Markets Update - 7/21/25

Update on US equity and bond markets, US economic reports, the Fed, and select commodities with charts!

To subscribe to these summaries, click below (it’s free!).

To invite others to check it out (sharing is caring!),

Link to posts - Neil Sethi (@neilksethi) / X

Note: links are to outside sources like Bloomberg, CNBC, etc., unless it specifically says they’re to the blog. Also please note that I do often add to or tweak items after first publishing, so it’s always safest to read it from the website where it will have any updates.

Finally, if you see an error (a chart or text wasn’t updated, etc.), PLEASE put a note in the comments section so I can fix it.

Major US equity indices started the day modestly higher (as they also were every session last week) following a welcomed less newsy period since Friday’s close. They traded sideways most of the day with some deterioration led by the Russell 200 which along with the DJIA finished lower. SPX and Nasdaq ended modestly in the green.

Elsewhere, Treasury yields fell back as did the dollar. Crude, bitcoin, and nat gas were also lower, while gold and copper gained.

The market-cap weighted S&P 500 (SPX) was +0.1%, the equal weighted S&P 500 index (SPXEW) -0.3%, Nasdaq Composite +0.4% (and the top 100 Nasdaq stocks (NDX) +0.5%), the SOX semiconductor index +0.1%, and the Russell 2000 (RUT) -0.4%.

Morningstar style box saw just modest gains at the large cap level, losses elsewhere.

Market commentary:

“Markets survived a ‘near-death’ experience in April after the president reversed course. Investors believe he’s afraid of the stock market and does not have the nerve to follow through on market-adverse policies,” said Michael O’Rourke, chief market strategist at JonesTrading LLC. Now they’re “embracing risk in all corners of the financial markets.”

“Equities still have, particularly in the US, a little bit of room to run further,” Max Kettner, chief multi-asset strategist at HSBC Holdings Plc, said on Bloomberg TV. “Let’s remember that we were going into this reporting season with very low expectations.”

“We’re at an all time high for the [S&P 500] right at the beginning of earnings season,” said Mark Malek, investment chief at Siebert Financial, adding, “If we can get through this earnings season with not too many major failures, I think that is really, really important at this point, if we want to continue this upward momentum that we have in the market.”

"Big banks kicked off earnings season on a mostly positive note last week, but tech and AI enthusiasm played a bigger role in helping some of the major indexes tag more record highs," said Chris Larkin, managing director for trading and investing at E-Trade from Morgan Stanley, in a note. The Nasdaq ended Friday at a record, while the S&P 500 notched a record finish on Thursday. "But with the S&P 500 up less than 0.3% over the past two weeks, it’s clear the market is still searching for its next catalyst. This week’s light economic calendar will put the focus squarely on earnings, including the first Mag-7 names to report this season," he wrote.

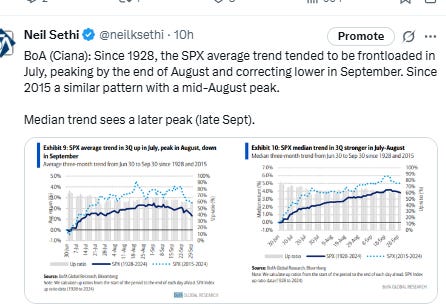

As Aaron Nordvik at UBS Securities LLC sees it, the tailwinds that were driving shares higher are now easing, such as the stock market’s history of strength in July. “I’ve been quite bullish for a while now, but most of the good news is now in the price,” said Nordvik, a macro equity strategist at the firm. While he says a sharp slump is unlikely, in his view the risk-reward profile for equities is less attractive than even just a couple weeks ago.

To Matt Maley at Miller Tabak, it is becoming more evident that the Trump Administration is going to be tougher on the tariff issue going forward. So, it’s important to decide whether this is something the stock market is pricing in right now. “Earnings season will move into full swing this week, and the guidance will be more important than usual,” he said. “This guidance is going to have create a very large increase in earnings estimates if the market is going to reach some of the targets that exist on Wall Street right now.

“While stocks may be due for a breather, we believe the bull market remains intact,” said Ulrike Hoffmann-Burchardi at UBS Global Wealth Management. “We maintain our June 2026 S&P 500 price target of 6,500, and recommend using volatility as an opportunity to phase into markets.”

