Markets Update - 5/28/26

A detailed look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

US equity indices would start Thursday’s session little changed after another exchange of fire earlier in the day between US and Iran as discussed in the morning update.

Equities were also digesting a deluge of economic data:

April personal income growth from March came in well under expectations in large part due to what should have been an expected end to farm assistance payments which surged in March, as compensation grew although was negative when adjusted for inflations.

April personal spending came in as expected with modest growth when adjusted for price rises.

April PCE prices (the Fed’s preferred inflation index) came in slightly below expectations as did core (ex-food and energy) but compared to a year earlier core inflation was the highest since November 2023.

April durable goods orders (lasting more than 3 years) came in well above expectations boosted by transport and defense orders, but core business orders were weak, a change from the past few months (report tomorrow).

Weekly jobless claims once again were little changed, remaining very low historically, with y/y continuing claims the lowest since Dec ‘22.

Q1 GDP was revised lower to 1.6% Q/Q growth (annualized) from +2.0% initially on weaker consumer and IT spending than was originally estimated (report coming).

Later in the morning we would get April new home sales which would drop -6.2% from March and -11.3% from a year ago to a seasonally adjusted annual rate of 622,000, well below expectations of 663,000 (report tomorrow).

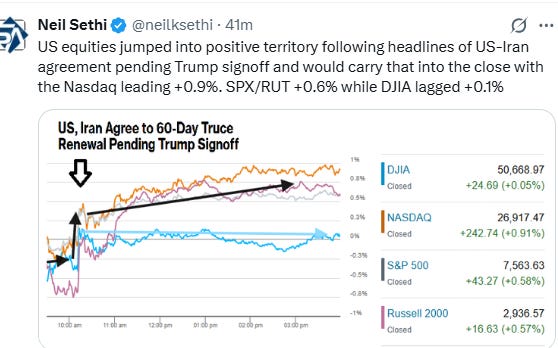

Today, though, some apparent tangible progress on the Mid-East impasse would send indices higher. Axios, citing two U.S. officials and a regional source, reported that the U.S. and Iranian negotiators agreed on a 60-day memorandum of understanding to extend the ceasefire, and further negotiations on Iran’s nuclear program. However, the report indicated President Donald Trump has yet to agree to the terms (which many speculate means that it has not yet been blessed by Iranian officials either). Treasury Secretary Scott Bessent on Thursday would only say “the teams have been going back and forth” when pressed if an interim deal has been clinched. The US-Iran memorandum of understanding would state that shipping through the vital Strait of Hormuz would be “unrestricted,” Axios reported. Iran would have to remove all mines from the strait within 30 days, according to the report.

Fada-Hossein Maleki, an Iranian lawmaker and member of the country’s parliamentary commission for national security, said negotiations between the US and Iran have shown “significant progress,” according to the semi-official Iranian Students’ News Agency. The US still has to decide on a number of Iran’s conditions, the ISNA quoted Maleki as saying, without giving details. WTI crude prices pared gains to trade near $95 a barrel, having earlier risen after the two sides accused each other of breaching the ceasefire.

Indices would be led Thursday by the Nasdaq on the back of another run higher in tech stocks boosted by the best day on record for Snowflake as discussed this morning (and which looks set to continue tomorrow following Dell’s blowout report discussed in the subscriber section). The Nasdaq would finish +0.9%, the small cap Russell 2000 (RUT) and S&P 500 +0.6% while the Dow Jones Industrial Average would lag +0.1% but enough to join the others with a quartet of all-time highs.

Elsewhere, bond yields would ease for a fifth session and the dollar and bitcoin futures would also finish lower while US natural gas futures would jump to the highest close since early February, and gold and copper futures would also end higher (all covered in the subscriber section).

The market-cap weighted S&P 500 (SPX) was +0.6%, the equal weighted S&P 500 index (SPXEW) +0.4%, Nasdaq Composite +0.9% (and the top 100 Nasdaq stocks NDX) +0.8%, the SOX semiconductor index +1.0%, and the Russell 2000 (RUT) +0.6%.

Some market commentary:

“The market has been expecting some type of MOU — memorandum of understanding — here,” said David Wagner, head of equities at Aptus Capital Advisors. “You’re going to see the discretionary names run as a first knee-jerk reaction to a lot of this news, which can drive the market higher.”

“The market has been caught between two very different worlds,” said Aneeka Gupta, director of macro-economic research at Wisdomtree. “One where we get a deal, and you have a follow-through of a very powerful cyclical recovery, and another where the conflict process deepens the stagflation impact on the economy.”

“If a peace deal takes another two weeks or two months, I don’t think markets care as much anymore unless oil meaningfully breaks higher,” Mathias Heim, chief investment officer at Belle Capital said. “The elephant in the room is the AI capex cycle, which drives profit growth and multiples. Structurally, equities remain the go-to asset class.”

“From a pure technical perspective, if we had to own one here, our money is on Small Caps,” Wolfe Research’s Rob Ginsberg wrote on Wednesday.

“Although the core rate was on the softer side of consensus, I would not take much solace from today’s result, as core inflation is likely to be firmer next month and risks to the upside from the lagged impact of the energy surge remain in place,” said Omair Sharif, president of Inflation Insights LLC.

“Core inflation moderated slightly, though the Iran war kept headline price pressures elevated. However, real spending growth has continued to moderate as higher goods prices weigh on volumes. Overall, the April data suggest a resilient labor market is still generating enough income to keep consumers spending, with elevated prices only modestly denting real activity.” — Chris G. Collins and Stuart Paul, BBG

“While prices are rising faster than comfortable, incomes are not, putting consumers in an uncomfortable spot,” said Elizabeth Renter, a senior economist at the personal finance website NerdWallet. “Rising prices, sluggish income and economic uncertainty could set the stage for a broader pullback in consumer spending and therefore economic growth.”

“We think it’s unlikely the Federal Reserve hikes rates, given how the oil price spike is likely to be short-term, and since there is immense pressure on the Fed to keep rates in check and a hike would require an especially rare set of circumstances, such as a year or longer of $100 per barrel oil, and we are nowhere near that point yet,” said David Laut at Kerux Financial.