May 2022 NY Fed Survey of Consumer Expectations - "Inflation Expectations Rise at One-Year Horizon, along with Spending Expectations"

Longer term inflation expectations remained unchanged while spending and labor market conditions remained robust

May 2022 NY Fed Survey of Consumer Expectations - "Inflation Expectations Rise at One-Year Horizon, along with Spending Expectations"

Survey of Consumer Expectations - FEDERAL RESERVE BANK of NEW YORK (newyorkfed.org)

The May 2022 NY Fed's Survey of Consumer Expectations may provide a small amount of comfort to Fed officials as it showed no increase in longer term inflation expectations. But it showed no slowdown in spending intentions which moved to a new series high (since 2013) nor cooling in the job market. Also 1-year inflation expectations reaccelerated after falling in April.

The 1-year inflation expectations, which had climbed to a new record of 6.6% in March matched that again in April. Three years out remained at 3.9%, remaining below the series high of 4.2% . Median inflation uncertainty (i.e., the spread between the 25th and 75th percentile) remained at series highs. Expectations for home prices declined to 5.8% from 6% but that remains elevated compared to pre-pandemic levels.

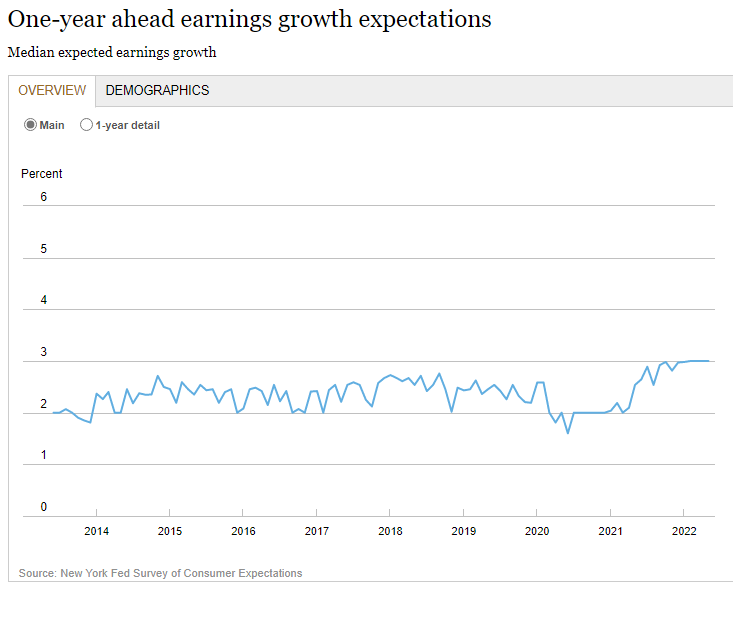

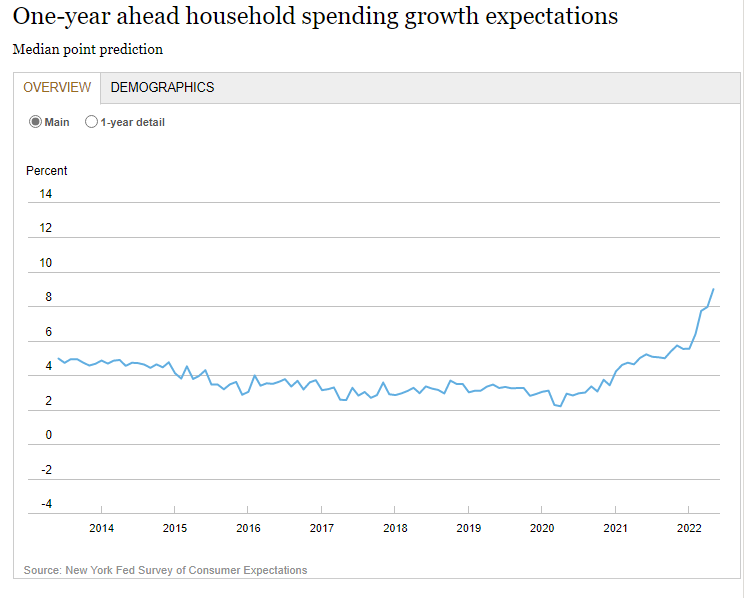

As noted we saw spending expectations hit a new series high for a third month, and earnings growth expectations remained at its series high for a fifth month at 3.0%. The chances of losing one’s job, which had fallen to a series low in April, ticked up marginally, but remained well below pre-pandemic levels while the probability of finding a new job increased to the highest since February 2020, and the probability of quitting a job increased to the highest since September 2020.

