Markets Update - 5/13/26

A detailed look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

US equity indices started the day again under pressure following another hot inflation reading, this time in the April producer prices index (PPI) which came in nearly triple expectations at +1.4% from a month earlier (m/m), the largest increase since March 2022, on a broad based advance that even excluding food and energy prices saw core prices +1.0% m/m, the most since March 2022, and +5.2% over the past year, the most since December 2022.

10-year and 30-year Treasury yields would push to new highs since July and May respectively and are threatening to “break out” of well established ranges (more on yields in the subscriber section).

The report continued to see markets coalescing around the idea that the next move from the Fed will be a rate hike with a 33% probability of a hike this year and 50% throughout 2027 as bets on a reversal of any hike faded (more in the subscriber section). As a side note, Kevin Warsh was confirmed by the Senate as the new Fed chair in the narrowest ever confirmation vote.

There was little progress on the Iran situation, which can be expected through at least the end of the week as President Trump is now in China to meet with Chinese President Xi. Their sit down is tomorrow (see details in the morning update).

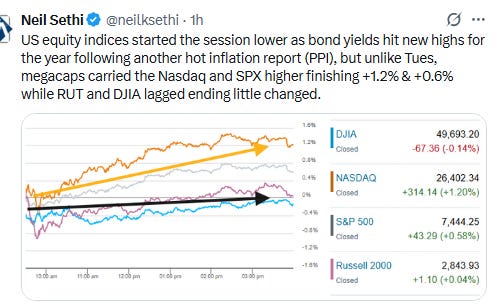

While there was much that was similar about today’s set-up as described above, investors gave a very different reaction as it came to the big winners year-to-date, buying Tuesday’s tiny dip and sending the Nasdaq and S&P 500 to new record highs (details in the subscriber section). The Mag-7 index would finish +2% and the SOX Semiconductor index +2.6%. Meanwhile the equal-weighted version of the S&P 500 index would finish -0.4%.

Elsewhere, the dollar would also push higher and copper futures set a new all-time closing high for a fourth straight session. Gold and US natural gas futures would see smaller gains, while crude and bitcoin futures would end lower (all covered in the subscriber section).

The market-cap weighted S&P 500 (SPX) was +0.6%, the equal weighted S&P 500 index (SPXEW) -0.4%, Nasdaq Composite +1.0% (and the top 100 Nasdaq stocks NDX) +1.0%, the SOX semiconductor index +2.6%, and the Russell 2000 (RUT) +0.1%.

Some market commentary:

“Wednesday’s PPI was strikingly elevated as producers are feeling the ripple effects of $100 per barrel oil, which is raising the cost of production across the board, as energy is arguably the most critical input cost,” said Clark Bellin at Bellwether Wealth. “The Federal Reserve has an inflation problem on its hands.”

“One takeaway is that companies are not passing through costs to consumers across the board just yet,” noted Chris Low at FHN Financial. “But company input costs are sharply higher, which obviously increases pressure to pass through costs in future.”

Olaolu Aganga, head of portfolio construction at Citi Wealth, believes that AI spend expanding outside of the tech sector leaves room for investors to buy into other opportunities in the market. “We have global views that we think are lasting and enduring, so energy security and infrastructure — those companies that can benefit from the capex spending with regards to energy and the grid and energy independence,” she said on CNBC’s “Closing Bell: Overtime” on Tuesday afternoon. “So if you’ve missed this particular wave, there are some themes that we believe will be playing out over time, frankly, that we need to focus on, that we think we have durable earnings there as well.”

“The consumer has not tapped out yet,” said Erik Aarts, senior fixed-income strategist at Touchstone Investments. Aarts expects business investment to continue this year, and with that backdrop, he thinks rates “should be right here.”

Wednesday’s tech moves comes after Nvidia CEO Jensen Huang joined President Donald Trump on his trip to China to meet Chinese President Xi Jinping. The decision signaled to investors that there could be positive developments regarding Nvidia being able to sell its artificial intelligence chips in Chinese markets, according to Mayfield, whose expectations for the meeting are still “fairly muted.” Semiconductor stocks in particular have been on a tear of late, leading the broader market back to record highs, amid renewed enthusiasm in the AI trade. However, even though chip stocks and those related to the AI infrastructure buildout are to some degree “moving completely on their own,” Mayfield is unconvinced that the recent momentum will last much longer. “At some point those investors will look up and, if they find a macro environment that has really turned against them, might look around and be like, ‘Alright, it’s time to take a few gains, because the promise that the war would be over quickly has clearly not materialized,’” he said.

“Yesterday’s price action leaned toward a ‘defensive’ trade... with the market increasingly feeling toppy to us over the very near-term and Tech stocks overdue for at least a consolidation of gains,” wrote Wolfe’s chief investment strategist Chris Senyek. “The short-term bull case from here rests on Oil prices falling rapidly from the end of the Iran conflict and/or [Nvidia’s] EPS print (and commentary) on 5/20 materially surprising to the upside further fueling animal spirits.” Senyek added that he thinks investors are becoming increasingly sensitive to inflation reports.

While investors are closely watching President Donald Trump’s two-day summit with Chinese leader Xi Jinping in Beijing, they are “tending to look through a little bit of the Trump noise,” according to Chelsea Wiater, senior portfolio manager at the EFG New Capital US Growth Fund. Trump “tends to come out with very prolific statements that tend to get walked back later,” Wiater said in a phone interview. “I would anticipate some rhetoric in those veins. But I also think that he’s attempting to position himself with China in a positive light, and so it might be a more friendly conversation than some investors currently anticipate.” Rather than reacting to every headline from the summit, investors are instead focusing more on AI expansion and the expected pickup in U.S. manufacturing investment, including efforts by companies to bring more production back to the U.S. or build new capacity domestically, Wiater added.