Markets Update - 6/29/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

US equity indices opened the Monday’s session like Friday’s solidly higher at the large cap level with the S&P 500 and Nasdaq looking to break 5-day losing streaks encouraged by the apparent dialing back of US-Iran tensions and a bounceback in growth names as discussed in the morning update.

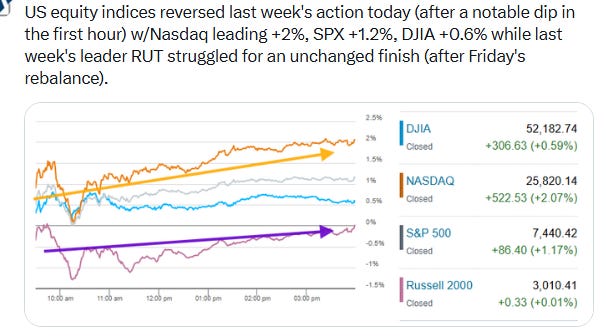

But unlike Friday, those large cap indices would, after a morning dip, maintain their gains into the close in a reverse of last week’s action with the Nasdaq leading +2.1%, the S&P 500 +1.2%, and the Dow Jones Industrial Average +0.6%, while last week’s leader, the Russell 2000, struggled to an unchanged finish perhaps impacted by Friday’s Russell rebalance discussed further in the subscriber section.

Monday’s gains were led by a rebound in the megacap growth names that had come under pressure last week. Thirteen of the largest sixteen S&P 500 components would finish in the green. Semiconductors were volatile but ultimately recovered from an early selloff, with the PHLX Semiconductor Index finishing up 3.8%. Defensive sectors such as Staples, Utilities, and Real Estate lagged as investors rotated back toward growth.

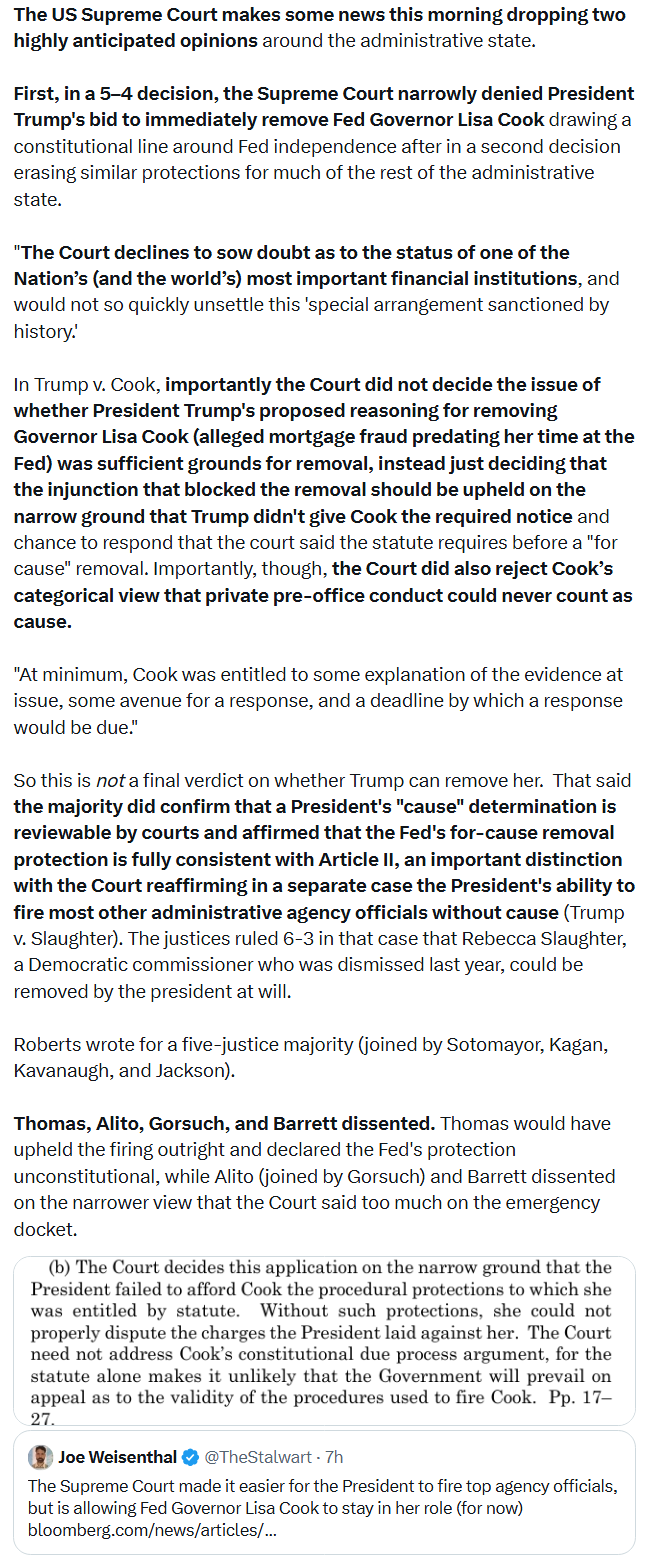

The rates backdrop was calm, with 2-year and 10-year yields stabilizing after four straight declines, unfazed by the Supreme Court’s decision that Lisa Cook could not be removed (for now) which helped reinforce Fed independence (see more in post below). Oil rose but remained near the least since the start of the Iran conflict.

