Markets Update - 7/16/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for tomorrow.

Quick Summary:

US equity indices started the Thursday session mostly trading solidly lower as the on-again, off-again love affair with semiconductors turned off again on the back of a continued selloff in South Korean heavyweights SK Hynix and Samsung and a poor reaction to Taiwan Semiconductor Manufacturing Co’s (TSMC) earnings which while a blowout on the revenue line also saw a big jump in its spending forecast as discussed in the morning update. The PHLX Semiconductor Index would end the day down 4.3%.

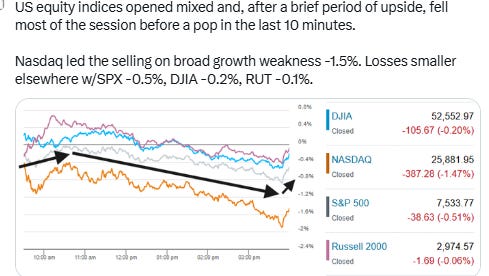

After a brief attempt at a rally, indices fell most of the session despite 8 out of 11 S&P 500 sectors finishing in the green as selling in growth names outweighed strength elsewhere. The Nasdaq Composite led the indices lower -1.5%, the S&P 500 fell -0.5%, the Dow Jones Industrial Average slipped -0.2%, and the Russell 2000 gave back earlier gains to finish -0.1%.

The weakness in the growth space broadened later in the day after reports Alphabet’s Gemini 3.5 Pro model will be delayed. As noted, though, under the surface, participation was stronger than the headline indices suggested. The S&P 500 Equal Weight Index gained +1.0%.

Economic data were mixed showing continued resilience in the consumer and labor market but a sluggish housing sector. June retail sales rose modestly but were held back by gasoline station sales which masked strength beneath the surface led by autos and online (Prime Day), initial jobless claims eased back remaining subdued historically and in the middle of multi-year ranges, June pending home sales fell the most this year, while the July NAHB Housing Market Index fell back to the least since September as builder concessions rose.

Oil settled modestly lower, though it remained higher for the week, as the US intensified strikes against Iran, hitting an oil tanker near the country’s main export terminal for the first time since the restart of the blockade on the Islamic Republic’s ports as discussed in the morning update.

Some market commentary:

“There’s been a lot of concentration in the market and that means there’s little room for error,” said Richard Flynn, managing director at Charles Schwab UK. “Global geopolitical risk is elevated and so there’s a relative tone of caution fundamentally looking at the macro outlook.”

“There’s been a lot of rotation within the AI trade, and a small rotation more broadly,” said Toni Meadows, head of investments at BRI Wealth Management. “It’s probably a healthy thing to have consolidation. The further things go, the more stretched they get and then the reaction is bigger.”

“The action in the chip stocks going forward is still the most-important issue for the stock market,” Matt Maley at Miller Tabak said. “They are definitely showing some meaningful cracks, so they’re going to have to see a strong and sustainable rebound soon or it will raise some real warning flags.”

“All told, it’s still a strong market when you look at earnings across all caps,” said Patrick Ryan, chief investment strategist at Madison Investments.

Consumer spending is a critical engine, and investors want to see households continue opening their wallets, according to Bret Kenwell at eToro. June’s retail sales report was not particularly robust, but it was not a red flag either — especially given the upward revision to May, he said. “Earnings should help separate signals from noise, revealing whether consumers remain resilient or are finally starting to pull back,” Kenwell concluded.

“Despite challenges, consumers are still spending and the labor market shows no signs of cracking,” said Ellen Zentner at Morgan Stanley Wealth Management. “This type of data won’t move the Fed’s needle either way, but it underscores the ongoing resilience of the US economy.”

In today’s Markets Update:

A deeper look at Thursday’s stock and sector breakdown, including semiconductor weakness, broader megacap growth pressure, and the rotation into defensive sectors.

A closer look at key company movers and corporate developments.

Updated technical charts across the SPX, Nasdaq, Russell 2000, and equal-weighted SPX.

A review of market breadth and participation, including large individual winners and losers, the equal-weighted SPX, and the split between headline index weakness and broader sector strength.

A look at the rates and Fed backdrop, including Treasury yields and Fed commentary from Dallas Fed President Logan.

A look at volatility and market structure, including VIX, VVIX, 1-day VIX, and options-expiration considerations.

A review of cross-asset trends, including WTI crude, the dollar, gold, copper, natural gas, and bitcoin.

A look at the after-hours drop in Netflix shares, Marvell’s weakness, the KBW bank index strength, Goldman’s high-beta momentum selloff, Leuthold on margin debt caution flags, BoA/Hartnett on excessive fund-manager positioning and cash levels, UBS on market themes, Yardeni on inflation, Goldman on the US-Iran war/macro backdrop, and Goldman on the Philadelphia Fed manufacturing report.

A look ahead to Friday’s calendar, including US economic data, Fed speakers, SPX earnings, and ex-US highlights.