Markets Update - 7/14/25

Update on US equity and bond markets, US economic reports, the Fed, and select commodities with charts!

To subscribe to these summaries, click below (it’s free!).

To invite others to check it out (sharing is caring!),

Link to posts - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog. Also please note that I do often add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

Finally, if you see an error (a chart or text wasn’t updated, etc.), PLEASE put a note in the comments section so I can fix it.

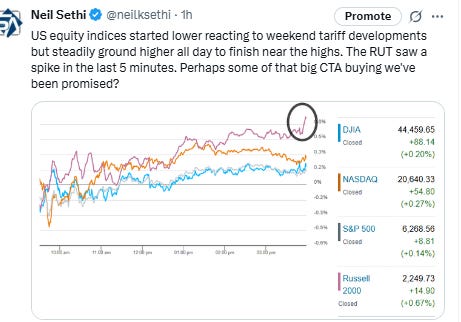

Major US equity indices started the day again modestly lower after President Trump announced increased tariffs on EU and Mexico, Trump administration officials increased pressure on FOMC Chair Powell, and ahead of a busy week of earnings and economic data. They steadily ground higher all day though to finish near the highs with modest gains. The RUT saw a spike in the last 5 minutes. Perhaps some of that big CTA buying we've been promised?

Elsewhere, Treasury yields edged higher as did the dollar (both to around 3-week highs), bitcoin (to another record close), and nat gas. Gold, crude, and copper were lower.

The market-cap weighted S&P 500 (SPX) was +0.1%, the equal weighted S&P 500 index (SPXEW) +0.1%, Nasdaq Composite +0.3% (and the top 100 Nasdaq stocks (NDX) +0.3%), the SOX semiconductor index -0.9%, and the Russell 2000 (RUT) +0.7%.

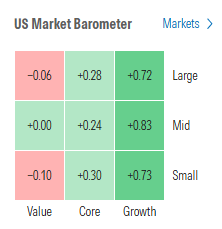

Morningstar style box showed the stronger relative performance in growth today.

Market commentary:

“I assume that what we are seeing here is a negotiating tactic,” said Lars Suedekum, a personal economic adviser to German Finance Minister Lars Klingbeil. “We have seen this many times in recent weeks: customs announcements followed by suspensions and customs breaks. It’s been quite a back and forth. I see no reason why it should be any different this time.”

“The real question is will Trump accept what they have on the table? Will they put a little more on the table? Where will it come out?” Wilbur Ross, Trump’s first-term commerce secretary, told Bloomberg Television Thursday.

“But worse comes to worst, he is fully prepared to go through with the tariffs and have that be the end of the story.”

“I worry that we could have a situation — and I don’t know that it’ll be on Aug. 1 or the future — but we’d have a situation where he’s not bluffing, but everyone thinks he is bluffing,” said Michael Strain, director of economic policy at the American Enterprise Institute, a conservative think tank. “The more times that happens, the more worried I get that the next up will be a real deadline.”

“The market has consistently shrugged off any issues, including tariffs, and even the brief conflict between Israel and Iran,” said Josh Kutin, head of multi-asset solutions, North America at Columbia Threadneedle Investments. “If the market is not overall responding negatively to any of those issues, I have a hard time seeing how that happens in the near-term.”

“We absolutely believe the recent bullish price action in risk assets makes sense,” said Max Kettner, chief multi-asset strategist at HSBC. “Bear in mind this is no longer just equities but spreading across virtually all risk assets. So if anything, we’d argue investors are once again under-exposed and continue to fight the rally.” Kettner, for his part, believes the US exceptionalism will continue as he ratchets up HSBC’s overweight, particularly to US equities. This week’s erratic tariff announcements may end up being a bullish catalyst if walked back, he says. With a weaker dollar and lowered earnings expectations, the upcoming reporting season could provide further support for equities.

“We also strongly disagree with the idea of complacency,” he said. “Equities and risk assets are well positioned to climb the wall of worries further in the coming weeks.”

“The stock market’s muted reaction to the latest volley of tariff headlines suggests investors may be growing numb to them, or are deciding that the tariff bark will likely be worse than the eventual bite,” said Chris Larkin at E*Trade from Morgan Stanley.

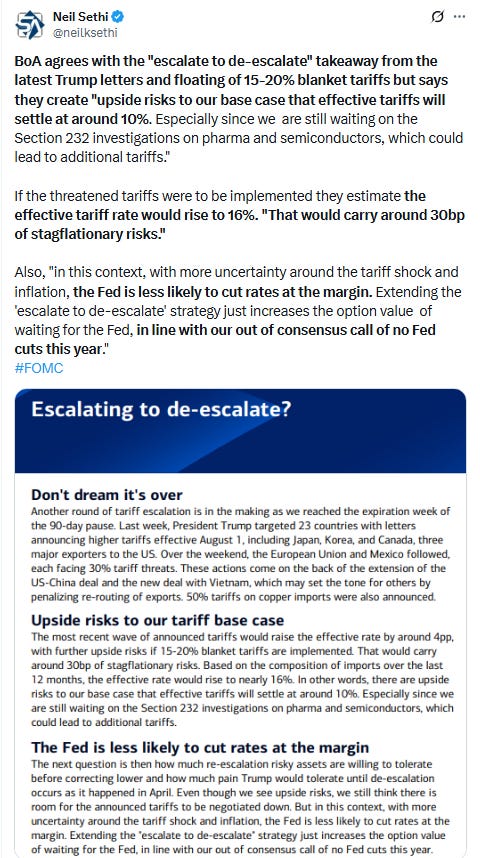

“We view the latest move from the White House as a negotiating tactic, and maintain our base case that the US effective tariff rate will settle around 15%, which we believe will allow the S&P 500 to rise further over the coming 12 months,” said Mark Haefele at UBS Global Wealth Management.

“People are getting a little bit too comfortable with this idea that Trump’s always going to back down,” said David Lebovitz, the global strategist of multi-asset solutions at JPMorgan Asset Management. “We’ve gone from a world where nobody knew anything to everybody knows something. It’s almost like the market’s going to go through this stress test where they see how far they can push it until they begin to see those cracks.”

“We are not out of the woods just yet, as the next few weeks will be pivotal to see how countries respond to the administration’s new Aug. 1 tariff deadline,” said Glen Smith at GDS Wealth Management. “The big question for markets in the coming weeks is if earnings, which are expected to be solid, can overshadow the tariff issues.”

