Markets Update - 7/18/25

Update on US equity and bond markets, US economic reports, the Fed, and select commodities with charts!

To subscribe to these summaries, click below (it’s free!).

To invite others to check it out (sharing is caring!),

Link to posts - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog. Also please note that I do often add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

Finally, if you see an error (a chart or text wasn’t updated, etc.), PLEASE put a note in the comments section so I can fix it.

Major US equity indices started the day modestly higher (as they’ve been every session this week) on a less newsy overnight highlighted by Fed Gov Waller calling for a rate cut at the end of the month and with the SPX on track for the 3rd weekly gain in the last 4 weeks aided by overall strong corporate earnings. But equities dropped right from the open into negative territory and didn't really recover. SPX & Nasdaq ended flat, DJIA & Russell 2000 sported modest losses. For the week, markets finished well off the spike lows from the Powell firing headlines, but gains overall were moderate led by the Nasdaq's +1.5%. SPX was +0.6%, RUT +0.2%, DJIA -0.1%, with the SPX and Nasdaq closing at all-time weekly highs.

Elsewhere, Treasury yields edged lower as did the dollar. Crude and bitcoin were also lower, while copper and nat gas were higher. Gold was little changed.

The market-cap weighted S&P 500 (SPX) was UNCH, the equal weighted S&P 500 index (SPXEW) UNCH, Nasdaq Composite +0.1% (and the top 100 Nasdaq stocks (NDX) -0.1%), the SOX semiconductor index -0.1%, and the Russell 2000 (RUT) -0.6%.

Morningstar style box showed mostly losses although oddly mid-caps were green across all styles.

Market commentary:

“Investors have something to cheer about with signs of improved inflation expectations,” said Jeff Roach at LPL Financial. “According to this report, the trajectory looks encouraging.”

Jefferies International’s chief European strategist, Mohit Kumar, said risk assets are likely to remain well-supported until next month, when US employment data may start to show some weakness. “We remain positive on risky assets over the coming weeks, though we have taken some chips off the table,” Kumar noted. “Technicals will start to shift in August.”

“I think this market deserves the benefit of the doubt, and what got you here is still the growth sectors,” Keith Lerner, co-chief investment officer and chief market strategist at Truist, said on CNBC’s “Closing Bell.” “We would stick with the underlying trend, which still seems positive in our world,” he continued.

“It’s a risk-on environment, and while there’s chatter about Fed cuts, the reality is more nuanced,” said Ken Mahoney, CEO at Mahoney Asset Management. “Historically, bull cycles tend to perform better without rate cuts and the first cut is often a bearish signal, though there’s a valid case to be made this time around, especially with inflation cooling and GDP growth projections still intact after we got through the threat of massive tariffs.”

“The lack of any clear damage from the tariffs, solid earnings results, a firm job market, and consumers who keep spending are supporting the high valuations,” said Louis Navellier, chief investment officer at Navellier & Associates.

Early results show S&P 500 earnings are on track to rise 3.2% for the second quarter, slightly ahead of pre-season expectations of 2.8%, according to data compiled by Bloomberg Intelligence. “All that helps to reinforce the bull case for equities, with this solid underlying economic momentum likely to see earnings growth remain healthy,” said Michael Brown, senior research strategist at Pepperstone.

To Mark Hackett at Nationwide, macroeconomic data remains broadly supportive, and the recent strength in markets has been impressive, though perhaps even more noteworthy is the prevailing sense of calm amid a busy and often volatile news cycle. “Investors have responded positively to robust economic indicators and earnings reports that highlight continued resilience in US consumer spending,” he said. “The rest of earnings season will be a key test given elevated valuations and expectations, though with current momentum and sentiment, the path of least resistance is higher.”

The current market leaders will likely continue taking stocks higher from here, according to Chris Senyek, chief investment strategist at Wolfe Research.

“The leadership is led by industrials and tech, and those are the stalwarts of the economy. So I think that leadership continues,” he said on CNBC’s “Squawk on the Street” Friday morning. “Earnings results have been very solid.” As evidence, Senyek pointed to industrial stock 3M, which posted a second-quarter earnings and revenue beat on Friday morning. The company also raised its full-year sales growth guidance.

“We think [Waller] is correct. The Fed’s role is to think ahead, not look behind, which is what Waller is doing concerning the slowing employment situation,” said Andrew Brenner at NatAlliance Securities. “Nonetheless a July cut won’t happen.”

