Markets Update - 6/24/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

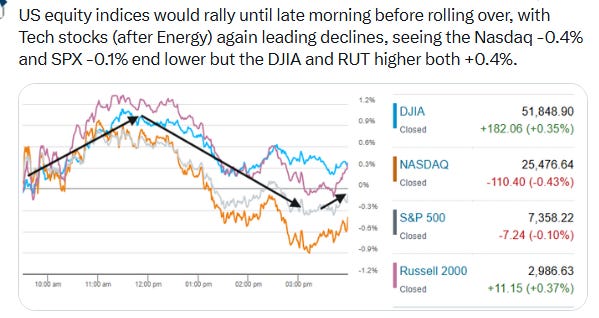

US equity indices started Wednesday’s session with a modest rebound as discussed in the morning update ahead of Micron Technology Inc.’s results after the close today (more on that below).

Indices made further headway for most of the morning session before turning lower late morning, dragged lower for a second day by the Technology sector, seeing the Nasdaq and S&P 500 finish in the red for a third session -0.4% and -0.1% respectively.

The declines came despite a continued fall in crude oil prices with Brent crude, the international benchmark, settling under $74 for the first time since the start of the conflict. That, along with a notable pullback in Treasury yields, helped other areas of the market, with again six S&P 500 sectors finishing higher, with the equal-weight version of the index +0.7% in contrast to the small loss for the market cap weighted index. The small cap Russell 2000 and Dow Jones Industrial average would also both end higher at +0.4%.

The Tech selloff would spill over into markets for gold and bitcoin, both of which saw futures prices fall to new lows for the year, the lowest since November 2025 and October 2024 respectively (although bitcoin would rebound after the Micron earnings discussed below). AI-adjacent copper would also continue its recent decline to a 6-week low. The dollar in contrast would close at another 1-year high.

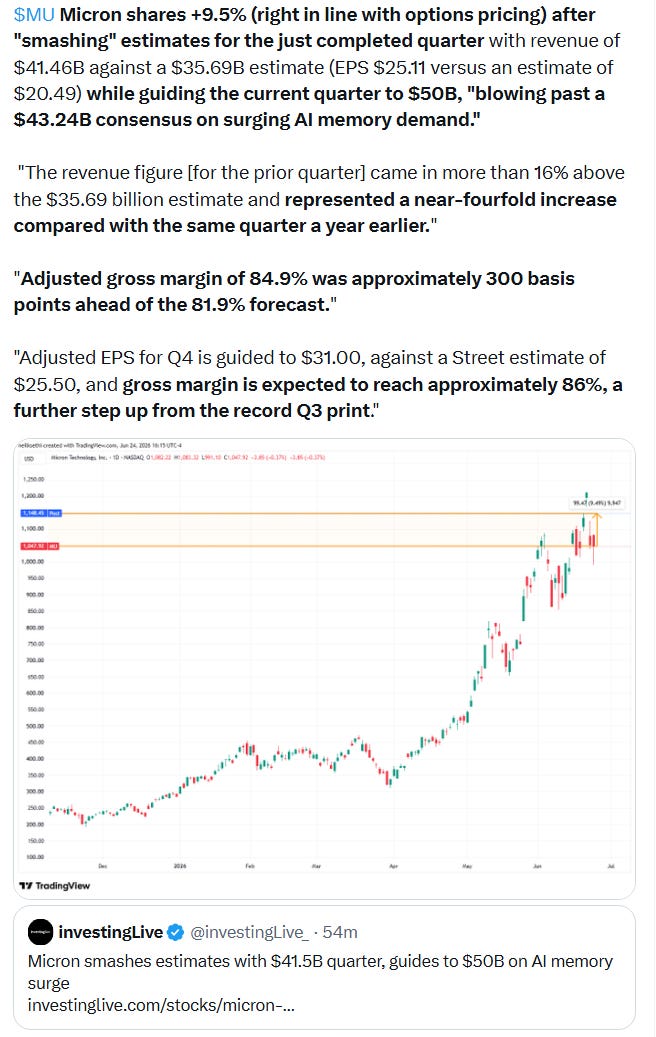

After the close, however, Micron delivered that much anticipated earnings report, and it appears to have cleared the high expectations “smashing" estimates for the just completed quarter with revenue of $41.46B against a $35.69B estimate (EPS $25.11 versus an estimate of $20.49) while guiding the current quarter to $50B, "blowing past a $43.24B consensus on surging AI memory demand." See post below for more.

Currently futures are indicating a higher open for the S&P 500 and Nasdaq-100 tomorrow at +0.5% and +1.5% respectively.

Some market commentary:

The selloff among the “Magnificent Seven” is a sign of a healthy market as investors rotate their money, according to Rogers. “This isn’t a rush for the exit,” Cullen Rogers, portfolio manager at Wedbush Funds said. “But it makes a lot of sense to look into the next layers where applications and eventually monetization will occur.”

“The law of large numbers works against these companies,” Steve Sosnick, chief strategist at Interactive Brokers, told MarketWatch. In his opinion, investors who want exposure to the “Magnificent Seven” have likely already invested in them. “It takes a lot of work now to get fresh money into these stocks,” he added. The “Magnificent Seven” certainly remain well-positioned to be AI winners, Sosnick said. These Big Tech companies have made aggressive early investments in various parts of the AI stack, giving them a first-mover advantage. “But there’s nothing saying that the current winners are the long-term winners,” he said. “The best AI company could yet to be formed.”

“The downside move in tech stocks is a healthy pullback, since many tech stocks have become overstretched,” said Rick Gardner, chief investment officer at RGA Investments. “The tech pullback suggests that investors are coming to the realization that earnings expectations for tech stocks are high, creating a more difficult bar to clear when earnings season re-starts in July, and we would characterize this pullback as a recalibration of expectations.”

“When stocks rise too much and too fast, a pullback almost always ensues,” said Gardner. “We would much rather be buying tech stocks on days when they are down, and the pullback can present an opportunity for investors who do not have adequate exposure to this space, which is still fundamentally strong.”“For high-performing companies that reflect the dynamics of a sector, market expectations naturally rise,” said Guillermo Hernández Sampere, head of trading at MPPM. “From a rational standpoint, these are difficult to meet, and disappointments become apparent in the stock’s price performance.”

“Whether or not we rally in the short-term, we continue to see medium-term downside risk for the tech/AI trade,” said Jonathan Krinsky, chief market technician at BTIG LLC. He said he sees between 10% and 15% additional downside in the semiconductors group and described Tuesday’s action as a “Chip-Wreck.”

“There is room for the dollar to head higher,” said strategist Jordan Rochester at Mizuho International Plc. “The dollar tends to rally into Fed hikes, with the market toying with the idea of a cycle starting in September.”

In today’s Markets Update:

A look at a mixed session for US equities, with Technology again weighing on the SPX and Nasdaq, even as the Dow, Russell 2000, and equal-weighted S&P 500 finished higher boosted by a continued rotation beneath the surface, with six S&P 500 sectors higher, led by strength in industrials, utilities, travel, homebuilders, and defensives.

Updated technical charts across the major US equity indices, Treasury yields, volatility gauges, the dollar, oil, gold, copper, natural gas, and bitcoin.

Some context on the competing market crosscurrents: falling crude prices and Treasury yields, a stronger dollar, weak commodity markets, and still-elevated short term volatility positioning.

A roundup of selected market commentary and positioning updates, including JPMorgan’s higher SPX target, Tom Lee’s constructive outlook, BoA’s client selling data, Goldman’s bubble/margin framework, and the Dow’s decision to add Alphabet among others.

A look at a busy day ahead.