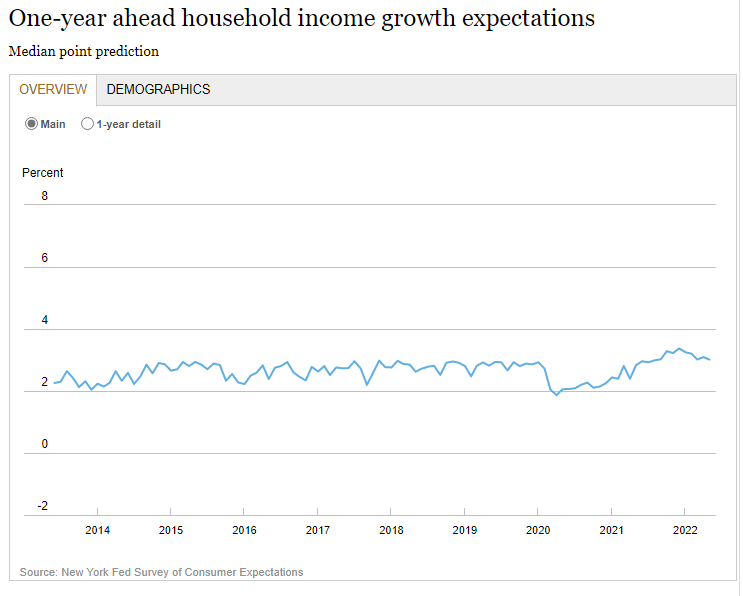

Household income growth expectations fell a tenth to 3.0%, one tenth above the 2021 average of 2.9%. As noted though perceptions of credit access compared to a year ago deteriorated sharply in May, decreasing for a fifth consecutive month, with more respondents saying it is harder to obtain credit than a year ago. Expectations about future credit availability also deteriorated, with more respondents expecting it will be harder to obtain credit in the year ahead.

Perceptions about households’ current financial situations deteriorated noticeably with more respondents reporting they are financially worse off today than a year ago, and year-ahead expectations about households’ financial situations also deteriorated. This is probably not very surprising given how we’ve seen inflation weigh on consumer sentiment in other reports.

Overall, this report remains more encouraging than most of the other sentiment surveys, particularly the continued consumer resilience and strong labor market conditions. Seeing 1-year inflation expectations tick up was not much of a surprise, but it was good to see longer term expectations not increase. It is unfortunate, though, to see the toll that inflation is taking on perceptions of financial health.

Here is the summary from the report, but I bolded some areas to emphasize for quicker reading if desired.

NEW YORK—The Federal Reserve Bank of New York’s Center for Microeconomic Data today released the May 2022 Survey of Consumer Expectations, which shows that inflation expectations increased at the one-year horizon and remained stable at the three-year horizon. Household spending expectations over the next year rose sharply to a new series high. Credit access perceptions (relative to a year ago) and expectations (one year from now) both deteriorated. Similarly, households’ perceptions and expectations for current and future financial situations both deteriorated in May.

The main findings from the May 2022 Survey are:

Inflation

The one-year ahead median inflation expectations increased from 6.3% to 6.6% in May, tying the highest reading of the series since the inception of the survey in June 2013. In contrast, the median three-year-ahead inflation expectations remained unchanged at 3.9%. Our measure of disagreement across respondents (the difference between the 75th and 25th percentile of inflation expectations) increased both at the one-year and the three-year horizons.

