Markets Update - 7/17/26

A look at what happened today impacting US equity, Treasury, and selected commodity markets, and what to watch for next week.

Quick Summary:

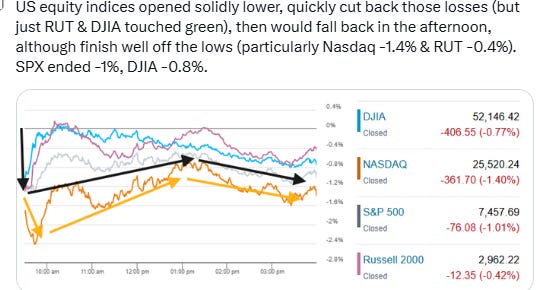

US equity indices opened solidly lower Friday, as the selloff in AI names continued after a powerful new model from Chinese AI pioneer Moonshot introduced new concerns about the sustainability of the US AI ecosystem as discussed in the morning update.

Indices though would quickly cut back those losses with a morning rally, although only the Russell 2000 and Dow Jones Industrial Average made it back to positive levels, before things unraveled again to a lesser extend in the afternoon, although indices all finished off their worst levels. The Nasdaq Composite led the decline -1.4%, the S&P 500 fell -1.0%, the Dow Jones Industrial Average declined -0.8%, and the Russell 2000 finished -0.4%.

Unlike Thursday, when the solidly down day for the S&P 500 masked 8 of 11 sectors finishing higher, Friday’s weakness was much broader with Energy the only positive sector. That saw the equal-weighted S&P 500 index fall -0.8%, just marginally better than its market cap-weighted counterpart. Growth sectors led the weakness with the Technology, Communication Services, and Consumer Discretionary sectors, three of the four largest, finishing at the bottom of the sector scorecard for a second day, all down at least 1%.

Also continuing to loom over markets was a very unstable Mid-East situation. Oil extended its advance after Axios reported that President Trump could decide within days whether to escalate military action against Iran, with options reportedly including strikes on Iranian infrastructure, nuclear facilities, and the underground Pickaxe Mountain site.

Economic data were mixed.

June housing starts beat expectations, but all due to a surge in multifamily starts while single-family starts and permits showed no growth.

Import prices rose more than expected mostly due to petroleum prices, although import prices from China hit a record monthly as the country moves up the value chain as discussed in Thursday’s morning update.

Industrial production was softer than expected (report coming) with US manufacturing production stalling, dragged down by a decline in durable goods such as machinery.

The preliminary July University of Michigan consumer sentiment reading improved more than expected, helped by lower gas prices, though the renewed jump in oil raises questions about whether that improvement can be sustained as inflation concerns remain elevated.

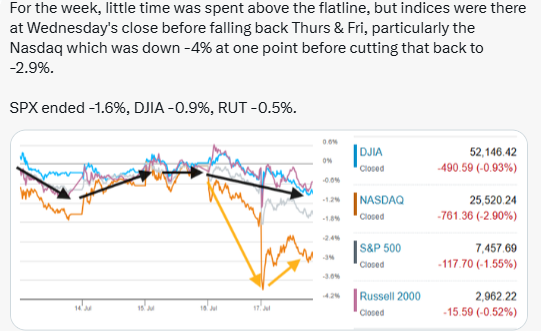

For the week, the indices spent little time above the flatline but were still there at Wednesday’s close before falling back Thursday and Friday. The Nasdaq Composite in particular was down as much as -4.0% for the week at one point this morning before cutting that loss to -2.9%, while the S&P 500 ended the week -1.6%, the Dow Jones Industrial Average -0.9%, and the Russell 2000 -0.5%.

Some market commentary:

“When there’s panic, no one wants to be the last one in a selloff, so the selling pressure increases,” said Guillermo Hernández Sampere, head of trading at MPPM. “With the start of reporting, the suspicion of overvaluation has been confirmed and will continue for a bit.”