“The market isn’t believing Trump, so we may see pressure on the exchange rate, but only temporarily,” said Gabriela Siller, director of economic analysis at Grupo Financiero Base. “Unless the tariff actually goes into effect and is collected, because according to US trade data, the IEEPA tariffs aren’t being collected to the letter.”

“Investors shouldn’t bank on Trump only bluffing with the 30% tariff threat on EU goods,” Brian Jacobsen, chief economist at Annex Wealth Management, wrote in an email. “That level of tariffs is punitive, but it likely hurts them more than the US, so the clock is ticking.”

“As usual, there are many conditions and clauses that can get these rates reduced,” Jacobsen wrote. “That’s probably why the market might not like the tariff talk, but it’s not panicking about it either.”

Investors are likely justified in their approach so far, according to Tom Essaye, founder of Sevens Report Research, as Trump has so far shown little inclination to follow through on his more aggressive tariff threats. But this time around, if Trump does insist on following through with higher levies on major U.S. trading partners, investors might need to stand up once again and push back. "So, it’s possible that stock vigilantes could appear and do the same thing with the administration on tariffs. If Trump views the new highs in stocks as a 'green light' to escalate the trade war, it may well have to decline to remind the administration that, while the U.S. economy can likely stomach some tariffs (again the level that seems 'ok' is around 10% aggregate tariffs), tariffs above certain levels will dramatically increase stagflation threats," Essaye said.

Traders may be too complacent about President Donald Trump's latest tariff threats, which still could push back above his “liberation day” levels, according to Thierry Wizman, global foreign-exchange and rates strategist at Macquarie Group. Traders "may reason that Pres. Trump doesn't want to preside over another market crash," Wizman wrote in a Monday client note. "But there's also the more ominous possibility that Trump has 'moved on' from using tariffs to extract concessions, and is now using tariffs to boost tariff revenues."

In that scenario, Trump's new Aug. 1 deadline for trade deals could "see a flood of new higher tariffs, as well as retaliation."

Investors already expect a sluggish second quarter, so the bigger risk may be to the back half of the year, according to Bret Kenwell at eToro. “Will management again tell a good story about the consumer and its customers, providing some stability (or even upward revisions) to third and fourth-quarter earnings?” he said. “If so, stocks could react favorably to that development. If not though, and estimates are instead revised lower, stocks may decline as they reflect this new reality.”

“I don’t think people are viewing any of the data points expected over this week as being materially indicative of how to position portfolios,” said Josh Rubin at Thornburg Investment Management. “We’re still in a waiting game around tariff policies as well as additional inflation and employment data that could influence Fed decision-making, and broader geopolitical developments, which are also in a quiet period.” Rubin notes that activity naturally slows down during the summer period, and while investors will pay attention to earnings, most won’t view them as highly indicative of companies’ future outlooks, rather waiting to hear about any updated thoughts on tariff policy.

“The rally has gone way too far,” said Kristina Hooper, chief market strategist at Man Group. “The tariff situation is far from resolved. It’s absolutely difficult for investors to model this out, so it’s easier to ignore it than think about the consequences.” Hooper advises reallocating to equity markets that offer better diversification and more attractive valuations — including Europe, the UK and even China. “I’m a sober realist,” Hooper said. “We have valuations that are at historically high levels. And so when stocks are priced at a near perfection, it’s a lot easier for disappointment to occur.”

“The big question for markets in the coming weeks is if earnings, which are expected to be solid, can overshadow the tariff issues that are still there in the background,” said Glen Smith, chief investment officer of Texas-based GDS Wealth Management. “So far, the market has been able to withstand tariff headlines and is more focused on earnings and economic resiliency.”

The market may be poised for a bit of a pullback as the start of earnings season takes hold, Paul Hickey of Bespoke Investment Group said on Monday.

“A moderate sell-off with the initial batch of earnings results wouldn’t be surprising at all,” the firm’s co-founder said on CNBC’s “The Exchange.” “The gains are going to be harder to come by in the next several weeks here as we do get into this seasonally weak period with a pretty high bar for earnings set.”

To be sure, analysts are feeling generally optimistic, as utilities is the only sector where there’s been downward momentum in earnings revisions, Hickey said. Still, that downward momentum is “just minor,” he added.

“For the majority of sectors, and as a result the broader market overall, we’ve seen a net of more positive earnings revisions than negative earnings revisions,” the co-founder continued.