A "cleaving" of the Federal Open Market Committee appears to be emerging as President Donald Trump ratchets up his pressure campaign on the Federal Reserve to cut its benchmark rate, including a revived threat to fire Chair Jerome Powell, according to Thierry Wizman and Gareth Barry, strategists at Macquarie. Emerging is a "vocal side arguing for rate cuts to begin now," as well as "another side (including Jay Powell) still wanting a delay," the duo wrote Friday. The danger would be a split that could evolve around party lines, "at the expense of adherence to the price stability mandate," they said in a Friday client note. That risks a further steepening of the U.S. yield curve, and that could start costing the U.S. government, economy and households more to finance their debt.

Link to posts - Neil Sethi (@neilksethi) / X for more details/access to charts.

In individual stock action:

On the earnings front, Netflix slid 5% after the company said its operating margin in the second half of this year will be lower than the first. Shares of 3M fell more than 3% after the company revised its organic sales growth forecast to reflect a gain of 2%. It previously gave a growth range of the "lower end of 2% to 3%." A 2% post-earnings slide in American Express dragged the Dow lower.

Corporate Highlights from BBG:

The Food and Drug Administration plans to ask Sarepta Therapeutics Inc. to pause shipments of its Elevidys treatment after three deaths were linked to the company’s gene therapies, according to a person familiar with the matter.

Humana Inc. lost a lawsuit seeking to reverse cuts to its Medicare bonus payments, a blow for the insurer that had hoped the court would restore billions in revenue.

American Express Co.’s expenses grew in the second quarter as the firm made risk-management investments for its affluent consumers, who continued to spend amid economic uncertainty.

Netflix Inc. beat expectations for second-quarter results and continues to trounce rival media companies, yet the shares slipped on Friday as investors took a pause after the stock has nearly doubled over the past year.

3M Co. raised its profit forecast and beat Wall Street’s estimates for the second quarter as Chief Executive Officer William Brown’s effort to reinvigorate the company gained momentum.

Chevron Corp. has prevailed in a 20-month fight to buy Hess Corp. for $53 billion, overcoming a challenge by arch rival Exxon Mobil Corp. that was unprecedented in the modern history of Big Oil.

SLB, the world’s largest oil-services provider, sees resiliency in the industry and remains constructive about the second half of 2025 despite uncertainties in customer demand.

Interactive Brokers Group Inc. reported total net interest income for the second quarter that beat the average analyst estimate.

Charles Schwab Corp. reported earnings per share that topped estimates as the firm said client assets hit a new record and trading revenue rose.

Ally Financial Inc. left most of its forecast unchanged despite strong second-quarter consumer auto-loan originations and earnings.

Meta Platforms Inc. said it won’t sign the code of practice for Europe’s new set of laws governing artificial intelligence, calling the guidelines to help companies follow the AI Act overreach.

Some tickers making moves at mid-day from CNBC:

In US economic data:

June housing starts rebound +4.6% to 1.32mn SAAR, better than the +3.5% to 1.3mn expected (and after dropping -9.7% in May (which was the fifth move of at least 9% in six months) to the least since May 2020). The rebound in June, like the drop in May, was all in multifamily which jumped +30.6% (after falling -26.6 in May), taking them to an annual pace of 414k, the second quickest (after April) since Dec ‘23, while single-family dropped -4.6% to 883k, the slowest since last July. Getting even more granular, the jump in MF starts was almost all in the NE where they rose by 76%, the most since Mar ‘23.

After May broke the five month streak of increasingly stagflationary preliminary #UMich consumer sentiment surveys, July continued the improvement we’ve seen starting in the final May read, with sentiment improving further to 61.8, a 5-mth high and up +11.3pts from the 60.5 May preliminary read (which was the 2nd lowest on record after June ‘22) slightly above expectations for 61.5 (and vs the 60.7 in the final June read). The increase in sentiment was driven by Republicans and political independents (BBG). Similarly, inflation expectations continued to fall sharply at the 1yr horizon now to 4.4% from 5.0% in the final June read (and -2.8% from the preliminary May read), after the steepest drop since Oct ‘01 in June, while 5-10yr inflation expectations softened to 3.6% from 4.0% in the final June read (and 4.6% in the preliminary May read, the highest since 1991), both the lowest since February, “but remain above December 2024, indicating that consumers still perceive substantial risk that inflation will increase in the future."

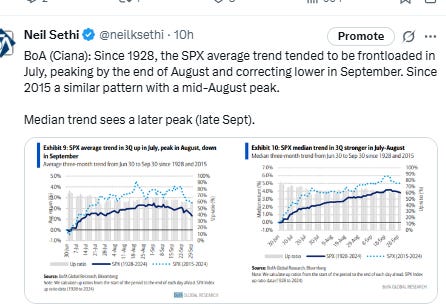

Link to posts for more details/access to charts (all free) - Neil Sethi (@neilksethi) / X

The SPX edged up to new ATH’s as it tries to push out of the mostly sideways range over the past 11 sessions. Its daily MACD and RSI are neutral.

