The Week Ahead - 2/22/26

A comprehensive look at the upcoming week for US economics, equities and fixed income

If you're a new reader or maybe one who doesn’t make it to the end feel free to take a second to subscribe now.

Or please take a moment to invite others who might be interested to check it out.

Please note that I do sometimes add to or tweak items after first publishing, so it’s usually safest to read it from the website where it will have any updates.

As a reminder, some things I leave in from prior weeks for reference purposes, because it’s in-between updates, it provides background information, etc.. Anything not updated this week is in italics. As always apologize for typos, errors, etc., as there’s a lot here, and I don’t really have time to do a thorough double-check.

For new subscribers, this is a relatively long post. The intent is to cover the same areas each week. Sometimes the various areas are more interesting, sometimes less, but it’s easier just to go through them all, so you can expect this format (with things in the same places) each week.

The main sections are intended to cover 1) what’s upcoming next week, 2) what the Fed and rates markets are up to, 3) what’s going on with earnings (which along with valuations and positioning are the main determinants to stock prices), 4) what’s going on with the economy (both because of its impact on our daily lives but also because it impacts earnings), 5) valuations, 6) breadth (which gets into sector/style performance), 7) positioning/flows (this is a key determinant to asset price changes in the short term), 8) sentiment (really only matters at extremes but interesting to track), 9) seasonality (gives you an idea of what normally happens), 10) “Final Thoughts” and 11) my portfolio (to be transparent about where my money is in the market (but note first it is most definitely not intended as financial advice, and second my portfolio is invested with the intention of wealth building not daily income, etc., so my portfolio is built with that in mind (plus finally see note about MLP’s in that section)).

A quick thank you to the many who have contributed to the charity fund. I appreciate very much each paid membership, and I have tried to respond to all messages from paid members. If you have sent me a message, and I have not responded, please don’t hesitate to send a new message, as it likely it was just buried in my email inbox or caught in my spam filter (I’m working on fixing that issue).

