Markets Update - 6/22/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

US equity indices started Monday’s session modestly higher with Tech shares in the lead even as SpaceX slid more than 5% in premarket trading, putting the stock on pace for a third straight loss after announcing it was selling debt to fund its AI ambitions. Supporting markets though were chipmakers who continued their recent rally with Micron one of the early outperformers, rising more than 4% as discussed in the morning update.

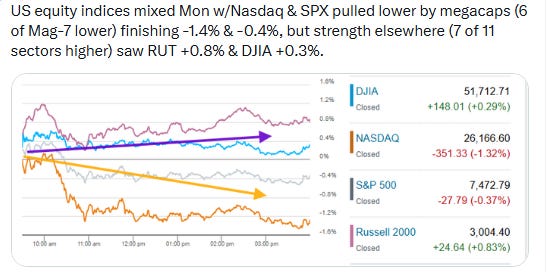

Some of those trends continued as the session wore on with SpaceX ending down -16% but Micron nearly +7%. Gains though would broaden with 7 of 11 S&P 500 sectors finishing higher. However weakness from the largest names including Alphabet (-5.2%), Microsoft (-3.2%), Amazon (-4.8%), Broadcom (-4.7%), and Meta (-2.3%) outweighed the positives dragging the SPX to a -0.4% finish and the Nasdaq to -1.3%.

In contrast the small cap Russell 2000 (RUT) pushed higher to again finish in the lead +0.8% while the price-weighted Dow Jones Industrial Average +0.3%.

Markets got some encouragement from Vice President JD Vance, leading the US delegation in four-party talks with Iran in Switzerland, describing the first round of negotiations as “very, very good” and said Iran had agreed to allow nuclear inspectors back into the country — a claim later backed up by President Donald Trump, although Iranian officials, who also cited progress, challenged that claim, saying Vance’s assertion was “false and does not reflect reality.” Lower-level delegates are set to remain to discuss technical matters, with Vance and Iran’s parliament speaker Mohammad Bagher Ghalibaf leaving.

In addition, crude prices would continue their decline as a 60-day reprieve of US sanctions on Iranian oil, part of the interim peace deal, saw more than 30 million barrels depart for Asia in the past week.

Finally, Alan Greenspan, the Federal Reserve chairman hailed by many as a wizard for guiding a then-record US economic expansion in his 18 years heading the Fed, has died at age 100.

Elsewhere, bond yields moved higher despite the softening in oil prices, as did the dollar, in its case to a fresh 1-year high. US natural gas and bitcoin futures were also higher, while gold and copper futures fell.

Some market commentary:

“The issue that stands out the most is the idea that the hyperscalers continue to receive an extremely low return on investment on their colossal level of spending on AI,” said Matt Maley at Miller Tabak. “Another big concern surrounds the issue of ‘circular investments,’ where companies invest in each other, while also committing to buying each other’s products.”

While Fundstrat Global Advisors’ Tom Lee believes a number of catalysts could impact the market down the line – such as the implementation of task forces at the Federal Reserve and supply chain impacts from the closure of the Strait of Hormuz – the environment remains positive. “We still believe later this year there is going to be an abrupt change of market conditions, one that feels very much like a bear market, but we don’t want to stand and call a top,” the firm’s head of research said on CNBC’s “Closing Bell” on Thursday. “I think conditions are still favorable for stocks.”

“Even during the midst of the conflict in the Middle East, equities still priced a positive outcome,” said Stephan Kemper, chief investment strategist at BNP Paribas Wealth Management. “It seems logical that markets don’t rally too hard on something which they had already priced to a fair degree.”

“If you look at who’s got the most wherewithal and transparency and earnings, it’s still the U.S. for right now, given the fact that we’re not concluding that [Middle East] conflict, given the fact that [oil] flows aren’t fully back to normal yet and given the fact that the U.S. still has its own energy supplies,” Tom Hainlin, U.S. Bank Asset Management Group’s national investment strategist said.

“As long as consumers are making money and confident their jobs they want to spend, and as long as businesses think the economy is in good shape and are expanding for the future, that’s still a pretty good setup,” he added.

“I do think it’s a good thing for the Fed to say a little less,” said Liz Thomas, chief market strategist at SoFi. “Yes, it would be a change,” she said. But it would let markets focus on other things, instead of Fed statements and forward guidance, which are a best guess, and often incorrect, she added.

“The June FOMC meeting, with half of the committee leaning toward a tighter policy path, sent a hawkish jolt through markets. Even though Warsh didn’t submit his own dot for the dot plot, his tone at the news conference seemed notably hawkish to us. A hot PCE inflation reading will likely reinforce that hawkish message.” —Anna Wong, Stuart Paul and Eliza Winger.

“While we’re skeptical of the notion that the [Federal Open Market Committee] will deliver the September hike that the futures market currently implies, we’re also sympathetic to the fact that the balance of risks now implies the Fed is taking a more balanced approach to policy rates from here,” Ian Lyngen, Vail Hartman and Delaney Choi of BMO Capital Markets said in commentary shared with MarketWatch earlier.

In today’s Markets Update:

• A look at a mixed session beneath the surface, with megacap weakness dragging the SPX and Nasdaq lower even as small caps and the majority of sectors held up better.

A review of the day’s notable stock movers and sector performance, including renewed pressure in Alphabet, Amazon, Microsoft, Netflix, and SpaceX, offset by strength in Micron, SMCI, Corning, AbbVie, and energy/real estate.

Updated technical charts across the major US equity indices, Treasury yields, volatility gauges, the dollar, oil, gold, copper, natural gas, and bitcoin.

Some context on the competing market crosscurrents: a more hawkish Fed/rates backdrop, a stronger dollar, sharply lower oil, easing Middle East risk premium, crowded AI/semiconductor positioning, and signs of better breadth outside the largest names.

A roundup of selected market commentary, positioning updates, AI/tech caution notes, and the day-ahead calendar.