Median inflation uncertainty—or the uncertainty expressed regarding future inflation outcomes—retreated at the short-term horizon from a series high in May. In contrast, median inflation uncertainty increased to a new series high at the medium-term horizon.

Median one-year ahead home price expectations declined to 5.8% from 6.0% in April but remains elevated relative to pre-pandemic levels.

After declining sharply last month, the year-ahead expected change in the price of gas rose slightly to 5.5% in May. In contrast, the expected change in the price of food, medical care and rent all fell by 0.1 percentage point to 9.3%, 9.4% and 10.2%, respectively. Similarly, the median expected change in the cost of a college education declined by 0.5 percentage point to 8.6%.

Labor Market

Median one-year-ahead earnings growth expectations remained unchanged for the fifth consecutive month at its series high of 3.0%.

Mean unemployment expectations—or the mean probability that the U.S. unemployment rate will be higher one year from now—increased for the third consecutive month from 36.3% in April to 38.6% in May. This is the highest reading since February 2021.

The mean perceived probability of losing one’s job in the next 12 months increased by 0.3 percentage point to 11.1%, remaining well below the series’ 2021 average of 12.5%. The mean probability of leaving one's job voluntarily in the next 12 months increased sharply to 20.3% from 19.0% in April. This is the highest reading since September 2020.

The mean perceived probability of finding a job (if one’s current job was lost) increased from 57.4% in April to 58.2%, its highest value since February 2020. The increase was driven by respondents over 40, those without a college education and those with lower household incomes (under $50,000).

Household Finance

The median expected growth in household income decreased by 0.1 percentage point to 3.0% in May, remaining just above its 2021 average of 2.9%.

Median household nominal spending growth expectations increased sharply to 9.0% from 8.0% in April. This is the fifth consecutive increase and a new series high. The increase was most pronounced for respondents between the age of 40 and 60 and respondents without a college education.

Perceptions of credit access compared to a year ago deteriorated sharply in May, with more respondents saying it is harder to obtain credit than a year ago. This marks the fifth consecutive month of decline in this series. Expectations about future credit availability also deteriorated, with more respondents expecting it will be harder to obtain credit in the year ahead.

The average perceived probability of missing a minimum debt payment over the next three months increased by 0.4 percentage point to 11.1% in May. The increase was most pronounced for respondents between the age of 40 and 60.

The median expectation regarding a year-ahead change in taxes (at current income level) decreased by 0.1 percentage point to 4.6% but remains just above its 12-month trailing average of 4.5%.

Median year-ahead expected growth in government debt increased by 1.4 percentage points to 11.9%, well above its pre-pandemic reading of 6.0% in February 2020.

The mean perceived probability that the average interest rate on saving accounts will be higher 12 months from now increased for the fifth consecutive month to 35.0%, its highest reading since January 2019.

Perceptions about households’ current financial situations deteriorated noticeably in May with more respondents reporting they are financially worse off today than a year ago. Year-ahead expectations about households’ financial situations also deteriorated in May, with more respondents expecting to be worse off a year from now than they are today.

The mean reported probability that U.S. stock prices will be higher 12 months from now decreased by 1.7 percentage point to 36.2%.

About the Survey of Consumer Expectations (SCE)

The SCE contains information about how consumers expect overall inflation and prices for food, gas, housing, and education to behave. It also provides insight into Americans’ views about job prospects and earnings growth and their expectations about future spending and access to credit. The SCE also provides measures of uncertainty regarding consumers’ outlooks. Expectations are also available by age, geography, income, education, and numeracy.

The SCE is a nationally representative, internet-based survey of a rotating panel of approximately 1,300 household heads. Respondents participate in the panel for up to 12 months, with a roughly equal number rotating in and out of the panel each month. Unlike comparable surveys based on repeated cross-sections with a different set of respondents in each wave, our panel allows us to observe the changes in expectations and behavior of the same individuals over time.

To subscribe to these summaries, click below.

To invite others to check it out:

To see more content, including summaries of most major U.S. economic reports and my morning and nightly updates go to Neil’s Newsletter Substack for newer posts or https://sethiassociates.blogspot.com for the full history.