Morgan Stanley strategists led by Michael Wilson advise investors to stay bullish on US stocks, as earnings momentum, positive operating leverage and cash tax savings are under-appreciated tailwinds.

Recent dollar weakness should provide a small tailwind to S&P 500 earnings, partially offsetting the tariff earnings pressure, Goldman Sachs Group Inc. strategists led by David Kostin said.

“Although valuations are elevated, a large component of the S&P 500 consists of large cap tech stocks which command higher multiples due to their consistent growth, incredibly strong cash flows and profit margins,” said Richard Saperstein at Treasury Partners. “Valuation isn’t a reliable indicator for future market direction.” The combination of declining inflation, continued growth and stable interest rates is a trifecta of positives that supports current stock market valuations, he noted. “Most of the Magnificent Seven should continue leading the market due to impressive earnings growth, copious levels of cash flow and continued demand for their businesses,” he said. “The AI tailwinds are in the early innings, and are set to benefit the biggest players in tech the most.”

It appears bearish investors may be capitulating as U.S. companies’ second-quarter earnings reports so far are strong and stocks are up since the White House announced tariffs in April, according to money-management firm Navellier & Associates. “With earnings strong and new highs being hit almost daily, not only is short covering in motion, but the huge amount of cash still on the sidelines has growing FOMO (Fear of Missing Out),” Louis Navellier, the firm's chief investment officer, said in emailed comments Monday. “In earnings reports, we keep hearing that there are few signs of customer concerns about tariffs or geopolitical issues,” he said. “It can be argued that we have yet to see the full impact of tariffs, as most have yet to be finalized, but there has been a global 10% in place since April, and stocks have gone straight up since.”

“Given the better-than-expected inflation and economic data — not to mention corporate commentary which thus far has been pretty good — I’m not sure I’d put too much stock in the technicals right now,” said Dan Greenhaus at Solus Alternative Asset Management, the firm’s chief market strategist.

“We would have always assumed there is no basis for firing a Fed chair and the Fed has been immune from political interference,” said Mark Dowding, chief investment officer of the BlueBay Fixed Income unit at RBC Global Asset Management. “There is a clear sense that this is now changing.”

Link to posts - Neil Sethi (@neilksethi) / X for more details/access to charts.

In individual stock action:

Both the SPX and Nasdaq hit new all-time intraday highs earlier in the session, bolstered by advances in major technology names like Meta Platforms and Amazon. Alphabet was a standout in the session, increasing more than 2% ahead of its quarterly results Wednesday after the bell. That name as well as Tesla — the first of the “Magnificent Seven” companies set to report — could boost the major averages if they manage to beat estimates. Shares of the electric vehicle maker ended the session marginally lower. Energy shares joined a decline in oil. Chipmakers almost erased their advance as Nvidia Corp. slipped.

Corporate Highlights from BBG:

Hackers exploited a security flaw in common Microsoft Corp. software to breach governments, businesses and other organizations across the globe and steal sensitive information, according to officials and cybersecurity researchers.

Verizon Communications Inc. posted second-quarter revenue that surpassed analysts’ estimates and raised its profit outlook, buoyed by wireless price increases and recent tax legislation.

Block Inc. rallied as the firm is set to join the S&P 500, a milestone that underscores the growing influence of digital payments and crypto in mainstream finance.

Domino’s Pizza’s launch of its Parmesan stuffed-crust pizza attracted new customers and boosted the company’s same-store sales, company executives said on its earnings call.

Opendoor Technologies Inc. soared on Monday, extending its gravity-defying rally from last week, as investors continued to pile into the stock that has found a sudden fandom among retail traders and social-media platforms.

Elliott Investment Management has built up its stake in Equinix Inc. and is pushing the data center operator to take steps to boost its share price, people with knowledge of the matter said.

BP Plc, under pressure from activist investor Elliott Investment Management to improve its performance, appointed the former boss of a building-materials company as its new chairman, replacing Helge Lund.

Shares of global consumer intelligence platform NIQ Global Intelligence Plc are expected to start trading this week, and their performance could open the door for other private equity-backed companies weighing going public.

GE Vernova Inc. is acquiring French software company Alteia SAS as the maker of power generation equipment looks to use artificial intelligence for ways to strengthen the electric grid.

Some tickers making moves at mid-day from CNBC:

In US economic data:

Link to posts for more details/access to charts (all free) - Neil Sethi (@neilksethi) / X

The SPX edged up to new ATH’s as it tries to push out of the mostly sideways range over the prior 11 sessions. Its daily MACD and RSI are neutral.

