish reading it.”

Despite the Nasdaq seeing a minimal gain, the semiconductor trade continued unabated with the SOX Semiconductor index adding another +2.6% taking its gains to 70% since March 30th (chart below).

Fed rate hike bets though followed the Iran news flow, increasing with now a 20% chance of a hike in 2026 and 43% by April 2026 (covered in the subscriber section).

US economic data Monday was lighter with just April existing home sales which edged up from 9-month lows but remained very weak historically despite rising inventories. Median prices were the highest on record for April. We’ll get April CPI tomorrow among other releases (full calendar in the subscriber section).

Elsewhere, bond yields and crude prices also saw more reaction to the Iran-US back and forth with solid advances. Unlike previous sessions, though, where those were higher, gold also was up (modestly) as was the dollar while bitcoin, US natural gas futures, and copper logged stronger advances (the latter to another record closing high) (all covered in the subscriber section).

The market-cap weighted S&P 500 (SPX) was +0.2%, the equal weighted S&P 500 index (SPXEW) -0.1%, Nasdaq Composite +0.1% (and the top 100 Nasdaq stocks (NDX) +0.3%, the SOX semiconductor index +2.6% (as noted another all-time high), and the Russell 2000 (RUT) +0.4%.

Some market commentary:

“The economy is so much better than what the doom crew has been saying,” Chris Zaccarelli, chief investment officer at Northlight Asset Management says. “There are a lot of headwinds—higher oil prices, sticky inflation, and higher-for-longer interest rates—and yet the labor market is adding jobs, GDP is growing, and corporate profits are expanding at a rapid pace.”

“The economy may slow somewhat from its prior path, due to the Iran war and subsequent oil price shock,” said Rick Rieder, chief investment officer of global fixed income at BlackRock. But, “there are many much larger structural components that should keep the aggregate economy in much better shape than many people expect.”

“Sure, the oil price outlook and geopolitical tensions do matter for rates and FX markets,” said Max Kettner, HSBC’s chief multi-asset strategist. “But for equities – especially the US large-cap universe – and by extension credit and the broader risk-asset spectrum too, what really matters is broader activity and the earnings backdrop.”

The high in stock markets “does make sense,” Grace Peters, global head of investment strategy at JPMorgan Private Bank, told Bloomberg TV. “The underlying driver is more capex being spent. That’s not just associated with the AI buildout, but governments directing capital and companies following suit.”

“I can’t think of a time when you’ve had this long of a string of earnings growth,” said Thomas Martin, senior portfolio manager at Globalt Investments LLC. He expects the current rally to be sustained as quarterly earnings growth continues in the double digits for 2026. AI is “going to drive growth for a while.”

“The market melt-up driven by robust earnings, AI enthusiasm and hopes for a short-lived energy shock faces a tougher test in the week ahead,” said Laura Cooper, global investment strategist and head of macro credit at Nuveen. “Hotter US inflation could push yields higher, while weaker retail sales may begin to reveal the impact of higher gas prices on consumers.”

“Global equities are performing much better than you would expect. If anything it’s a good indication of the underlying strength in stocks that will presumably be even more evident if the firmer contours of a deal emerge later this week. The Trump-Xi talks still scheduled for Thursday and Friday could serve as a catalyst. ” — Conor Cooper, Macro Squawk

“The tech boom is just too powerful to let the fact that energy prices are high affect the U.S. economy or the U.S. stock market,” said Jay Hatfield, founder and CEO at Infrastructure Capital Advisors. “Everybody’s tuning out the Middle East.” Hatfield believes that the market might be “more flattish” for the next couple months as long as the overhang from the Iran war persists, with such overhang being offset by the “unprecedented” tech boom.

“This market does not want to go down because of the tech boom,” he added.

“Valuation has been thrown out of the window for the time being because there is no doubt that there’s a tightness in supply” in AI infrastructure, said Mark Hawtin, head of global equities at Liontrust Asset Management, which runs and advises about £20 billion ($27 billion). “When does it change? That is the million-dollar question and extremely difficult to answer because I think there’s a huge amount of liquidity.”

“With some of the semiconductor names, it does feel a little bit casino-like,” he said. “It’s not rational on a long-term investing time horizon for these names to be where they are, but as we know, markets can remain irrational for some time.”“Following the +50% rally in AI winners from the end of March lows, both AI, and thus the momentum factor feels vulnerable in the short term as we saw Thursday,” said Michael Romano, head of hedge fund equity derivative sales at UBS Securities. “I can see a case for owning short-term downside in AI winners to hedge.”

“Everything appears to be very fragile, and that’s very unsettling,” said Joseph Tanious, chief investment strategist for North America at Northern Trust Asset Management. “It’s hard to reconcile seeing the S&P 500 flirt with record highs when there’s a war going on in the Middle East,” he added, noting the impact of higher oil, gas and diesel prices on many families.

Trump said Monday that the ceasefire is on life support. But the president’s decision to not treat the fighting last week as a violation of the ceasefire was telling, Wolfe Research analyst Tobin Marcus wrote. wrote. “Despite the frustration and the low-level exchanges of fire, we don’t expect a return to hot war,” Marcus wrote. The big sticking point is Iran’s enriched uranium, Marcus said. Tehran has indicated a willingness to turn the uranium over to a third country on the condition it will be returned if the U.S. exits a deal, he said.

But Trump wants the U.S. to take physical possession of the uranium, the analyst said. Iran, however, views this as a red line, he said.