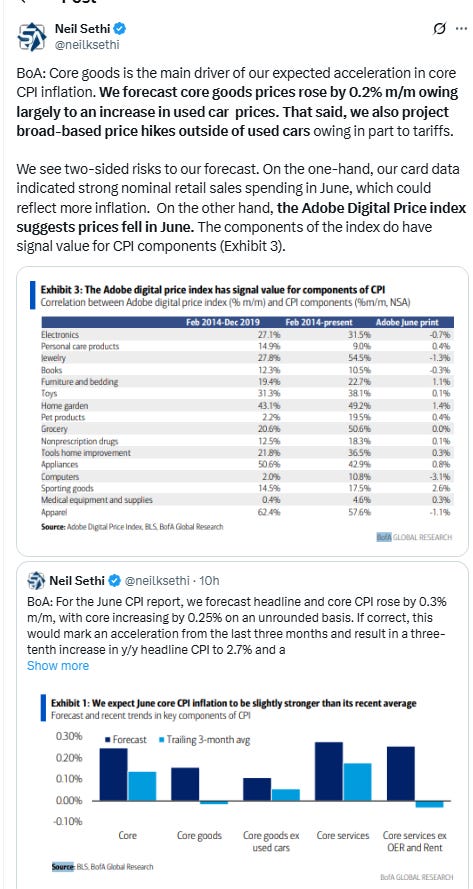

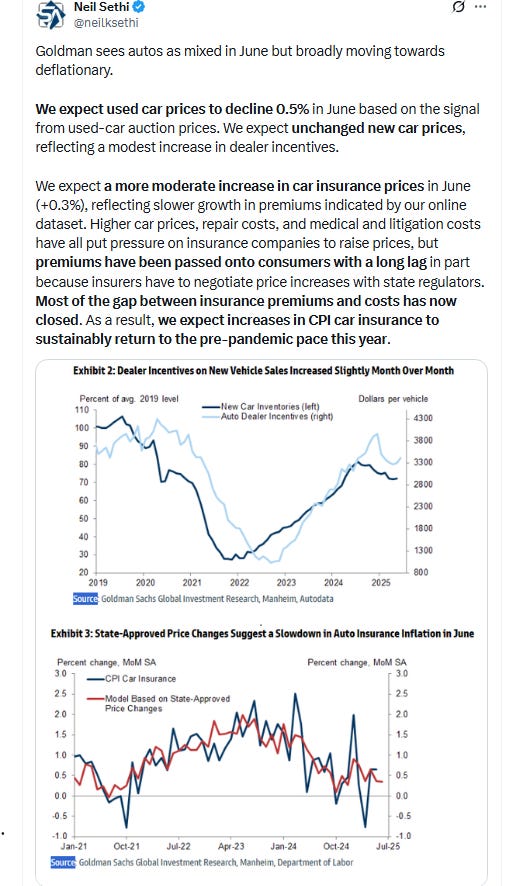

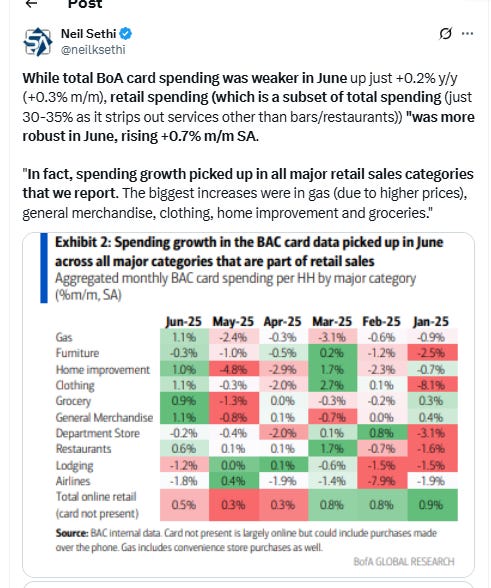

Tuesday's CPI inflation index for June might help foretell what's in store for the months ahead, but Thursday's retail-sales data for June also will be in focus.

"Last month’s report showed weak sales growth after a strong March, which likely reflected consumers buying ahead of expected tariffs," Brent Schutte, chief investment officer at Northwestern Mutual Wealth Management Co. wrote, in a Monday client note. "We will be watching to see if consumers are continuing to spend, even as tariffs have mostly been put on hold."

“It is important to note that investors are already pricing in rate cut expectations,” noted Linh Tran, market analyst at XS.com. “If the data points to stronger-than-expected inflationary pressures or a tight labor market, the Fed may be forced to delay rate cuts — potentially triggering a valuation shock for equity markets.”

Deutsche Bank strategists warned that stock market investors haven’t appropriately discounted risks from tariffs, as multiple negative factors are set to be in play by the end of the month. “Markets are clearly not pricing in these higher tariffs, and we may only know the outcome in the final hours, offering the potential for a sharp market reaction and heightened volatility,” said Henry Allen, macro strategist at Deutsche Bank. “Second, it’s the US jobs report that same day, and last year demonstrated that even a modest downside surprise can cause a big selloff, if investors are already jittery,” added Allen. Markets had fallen nearly 3% on the week ending 2nd August 2024 after data showed that far fewer jobs were created than expected, while unemployment had risen the most in nearly three years. “Third, long-end bond yields are going into this period at higher levels today, meaning it would take less of a jump before we move into problematic territory that re-ignites fears around fiscal policy,” Allen concluded.

Link to posts - Neil Sethi (@neilksethi) / X for more details/access to charts.

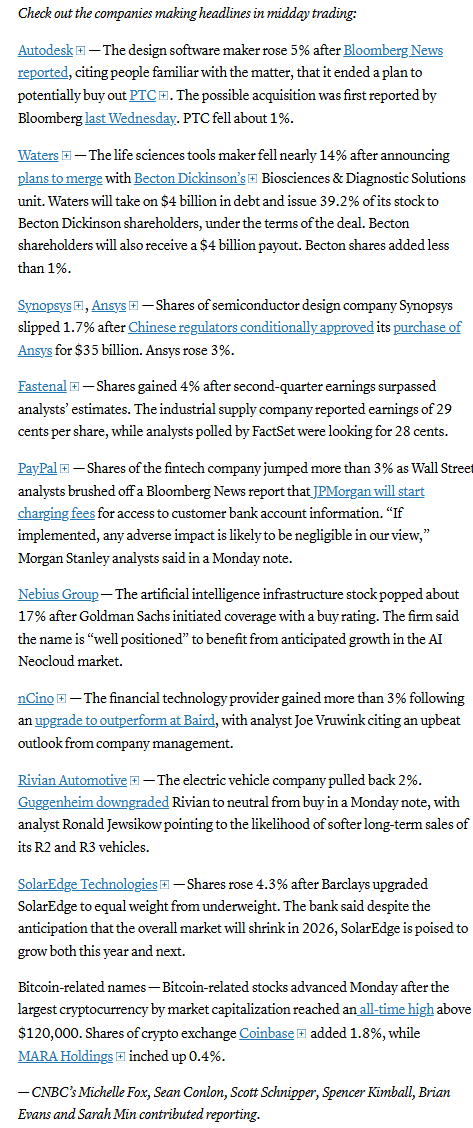

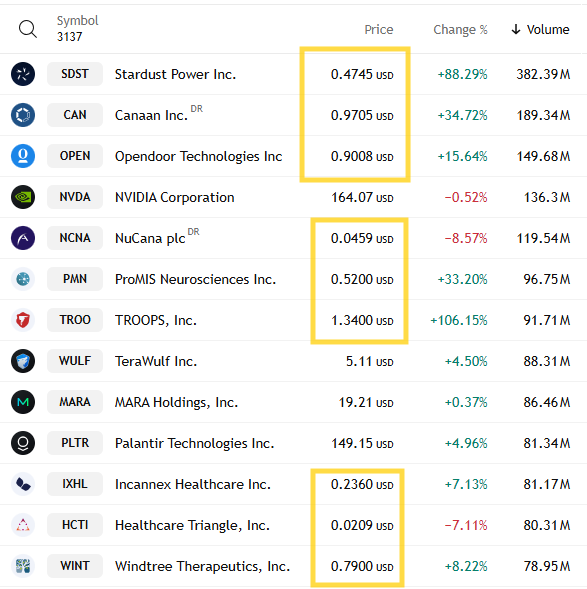

In individual stock action:

Corporate Highlights from BBG:

Tesla Inc. shareholders will vote on whether to invest in Elon Musk’s xAI, the billionaire said, after the Wall Street Journal reported that SpaceX agreed to pump $2 billion into the artificial intelligence startup.