The Nasdaq Composite a similar but little more favorable picture. Getting increasingly overbought though.

RUT’s (Russell 2000) “clear path to move at least to the 2300 level” per my note three weeks ago remains “choppy” to “in jeopardy” as I have described it variously during that time. Daily MACD is starting to slip negative while the RSI is mixed but for now remains above 50.

Sector breadth from CME Cash Indices a little better Monday with 7 of 11 sectors in the green (up from five Friday but down from nine Thurs), and again just one (Comm Services) up over 1% (it was Utilities Friday). Again, though, no sector down that much (although Energy was again close finishing -0.96% lower for a second session (odd)). Health care weak for a third session (-0.61% after -0.60% Friday).

Megacap growth outperformed taking top two spots.

SPX stock-by-stock flag from @FINVIZ_com relatively consistent although it doesn’t look as favorable as the sector-by-sector chart, very mixed.

Still just seven components down more than -3% (vs 9 or 10 the past three sessions). Health care continued to get its fair share (MOH, TECH, CRL), while five were in energy (EQT, EXE, CTRA, TRGP, OKE). URI the only other component.

Just four stocks up over 3% (vs 6 Friday, 45 Thurs, 12 Wed). They were VZ, HSY, ROST, DECK.

NYSE positive volume (percent of total volume that was in advancing stocks), which had been relatively strong coming into last week and has been mixed since then remained so at 46% in line with the -0.13% loss in the index, but it was 45.4% Friday with a slightly larger (-0.23%) loss.

Nasdaq positive volume was better at 64.8%, vs the +0.38% gain in the index. But in comparison it was 75.5% Wed on a +0.25% gain.

And the weaker positive volume can’t be blamed on less penny stock volumes (which I treat as sub $2) which accounted for 8 of the top 13 stocks by volume (up from 6 Friday and 7 Wed (but down from 12 a week ago Friday) and the total volume in those stocks came in at a huge 2.6bn or 21.4% of total Nasdaq volume up from 13.2% Friday and 17.6% Wed.

And that doesn’t count meme stock Opendoor which at one point was up 1,000% this month and traded 1.86 billion shares on its own accounting for 15% of total Nasdaq volume.

Positive issues (percent of stocks trading higher for the day) were around the same level on the NYSE but unsurprisingly weaker on the Nasdaq at 47 & 52% respectively.

New 52-wk highs minus new 52-wk lows (red-black dotted lines) edged back on the NYSE to 59 but the Nasdaq improved to 228, its second best level of the year.

FOMC rate cut pricing for 2025 softened a bit but remained above the least since February hit on Thursday -1bps to 45bps according to CME’s #Fedwatch tool (still well below the 64bps July 2nd before the June NFP & from 92bps on May 1st (the peak this year was at 103bps on Apr 8th, the low was 36bps Feb 11th)).

The probability of a cut at the July meeting is 3% (meaning if Waller votes for a cut, it will be in dissent) down from 23% pre-NFP (and from 78% at the start of May) while a cut by the following meeting (Sept) edged to 57% a little above the lowest since February on Thursday (54%). It was 94% pre-NFP.

Chances of 2 cuts this year is 65% (down from 90% pre-NFP and also up from the lowest since February (60%)), three is 22% (down from 55%), and four is 0.5% (from 10%). The chance of no cuts low at 6.4% but still up from 0.6% pre-NFP.

2026 cuts also -1bps to 73bps, seeing total cuts through Dec '26 at 118bps, down -28bps from the start of May.

I said after the big pricing out of cuts in January (and again in February) that the market had pivoted too aggressively away from cuts, and that I continued to think cuts were more likely than no cuts, and as I said when they hit 60 bps “I think we’re getting back to fairly priced (and at 80 “maybe actually going a little too far” which is back to where we probably were Apr 20th (a little too far) at 102bps). Seems like we’re getting back to “fairly priced,” and as of May 14th at 48bps perhaps starting to go a little too far in the other direction, but as I’ve said all year “It’s a long time until December.”

Also remember that these are the construct of probabilities. While some are bets on exactly two, three, or four cuts much of it is bets on a lot of cuts (5+) or just one or none.

10yr #UST yields fell back -6bps to 4.37% falling back away from 4.5%.

