Markets Update - 6/15/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

US equity indices would start Monday’s session solidly higher after US and Iran said Sunday they reached an interim agreement to reopen the Strait of Hormuz and extend the current ceasefire for 60 days as discussed in detail in the morning update.

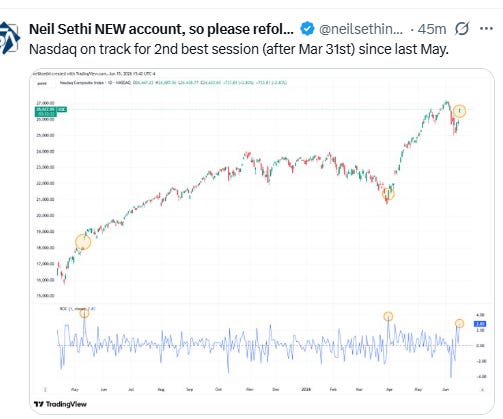

With no notable additional news on the Iran front surfacing during the session or other major catalysts, equities would drift, with an upward bias for the Nasdaq finishing +3.1%, it’s second best day since last May, supported by continued excitement around the coming inclusion of SpaceX, which jumped another 20% during the session, in that index.

The S&P 500 would also move higher during the session ending +1.7%, while the Dow Jones Industrial Average and small cap Russell 2000 would ease throughout the day to +0.9% and +0.7% respectively. Still it was those latter two indices that would set fresh all-time highs.

On the economic front, May industrial production (our most comprehensive look at the manufacturing sector) would miss estimates, but April would be revised higher, lifting both on a year-over-year basis to the strongest since November.

Elsewhere, bond yields would edge lower as crude prices continued their sell-off. Gold and bitcoin saw healthy advances, and copper and US natural gas futures were also higher, while the dollar was little changed.

Some market commentary:

“Risk appetite is back on, but the issue is to know whether the Strait fully reopens,” said Christopher Dembik, senior investment manager at Pictet Asset Management. “Trump doesn’t have a great track record of lasting deals in the Middle East, so there’s a risk of tensions spiking back during the summer.”

“It’s not a permanent solution, so a significant risk premium will likely be priced into markets,” said George Moran, European macro strategist at RBC. “But, if oil stays around $80-85, it certainly takes a good amount of pressure off central bankers’ shoulders.”

“The key question is whether recent price pressures prove temporary or become embedded in broader price dynamics,” said Laura Cooper, global investment strategist and head of macro credit at Nuveen. “A de-escalation could reduce concerns about a persistent energy shock, but is unlikely on its own to shift policy guidance.”

“Once the initial enthusiasm surrounding a deal fades, equities can continue to rally given resilient earnings growth, AI optimism and their tendency to look through geopolitical shocks. For fixed income and FX, however, the change to the macro backdrop is likely to prove a sustained headwind.” — Skylar Montgomery Koning, macro strategist.

“A successful SpaceX IPO is generally a positive signal for broader investor interest in innovation and technology,” said Evan Schlossman, principal at SuRo Capital. “It’s a reflection of the demand, interest, and desire to invest in these types of companies.”

In today’s Markets Update:

The usual look at notable stock movers, sector performance, and corporate news from today.

A look at the disappointing positive volume in the Nasdaq.

Updated technical charts on a variety of US equity, bond, and volatility indices as well as select commodities.

The latest on Fed rate hike expectations.

Catch up on posts from the weekend.

Wrap-up and Tuesday’s global highlights.