Weekly charts continue to look very solid.

The Nasdaq Composite a similar but little more favorable picture.

Weekly

RUT’s (Russell 2000) “clear path to move at least to the 2300 level” per my note three weeks ago which had gone from “gotten choppy,” as I noted Friday, to “in jeopardy” as I noted Tuesday back to choppy Friday as it makes very slow progress to that 2300 target. Daily MACD is relatively neutral while the RSI still tilts a bit negative.

Weekly

Sector breadth from CME Cash Indices eased back after two strong sessions to just 5 of 11 sectors in the green (from nine Thurs & eight Wed but up from just one Tues, the worst in weeks), and one (Utilities) up over 1% (vs none Thurs). No sector down that much. Health care weak for a second session.

SPX stock-by-stock flag from FINVIZ_com relatively consistent with more red Friday, although just one more down more than -3% (ten vs nine the past two days). Health care continues to get more than its fair share with MOH, ELV, WST, VTRS, & CNC all down at least that much. Energy also well represented with SLB, XOM, & WAT. NFLX and MMM round out the list.

Much fewer stocks up over 3% though with just six (vs 45 Thurs, 12 Wed). They were INVZ, RF, VST, DELL, CEG & TSLA.

NYSE positive volume (percent of total volume that was in advancing stocks), which had been relatively strong the last couple of weeks but Fri-Wed, was much better Thurs before ending the week “ok” at 45.4% in line with the -0.23% loss in the index.

Nasdaq positive volume also was “ok” at 56.2%, vs the +0.05% gain in the index. But in comparison it was 76.1% July 10th on a +0.09% gain.

At least in part that was due to penny stock volumes (which I treat as sub $2) while remaining elevated falling to the lows of the week again accounting for just 6 of the top 13 stocks by volume (down from 7 Wed & Tuesday, 9 Monday and 12 Friday) while the total volume in those stocks came in at 1.24bn or 13.2% of total Nasdaq volume down from 14.6% Thurs and 17.6% Wed.

Positive issues (percent of stocks trading higher for the day) were weaker though at 38 & 39% respectively.

New 52-wk highs minus new 52-wk lows (red-black dotted lines) were little changed with the NYSE at 80 while the Nasdaq edged up to 208, its second best of the year.

Following Gov Waller’s call for a July rate cut, #FOMC rate cut pricing for 2025 rebounded from the least since February +3bps to 46bps according to CME’s #Fedwatch tool (still well below the 64bps July 2nd before the June NFP & from 92bps on May 1st (the peak this year was at 103bps on Apr 8th, the low was 36bps Feb 11th)).

The probability of a cut at the July meeting is 5% (meaning if Waller votes for a cut, it will be in dissent) down from 23% pre-NFP (and from 78% at the start of May) while a cut by the following meeting (Sept) edged to 61% from the lowest since February on Thursday (54%). It was 94% pre-NFP.

Chances of 2 cuts this year is 65% (down from 90% pre-NFP and also up from the lowest since February (60%)), three is 23% (down from 55%), and four is 1% (from 10%). The chance of no cuts low at 6.2% but still up from 0.6% pre-NFP..

2026 cuts also +3bps to 74bps, seeing total cuts through Dec '26 at 120bps, up now +12 bps from last week but -26bps from the start of May.

I said after the big pricing out of cuts in January (and again in February) that the market had pivoted too aggressively away from cuts, and that I continued to think cuts were more likely than no cuts, and as I said when they hit 60 bps “I think we’re getting back to fairly priced (and at 80 “maybe actually going a little too far” which is back to where we probably were Apr 20th (a little too far) at 102bps). Seems like we’re getting back to “fairly priced,” and as of May 14th at 48bps perhaps starting to go a little too far in the other direction, but as I’ve said all year “It’s a long time until December.”

Also remember that these are the construct of probabilities. While some are bets on exactly two, three, or four cuts much of it is bets on a lot of cuts (5+) or just one or none.

10yr #UST yields edged -3bps to 4.43% ending the week little changed after not getting through 4.5%.

The 2yr yield, more sensitive to #FOMC policy, -4bps to 3.87%, ending the week -2bps lower. It is -46bps below the Fed Funds midpoint, so still calling for rate cuts but also up +15bps this month.