The 2yr yield, more sensitive to #FOMC policy, saw less of a pullback -1bps to 3.86%. It is -47bps below the Fed Funds midpoint, so still calling for rate cuts but also up +14bps this month.

I had said when it was around 4.35% (in Jan & again early Feb) that I found the 2-yr trading rich as it was reflecting as much or more chance of rate hikes as cuts while I thought it was too early to take rate cuts off the table (and too early to put hikes in the next two years on), but then the 2yr fell to 3.65% past where I thought we’d see it, so I took some exposure off there. We got back there but I never added back what I sold, so I stuck tight. Ian Lygan of BMO saw it going to 3.5% by year’s end before all this tariff business but now thinks it’s at fair value at around 3.75% so I took some more off at the end of June.

DXY dollar index (which as a reminder is very euro heavy (over 50%) and not trade weighted) fell back more notably Monday from the 50-DMA/$99 level. It did find some support at the 20-DMA so we’ll see if that will hold.

The daily MACD as noted two weeks ago crossed over to “cover shorts” and while the RSI had hit the highest in nearly two months and over 50 after having moved from under to over 30, which can be a signal of a reversal of a downtrend, it’s now softened back to a 2-week low. I had said two weeks ago “it’s got a lot of boxes checked for a move higher,” and we did see a healthy move, but as noted Friday “it’s having some trouble pushing through this resistance area,” and technicals are softening.

VIX remained right around 16 for the 18th straight session at 16.7. The current level is consistent w/~1.04% average daily moves in the SPX over the next 30 days.

Remember, though, we’re in a seasonally strong period for the VIX. Chart from July 9th.

The VVIX (VIX of the VIX) like the VIX remained in the area it’s traded in the past 18 sessions at 92.3, still under Nomura’s Charlie McElligott’s “stress level” of 100 (consistent with “moderate” daily moves in the VIX over the next 30 days (normal is 80-100)).

1-Day VIX fell to the lowest close since Dec 11th at 8.85, consistent with traders implying a ~0.55% move in the SPX next session. It’s now firmly broken its uptrend line from the December lows.

#WTI futures again tested the 50/100-DMA/$65 support which again held. They’ve now officially lost their uptrend line from the May lows after failing to get through the 200-DMA resistance for over a week. The daily MACD remains in “sell longs” positioning while the RSI fluctuates around 50 but both softened last week.

#oott

Gold futures (/GC) finally broke out of their three week malaise jumping 1.6% to the highest close in that time. They still remain around the bottom of the uptrend channel from January, a little above the 50-DMA. Also, the move flipped the daily MACD to a positive “go long” configuration, while the RSI pushed near a 1-mth high and over 50, so a lot of good things happening with the gold chart.

Copper (/HG) futures continued their move up after pushing out of the wedge pattern they had been in since spiking higher two weeks ago on the Trump tariff threat. As noted on Friday that would normally “bode well for higher prices.”

Nat gas futures (/NG) fell back giving up all of their small run higher after a week ago breaking out of the short-term falling wedge they’d been trading in for a month. Now back under the 200-DMA, which as noted last month has for the most part held since last August.

Overall they remain in their range this year. Daily MACD and RSI have also turned more negative.

Bitcoin futures fell back but as noted Thurs seem to be forming a flag pattern not unlike what we say during their climb back in April/May. The daily MACD and RSI remain positive, although the latter has gone from over to under 70 and is the weakest in a couple of weeks.

The Day Ahead

As noted at the start of the week, it’s a light calendar for US economic data this week, and there’s no major US economic data Tuesday.

The Fed will be having their Capital Framework for Large Banks Conference on Tuesday where Chair Powell will be making opening remarks and Michelle Bowman will be participating in a “fireside chat”, but given the pretty hard rule on discussing monetary policy, I doubt we’ll get anything on that front.

And earnings will continue to build with 32 SPX reporters of which nine are >$100bn in market cap (KO, PM, RTX, TXN, ISRG, COF, DHR, CB, LMT (highest to lowest market caps)).

EX US DM we’ll get the ECB lending survey, an update on UK public finances, and RBA meeting minutes among other reports.

In EM, we’ll get a policy decision from Hungary and a number of reports from Mexico among others.

Link to X posts - Neil Sethi (@nelksethi) / X

To subscribe to these summaries, click below (it’s free!).

To invite others to check it out,