“The question now is whether this will become yet another ‘buy the dip’ opportunity, or if the pace of selling accelerates as everyone rushes to the exit doors at the same time,” David Morrison at Trade Nation asked.

“The market has started to hope for some long-awaited broadening,” Citigroup Inc.’s Beata Manthey told Bloomberg Television. “For that to happen, you need to have some rotations, and rotations tend to happen in quite a violent way sometimes — and this is what we’re seeing right now.”

In a note on Friday morning, strategists at BBH said investors are “increasingly questioning the sustainability of the ongoing AI capital expenditure boom.”

“The [Bank for International Settlements] annual economic report cautions that boom-bust cycles are a regular feature of past investment surges driven by transformative technologies,” they said.

Barclays strategists appeared unperturbed by the tech volatility in a Friday note. “While Tech volatility may persist in the near term, we believe that the reset in positioning should ultimately prove healthy, creating more attractive entry points for long-term investors targeting the structural AI theme,” they said.

For Francisco Simon, European head of strategy at Santander Asset Management, the selloff still looks moderate in comparison to the preceding rally. “We would distinguish between fundamentals and positioning,” he said. “From a fundamental perspective, the picture remains solid: earnings momentum has been exceptional this year, and results are still coming in strongly.” Cash would offer good protection in the near term, Simon said. Bonds are a less attractive option as higher oil prices could undermine the defensive characteristics of sovereign debt. “The key reassurance would probably come from the earnings season,” he said. “If companies continue to deliver solid results, and valuations become more attractive after the correction, that could help bring longer-term buyers back.”

“The latest development is competition from open-source models in China, which are reportedly rivaling the performance of leading offerings from Anthropic and OpenAI, raising fresh concerns about the heavy pace of technology spending,” said Angelo Kourkafas, senior investment strategist at Edward Jones. “We are seeing signs of fatigue, with end-user demand for AI becoming more price sensitive and the market starting to penalize companies that are ramping spending too aggressively,” he continued. “We view this volatility as a signal that the AI theme is likely maturing rather than breaking, which is a healthy part of how transformative investment cycles evolve.”

With Iran continuing maritime attacks and insisting all ships seek its permission before sailing through the strait, there’s a good chance both sides continue to escalate, according to Mehran Kamrava, a professor of political science at Georgetown University in Qatar. The attacks are “an ominous sign of more to come, worse to come,” Kamrava told Bloomberg TV on Friday from Doha. “Neither side wants to see this escalation but both have become dependent on the path of an escalatory cycle from which they cannot back out. This tit-for-tat is now very dangerous in the sense of attacks and counter attacks on critical infrastructure.”

In today’s Markets Update:

A deeper look at Friday’s stock and sector breakdown, including semiconductor weakness tied to Moonshot AI, renewed megacap growth pressure, Energy’s relative strength, and the weakness broadening.

A closer look at key company movers and corporate developments.

Updated daily and weekly technical charts across the SPX, Nasdaq, Russell 2000, and equal-weighted SPX.

A review of market breadth and participation, including weakness among the largest stocks, IBM’s record week, and large individual winners and losers.

A look at the rates and Fed backdrop, including Treasury yields, Fed hike expectations, the move into the blackout period, and Fed Vice Chair Jefferson’s comments on inflation and the policy stance.

A look at volatility and market structure, including VIX, VVIX, 1-day VIX, and Citadel’s Rubner on the spike in stock-level risk relative to index risk.

A review of cross-asset trends, including WTI crude, the dollar, gold, copper, natural gas, and bitcoin including select weekly charts.

A comment on the Morgan Stanley Tech Momentum Index, Truist on Financials and Health Care, Goldman on high-beta momentum, Warren Pies on semiconductor analogs, Bloomberg on corporate insider selling, Goldman on central-bank gold demand, the Atlanta Fed GDPNow tracker, and John Authers on inflation swaps.

A wrap-up on the various cross-currents and Friday’s broader “sell everything” tone.

A look ahead to next week’s calendar, including US economic data, the Fed blackout, Treasury auctions, and SPX earnings.