Productivity - 4Q 2025

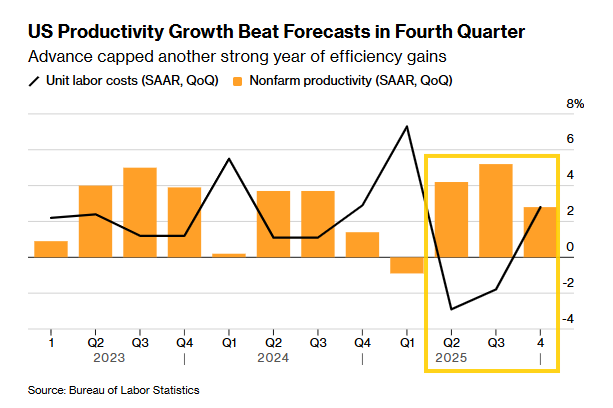

Productivity decelerates but remains solid coming in above expectations while unit labor costs are also above expectations on very strong compensation growth

Productivity is a metric closely followed by the Fed, and one which has heightened importance today given the avowed feeling from several Fed members (as well as likely incoming Fed chair Warsh) that like the 1990’s, productivity may be the key to allowing for rate cuts even while maintaining strong growth and a relatively healthy labor market while also continuing to see inflation moderate (it’s been described by some economists as “fairy dust”).

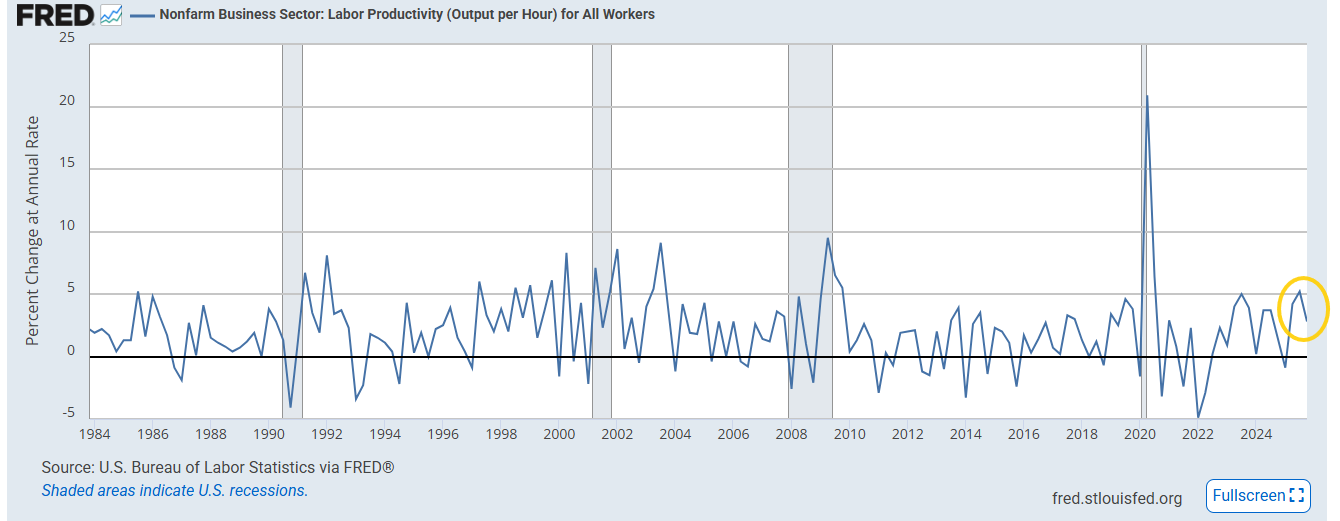

With that intro, the 4Q preliminary number came in at a solid +2.8% Q/Q SAAR, above the +1.9% median Bloomberg economist forecast, although slowing from an upwardly revised +5.2% in Q3 (from the initially reported +4.9%), the strongest quarter since Q3 ‘23. Pre-pandemic we didn’t have a quarter that strong since 2009, and before that 2020. For full year 2025 productivity increased +2.2%.

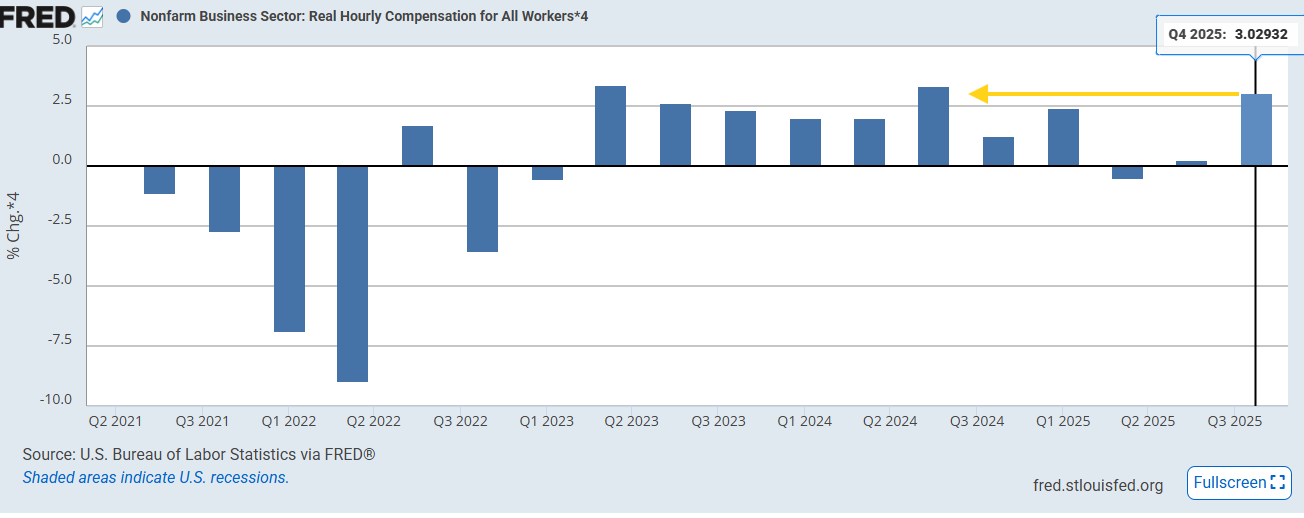

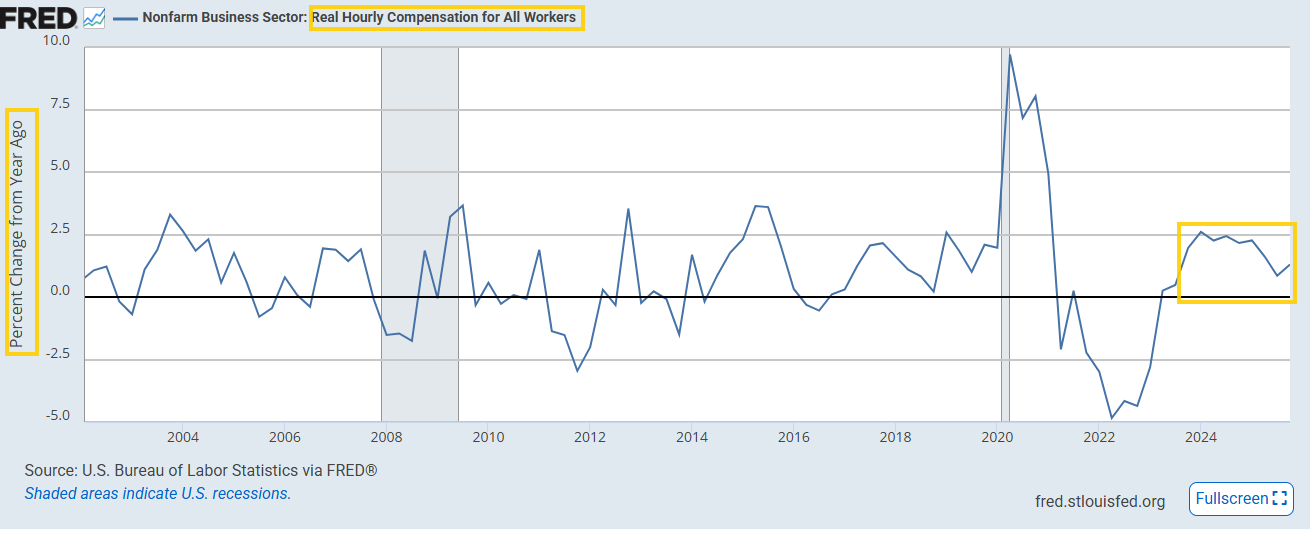

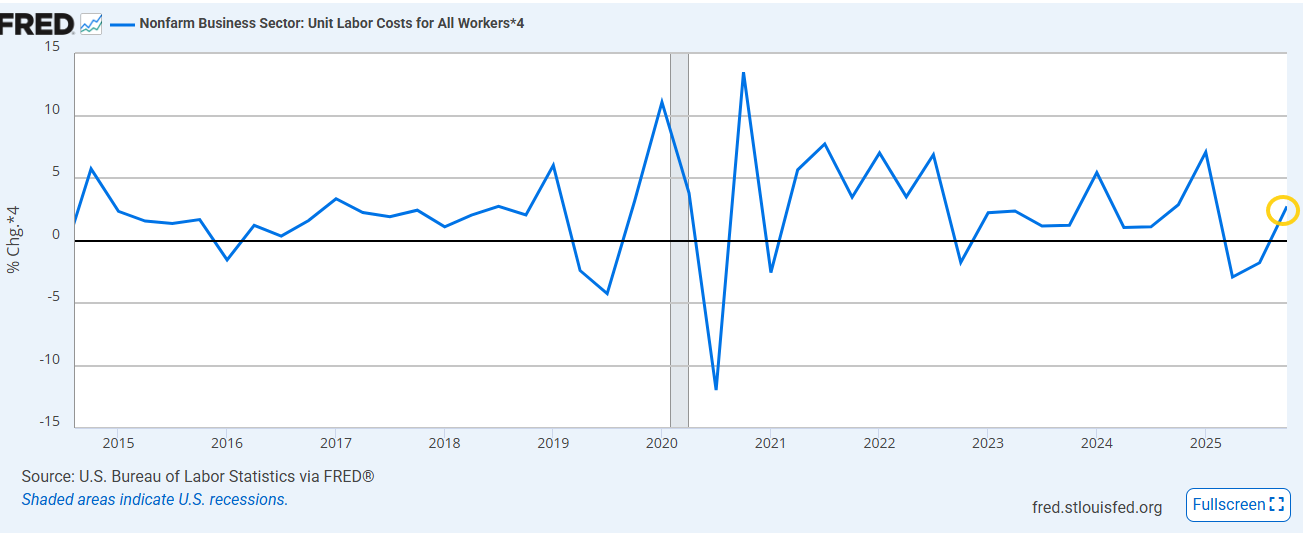

However, even with the strong productivity, unit labor costs (ULC), a key component of wage pressures, rose +2.8% in Q4 — a reversal from the prior two quarters of declines (-1.8% revised in 3Q and -2.9% in Q2) — as the productivity gain was offset by a +5.7% surge in hourly compensation (which saw real (inflation-adjusted) compensation rise +3.1%, the fastest pace in more than a year). On a y/y basis unit labor costs came in at +1.3% and and ULC rose +1.9%, both consistent with the Fed’s 2% inflation target.

Digger deeper, the gains were less broad based than in Q3 with services (non-manufacturing) +2.8% Q/Q SAAR but manufacturing -1.9%, with the decline led by durable manufacturing -3.0% (non-durable -0.2%).

As a result, manufacturing ULC surged +8.3% — the largest increase since Q3 2022 (+11.4%) — with +6.2% rise in hourly compensation running against the productivity decline. Services ULC was a more contained +2.7% although compensation was up a similar +5.6%, helped by the better productivity.

For full year 2025, though, manufacturing productivity rose +2.0% according to the report, the largest annual gain since 2010, with manufacturing ULC rising +2.3% — lower than each of the prior three years, each of which exceeded +4.0%. Manufacturing real hourly compensation increased +1.6% in 2025.

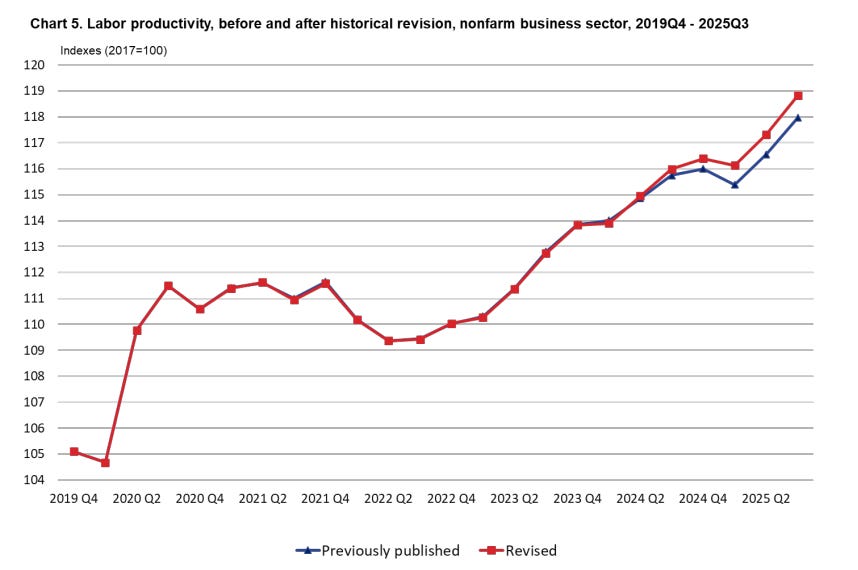

Also, the report made healthy revisions to the past five years with “the largest revisions in 2024 and 2025…combined with the fourth-quarter increase, resulted in an upward revision in the growth rate for the current business cycle, from 2.0 percent to 2.2 percent.” (chart below)

https://www.bls.gov/news.release/pdf/prod2.pdf

Productivity (Q/Q SAAR)

Real (inflation-adjusted) compensation

ULC (Q/Q SAAR)

Past quarters revised higher

To subscribe to these summaries, click below.

To invite others to check it out,