Markets Update - 5/15/26

A detailed look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for next week.

Quick Summary:

US equity indices started the day joining a global equity selloff pressured by another leg higher in global bond yields as detailed at length in the morning update.

Bond yields would continue to climb throughout the session along with crude prices with the 30-year US Treasury closing at a yield of 5.12%, the highest since 2007. The benchmark 10-yr yield would close at 4.60% and the 2-year yield (sensitive to Fed rate cut pricing) at 4.08%, both the highest closes since February 2025. In that regard, pricing for a Fed rate hike by the end of the year moved to 50% while the chances of a cut are less than 1% (detailed in the subscriber section).

Investors took the opportunity to book profits in some of the highest flying technology stocks over the past few weeks. Notably, Intel retreated 6%, while Advanced Micro Devices and Micron Technology lost 5.7% and 6.6%, respectively. Nvidia dropped 4.4%, while Cerebras Systems — which surged 68% Thursday after it began trading on the Nasdaq — shed 10% (more in the subscriber section).

There was also according to news outlets disappointment that President Trump’s China trip didn’t yield much in terms of progress towards an end to the Iran standoff as Trump said he didn’t push his Chinese counterpart Xi Jinping to pressure Tehran to revive Hormuz. Meanwhile, “the few headlines that did come out of the summit (like the order for 200 Boeing aircraft which was below expectations) were underwhelming,” wrote Adam Crisafulli of Vital Knowledge.

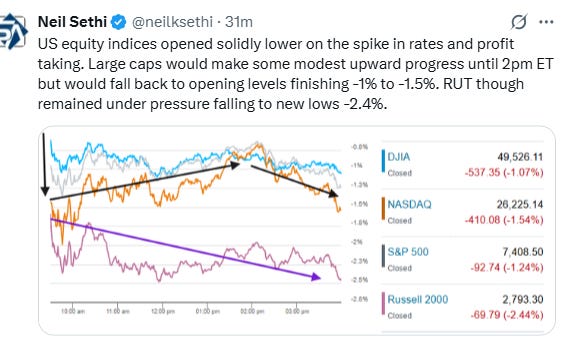

Despite no letup in yields and the selloff in some tech heavyweights, large capitalization indices (S&P 500 (SPX), Nasdaq, Dow Jones Industrial Average (DJIA)) would make some modest upward progress until 2pm ET but would fall back to opening levels from there finishing -1% (DJIA) to -1.5% (Nasdaq). Smaller caps though, more sensitive to interest rates, remained under pressure all day, with the Russell 2000 (RUT) falling to new lows -2.4%, its worst session since November.

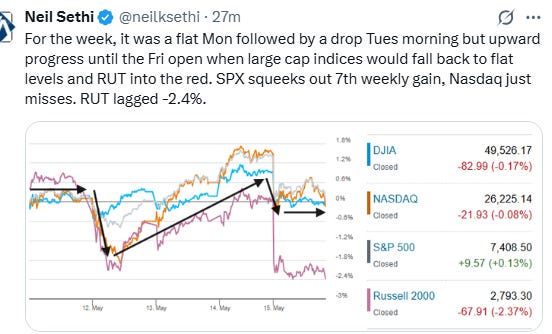

The losses would bring the large cap indices to right around unchanged levels for the week, with the SPX eking out a modest gain (+0.1%) to keep alive its 7-week win streak (longest since 20203) while the Nasdaq and DJIA would finish just on the other side -0.1% and -0.2% respectively ending their respective six- and five-week streaks. The RUT would finish down -2.4%.

In US economic data, April industrial production (our most complete look at the manufacturing sector) came in more than double expectations at +0.68% m/m (vs +0.3% expected), the strongest since February 2025, boosted by autos, tech, and other industrial items which boosted 2Q GDP estimates.

It was also Jerome Powell’s last day as Fed chair after a tumultuous run that started on Volmageddon and included among other things a pandemic, surging inflation, mini-banking crisis, multiple wars, and a criminal investigation. Kevin Warsh will take over now and Governor Miran will depart, removing the most vocal proponent of lower rates.

