Markets Update - 5/12/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

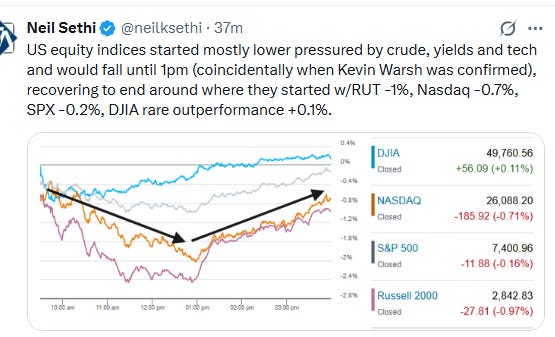

US equity indices were under pressure all session from a combination of rising oil prices and bond yields, the latter of which were pushed higher not only from the rising crude prices but also a hotter than expected core CPI print that reflected the largest monthly rise since January 2025. That came along with headline (all items) CPI rising the most on an annual basis since May 2023 on the back of a continued jump in energy but also the largest rise in grocery prices in four years (along with airfares, hotel prices, etc., as detailed in the link). 10-year and 30-year Treasury yields would close at the highest levels since July (more on yields in the subscriber section).

Yields also were boosted by Fed rate hike bets which now see a hike as an ~70% probability by next June. The chances for two hikes by then is 38% (more in the subscriber section). As a side note, Kevin Warsh was confirmed by the Senate as the new Fed chair.

Not helping matters Iran (via the Fars news agency) set five conditions for the continuation of talks with the US including ending the war on all fronts (including Lebanon), lifting of all sanctions, the release of frozen funds, compensation for damages and losses resulting from the war, and the acceptance of Iran's sovereign right over the Strait of Hormuz, most of which are unacceptable for the US.

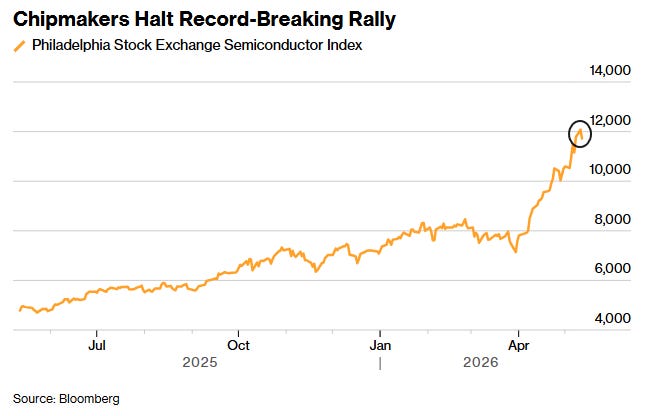

Whether it was due to the rising yields or just profit taking after a nearly unprecedented run, indices were also pressured by a pullback in many of the highest-flying technology stocks (details in the subscriber section).

After falling to session lows mid-day, indices would battle back to finish around where they started, though mostly in the red with just the Dow Jones Industrial Average (+0.1%) making it into the green, a rare outperformance due to its larger share of health care and consumer staples companies which led today (more in the subscriber section).

Elsewhere, the dollar would also finish higher and copper would hit new all-time closing highs. Gold, bitcoin, and US natural gas futures would finish lower (all covered in the subscriber section).

The market-cap weighted S&P 500 (SPX) was -0.2%, the equal weighted S&P 500 index (SPXEW) -0.1%, Nasdaq Composite -0.7% (and the top 100 Nasdaq stocks (NDX) -0.9%, the SOX semiconductor index -3.0% (from an all-time high), and the Russell 2000 (RUT) -1.0%.

Some market commentary:

“Inflation is roaring back largely driven by stubbornly high oil prices,” said Skyler Weinand at Regan Capital. “As a result, we expect the Federal Reserve to be on hold through the summer on interest rates.”

“It isn’t like it’s an avalanche, but it’s a steady move upward,” Thomas Martin, senior portfolio manager at Globalt Investments, said to CNBC, adding that inflation is just “going to keep on building” the longer the conflict in the Middle East continues amid a lack of progress in negotiations between the U.S. and Iran. “As these gas prices and other prices are higher, it’s going to crimp more and more people, so the setup is for there to be continued struggles for the consumer,” he said.

“The increase in the core CPI suggests high energy prices are making themselves felt throughout the economy,” said Ellen Zentner at Morgan Stanley Wealth Management. “It doesn’t mean the Fed will pivot to rate hikes, but it does reinforce the reality that new Fed leadership won’t result in an immediate dovish shift.”

Chris Zaccarelli, chief investment officer at Northlight Asset Management.

“The stock market has rallied an impressive 16.9% since the March lows on much better-than-expected earnings, but at best the Fed is on hold for an increasingly long period of time and at worst the next move from the Fed may be a rate hike (albeit not until next year),” Zaccarelli wrote in an email.

He said that the stock market doesn’t need rate cuts to keep climbing as long as earnings growth stays strong.

April’s inflation report will probably make policymakers at the Federal Reserve more concerned about “renewed signs of food inflation accelerating, given the risk that higher gasoline and food prices together will further boost households’ inflation expectations,” Capital Economics chief North America economist Stephen Brown wrote Tuesday. The 2.1% rise in monthly electricity prices, compared with March, and 0.5% gain in monthly food prices from the prior month were both upward surprises, Brown said. “President Trump might feel in a greater rush to sign the reported executive order to remove tariffs on beef imports, with a 2.7% [month-over-month] jump there adding to the impact of a larger 1.8% m/m rise in fruit & vegetable prices. The latter appears to mainly reflect drought conditions in much of North America with, for example, tomato prices soaring by 15% m/m for the second month running,” according to Capital Economics.

Greenlight Capital president David Einhorn said he missed the market’s recent rebound, but remains concerned about lofty valuations. “I have thought the market is very highly valued for a few years, honestly,” Einhorn told CNBC on Tuesday on the sidelines of the Sohn Conference in New York. Einhorn said being on defense over the last six weeks hasn’t been the “best position” as he has not benefitted from the market’s “V”-shaped recovery. But he said stocks remain “very, very pricey” on a historical basis. “Sooner or later, I think we’ll wind up with a better opportunity,” Einhorn said.

“After such a powerful earnings-driven rally, equities may simply need a breather,” said Bret Kenwell at eToro. “While the labor market and broader economy still look stable — if not exactly robust — a disjointed Fed and rising inflation complicate matters.”

“Every major cloud provider has signaled that AI infrastructure remains supply-constrained, not demand-constrained,” writes Ameriprise Chief Market Strategist Anthony Saglimbene. “Simply put, it likely means the investment cycle has a demand floor that extends well beyond the current quarter.”

“For now, the party is still going,” said Robert Pavlik, senior portfolio manager at Dakota Wealth Management. Yet the party also feels like it started around 7 p.m., he said, and it’s now getting closer to 10:30 p.m. “People are still having a good time,” Pavlik said Monday. But for anyone who got to the party early, “you start thinking about how long you are going to hang around,” he said.4

A solid earnings season has continued to push stocks to new highs in recent sessions. Marci McGregor, head of portfolio strategy, chief investment office, at Merrill and Bank of America Private Bank, said on CNBC’s “Closing Bell” on Monday afternoon that she’s still feeling good about the markets overall.

“If we get weakness after this really strong recovery from the March lows, I would see it as a buying opportunity, because this is a market that is being fueled by corporate profits, by capex, and frankly by a strong labor market,” she said. “There’s a lot of reasons to be positive.”