Markets Update - 6/17/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

US equity indices would start Wednesday’s session modestly higher following a stronger than expected May retail sales report, indicating continued resilience in consumer spending, and as they awaited the highly anticipated FOMC decision and press conference this afternoon, the first under new chair Kevin Warsh.

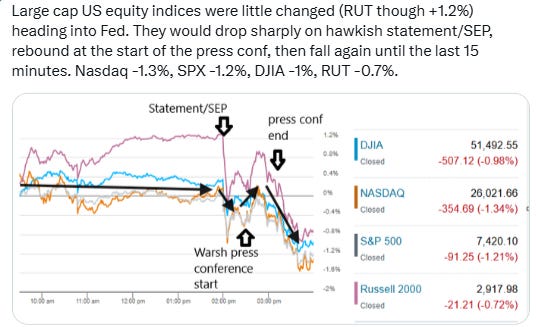

The premarket advance was larger on the Nasdaq as Tech shares rebounded after leading sectors to the downside on Tuesday (as discussed in the morning update), but it was small caps (Russell 2000 (RUT)) which would see the largest gains ahead of the Fed over 1% at one point. Large cap indices would hug closer to the unchanged mark.

All though would fall sharply following a more hawkish than expected statement (which was also notably shortened) and Summary of Economic Projections which includes the “dot plot” that indicated half of the committee was in favor of at least one rate hike this year, with around a third in favor of two. Only one member in contrast penciled in a rate cut.

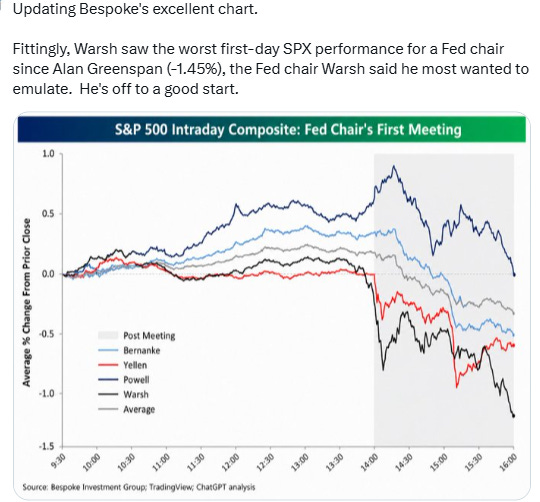

Fed rate hike expectations would also shoot higher. The equity declines would soften, with the indices touching positive territory again, at the start of Warsh’s press conference before renewed selling kicked in taking them to the lows of the day, where they would end, led to the downside by the Nasdaq -1.3%. The S&P 500 would finish -1.2%, the Dow Jones Industrial Average -1.0%, and the RUT -0.7%. It was the worst first-meeting SPX performance for a Fed chair since Alan Greenspan.

Warsh made a point to indicate that “the institution is going back to first principles,” and emphasized (as did the statement) that “this committee will deliver price stability." Warsh also made clear significant changes were coming to the Fed. He announced the appointment of task forces that he expects to provide recommendations for changes by year end in five key areas: 1) communications, 2) the Fed’s balance sheet, 3) the use and reliance on existing data sources, 4) on productivity and jobs, and 5) on the inflation framework. Much more on the Fed in the subscriber section.

On the economic front, in addition to the strong retail sales report, May pending home sales (contract signings so more forward looking) rose +3.8% from April, the fourth straight gain after hitting an all-time low in January, and the strongest monthly gain since September 2024 (although the sales pace remains quite low historically).

Elsewhere, bond yields were mixed with the short end (more sensitive to Fed rate expectations) shooting higher but the long end more subdued as inflation expectations fell, oil prices fell for a fifth day, and gold, copper, bitcoin, and US natural gas futures all were lower as well, while the dollar jumped.

Some market commentary:

“Inflationary pressures in the US are unlikely to abate quickly,” said Bank J Safra Sarasin equity strategist Wolf von Rotberg. “Solid growth and elevated core inflation suggest a hawkish bias, regardless of oil prices.”

“Retail sales in May point to a resilient consumer despite accelerating inflation and higher borrowing costs,” said Angelo Kourkafas at Edward Jones. “Looking ahead, the recent drop in oil prices should provide relief at the pump, while an improving labor market suggests a stable outlook for consumer spending.”

BBG Chris Anstey senior editor: So, all in all, I’d argue that we heard a little bit more of the old “inflation hawk” Warsh today than we did the more recent “dovish” iteration. Even if we assume that he was the one who threw out the “proposal” to discuss a rate cut today. Which, again, could well have been done so he could tell Bessent and anyone else in the Trump administration privately that look, he had made the case. But we may know a lot more when we see who he taps to head these panels. Are they hawks? Doves? A true mix? A lot to be learned in the coming weeks and months.

From Bloomberg Economics’ Anna Wong: “The Kevin Warsh era has arrived with a bang – in the form of a dramatically shortened FOMC policy statement and a dot plot that didn’t contain any dot from the chairman himself. That marks a break from the eras of former chairs Jerome Powell, Janet Yellen, and Ben Bernanke. But the rest of the committee sent an equally strong signal: They want rate hikes. Half of the committee penciled in hikes this year, while the other half anticipates holding rates steady or cutting once. That means Warsh could play a key role in influencing the direction of rates. We no longer expect the FOMC to cut rates by 25 basis points later this year.”

“The bigger takeaway came from the rate projections,” said Bret Kenwell at eToro. “Markets were prepared for higher rates, but the Fed’s projections suggest policymakers may be willing to stay more hawkish than investors expected.”

“We continue to think the Fed will be on hold this year, with the recent de-escalation in tensions in the Middle East and a drop in oil prices helping to soften inflation risks,” said James McCann at Edward Jones. “However, the bar for a rate hike looks lower after today’s meeting.”

“Despite a more-hawkish statement, we expect the Fed’s next move is still likely a cut, but it will take time for inflation to unwind enough to give the board the breathing room to act,” said Ellen Zentner at Morgan Stanley Wealth Management.

“The Fed’s recent hawkish shift was not just about higher energy prices,” said Kay Haigh at Goldman Sachs Asset Management. “Despite the recent pullback in oil, half of the members of the FOMC expect rate hikes as soon as this year, reflecting strong labor market and inflation data.”

“Our base case remains that the Fed can just about avoid hikes, but the path is narrow and there will be a high premium on the incoming inflation data,” Haigh wrote.“He is absolutely telling you that he plans on delivering on price stability. So that means ... we’re not going to have such easy money policy as everybody thought maybe Chairman Warsh would do back in the first quarter of this year, when everyone was counting on rate cuts,” DoubleLine Capital CEO Jeffrey Gundlach said on CNBC’s “Closing Bell.” “He doesn’t sound like that today at all.”

“A victory for those that believe the bond market is smarter than the stock market,” Potomac Fund Management’s Shawn Snyder said. “Today’s message from the dot-plot is that most Fed officials are now aligned with the bond market, which has been predicting at least one rate hike for months now.”

Snyder added that Warsh’s vow to “deliver price stability” should ease investors’ concerns surrounding the central bank’s independence.

In today’s Markets Update:

A LOT more on the Fed decision and Warsh press conference.

The usual look at notable stock movers, sector performance, and corporate news from today.

A look at the pop in speculative activity on the Nasdaq.

Updated technical charts on a variety of US equity, bond, and volatility indices as well as select commodities.

Catch up on posts from the day.

Wrap-up and Thursday’s global highlights.