Elsewhere, the dollar would continue its breakout, and US natural gas futures were also higher. Gold, copper, and bitcoin futures would all decline (all covered in the subscriber section).

The market-cap weighted S&P 500 (SPX) was -1.2%, the equal weighted S&P 500 index (SPXEW) -1.1%, Nasdaq Composite -1.5% (and the top 100 Nasdaq stocks NDX) -1.5%, the SOX semiconductor index -4.0%, and the Russell 2000 (RUT) -2.6%.

Some market commentary:

“The move higher in global bond yields is a little unsettling,” said Prashant Newnaha, senior Asia-Pacific rates strategist at TD Securities in Singapore. “An extended and persistently high oil price could be the nail in the coffin for bonds.”

“Risk sentiment is being dented by a global rise in bond yields, driven by a combination of inflation concerns, rising expectations for central-bank rate hikes, and growing worries around government debt as countries look to cushion the impact of higher energy prices,” said Angelo Kourkafas at Edward Jones. “The recent rise in yields may be approaching levels that begin to weigh on equity performance,” he said. “Prior to the conflict, global oil supply was exceeding demand, and when conditions normalize in the Strait of Hormuz, oil prices are likely to retrace toward prior levels,” he noted. “As long as earnings momentum remains strong, investors have good reason to avoid becoming overly negative.”

Bullish calls on US stocks will be challenged if Treasury 10-year yields hit 5%, a level that usually depresses price-to-earnings ratios and “seems to spook people,” Lori Calvasina at RBC Capital Markets told Bloomberg Television.

“We were a little bit surprised that the market kind of shrugged off the inflation numbers from earlier this week,” said Adam Phillips, managing director of investments at EP Wealth, during an interview with MarketWatch. “But these things don’t matter until they do.”

“What is really, really going to be important for Kevin Warsh is keeping inflation expectations in check,” Subadra Rajappa at Societe Generale Americas told Bloomberg Television. “When inflation expectations start to get a bit unhinged, then he has a problem on his hands.”

“There’s no question that momentum has been so aggressive on the upside that the risk of a correction is there,” Paul Skinner of Wellington Management told Bloomberg TV. “With a background of bond markets looking unsettled, with the problem of inflation, with the Strait of Hormuz not having a solution out of that Summit, I think there definitely is some volatility to come.”

“The group has witnessed an extremely unsustainable move in recent weeks and remains vulnerable to profit taking regardless of the headlines,” wrote Adam Crisafulli of Vital Knowledge.

“That broadening trade has really fizzled out,” Keith Lerner, investment chief at Truist Advisory Services told CNBC’s “Closing Bell: Overtime” on Thursday. “We are seeing some of that, kind of, more subdued action in the economy reflected in areas of the market. But ... it’s top heavy with tech, and that’s why the broad-based indices are doing fine.”

“While it may be difficult for incoming Fed Chair Warsh to cut interest rates in the near-term given the hot economic and inflation data, we believe the markets can withstand this, and can still move higher even if the Fed stays on hold through year-end,” Rick Gardner, chief investment officer, of RGA Investments, stated.

“There are signs of extended positioning and extreme optimism, which could lead to a natural and healthy period of consolidation,” said Mark Hackett at Nationwide. “Ultimately, however, if the macro and earnings environment remain supportive, the path of least resistance is higher.”

Argent Capital Management’s Jed Ellerbroek believes sentiment among investors “remains very optimistic overall,” a peek under the hood is showing that the broader market is lagging the largest tech companies, a divergence that is increasingly worrying some investors as it suggests a fragile rally. “It doesn’t feel right to say that tech is just going to lead forever,” the portfolio manager said, noting that the “HALO” trade earlier this year saw tech stocks “shunned” in support of those in sectors such as consumer staples and materials. “One thing kind of popping up and driving the market is inherently more risky than if there were several things.”