Markets Update - 5/22/26

A detailed look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for next week.

Quick Summary:

US equity indices would start the Friday session trading modestly higher ahead of the long weekend in the US, as bond yields eased for a third day and oil prices remained calm on continued hopes for a US-Iran deal as covered in the morning update.

Indices would fall back at 10am on a double dose of bearish headlines. First, Governor Waller, previously one of the most dovish members of the FOMC, made an important speech where he indicated with the labor market "stabilizing" and inflation "not headed in the right direction," he would "support removing the 'easing bias' language in our policy statement to make it clear that a rate cut is no more likely in the future than a rate increase." He added, “I can no longer rule out rate hikes further down the road if inflation does not abate soon, and that is especially true if measures of inflation expectations, some of which have risen lately, show signs of becoming unanchored." More on that speech and what it would take for him to support a rate cut in the subscriber section.

Second, the consumer sentiment index from the University of Michigan would come in at a record low (as did both index components) with long-run inflation expectations jumping to a 7-month high.

Equities would nevertheless rally again, boosted at one point by a headline that the Pakistani Army Chief and the Iranian Revolutionary Guard Commander would be meeting tomorrow, but almost immediately thereafter a headline crossed of Iran’s Foreign Minister saying “We cannot necessarily say we have reached a point where a deal is near.”

Equities would fall back, although hold in positive territory, led for a third straight session by the small cap Russell 2000 (RUT) +0.9% (+4.4% past three sessions). The Dow Jones Industrial Average (DJIA) would again finish next +0.6% (at a record high), the S&P 500 (SPX) +0.4% (but the equal-weight index +0.9%) and the tech-heavy Nasdaq would once again lag +0.2% (even as the SOX semiconductor index would end +2% at a new all-time high).

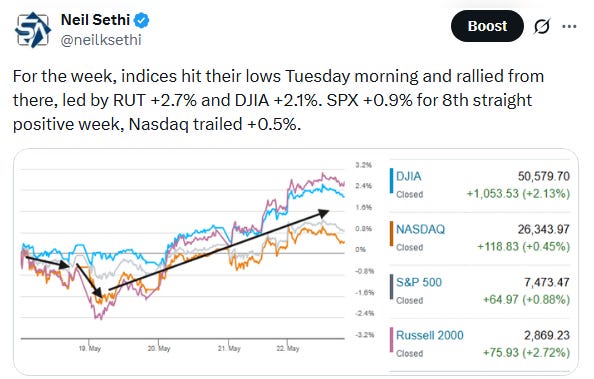

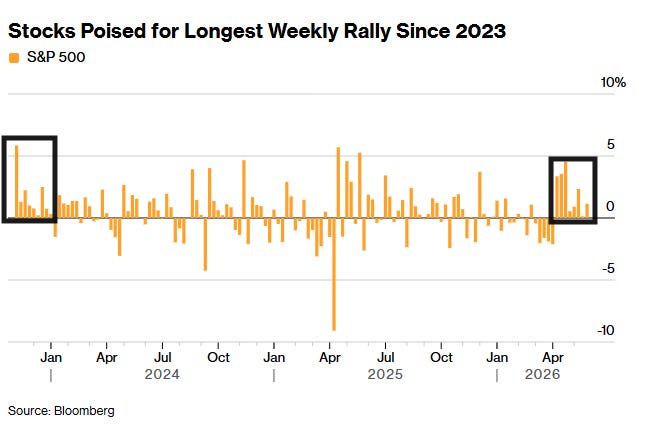

For the week, indices hit their lows Tuesday morning and rallied from there, led by the RUT +2.7% followed by the DJIA +2.1%, SPX +0.9% (its 8th straight positive week the longest streak since the end of 2023), while Nasdaq trailed +0.5%.

Elsewhere, the dollar would edge higher and copper futures would also gain while gold, US natural gas, and bitcoin futures would fall back (all covered in the subscriber section).

The market-cap weighted S&P 500 (SPX) was +0.4%, the equal weighted S&P 500 index (SPXEW) +0.9%, Nasdaq Composite +0.2% (and the top 100 Nasdaq stocks NDX) +0.4%, the SOX semiconductor index +2.0% (to a new all-time high), and the Russell 2000 (RUT) +0.9%.

Some market commentary:

“The market is fully aware that headlines will remain volatile, and while oil needs to react for practical reasons, equities have probably moved on,” said Geoff Yu, senior macro strategist at BNY. “The lack of an agreement does not imply re-escalation, so the focus for now will stay with earnings and data.”

“Our view on Iran is the same as before: a deal is much more likely than not, but this is already priced in, and the conflict will have stagflationary effects for at least the next few quarters,” Adam Crisafulli, founder of Vital Knowledge, said in a note.

Investors are looking past macro headwinds and rewarding rhetoric around peace prospects, and that has acted as a tailwind for equities, according to Craig Johnson at Piper Sandler. “The stock market is exhibiting a ‘hope-driven’ rally,” he said.

“In a more risk-averse environment, we might expect traders to pare risk and square positions,” Steve Sosnick at Interactive Brokers said. “Instead, they are quite willing to add to long positions, implying that they are unwilling to risk missing a peace-dividend rally.”

“The administration is well-focused on the bond market, even more than equities in my view, so they won’t allow the curve to steepen much further,” said Andrea Gabellone, head of global equities at KBC Securities.

“We’ve got the biggest capital spending boom since the financial crisis,” said Guy Miller, chief market strategist at Zurich Insurance. “That’s leading to record corporate profitability; we are in this virtuous circle where it’s generating profitability for other suppliers, other companies too.”

Brian Mulberry, senior portfolio manager at Zacks Investment Management, said investors found plenty to like in the latest earnings reports from a number of major U.S. retailers, including Walmart, Home Depot, Target and Lowe’s. While the strong results didn’t do much to lift retail stocks — disappointing guidance was blamed for Walmart’s post-earnings drop — the broader market cheered. “It’s pushing back against the idea that we’re looking at stagflation or recession,” Mulberry told MarketWatch during an interview.

“Waller’s latest remarks confirm the hawkish shift at the Fed,” said Krishna Guha at Evercore. “At the same time though, his policy posture was not as hawkish as his tone, with Waller saying he is prepared to wait and see for now.”

Still, Guha noted the remarks underline the challenges facing Kevin Warsh, who was sworn in as the new Fed chair on Friday.