Markets Update - 5/4/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow

Quick Summary:

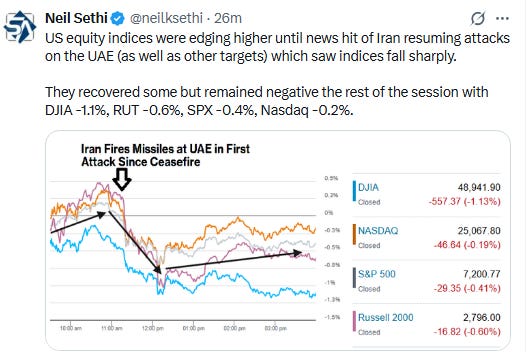

US equity indices opened modestly lower amid whipsawing headlines following the US initiation of “Project Freedom” but dropped solidly negative after news hit of Iran resuming attacks on the UAE (as well as other targets). The news wouldn’t get much better keeping indices underwater the rest of the session, although losses were relatively mild.

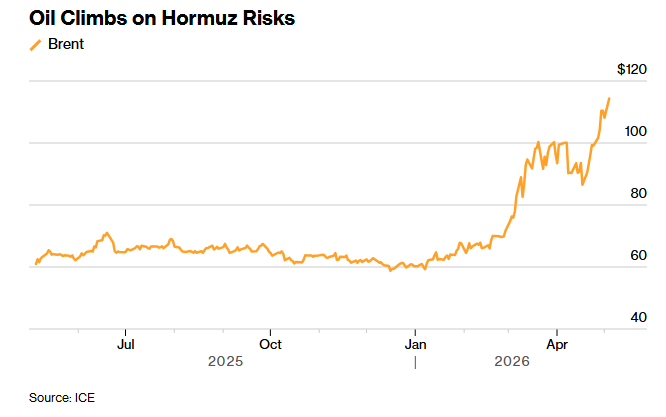

The resumption of military conflict saw oil prices jump, pushing up bond yields to the highs of the year with the 30-year Treasury yield breaching 5%. Fed funds pricing continued to pivot towards rate hikes as soon as this year.

In economic data I caught up on the Employment Cost Index, the Fed’s favorite employment wage index which ticked higher but growth remained near post-pandemic lows compared to the prior year, while March factory orders showed total manufacturing orders much stronger than expected boosted by energy goods but also showed the strongest business cap ex since June 2020.

US equity indices opened trading opened trading for the week modestly lower amid whipsawing headlines following the US initiation of “Project Freedom” to free trapped vessels in the Persian Gulf as detailed in the morning update.

And headlines would start to deteriorate about an hour later as Iran resumed attacks on the United Arab Emirates and some vessels in the region followed by reports of fire exchanged between US and Iran forces as US military fought off attacks from Iranian drones, missiles and armed small boats as it facilitated the passage of two US-flagged vessels through the Strait of Hormuz, US Central Command chief Admiral Brad Cooper told reporters in a briefing on Monday. Despite that indication from US CentCom President Trump told Fox News Iran will be “blown off the face of the earth” if they attack American ships guiding vessels.

The news sent oil prices up as much as 6% and pressured bond yields which rose to the highest closes of the year with the 30-year Treasury in particular breaching technical levels and trading above 5%. Meanwhile Fed fund futures would price in a 26% chance of a rate hike by December (from a 16% chance of a cut Friday).

Elsewhere, the dollar and US natural gas and bitcoin futures were also higher while gold and copper futures fell (all covered in the subscriber section with charts).

The market-cap weighted S&P 500 (SPX) was -0.4%, the equal weighted S&P 500 index (SPXEW) -0.6% (its eight loss in nine sessions), Nasdaq Composite -0.2% (and the top 100 Nasdaq stocks (NDX) -0.2%, the SOX semiconductor index -0.6% (to a new all-time high), and the Russell 2000 (RUT) -0.6%.