I had said when it was around 4.35% (in Jan & again early Feb) that I found the 2-yr trading rich as it was reflecting as much or more chance of rate hikes as cuts while I thought it was too early to take rate cuts off the table (and too early to put hikes in the next two years on), but then the 2yr fell to 3.65% past where I thought we’d see it, so I took some exposure off there. We got back there but I never added back what I sold, so I stuck tight. Ian Lygan of BMO saw it going to 3.5% by year’s end before all this tariff business but now thinks it’s at fair value at around 3.75% so I took some more off at the end of June.

DXY dollar index (which as a reminder is very euro heavy (over 50%) and not trade weighted) fell back as it again couldn’t get over the 50-DMA/$99 level.

The daily MACD as noted last Monday crossed over to “cover shorts” while the RSI is just off the highest in nearly two months and over 50 after having moved from under to over 30, which can be a signal of a reversal of a downtrend, “so it’s got a lot of boxes checked for a move higher,” as I noted two weeks ago, but it’s having some trouble pushing through this resistance area.

Weekly chart improving but not quite there yet.

VIX remained right around 16 for the 17th straight session Friday at 16.4. The current level is consistent w/~1.03% average daily moves in the SPX over the next 30 days.

Remember, though, we’re in a seasonally strong period for the VIX. Chart from July 9th.

The VVIX (VIX of the VIX) like the VIX remained in the area it’s traded in the past 17 sessions at 93.2, still under Nomura’s Charlie McElligott’s “stress level” of 100 (consistent with “moderate” daily moves in the VIX over the next 30 days (normal is 80-100)).

Even though it was ahead of a weekend, the 1-Day VIX edged to the lowest close in a week Friday at 9.9, consistent with traders implying a ~0.62% move in the SPX next session.

#WTI futures fell back to close lower on the week looking they they’re going to lose their uptrend line from the May lows after failing to get through the 200-DMA resistance for over a week. The daily MACD remains in “sell longs” positioning while the RSI fluctuates around 50 but both softened over the week.

#oott

Weekly chart a similar story except the MACD is in a more positive configuration.

Gold futures (/GC) little changed as they continued to drift in the same range over the past three weeks. They remain around the bottom of the uptrend channel from January, right on the 50-DMA. Daily MACD remains negative as noted two weeks ago but is very close to flipping positive, while the RSI fluctuates around 50.

Weekly chart continues to deteriorate evidencing the clear loss of momentum.

Copper (/HG) futures got a boost from Pres Trump’s recommitment to copper tariffs Aug 1st which pushed them out of the wedge pattern they had been in since spiking higher last week on the Trump tariff threat. We’ll see if they can keep that going which would bode well for higher prices.

Weekly chart shows doji candle (indecision, possible reversal). Otherwise chart is very solid.

Nat gas futures (/NG) resumed their small run higher after breaking out of the short-term falling wedge they’d been trading in the past month on Monday, which as I noted “would commonly be associated with more good things to come for the bulls,” and now back over the 200-DMA, which as noted three weeks ago has for the most part held since last August.

Overall they remain in their range this year. Daily MACD and RSI have also turned more positive.

Weekly chart shows the rangebound action since October.

Bitcoin futures fell back but as noted Thurs seem to be forming a flag pattern not unlike what we say during their climb back in April/May. The daily MACD and RSI remain positive, the latter though going from over to under 70.

Weekly chart looks very solid as well.

The Day Ahead

Enjoy the weekend. After a busy week, we’ll get a lighter one next week before we get “one of those weeks” to end the month (a packed schedule of economic and earnings reports and central bank policy decisions along with the Aug 1st scheduled implementation date for Pres Trump’s new tariffs). For next week though, it’s lighter on the economic calendar with the headliners flash PMI’s, new and existing home sales, durable goods orders, and weekly jobless claims.

The Fed will be in their blackout period (it appears Chair Powell will be making opening remarks at a banking conference, but given he’s a stickler for the rules I doubt he’ll say anything about monetary policy).

Earnings though will heat up with 113 SPX components representing 20% of the SPX (by earnings weight) reporting with 23 >$100bn (GOOG/GOOGL, TSLA, KO, PM, IBM, TMUS, BX, RTX, NOW, TXN, T, ISRG, VZ, TMO, GEV, BSX, NEE, HON, COF, DHR, UNP, APH, CB, LMT, LMT, CME (and INTC is right there at $99.5bn).

Ex-US the global calendar is light as well (highlights from JPM below).

Link to X posts - Neil Sethi (@nelksethi) / X

To subscribe to these summaries, click below (it’s free!).

To invite others to check it out,