Some market commentary:

“Neither side (especially the US) seems keen on a full resumption of hostilities and while unanticipated/unplanned escalation is possible, it’s likely the overall process remains headed toward a sustained détente,” said Adam Crisafulli of Vital Knowledge.

“The bounce we’re seeing is a welcome development for the bulls,” said Matt Maley at Miller Tabak. “We continue to believe strongly that the action in the tech sector will continue to be the main driver in the stock market.”

“After the hawkish pause of the Fed earlier in the month, one would have expected market exuberance to stall, but that doesn’t seem to be the case,” said Andrea Gabellone, head of global equities at KBC Securities. “That means the market believes that US exceptionalism is there to stay. It also means that the rally will likely broaden toward other corners of the market.”

“It wasn’t a full-blown selloff, but more a rotation of the kind that we saw many times in the last 12 months,” said Guy Miller at Zurich Insurance. “There are strong fundamentals in terms of super-normal profits. In semiconductors in particular, there’s still clearly a supply-demand imbalance.”

“Investors still recognize that the fundamental backdrop supports owning equities, but they are expressing that view with a degree of caution. That caution is welcome if you’re concerned about excessive optimism or the risk of bubbles forming. Taken together, improving market breadth, lower yields and continued investor discipline suggest there is still likely upside.” — Skylar Montgomery Koning, Macro Strategist.

“I think there’s a very good chance that equities can continue to rally from here in a pretty significant way through the end of the year,” said David Miller, investment chief at Catalyst Funds.

Last week’s pullback in technology stocks looked more like profit-taking than a total break in the market’s AI-driven rally, according to Ross Mayfield, investment strategist at Baird Private Wealth Management. Investors rushed to exit some highly appreciated positions in tech stocks last week after a sharp run-up, Mayfield said in a phone interview. But nothing has meaningfully changed in the AI- or chip-stock narratives that have helped drive the broader market higher. “When that’s the case, I don’t worry about [the pullback] continuing for a long period of time,” Mayfield said. The rebound in tech shares on Monday suggests buyers are already returning, he added.

“As the week begins, remember it marks the end of the quarter and the first half,” said JJ Kinahan at Cboe Global Markets. “That means we’re likely to see waves of volatility as institutional fund managers rebalance their portfolios. Expect some instability, but don’t overthink it.”

“It might be a little bit of light liquidity [due to the holiday-shortened trading week], so you might see bigger-than-expected moves,” Joe Tigay, a portfolio manager under Equity Armor Investments, told CNBC. “We also have the end of quarter happening soon, which can cause some window dressing to happen, so advisors are wanting what they report on their quarterly statements to look attractive to their clients, and they’ve been locking in some gains too. A lot of big names have had really big gains so far this year, so locking them in right now… a lot of advisors are happy to do so.”

“If I’m an investor looking to invest the next marginal dollar into equities, I would just say to them, ‘be a little patient,’” said Darrell Cronk, chief investment officer for Wealth & Investment Management, a division of Wells Fargo. “We think you might get some volatility buying opportunities as we move through the summer.”

“Quarter-end rebalancing could also add volatility, as strong equity gains may leave balanced portfolios overweight on stocks and create net selling pressure,” Mark Hackett, chief market strategist at Nationwide said in written commentary.

“As in every technological revolution, growth at one point shifts from the infrastructure to the application layer. Most value of the internet economy was captured by companies like Amazon or Google, not Cisco or Sun,” says Igor Pejic, author of the book Tech Money. “In the case of AI, growth momentum is now shifting from chips and data centers to vertical companies applying and monetizing the models. Examples include biotech, robotics and defense tech. This transition from the infrastructure to the application layer will take quite some time, but investors must be vigilant not to end up in a value-trap and overspend on infrastructure players.”

In today’s Markets Update:

A deeper look into Monday’s rebound in US equities including a review of the stock and sector breakdown, including renewed leadership from Communication Services, Consumer Discretionary, and Technology.

A closer look at key company movers and corporate developments.

Updated technical charts across the SPX, Nasdaq, Russell 2000, equal-weighted SPX, Treasury yields, volatility gauges, WTI crude, the dollar, gold, copper, natural gas, and bitcoin.

A look at the rates and Fed backdrop, including analysis from Goldman and BoA/Hartnett.

A review of market breadth and positioning, including weak NYSE positive volume despite the strong headline index move, Goldman’s data on last week’s Technology flows, Deutsche Bank’s rotation framework, and the slowdown in the recent penny-stock volume surge.

A look at volatility and flows, including VIX and VVIX easing, 1-day VIX remaining elevated versus recent quiet-catalyst days, Tier1Alpha’s gamma framework, quarter-end and holiday-week liquidity considerations, and commentary on buybacks, pension rebalancing, margin debt, and potential summer volatility.

A review of the AI debate, including the shift from AI infrastructure to applications, hyperscaler capex and buyback concerns, BIS warnings about AI-related financial fragility, sovereign AI competition from Europe and China, Goldman’s view on hyperscaler capex constraints, Citi’s tech downgrade, and the importance of AI infrastructure stocks to expected Q2 earnings growth.

A look at broader market and macro context, including RBC’s higher SPX target, Goldman’s earnings-driven market framework, Dow Theory commentary from Yardeni, Fed stress-test takeaways, JPMorgan’s global growth outlook, IPO supply concerns, private credit redemption pressure, and the NY Fed’s Multivariate Core Trend inflation model.

A look ahead to Tuesday’s calendar, including global economic data, Fed speakers, and corporate earnings.