Some market commentary:

Markets saw at least 10 intraday swings tied to Iran tensions on Monday, Daniel O’Regan, managing director of equity trading at Mizuho Securities, wrote in a Monday note. “It’s a fool’s errand to track in real time,” he added.

“This equity market is not ready to hear that it may need to endure Fed hikes, although that’s what the Treasury complex is telling it,” Torres wrote in emailed comments to MarketWatch. “Every day that passes without a Middle East peace deal raises the odds that the central bank needs to raise, and that’s likely going to lead to a correction here for stocks, coinciding with a weak seasonal period and a new inflation-fighting Fed chair who will be tested by these developments,” he added.

“I think as people look at the realities of very tight supplies, it’s not just a question of price,” Chevron CEO Mike Wirthtold CNBC’s David Faber at the Milken Institute Global Conference. “It’s actually — can we get the fuel? I think over the course of the next several weeks, we’ll see those effects begin to move throughout the system.”

“Even if the immediate conflict de-escalates, we expect the aftershocks will remain with us for some time,” said Darrell Cronk at Wells Fargo Investment Institute. “The effects — on energy prices, industrial activity, and geopolitical risk premia — are unlikely to fade quickly.”

Investors should brace themselves for a market pullback in the near future, according to Trivariate Research. Stocks saw double-digit monthly appreciation in April, the best for the S&P 500 since November 2020, founder Adam Parker said in a note Sunday. It was the 25th best month ever over the last 1167 months, making the rally a once in every 56 months event, he said.

“All of our previous work tells us that trying to make short-term market calls is a Fool’s Game. Yet, after a rally this strong, we, and many institutional investors can’t help but acknowledge that a pullback after this huge rally seems more likely-than-not,” Parker wrote. “It is just hard to think that we won’t have a bad month in the next couple of months.”

“A diplomatic solution to this conflict remains the most likely outcome,” said James McCann at Edward Jones. “However, the risk of a more prolonged or larger disruption to global energy markets remains important to monitor, in our view, especially with markets having rallied sharply in recent weeks.”

“Unless we experience a meaningful external shock, it will be hard to derail momentum and hand control back to the bears,” said Mark Hackett at Nationwide. “That is what is giving this rally a more durable and credible foundation than what we saw just a few weeks ago.”

“We don’t anticipate the war being resolved quickly,” said Jay Hatfield, founder and CEO at Infrastructure Capital Advisors. “We don’t think Iran is going to have an epiphany and get rid of their nuclear capabilities, and so that’s probably going to have to happen by force, and that’s not going to be well received by the market.” Still, investors’ hopefulness over the situation in the Middle East and a strong first-quarter earnings season have driven stocks higher to new records in recent days. Even if the war is not resolved, Hatfield sees the S&P 500 hitting 8,000 by the end of the year.

“We’ve gone from a market mainly driven by geopolitics to a market focused on earnings and these have been really positive across the board,” said Vincent Juvyns, chief investment strategist at ING in Brussels “Tech has been a driving force, but financial and energy stocks have also lifted indexes and earnings expectations.”

“This is just another dip that investors will want to buy into,” said David Kruk, head of trading at La Financiere de l’Echiquier in Paris. “Yes, the news from Iran led to a spike in oil prices but we’re now used to those. Investors are very much focused on the surprisingly good earnings season we’ve had so far, on the AI trade.”

Investors’ hopefulness over the situation in the Middle East and a strong first-quarter earnings season have driven stocks higher to new records in recent days, with Bank of America strategist Nigel Tupper seeing reason to remain bullish going forward. “The strong global earnings cycle and a few persistent investment themes remain supportive of global equity market returns,” Tupper wrote in a Friday note to clients.

Chris Senyek, chief investment strategist at Wolfe Research, believes that strong earnings from the “Magnificent Seven” tech titans will result in artificial intelligence remaining the most dominant market theme. “With mega cap tech earnings coming in solid, adding more fuel to the AI theme, we believe that investors are likely to continue to chase the perceived tech winners in semis and memory, among others,” he wrote.