The Week Ahead

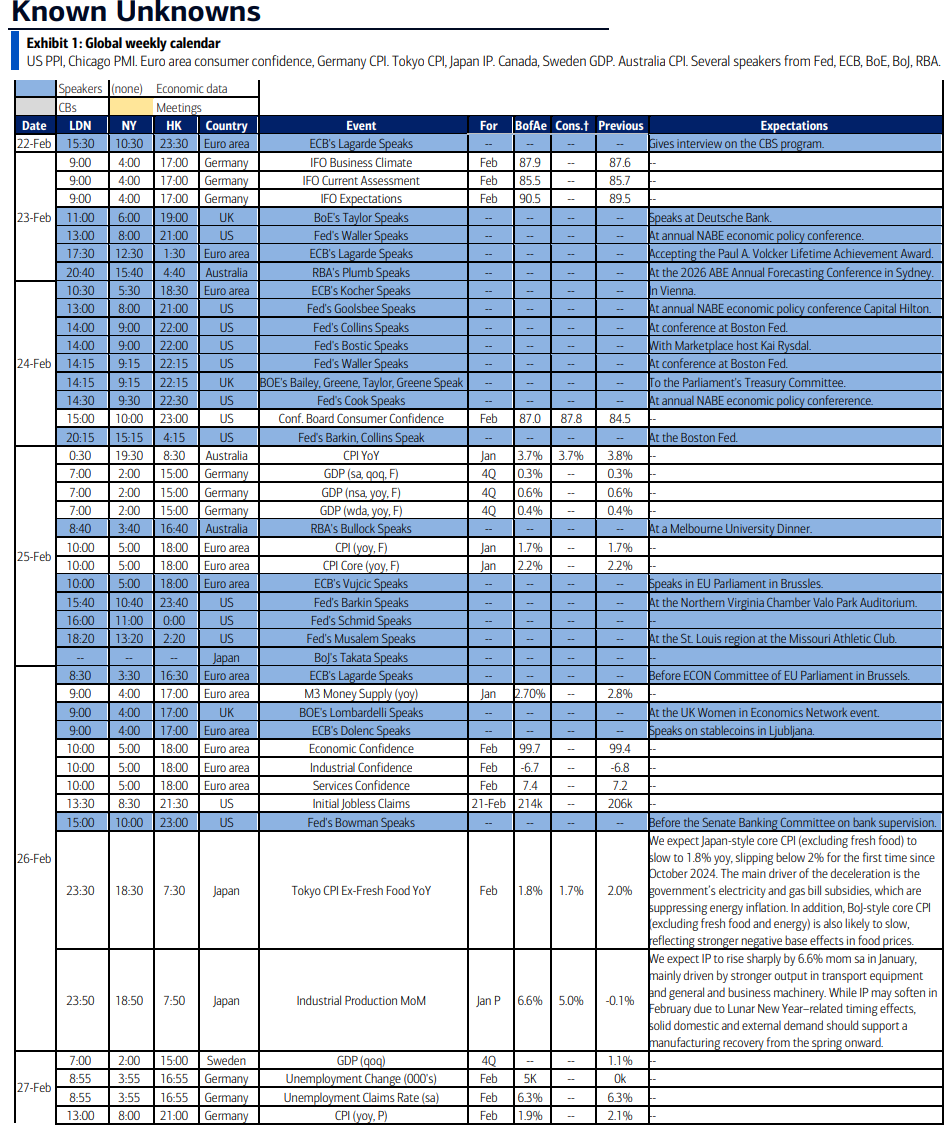

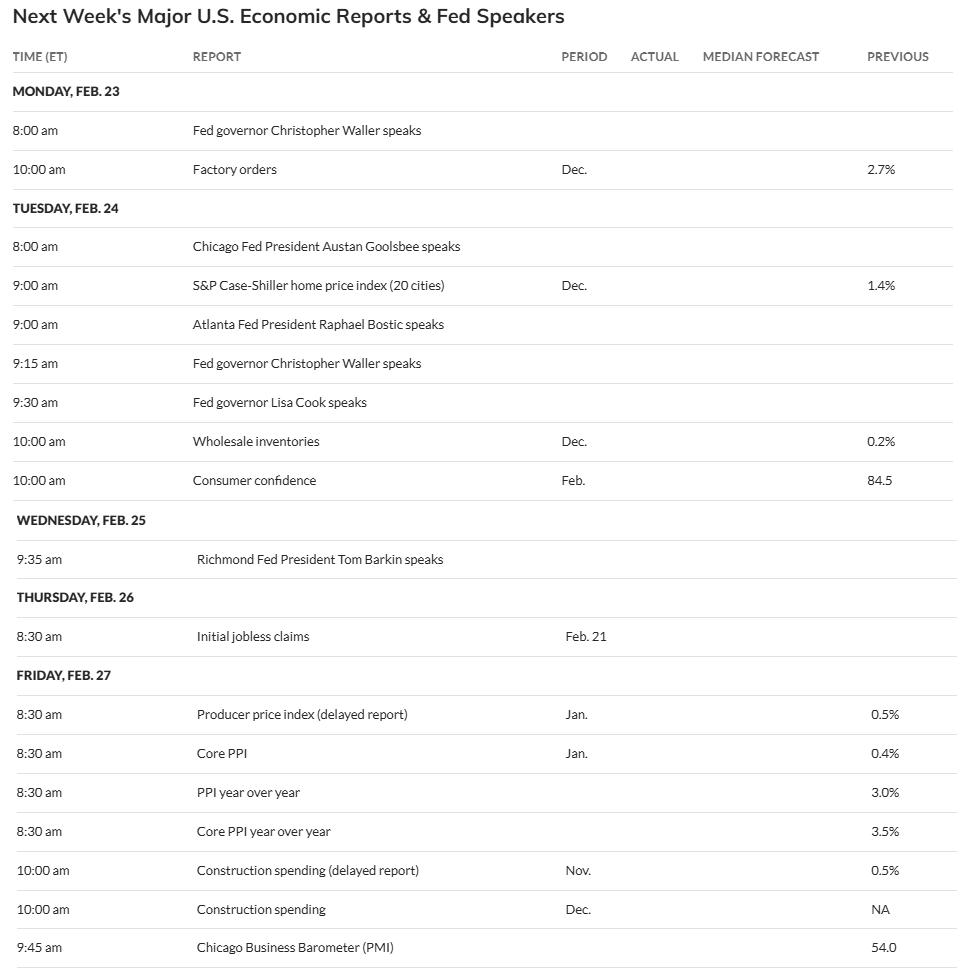

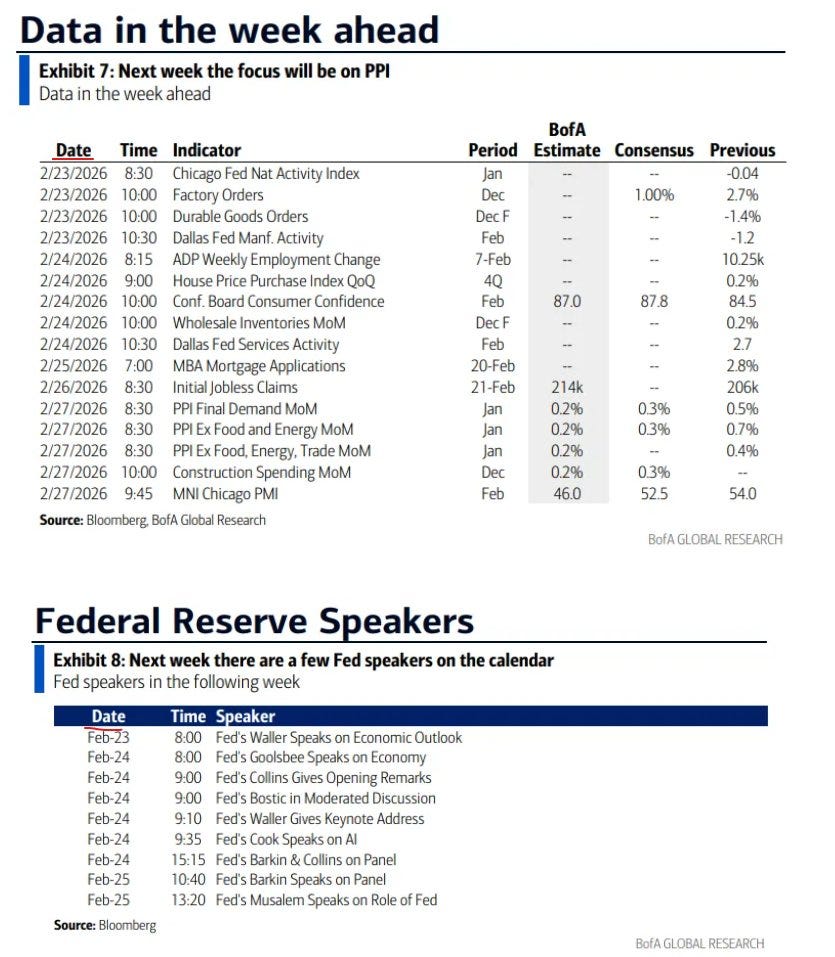

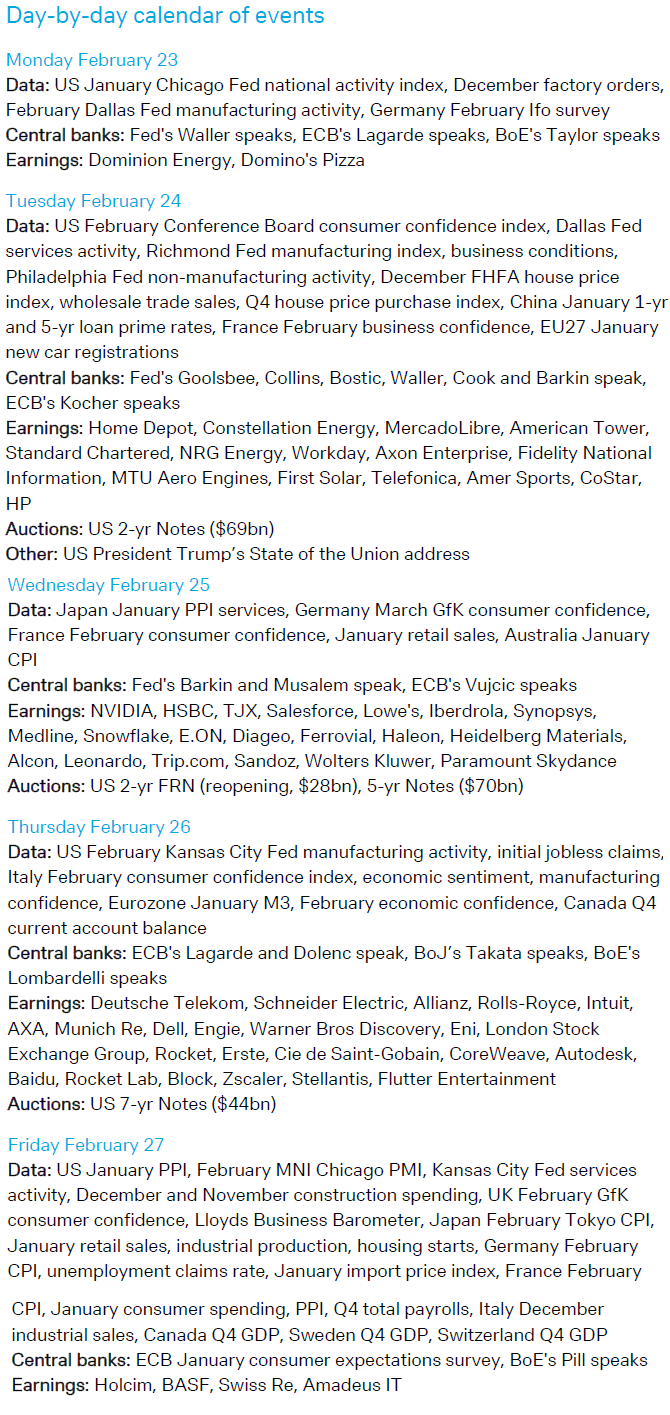

US economic data next week lighter as we close out the month. No top-tier data with Jan PPI and Chicago National Activity Index, Dec factory orders, construction spending, repeat sale home price indices, and wholesale inventories, Feb Conf Board consumer confidence, plus the weekly reports (ADP, jobless claims, etc.).

Fed speakers will continue. At this point it feels like everyone is locked in to their positions, at least until we get another round of employment and inflation data, but we’ll see if there’s any movement. On the schedule are Gov’s Waller and Cook and regional Fed Presidents Bostic (of course), Collins, Goolsbee, Musalem, and Barkin (and there are almost always more with media interviews, etc.). Out of that list, just the Gov’s are voters though.

Non-bill Treasury auctions (>1yr in duration) pick back up with 2, 5, and 7-years on Tues, Wed, Thurs respectively.

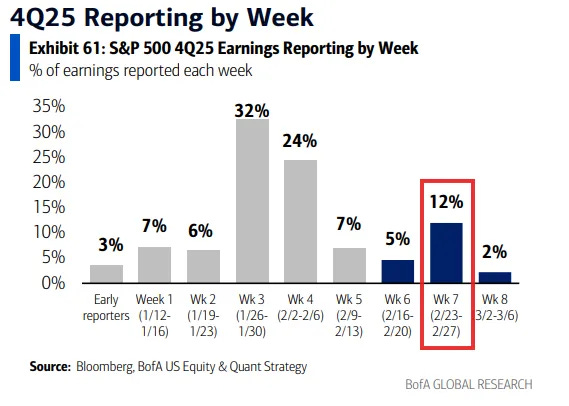

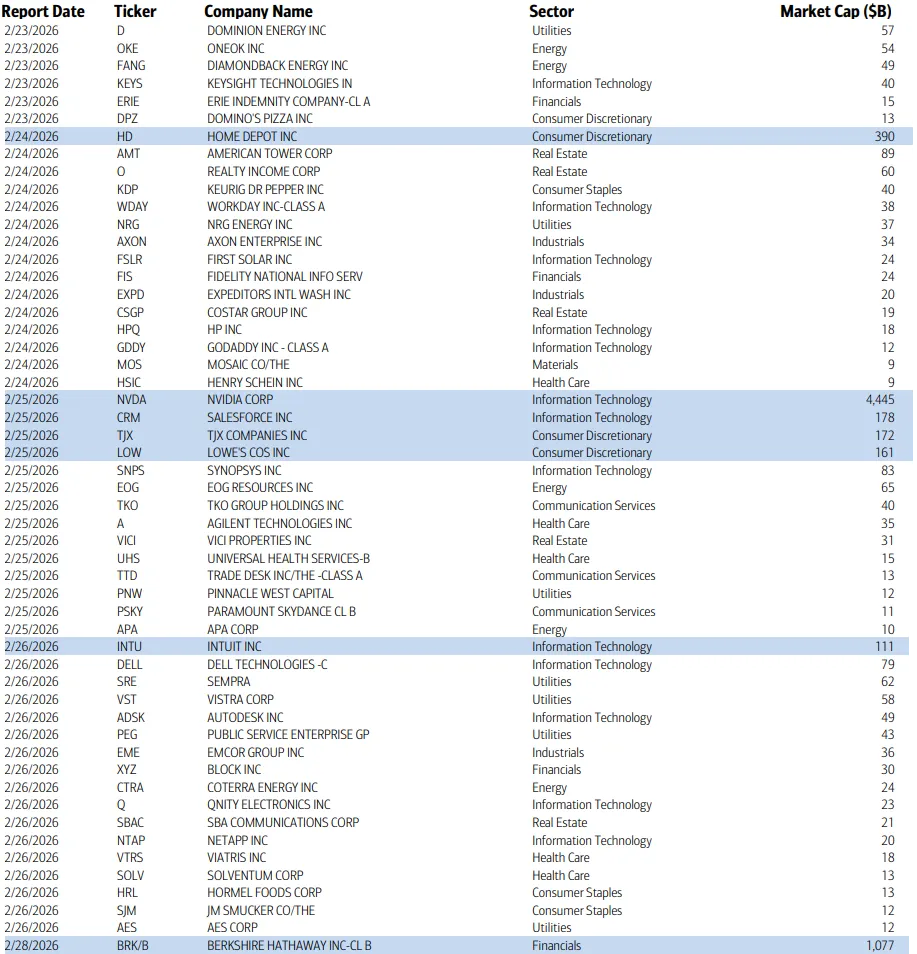

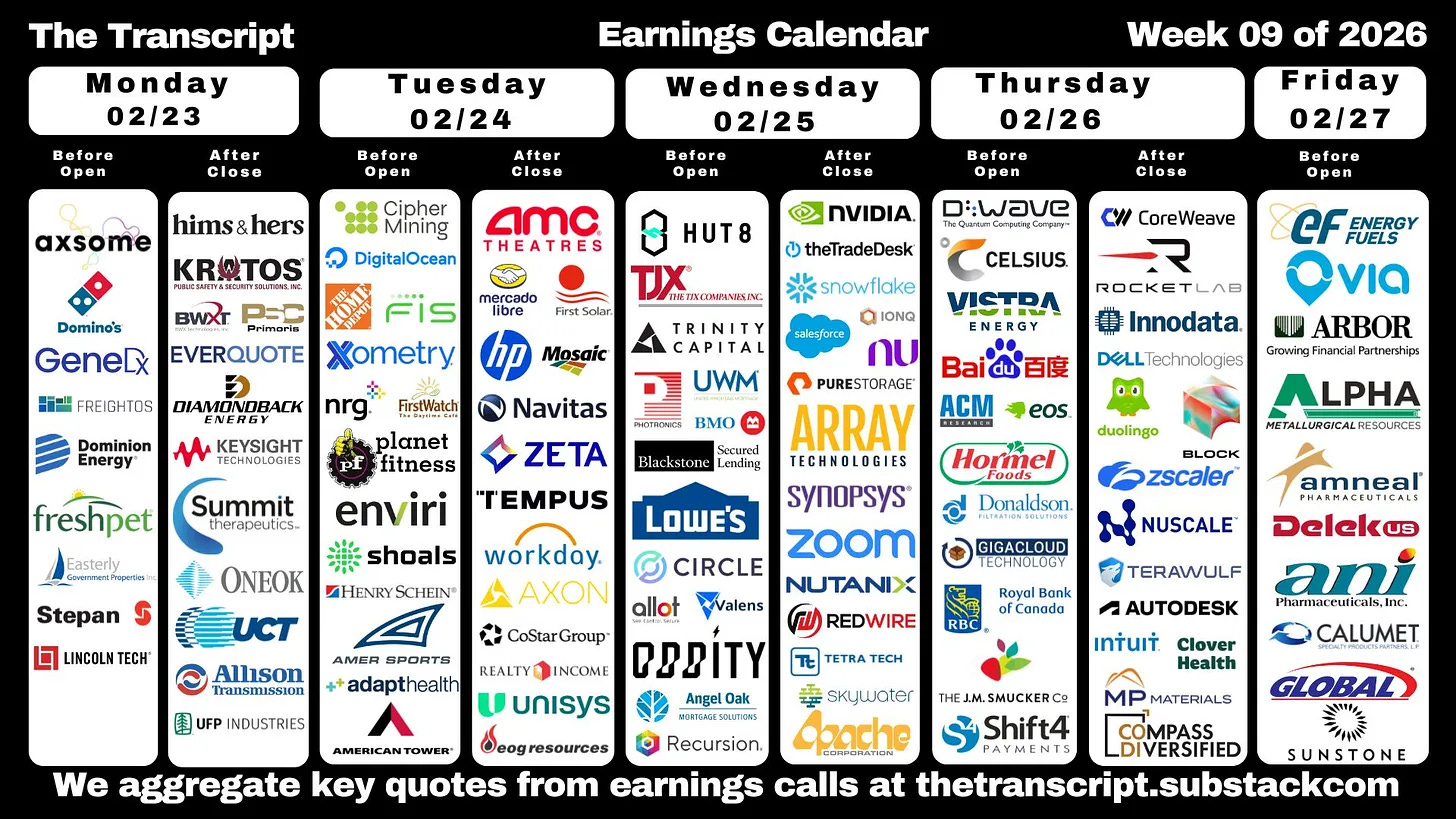

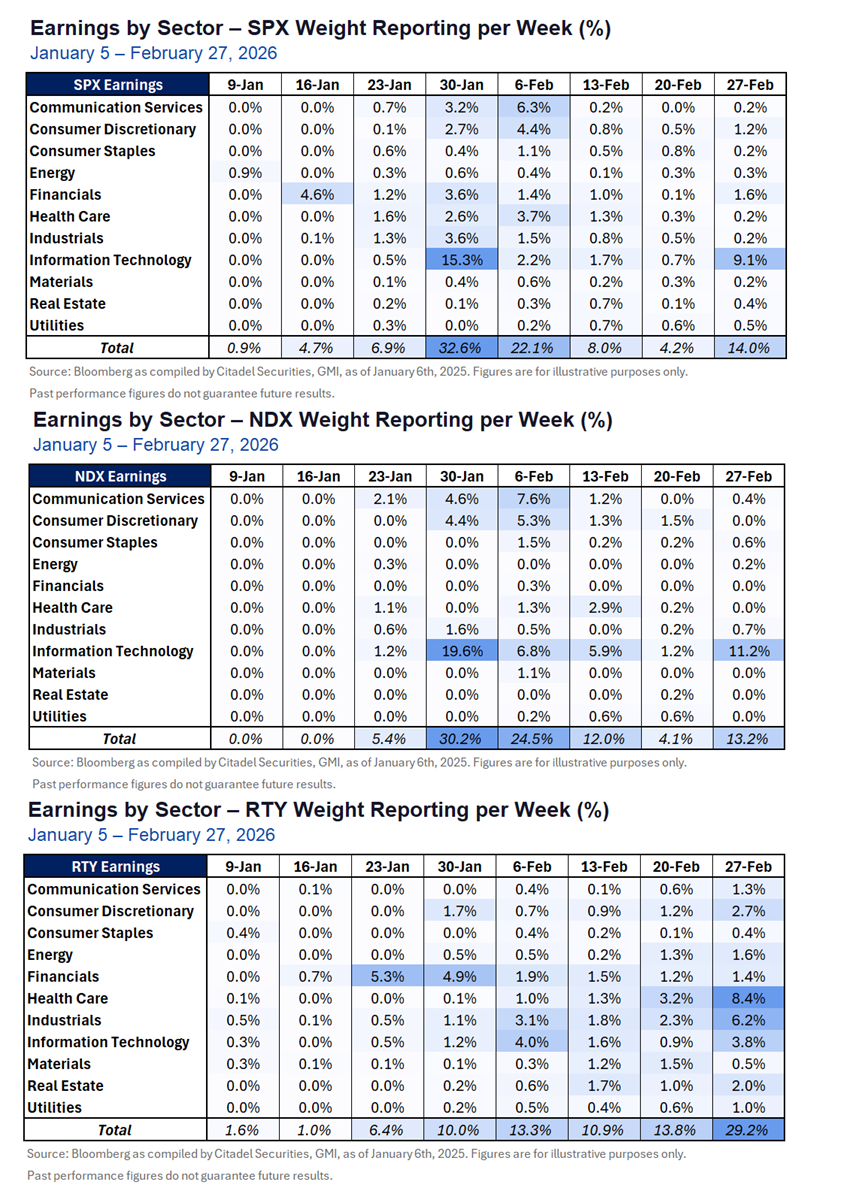

Q4 earning season also continues with ~50 SPX components but 12% of the SPX in earnings weight because we’ll get the biggest in NVDA (~$4.5tn market cap) on Wed. In addition, there’s another six >$100bn in market cap in HD, CRM, TJX, LOW, INTU, BRK/B (by reporting date - Berkshire is the 28th).

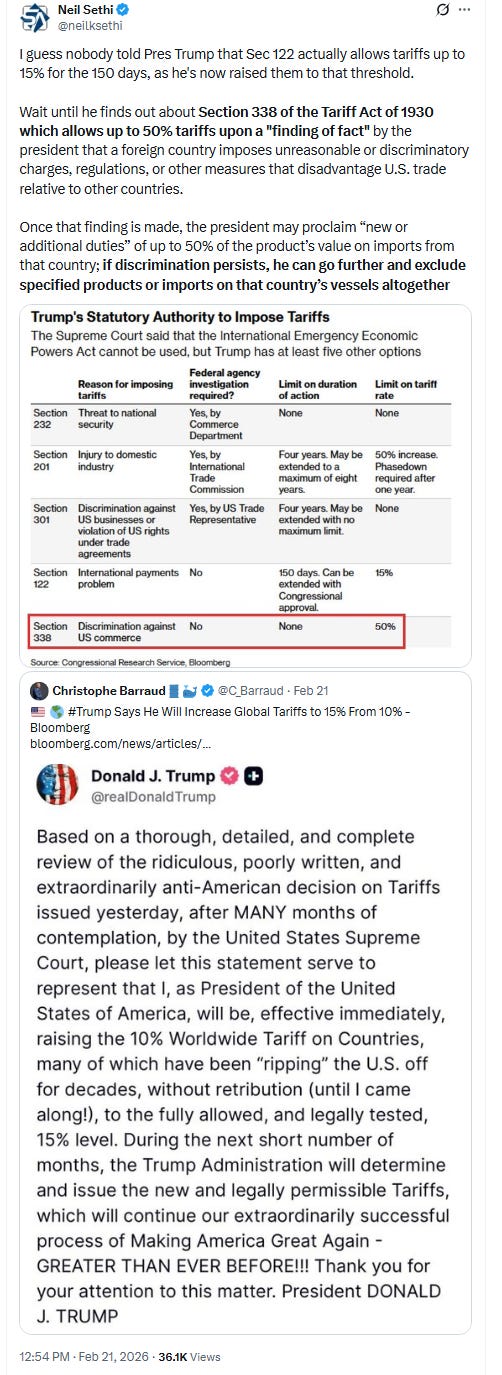

And while we did get the IEEPA decision from the Supreme Court we’re still waiting on the Lisa Cook opinion as well as one getting less attention - Louisiana v. Callais which is expected to further narrow the scope of the Voting Rights Act’s protections against racial vote dilution, which could be coming next week (in addition to other consequential decisions of course).

And that IEEPA decision has unleashed an entire new round of tariff uncertainty. While my base case is that things will end up not far off from where they were prior ot the decision, you never know with these things, and until then investors will be swung around by headlines.

We’ll also get the State of the Union address on Tuesday.

Ex-US it’s a lighter week as well in terms of scheduled events, giving trade negotiations a wide berth to take center stage. Already the EU and India said they are rethinking their previously negotiated trade arrangements.

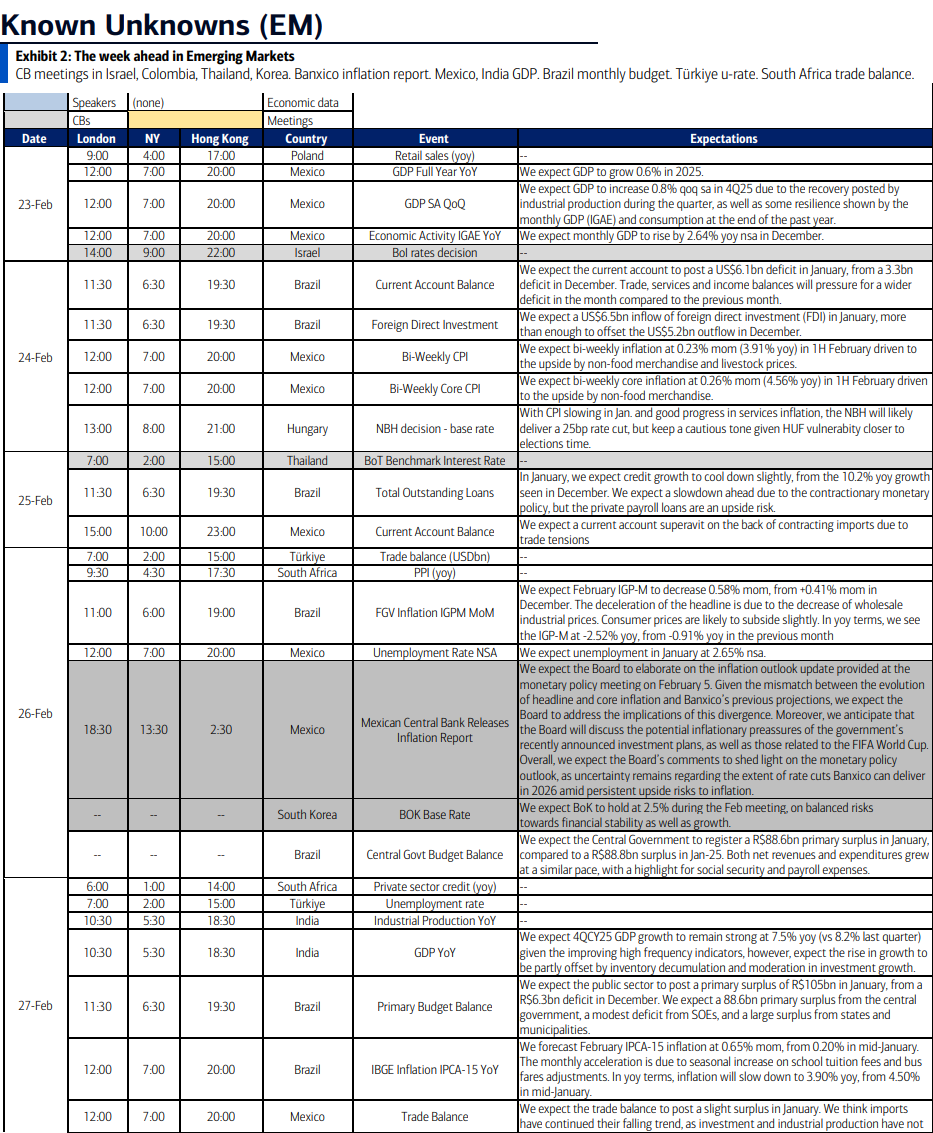

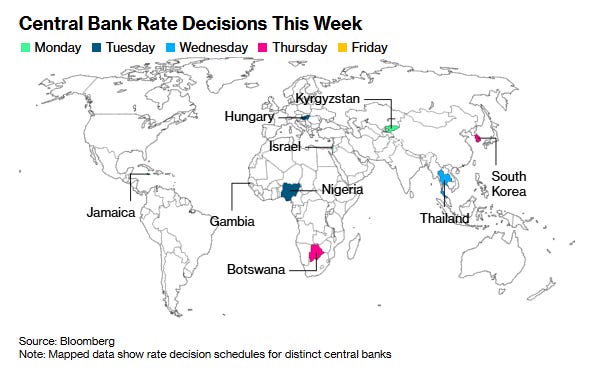

But in terms of what’s on the schedule, there are a few policy decisions highlighted by central banks in Korea and Thailand expected to keep interest rates steady, while Israel and Nigeria may cut. In terms of economic data, the focus will be on inflation with readings from the EU and Japan, as well as a number of sentiment reads.

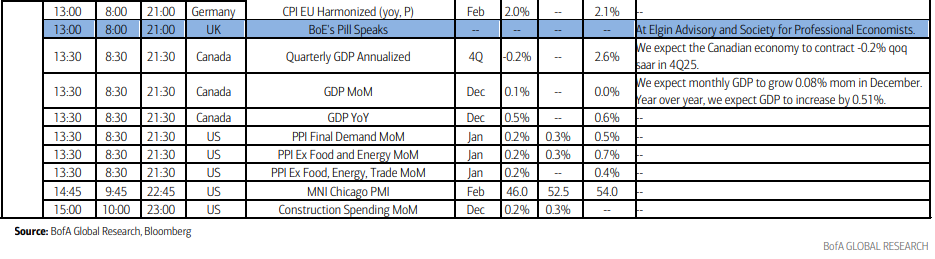

Canada

Statistics Canada will release fourth-quarter GDP by expenditure, with the Bank of Canada expecting a flat reading even as industry-based data point to a contraction. US tariffs and slowing immigration continue to weigh on growth, while higher government capital spending and modestly accommodative rates are helping to offset some of that drag.

Asia

Several inflation reports will grab the spotlight in the Asia-Pacific. Fresh off the Reserve Bank’s rate hike earlier in the month, Australia gets data Wednesday that will indicate whether elevated price gains at the end of 2025 carried over into January. On Friday, Japan’s price data for Tokyo are likely to show that the gauge excluding fresh food slid to 2% in February, the slowest pace in more than a year. Even so, the figures won’t derail the Bank of Japan from its quest to normalize policy settings with rate hikes, as the slowdown will reflect temporary effects from utility subsidies and comparison with a fast advance a year earlier. Also in the coming week, Sri Lanka publishes its Colombo CPI gauge for February, and Singapore releases January CPI data.

India publishes fourth-quarter GDP figures on Friday, with economists looking for a slight moderation of growth to 7.4% year on year after an 8.2% surge in the previous period. New Zealand releases a pair of February sentiment surveys, the ANZ Business Confidence gauge on Thursday and, a day later, the ANZ Consumer Confidence index. The latter soared to its highest reading in more than four years in January. Trade data is scheduled from Sri Lanka, Hong Kong, Thailand and the Philippines.

On the policy front, China will likely hold its 1- and 5-year loan prime rates steady on Tuesday, while Bank of Thailand officials gather a day later to debate whether to follow their December rate cut with another. With the government having upgraded its growth projections for 2026, the broad consensus is for a hold, but it’s not a unanimous position. The Bank of Korea on Thursday is expected to hold its base rate steady after essentially ending its easing cycle in recent months, with the focus falling on any hints about the policy trajectory in 2026.

Europe, Middle East, Africa

Germany, France and Spain will release preliminary inflation data for February, with Bloomberg Economics seeing energy and food prices as the main drivers. Those numbers — due at the end of the week — come after the final reading for the euro area, which will shed light on what pushed the services measure lower in January. A few ECB speakers are set to appear. Lagarde kicked off things on Sunday, telling CBS’s Face the Nation that the repercussions from the US Supreme Court’s tariff ruling could create new business disruptions. She speaks next at an award ceremony in Washington on Monday, and faces lawmaker scrutiny in the ECON Committee of EU Parliament in Brussels on Thursday.

Lagarde’s future vice president, Croatia’s Boris Vujcic, will be in front of that same committee a day earlier as part of the formal process to assume his new role in June. Governing Council members Martin Kocher and Primoz Dolenc are also are scheduled to speak and the ECB’s full-year results and its survey of consumers’ inflation expectations are due toward the end of the week.

In the UK, Bank of England Governor Andrew Bailey gives evidence on the latest Monetary Policy Report to a parliamentary committee on Tuesday, joined by colleagues Huw Pill, Megan Greene and Alan Taylor. On the fiscal front, South African Finance Minister Enoch Godongwana presents his annual budget on Wednesday, a speech to be closely watched by investors for signs the government remains committed to repairing public finances. After years of strain, the budget is expected to showcase progress on fiscal consolidation, supported by stronger revenue collection and a narrower deficit.

Several rate decisions are due in the region: On Monday, Israel’s central bank is expected to cut its benchmark by 25 basis points to 3.75%, as the shekel’s appreciation and a slowdown in annual inflation to 1.8% — below the midpoint of the 1%–3% target range — ease pressure on policymakers. Still, officials have sent mixed signals: Governor Amir Yaron said last month the bank would remain cautious on easing, while Finance Minister Bezalel Smotrich has stepped up calls for rate cuts. A day later, Hungary decides whether to begin a long-awaited cutting cycle that would come less than two months before a closely-watched general election. The same day, Nigerian policymakers are set to resume their easing cycle after inflation unexpectedly slowed in January. The central bank will likely lower its key rate by 100 basis points to 26%. On Thursday, Botswana is likely to leave the policy rate unchanged at 3.5% as inflation continues to accelerate.

Latin America

Mexico kicks off a busy and telling week on Monday with final fourth-quarter output figures. While the flash readings posted last month were better than expected, they also portrayed an economy operating below its potential. Mid-month consumer price readings on Tuesday may offer Mexican policymakers little reason to resume easing at their meeting next month, while Banxico’s quarterly inflation report is likely to sound a bit less dovish and a bit more cautious than its prior assessment in November.Trump’s musings about pulling the US out of the USMCA trade deal sound to most observers like a negotiating tactic, but still add layers of risk and uncertainty to Mexico’s outlook.

Brazil will serve up a welter of economic reports — current account, foreign direct investment, lending, the broad-based IGP-M inflation index and the mid-month IPCA inflation reading, along with budget balances. While the debt metrics bear watching — the year-end fiscal deficit has exceeded 8% in all three years of President Luiz Inacio Lula da Silva’s third term — the cooling of LatAm’s No. 1 economy suggests consumer price data will greenlight at least a quarter-point rate cut by the central bank next month.

December GDP-proxy figures from Argentina, especially if they suggest a continuation of November’s stall speed, may animate concerns over stagflation with consumer confidence running at a four-month low. Peru, whose economy continues to power through the political chaos of having had five presidents in five years, is slated to post fourth-quarter and 2025 output. Based on the December GDP-proxy report published mid-month, annual GDP should come in at about 3.4% with a 0.5% quarter-on-quarter expansion. Chile-watchers can look forward to the usual end-of-month data dump, featuring seven separate economic reports for January, with the highlight being monthly copper production — the red metal is the South American nation’s top export.

DB one pager:

BoA’s cheat sheets: