The Week Ahead - 3/15/26

A comprehensive look at the upcoming week for US economics, equities and fixed income (including earnings, the Fed, valuations, positioning, breadth, sentiment, and seasonality)

If you're a new reader or maybe one who doesn’t make it to the end feel free to take a second to subscribe now.

Or take a moment to invite others who might be interested to check it out (it’s appreciated!).

Please note that I do sometimes add to or tweak items after first publishing, so it’s usually safest to read it from the website where it will have any updates.

As a reminder, some things I leave in from prior weeks for reference purposes, because it’s in-between updates, it provides background information, etc.. Anything not updated this week is in italics. As always apologize for typos, errors, etc., as there’s a lot here, and I don’t really have time to do a thorough double-check.

For new subscribers, this is a relatively long post. The intent is to cover the same areas each week. Sometimes the various areas are more interesting, sometimes less, but it’s easier just to go through them all, so you can expect this format (with things in the same places) each week.

The main sections are intended to cover 1) what’s upcoming next week, 2) what the Fed and rates markets are up to, 3) what’s going on with earnings (the most important determinate to stock prices over the long term (along with valuations (the price paid for those earnings))), 4) what’s going on with the economy (both because of its impact on our daily lives but also because it impacts earnings), 5) valuations (for the reason noted), 6) breadth (which gets into sector/style performance), 7) positioning/flows (this is the largest determinant to equity price changes in the short term), 8) sentiment (really only matters at extremes but interesting to track), 9) seasonality (gives you an idea of what normally happens), 10) “Final Thoughts” and 11) my portfolio (to be transparent about where my money is in the market (but note first it is most definitely not intended as financial advice, and second my portfolio is invested with the intention of wealth building not daily income, etc., so my portfolio is built with that in mind (plus see note about MLP’s in that section)).

A continued thank you to the many who have contributed to the charity fund. I appreciate very much each paid membership, and I have tried to respond to all messages from paid members. If you have sent me a message, and I have not responded, please don’t hesitate to send a new message, as it likely was just buried in my email inbox.

Also, a few readers mentioned that the volume of material can feel like a lot to get through. That’s understandable, especially as different readers find value from different parts of the subscription. But everything I publish is meant to stand on its own (often even each section), so please feel free to read whatever is most useful and skip the rest.

I have this week also continued to remove some things to try to clean up the flow. If I remove something that you would like in, just let me know, and I’ll see what I can do. As always, feedback is welcome.

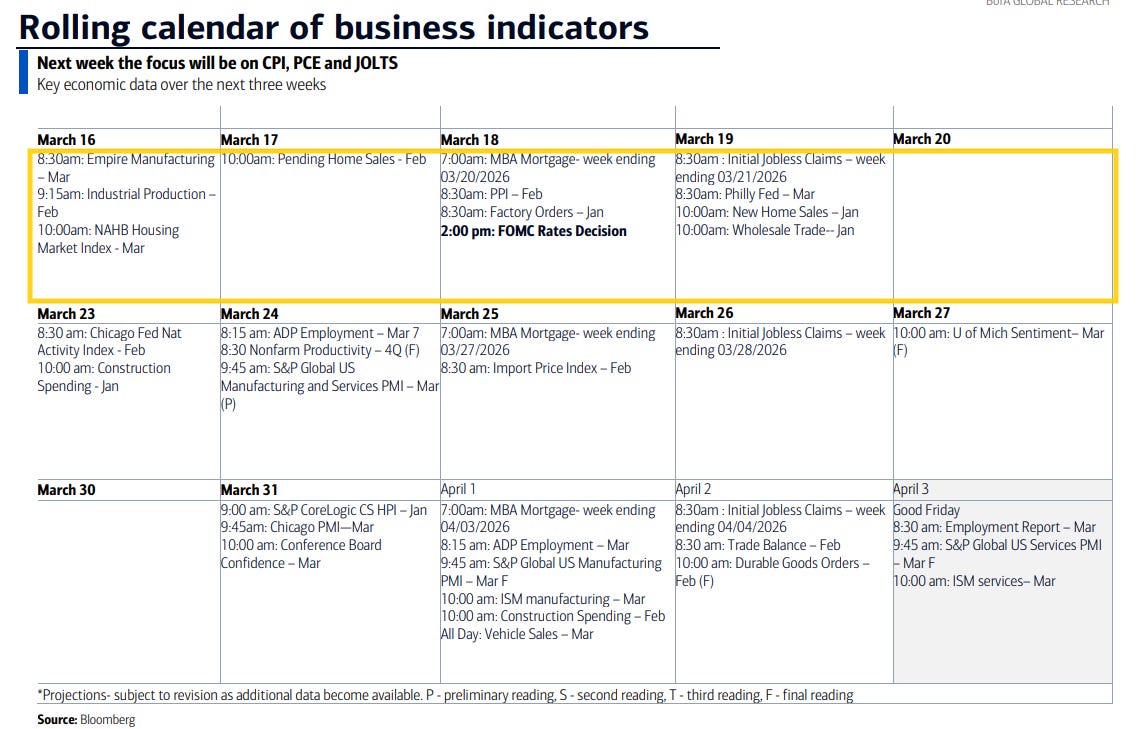

The Week Ahead

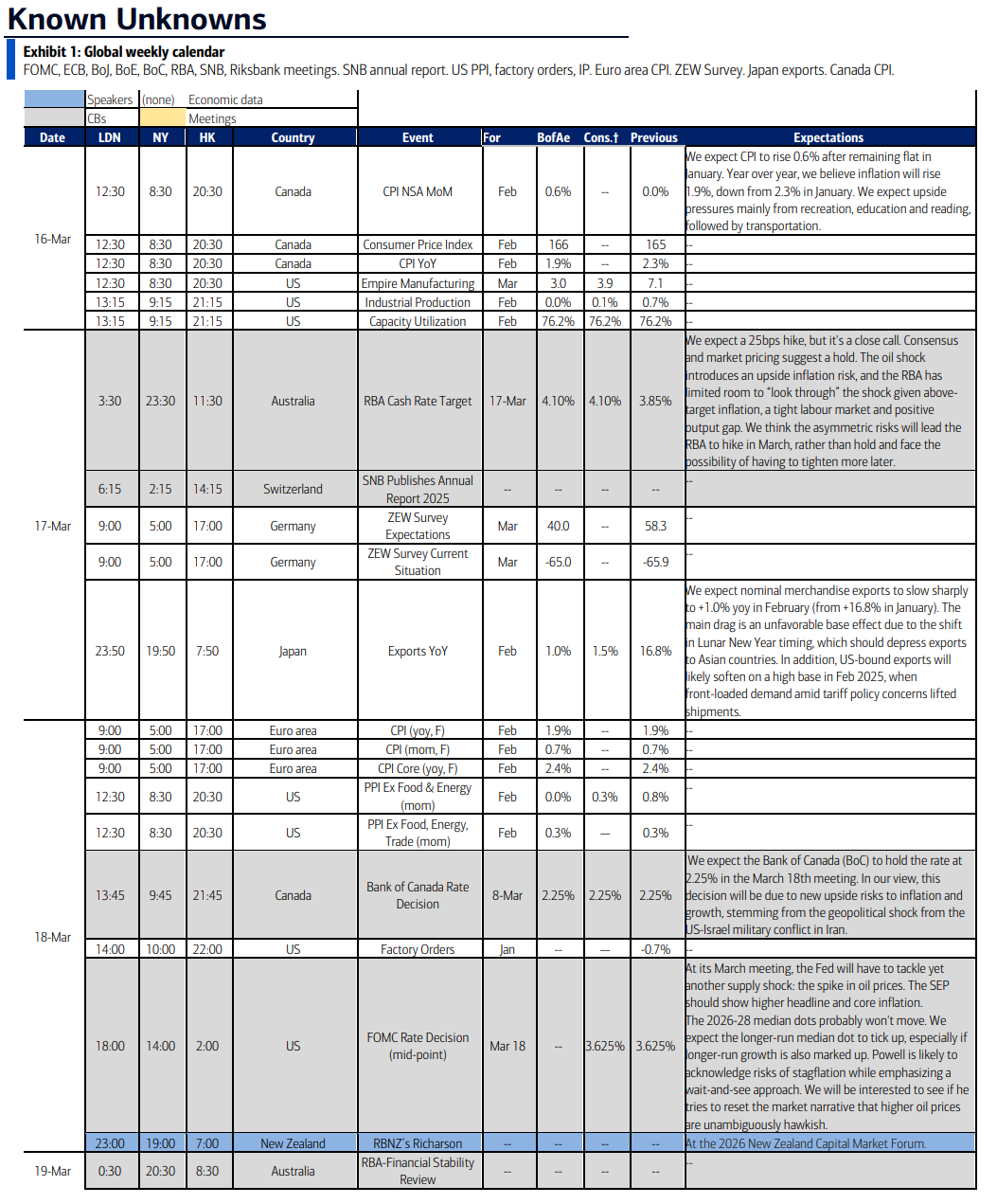

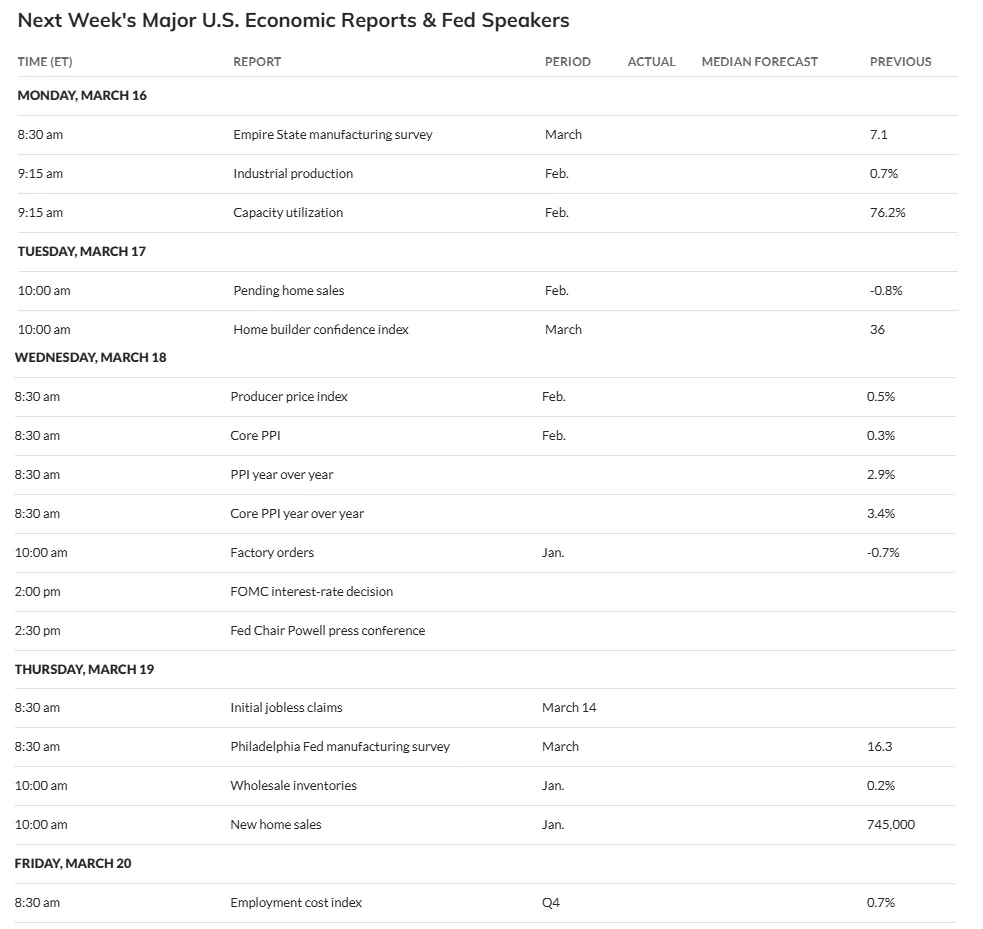

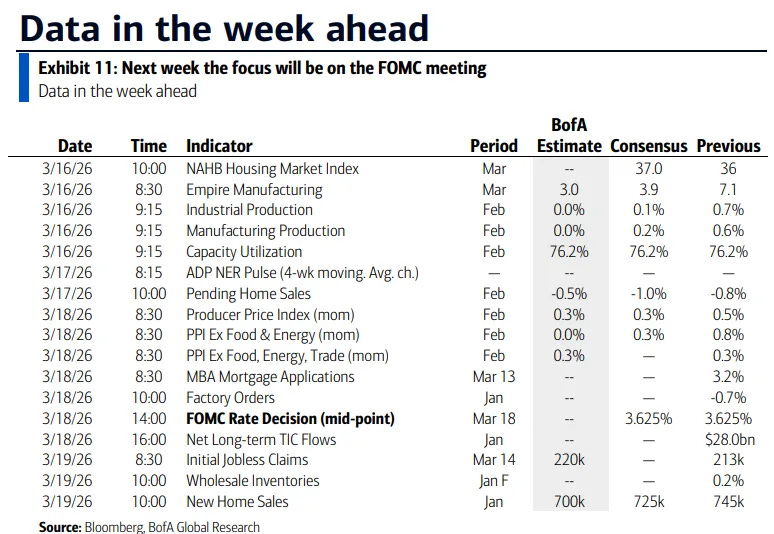

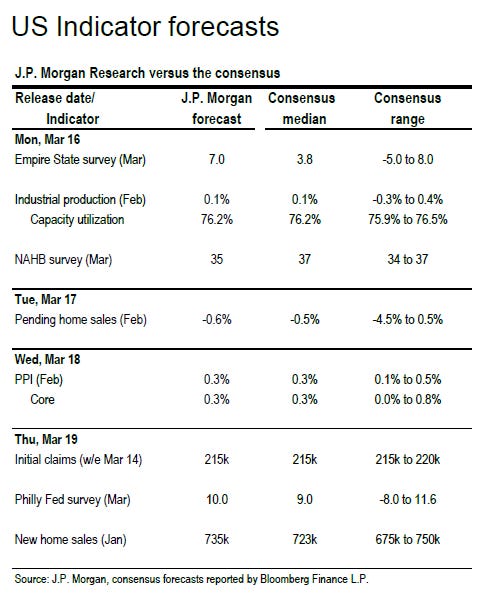

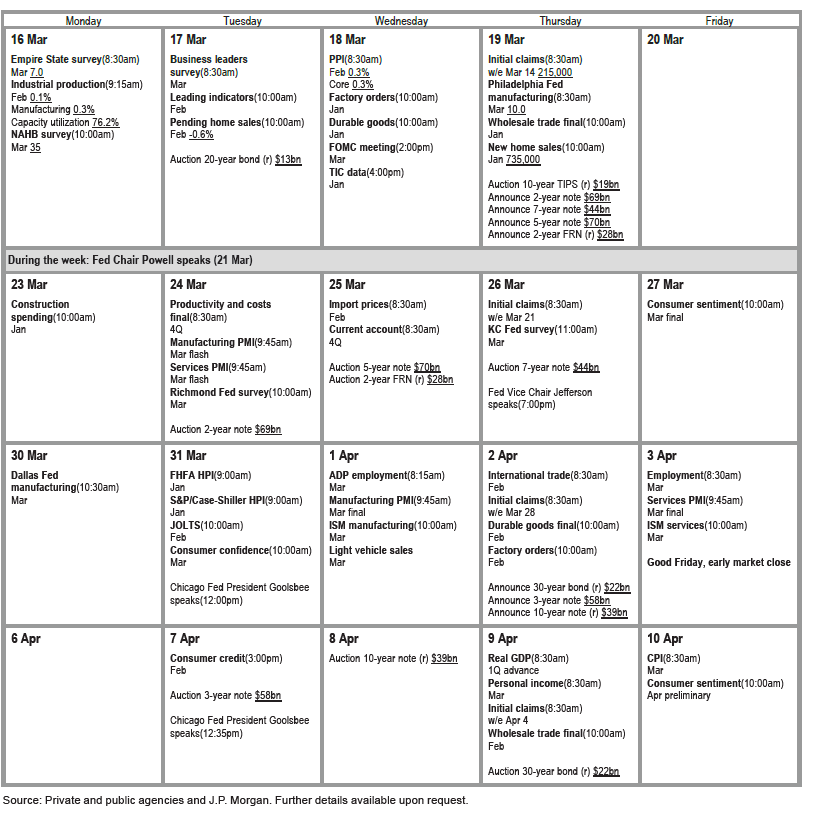

US economic data lightens somewhat next week, but we’ll still get a number of important reports highlighted by Feb industrial production (our best and broadest look at the manufacturing sector) and PPI (an important factor in PCE prices (which is our best look at economy-wide inflation)), plus pending home sales (contract signings so more forward looking), the Q4 employment cost index (the Fed’s favorite wages metric), Jan factory orders and new home sales, and March NAHB homebuilder confidence in addition to the weekly reports (ADP, jobless claims, etc.).

