Markets Update - 5/29/26

A detailed look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for next week.

Quick Summary:

US equity indices would start Thursday’s session again little changed as markets awaited a clearer signal as to whether the US and Iran were going to sign some sort of peace agreement as discussed in the morning update.

Things wouldn’t get any clearer during the session with President Donald Trump saying he would soon make a “final determination” on a preliminary deal to extend a ceasefire with Iran among continuing mixed messages from both sides. Trump reiterated Tehran “will never have a Nuclear Weapon or Bomb” and the Strait of Hormuz must be open and any mines destroyed, while an administration official told the New York Post it was the “closest” the two sides have been. Separately, Treasury Secretary Scott Bessent suggested the US could remove some sanctions on Iran depending on how matters proceed in the current standoff.

A senior Iranian source likewise told Reuters an agreement was close but had not yet been approved. Iran's semi-official Fars news agency said the strait would be reopened under Tehran's conditions after the U.S. lifts its blockade on Iranian ships. Fars also said there was agreement to release $12 billion of Iran’s frozen assets.

Separately, Bloomberg reported at least two shipowners, who asked not to be identified discussing sensitive information, said they were in touch with American military forces, which advised them on how best to navigate the Strait. If sustained, the increase in transits could signal that more shipping companies are willing to make the journey, boosting the flow of everything from oil and gas to consumer goods

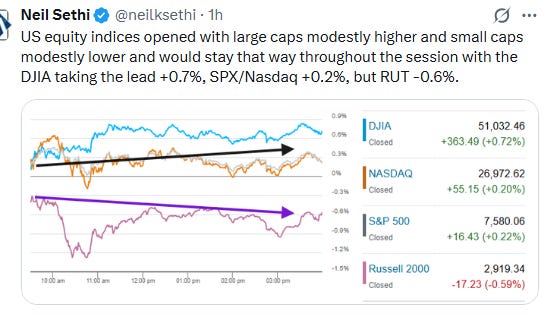

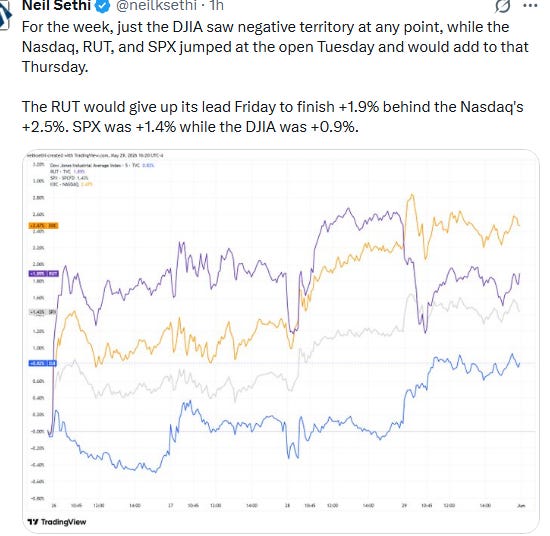

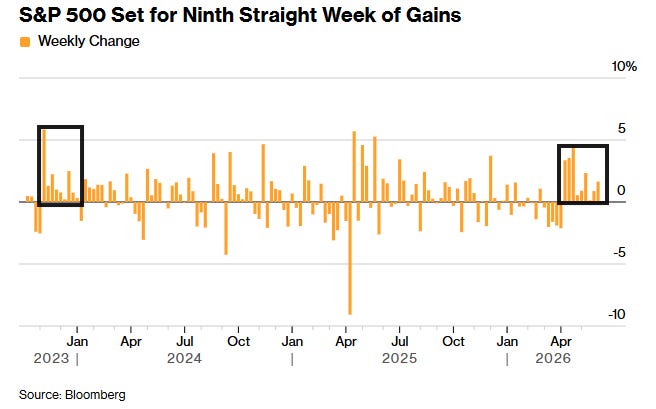

The large cap indices would see modest gains while the small cap Russell 2000 (RUT) would log a loss of -0.6% but still finish with a gain of +1.9% for the week just behind the Nasdaq’s strong +2.5% performance. The S&P 500 (SPX) and Dow Jones Industrial Average (DJIA) would also see solid gains for the SPX its 9th straight, the longest streak since 2023.

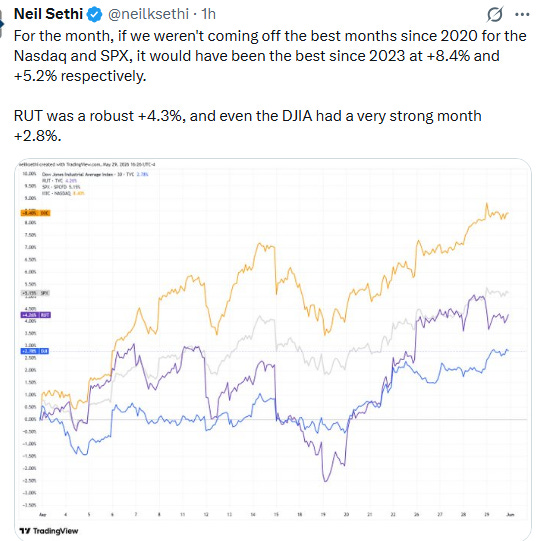

Friday also marked the final trading session of May, and all four averages notched robust gains for the month as well. The Nasdaq outperformed, recording an advance of more than +8% for the month, paired with April’s +15.3% gain, it was the best back-to-back months for the Nasdaq since 2009. The S&P 500 finished up +5.2%, the RUT +4.3%, while the DJIA posted an almost +3% gain.

Elsewhere, bond yields edged lower as did copper futures while gold futures would continue their bounce from support. The dollar, US natural gas and bitcoin futures would end little changed (all covered in the subscriber section).

The market-cap weighted S&P 500 (SPX) was +0.2%, the equal weighted S&P 500 index (SPXEW) +0.2%, Nasdaq Composite +0.2% (and the top 100 Nasdaq stocks NDX) +0.4%, the SOX semiconductor index UNCH, and the Russell 2000 (RUT) -0.6%.

Some market commentary:

“We suppose there is still the risk that this deal will fall through. However, it does look like there will be at least an extension of the ceasefire,” said Matt Maley at Miller Tabak. “The only question now is whether the stock market has already priced in this outcome.”

“Brent below $90 by the end of next week seems at our reach,” wrote Florian Ielpo, head of macro at Lombard Odier Investment Managers. “It would create a rather supportive environment should it happen, clearly as oil prices have been the source of most macro fears this year.”

“The recent pullback in oil prices is helping to ease some of those worries,” said Angelo Kourkafas at Edward Jones. “However, with inflation moving further away from the Fed’s 2% target and labor-market trends stabilizing or even improving, policymakers may begin to shift away from their easing bias at the June meeting.”

“The enthusiasm for stocks is warranted,” said Emily Bowersock Hill at Bowersock Capital Partners. “Investors expect the AI infrastructure boom to continue to mask the negative impact of geopolitical disruption. Stock markets care about company profits. As long as earnings grow, stock prices can continue to rise.”

“Dell is like the poster child for [the] AI broadening earning story,” said David Nicholas, CEO and Founder of XFUNDs by Nicholas Wealth. “We started with chips, memory, but it’s really now about the broad kind of AI infrastructure stack.”

“There’s always that black swan risk that something pops off, but my gut tells me that this thing should be coming to an end very quickly,” Nicholas said. “The market has priced a lot of that in, but I just think it unlocks the market to continue moving higher.”However, Kate Moore, chief investment officer at Citi Wealth, believes that the market’s rally to new heights may continue to be dictated more by strong earnings growth versus headlines about any Middle East tensions.

“I think a lot of the snapback we saw since the lows in March was this acceptance that there was going to be a resolution at some point, but obviously the scope of that and the timing of that is still anybody’s guess,” she said on CNBC’s “Closing Bell: Overtime” on Thursday afternoon. “I really do think what’s been driving the market higher is, frankly, the power of the technology earnings … this has been happening company after company throughout the course of this earnings season.”