Investigators of the fatal Air India crash last month have found no evidence so far that would require them to take actions over the Boeing Co. 787 aircraft or the GE engines powering it.

Autodesk Inc. is no longer pursuing an acquisition of PTC Inc., people familiar with the matter said, which would have ranked as one of the year’s largest deals.

Kenvue Inc. said Chief Executive Officer Thibaut Mongon will leave the company as it continues to revamp the maker of Tylenol, Neutrogena and Listerine brands.

CoreWeave Inc. is expanding a data center that is projected to double the electricity needs of a city near Dallas, another example of the strains that artificial intelligence workloads are placing on the US power supply.

Best Buy Co. was downgraded to neutral at Piper Sandler, which cited lack of catalysts and competition.

Crowdstrike Holdings Inc. was cut to equal-weight at Morgan Stanley, which cited “full valuation.”

Huntington Bancshares Inc. agreed to buy Veritex Holdings Inc., which operates more than 30 bank branches in Texas, for $1.9 billion in an all-stock transaction.

Chip-design software maker Synopsys Inc. secured China’s approval to buy Ansys Inc., setting the stage to close the $35 billion deal later this week.

NIQ Global Intelligence Plc is seeking to raise as much as $1.2 billion in a US initial public offering, adding to a rush of summer listings.

Some tickers making moves at mid-day from CNBC:

In US economic data:

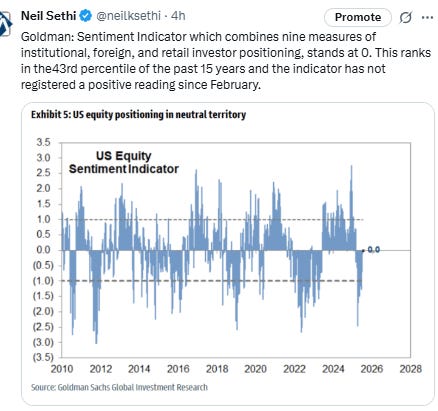

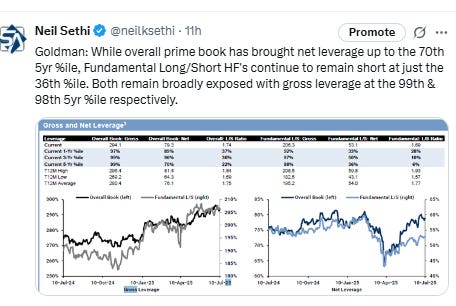

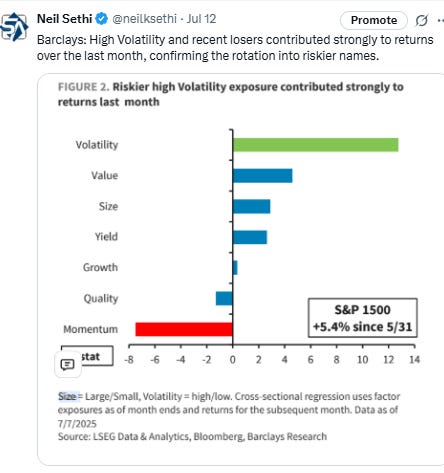

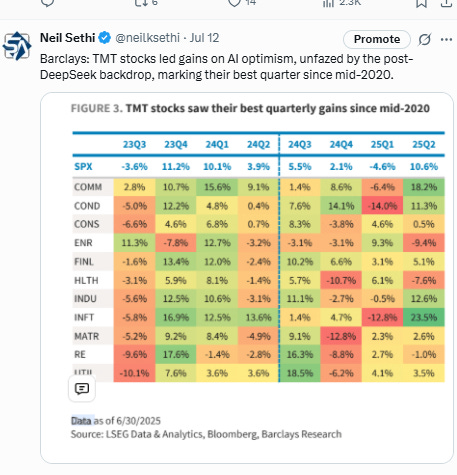

Link to posts for more details/access to charts (all free) - Neil Sethi (@neilksethi) / X

The SPX closed just under its ATH as it continues to trade mostly sideways over the past seven sessions. Its daily MACD remains positive although very mildly so now, and the RSI continues to fluctuate around 70.

The Nasdaq Composite a similar setup although it did edge to a new ATH today.

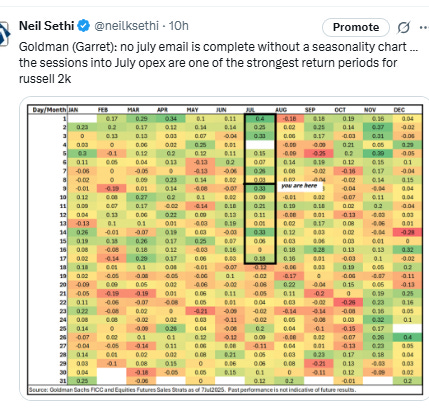

RUT’s (Russell 2000) “clear path to move at least to the 2300 level” per my note three weeks ago “has gotten choppy,” as I noted Friday, “but so far the overall uptrend from the April lows remains intact. MACD remains positive, although but RSI has the same over to under 70 phenomenon as the SPX (a little more so). As mentioned last week, CTAs are modeled to be big buyers which should support a test of the 2300 level absent a larger down move although we haven’t seen a ton of evidence of it in the daily price movements.” Perhaps today we’re starting to see some of that last piece.

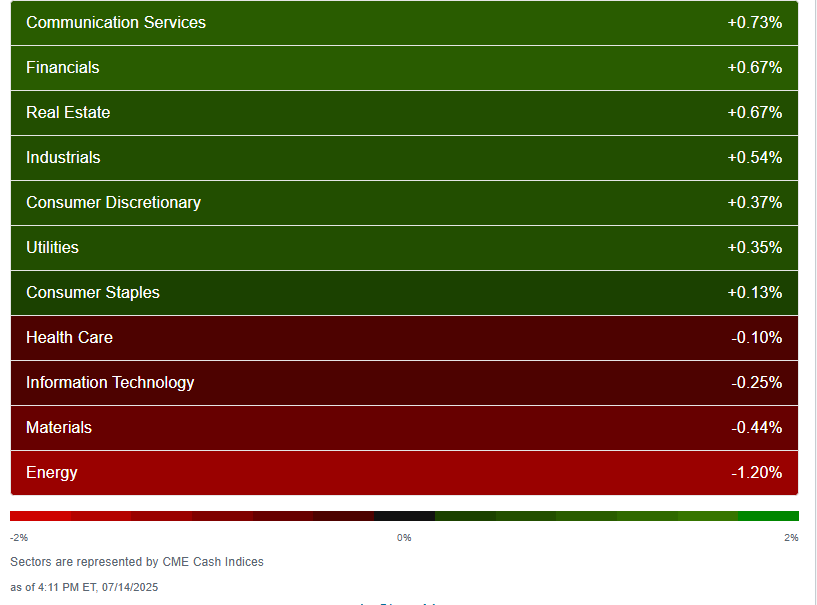

Sector breadth from CME Cash Indices improved to 7 green sectors from just 2 Friday (which was the least in over two weeks), but just four up >0.5% (vs six Thurs), with one sector down more than that in Energy (vs none Thurs), the only sector down over -1%. No sector up that much though.

SPX stock-by-stock flag from FINVIZ_com relatively consistent with a lot more green today than Friday with a much better performance from financials, software, and telecom which were weak on Friday. Industrials were particularly strong today. Tech hardware, energy, and medical devices (again) were weak.

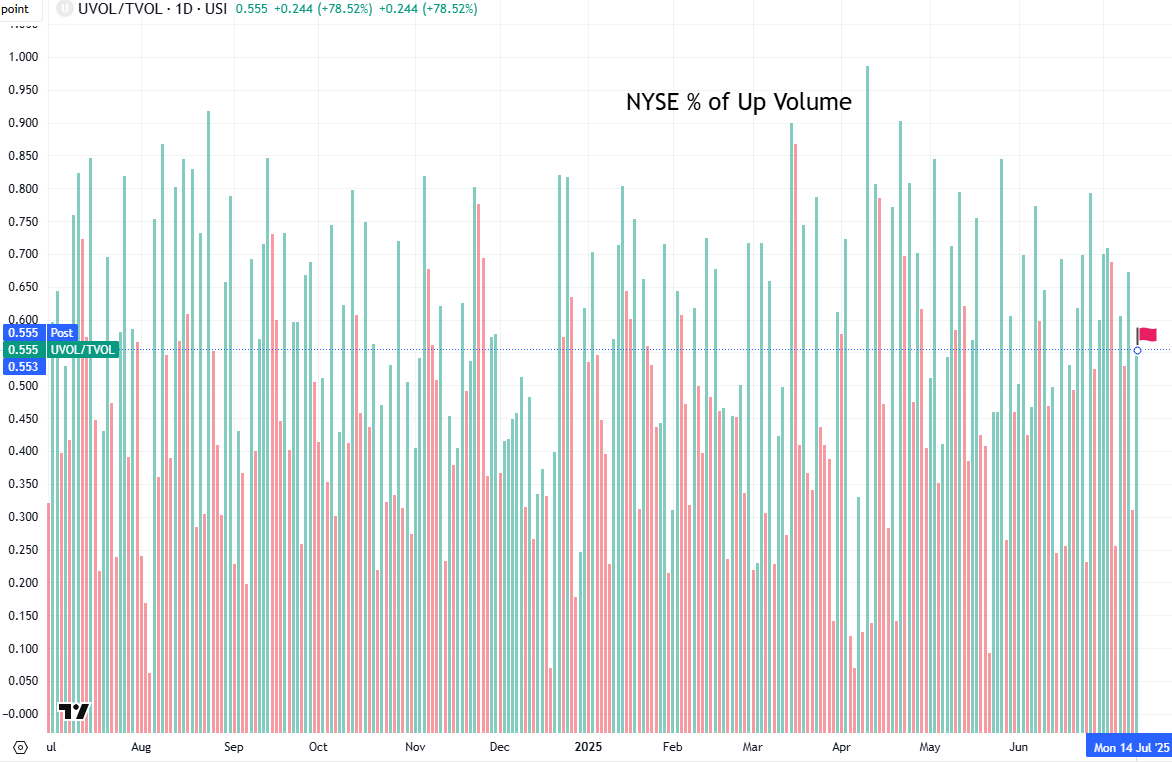

NYSE positive volume (percent of total volume that was in advancing stocks), which had been relatively strong the last couple of weeks Monday was like Friday “ok” at 55.5% relatively in line with the +0.16% gain in the index, and better than the 52.9% last Wednesday on a +0.32% gain.

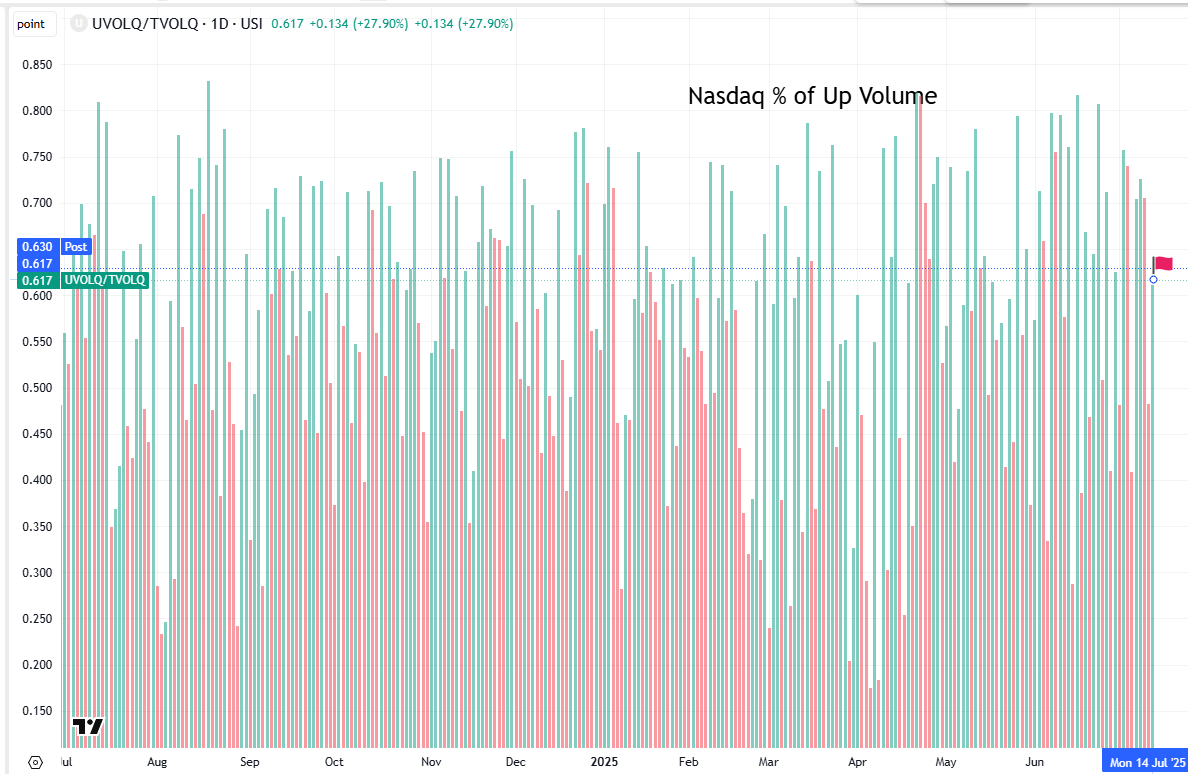

Nasdaq positive volume also improved and remained more elevated than the NYSE in part due to elevated penny stock volume at 61.7% in line with the +0.27% gain in the index. That said, the penny stock volumes were a little less extreme than last week. For example, Friday of the top 13 stocks by volume on the Nasdaq only NVDA had a share price higher than $4. While that was true of 9 of the top 13 today, their total volume was less than 1bn shares well under what we’ve seen on other days (they represented around 16% of total volume Monday).

That might also explain why the performance today was a bit lackluster compared to some days last week. For example, Thursday we saw 76.1% positive volume on just a +0.09% advance in the index.

Positive issues (percent of stocks trading higher for the day) were weaker at 51 & 56% respectively.

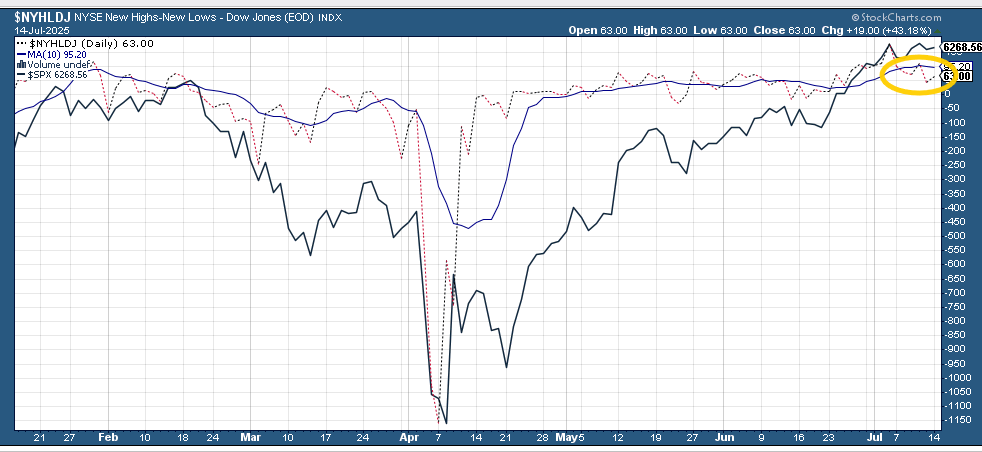

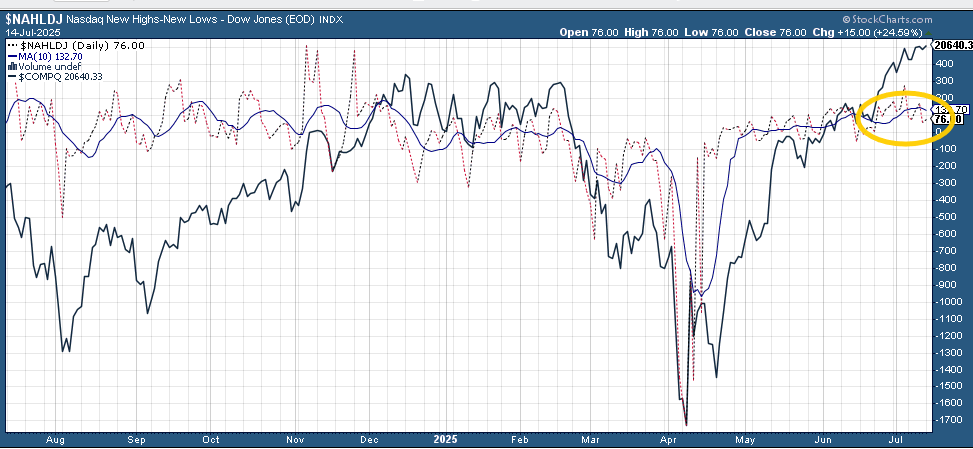

New 52-wk highs-new lows (red-black dotted lines) improved modestly from 3-wk lows to 63 on the NYSE, and also to 63 on the Nasdaq (but those are down from 179 and 265 on the 3rd).

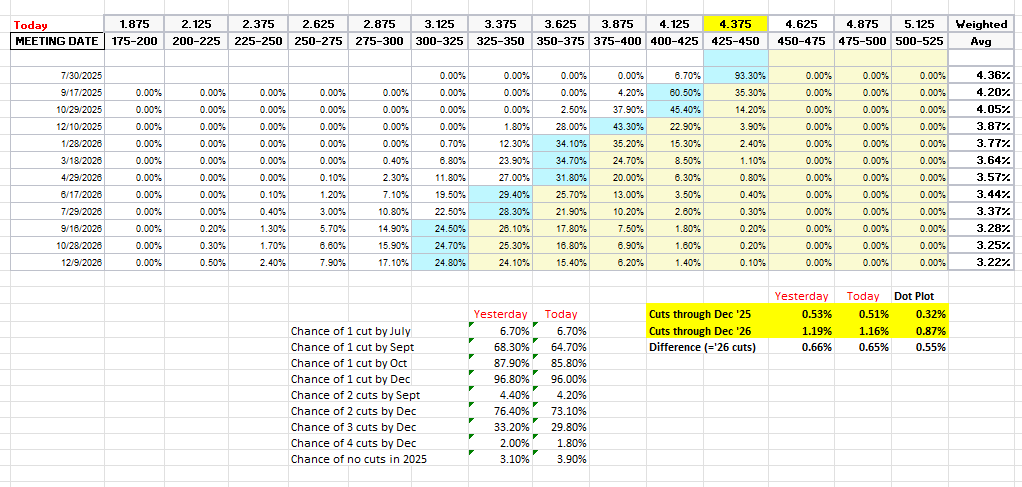

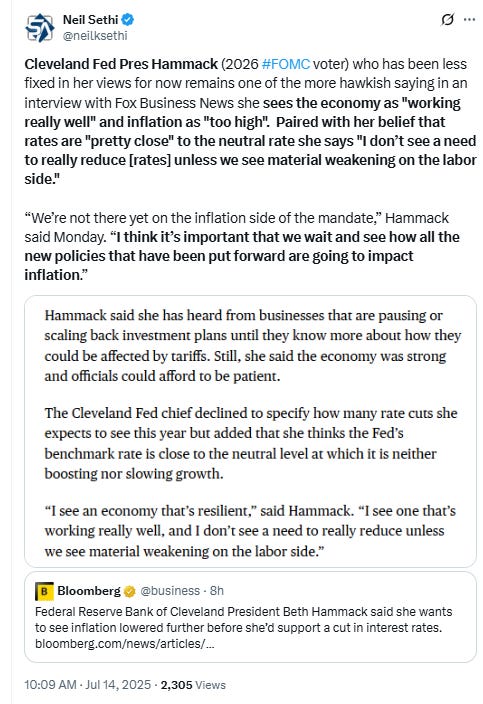

Fed rate cut bets shifted into 2026 following a hawkish interview by Cleveland Fed Pres Hammack with pricing for 2025 #FOMC rate cuts -3bps to 48bps according to CME’s #Fedwatch tool, (down from 64bps pre-June NFP & 92bps on May 1st (and the peak this year at 103bps on Apr 8th) (the low was 36bps Feb 11th)).

The probability of a cut at the July meeting is 5% down from 23% pre-NFP(and from 78% at the start of May) while a cut by the following meeting (Sept) is 62% from 94% pre-NFP getting back towards the lowest since February.

Chances of 2 cuts this year is 70% (down from 90% pre-NFP although still up from 62% on June FOMC Day), three is 26% (down from 55%), and four is 1% (from 10%). The chance of no cuts low at 5% but still up from 0.6% pre-NFP (but down from 8% FOMC Day).

2026 cuts though +6bps to 71bps, seeing total cuts through Dec '26 at 119bps, +9bps from FOMC Day and -27bps from the start of May.

I said after the big pricing out of cuts in January (and again in February) that the market had pivoted too aggressively away from cuts, and that I continued to think cuts were more likely than no cuts, and as I said when they hit 60 bps “I think we’re getting back to fairly priced (and at 80 “maybe actually going a little too far” which is back to where we probably were Apr 20th (a little too far) at 102bps). Seems like we’re getting back to “fairly priced,” and as of May 14th at 48bps perhaps starting to go a little too far in the other direction, but as I’ve said all year “It’s a long time until December.”

Also remember that these are the construct of probabilities. While some are bets on exactly two, three, or four cuts much of it is bets on a lot of cuts (5+) or just one or none.

10yr #UST yields up +1bps Friday to 4.43%, the highest close in nearly three weeks. As noted last Monday next resistance to the upside is 4.5%.

The 2yr yield, more sensitive to #FOMC policy, +1bps to 3.90%. It is -43bps below the Fed Funds midpoint, so still calling for rate cuts but also up +18bps this month.

I had said when it was around 4.35% (in Jan & again early Feb) that I found the 2-yr trading rich as it was reflecting as much or more chance of rate hikes as cuts while I thought it was too early to take rate cuts off the table (and too early to put hikes in the next two years on), but then the 2yr fell to 3.65% past where I thought we’d see it, so I took some exposure off there. We got back there but I never added back what I sold, so I stuck tight. Ian Lygan of BMO saw it going to 3.5% by year’s end before all this tariff business but now thinks it’s at fair value at around 3.75% so I took some more off at the end of June.

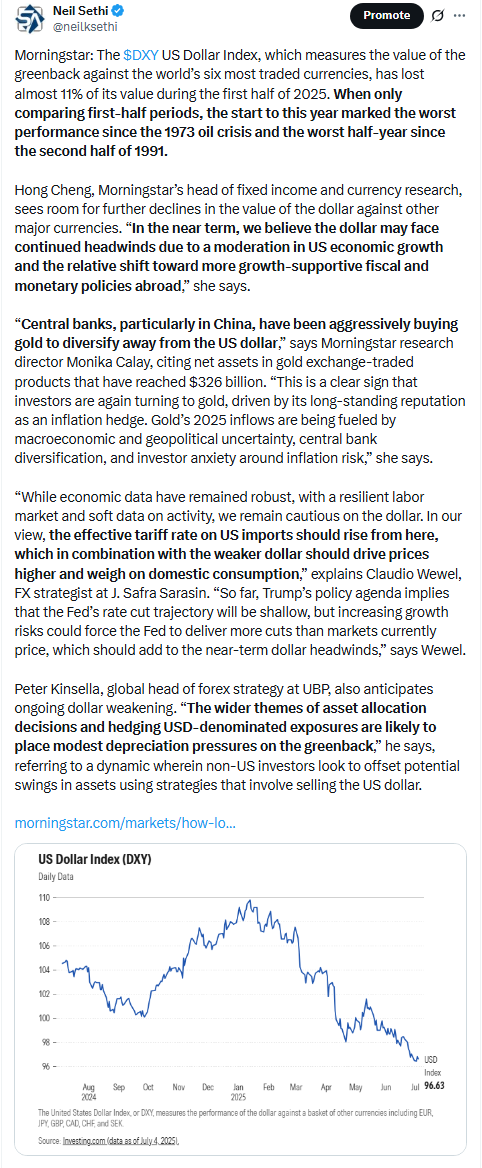

$DXY dollar index (which as a reminder is very euro heavy (over 50%) and not trade weighted) was up for a 3rd day (and 7th in 9) pushing now through the 98 level as it gains momentum after breaking first the downtrend line from the Feb highs and then the 20-DMA. Next is the 50-DMA at $98.85.

The daily MACD as noted last Monday crossed over to “cover shorts” while the RSI is now the highest in nearly two months and over 50 after having moved from under to over 30, which can be a signal of a reversal of a downtrend, so it’s got a lot of boxes checked for a move higher.

VIX edged up to 17.2, after closing sub-16 Wed & Thurs for the first time since Feb 20th, overall remaining in the same narrow range it’s been in for almost three weeks. The current level is consistent w/~1.08% average daily moves in the SPX over the next 30 days. Remember, though, we’re in a seasonally strong period for the VIX.

Chart from July 9th.

The VVIX (VIX of the VIX) also edged higher bur like the VIX remained in the area it’s traded in the past thirteen sessions at 96, still under Nomura’s Charlie McElligott’s “stress level” of 100 (consistent with “moderate” daily moves in the VIX over the next 30 days (normal is 80-100)).

While the weekend is behind us, the 1-Day VIX remained at the highest in a week at 12.5, consistent with traders implying a ~0.78% move in the SPX next session.

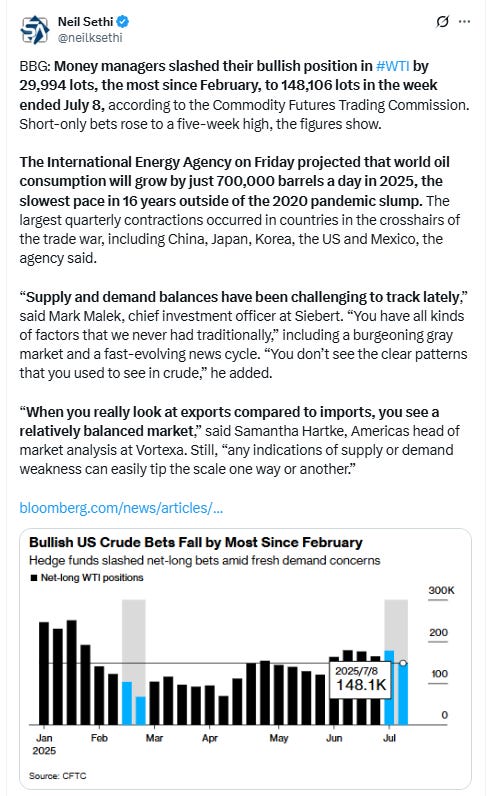

#WTI futures fell back once again to the uptrend line from the May lows as they continue to struggle with the 200-DMA resistance. The daily MACD remains in “sell longs” positioning but is close to turning more positive while the RSI is just over 50.

#oott

Gold futures (/GC) edged back a half percent from a 3-week high. They remain around the bottom of the uptrend channel from January just above the 50-DMA. Daily MACD remains negative as noted two weeks ago but is very close to flipping positive, while the RSI remains just over 50.

Copper (/HG) futures had their second straight down session since spiking higher last week on the Trump tariff threat, now down -2%, but remaining well into record territory pre-last week.

Nat gas futures (/NG) broke out of the short-term falling wedge they’ve been trading in the past month to the upside, which would commonly be associated with more good things to come for the bulls, moving back towards the 200-DMA, which as noted three weeks ago has for the most part held since last August. That said, it is nat gas, and it rarely does what anyone expects.

Overall they remain in their range this year. Daily MACD and RSI tilt negative but are improving.

Bitcoin futures up another +2% taking their four-day gain to +10%, although they finished well off the highs. Another daily ATH close, now firmly out of the congestion zone they had been in the past two months. The daily MACD and RSI are positive, and the latter is just starting to get overbought.

The Day Ahead

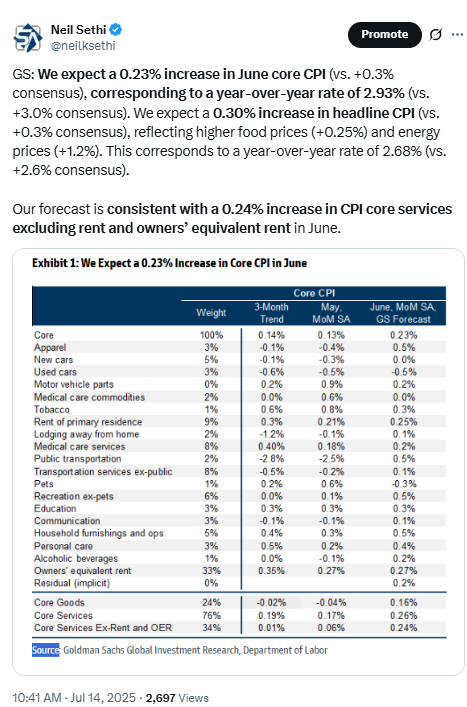

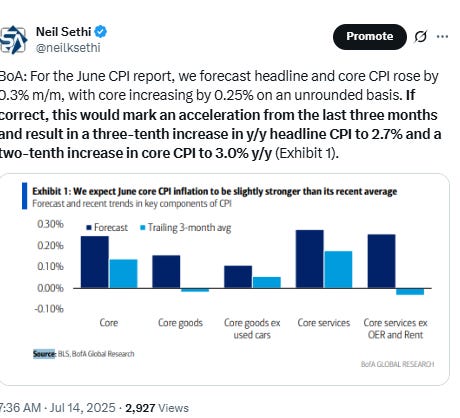

US economic data gives us our highlight of the week with the CPI report. Some posts on expectations are below.

We’ll also get a full slate of Fed speakers. In terms of Fed Governors (generally considered more influential with 14-yr terms who vote every year) we’ll get Bowman and Barr. In terms of regional Fed Presidents (who serve 5-yr terms (up to 10 yrs) and vote on a rotating schedule (except the NY Fed Pres (Williams) who votes every year) we’ll get Collins, Logan, and Barkin. .

But more importantly we’ll get the unofficial kickoff to 2Q earnings season with JP Morgan. Joining them in terms of SPX reporters will be BLK, WFC, C, BK, STT, JBHT, OMC (in order of market cap, the first three along with JPM are all >$100bn).

Ex-US DM we’ll get Germany and EU ZEW investor expectations, EU industrial production, and Canada CPI among other reports.

In EM, we’ll get the China monthly “data dump” including retail sales, industrial production, fixed asset investment, property sales, and employment along with GDP among other reports including South Korea and India trade and Poland CPI.

Link to X posts - Neil Sethi (@nelksethi) / X

To subscribe to these summaries, click below (it’s free!).

To invite others to check it out,