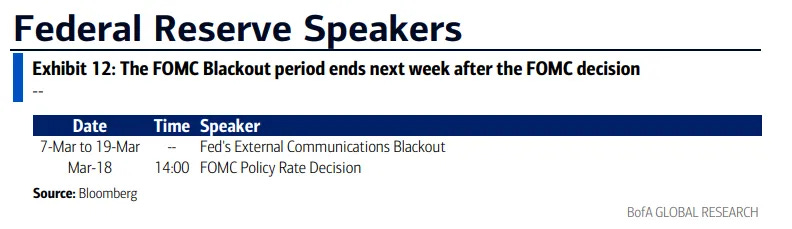

The highlight though will be the March FOMC meeting even as there is almost no chance of anything but a hold. Still it will be interesting to see how the Fed is thinking about the Iran situation, and, more importantly, we’ll get updated economic projections and dot plot.

Non-bill Treasury auctions (>1yr in duration) are light with just a 20-yr reopening (a duration which the Treasury is actively looking to phase out due to low liquidity so don’t read anything into it) and a 10-yr TIPS reopening (you can read even less into that).

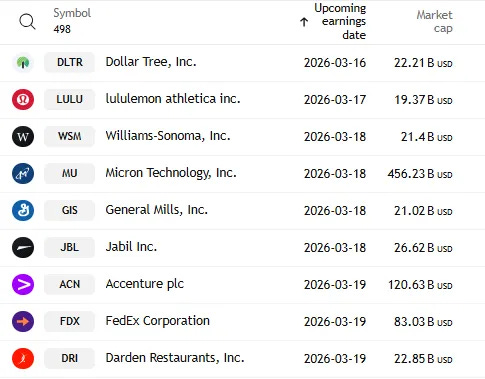

Q4 earnings season continues to wind down with 9 SPX component reporting, two >$100bn in market cap in MU and ACN. More importantly (for markets) next week is the NVIDIA GTC 2026 global AI conference March 16–19, in San Jose, California. CEO Jensen Huang will deliver the opening keynote, which is expected to outline the future of NVIDIA’s AI and GPU roadmap.

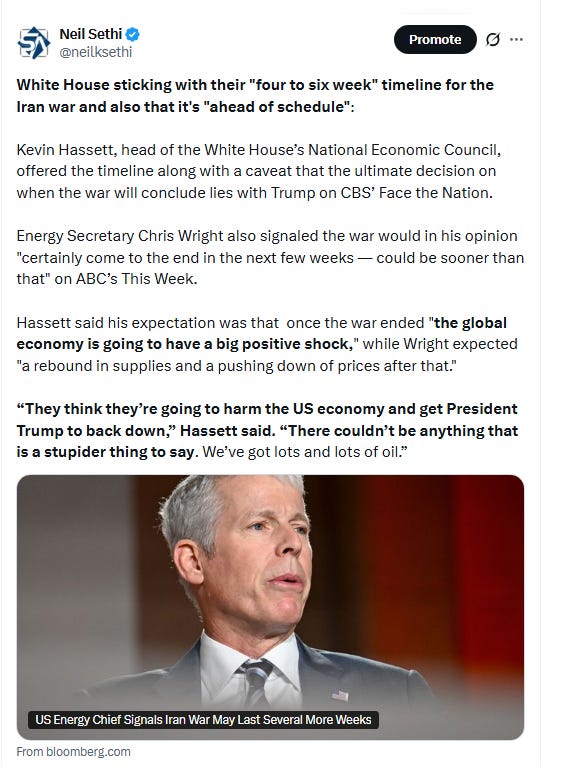

Of course overshadowing most all of that will continue to be what’s going on with Iran. As of now I continue to believe, as I have since it began, the duration of this conflict will end up being measured in weeks not months (if only to get energy and other prices (it’s feeding into food prices, etc.) back down and otherwise assuage his base, which is not thrilled about foreign entanglements, ahead of the mid-terms), but as I noted last week “I have to respect that consensus (if Polymarket can be considered consensus) is that this will stretch out past March with just a 13% chance of it ending this month and 36% by the end of April.”

So while on the one hand I do think it will be “weeks,” on the other as it seems there will be no “popular uprising,” the administration has not been able to get anywhere with the current leadership, and there doesn’t appear any desire to send in sufficient ground troops to force a leadership change, so it does seem the conflict will likely extend into April (which also allows Pres Trump to use it as leverage in his meeting with Pres Xi at the end of the month). I still have a hard time believing this goes past April, but quite honestly the whole thing has surprised me thus far. FWIW, administration officials were on the Sunday Shows expressing a likely late March/early April resolution (see post below).

And while we did get the IEEPA decision from the Supreme Court we’re still waiting on the Lisa Cook opinion which we’ll get at some point. And that IEEPA decision has unleashed an entire new round of tariff uncertainty, which will continue, if in the background. While my base case has been that things will end up not far off from where they were prior to the decision, you never know with these things although it does seem that markets have settled into this “new normal”.

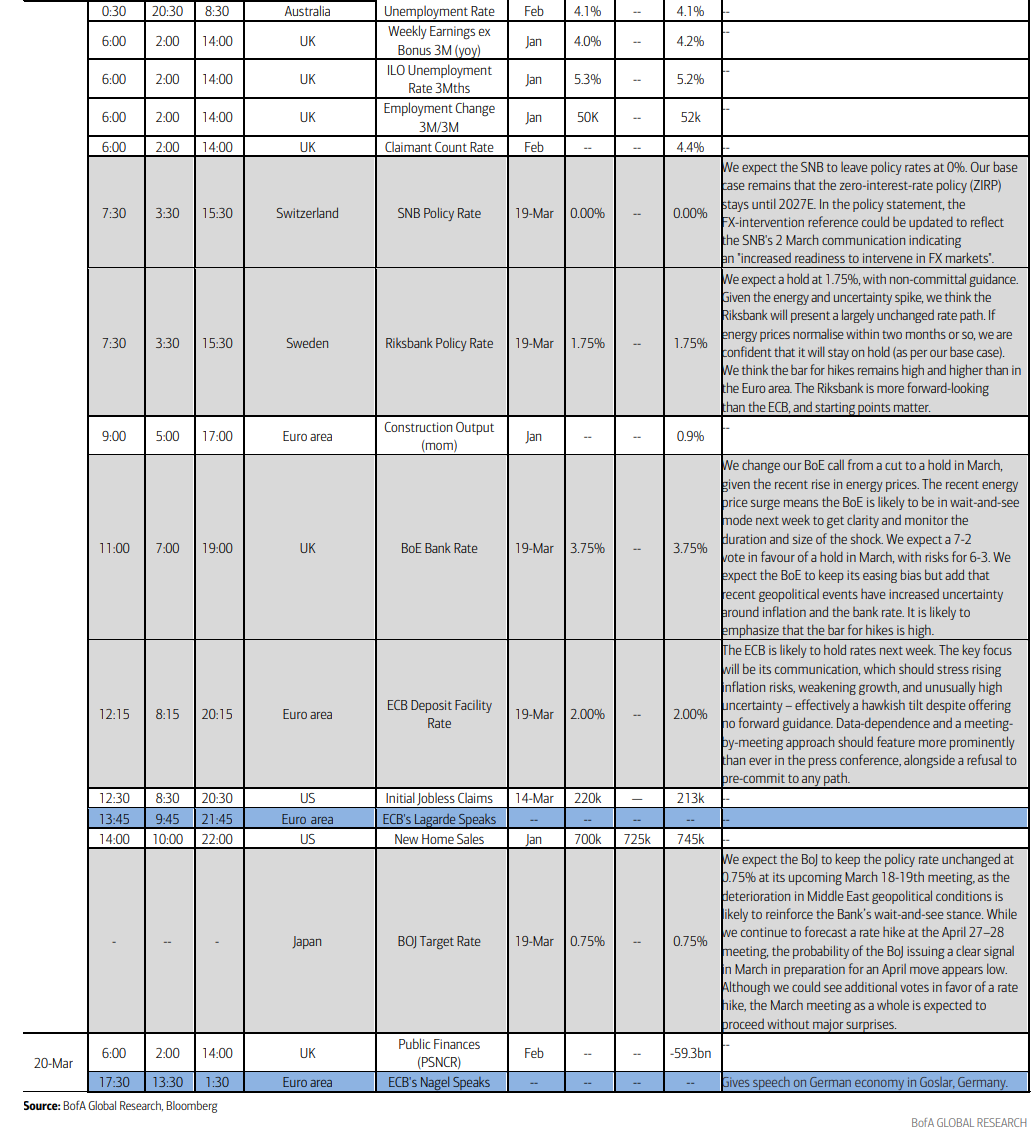

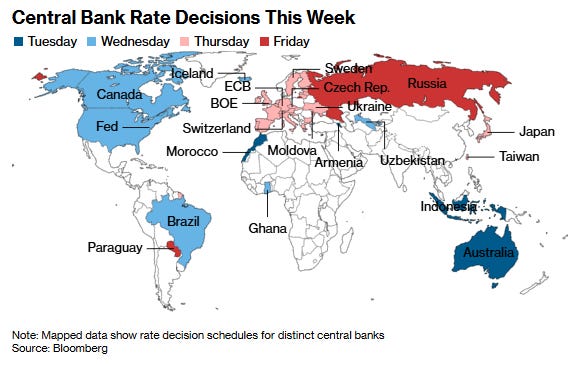

Ex-US it’s also a central bank dominated week with every member of the G-7 and eight of the world’s 10 most-traded currency jurisdictions with policy decisions this week. Otherwise, we’ll get Germany’s ZEW survey, UK labor market data, China’s monthly roundup of economic activity, Japan exports, Canada CPI, and a meeting between leaders of the US and Japan on Thursday in Washington.

Bank of Japan

The BOJ is widely expected to hold its benchmark rate steady on Thursday, while assuring markets that it remains on the path toward policy normalization. Governor Kazuo Ueda is likely to emphasize the need to closely monitor developments given the country’s heavy reliance on oil imports from the Middle East. While sustained high crude prices could hurt Japan’s economy, they would also add to inflationary pressures. Policymakers must additionally assess the risk of further weakening the yen if they strike an overly dovish tone. The currency on Friday slid to its lowest level against the dollar since 2024.

Bank of England

A decision that appeared just last month to be tilted “50-50” toward a potential cut, according to Governor Andrew Bailey, is now highly likely to favor unchanged rates on Thursday. Economists at ING and RSM UK reckon that inflation could rebound to more than double the central bank’s 2% target if the recent jump in oil and gas costs proves enduring. . Data on Friday showed the UK economy unexpectedly failed to expand in January, threatening to undershoot the BOE’s first-quarter forecast for gross domestic product to rise 0.3%.

Bank of Canada

Inflation data for February released two days before the Bank of Canada decision on Wednesday will provide policymakers with an important read on price pressures before the Middle East conflict pushed oil prices higher. Also on their minds will be Friday’s data that showed the economy lost more jobs during February than in any month over the past four years. With headline inflation hovering near the central bank’s 2% target, markets expect policymakers to hold their policy rate at 2.25% on Wednesday, while watching Governor Tiff Macklem’s news conference for signals on how the Iran crisis may affect the outlook.

Swiss National Bank

The central bank’s resolve to cap gains that pushed the franc to decade highs against the euro will draw close scrutiny at its first quarterly decision of the year on Thursday, after Swiss policymakers broke their usual silence to reveal increased willingness for intervention.

While any change in language on foreign exchange will be notable, economists are unanimous in predicting the rate will stay at zero, meaning that they judge the present juncture won’t warrant the more drastic and economically harmful option of a return to negative borrowing costs.

Riksbank

The Swedish central bank is widely expected to leave its benchmark unchanged at 1.75% on Thursday, in line with previous signals, as the economy continues to strengthen at the same time as inflation ebbs below the 2% target.

Reserve Bank of Australia

Australian policymakers on Tuesday are due to set the cash rate, currently at 3.85%, with markets pricing a solid chance of a second consecutive increase. The RBA last month became the first major developed-market central bank this year to lift borrowing costs, citing stubborn price pressures and excess demand in a supply-constrained economy. Since then, data have reinforced the picture of resilience, while the Iran war has heightened concerns about domestic price pressures.

Brazil

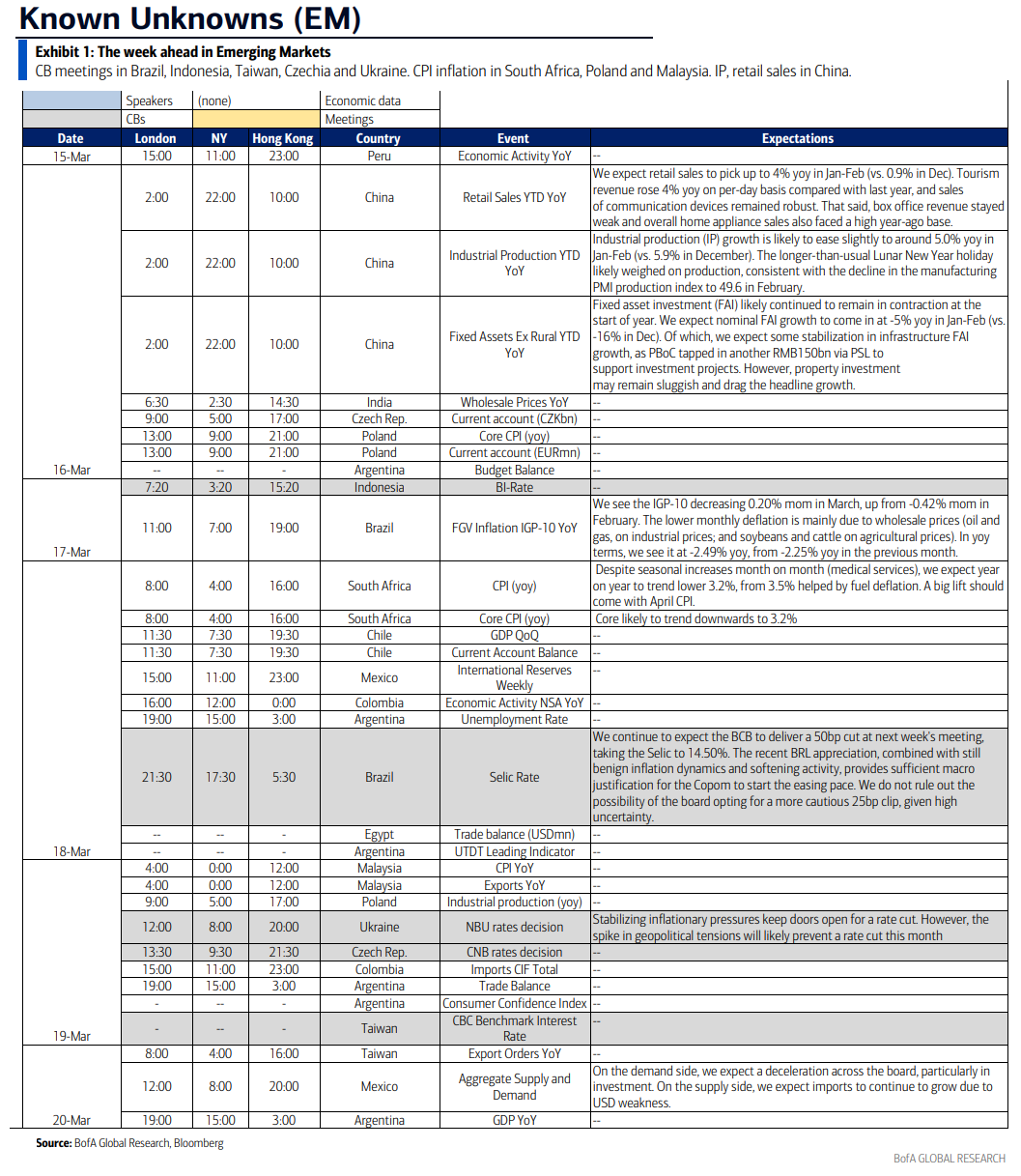

Until the war in Iran broke out, Brazil’s central bank had been all but certain to begin an easing campaign: policymakers in January signaled that a March cut was their base case, while disinflation and lower expectations gave them more than a little room for maneuver. Now, rather than the half-point cut that many analysts had anticipated, the consensus now expects a quarter-point reduction, and some Brazil-watchers can also see the cautious board giving some consideration to holding yet again at 15%.

Bank Indonesia

The central bank in Jakarta is widely expected to keep its rate steady at 4.75% on Tuesday, a decision that will force officials to balance rupiah stability against renewed worries about consumer prices. While fuel subsidies will probably cushion faster inflation, such measures risk bloating the deficit amid heightened fiscal concerns. That could spur more capital outflows and undermine officials’ efforts to maintain a stable currency.

Russia

Bank of Russia officials on Friday will weigh whether an uptick in inflation after an increase in the value-added-tax rate is easing sufficiently to allow a seventh straight cut in its key interest rate. Policymakers shaved 50 basis points off the rate at each of the past three meetings. Their decision will take place just before consumer-price data for February are due.

DB one pager:

BoA’s cheat sheets: